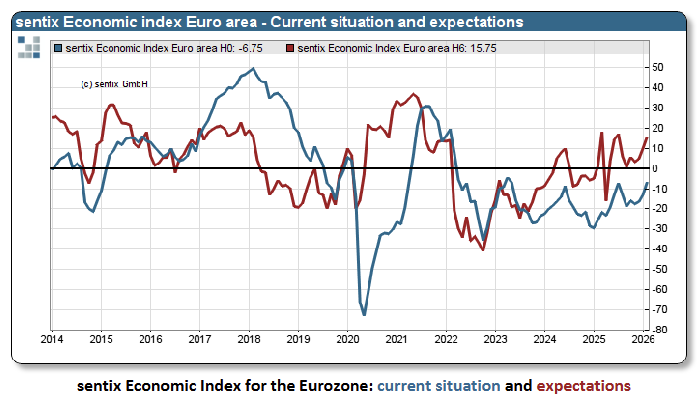

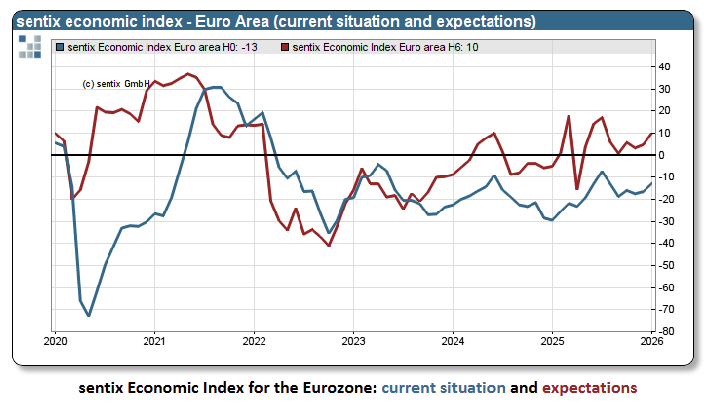

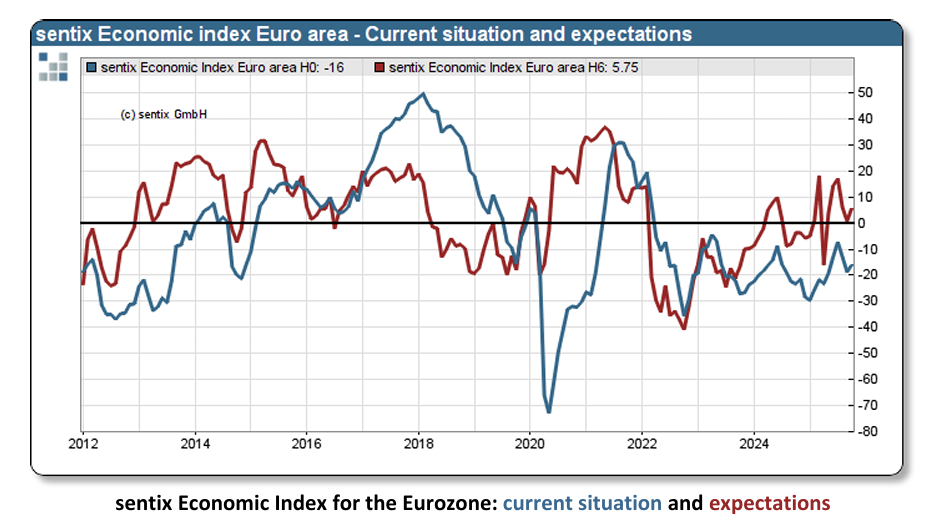

Sentix Economic Indexes

Sentix Economic Indexes

- Source

- Sentix

- Source Link

- https://www.sentix.de/

- Frequency

- Monthly

- Next Release(s)

- May 4th, 2026 4:30 AM

Latest Updates

-

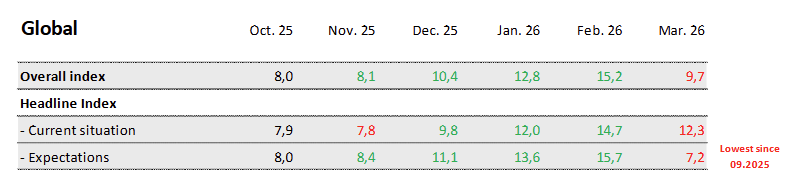

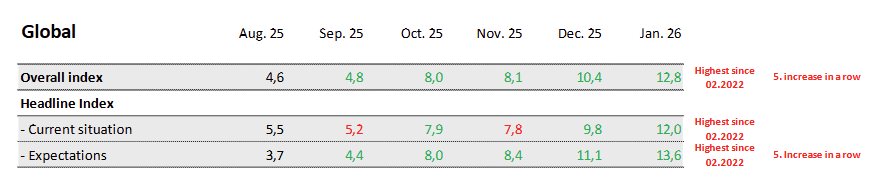

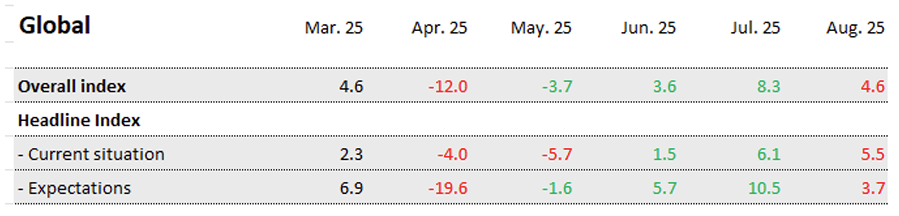

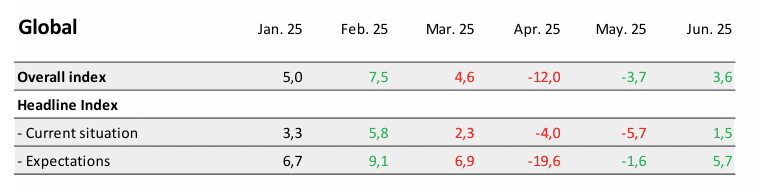

The Sentix Global Economic Index fell -5.5 pts MoM to +9.7 in March 2026, with expectations dropping to 7.2 (lowest since September 2025), signaling a broad deterioration in global investor sentiment.

-

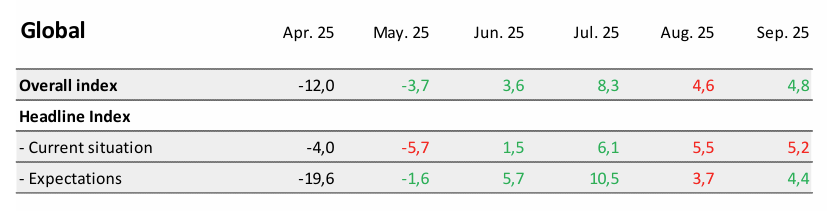

Globally, the overall Sentix index declined to +9.7 (-5.5 pts MoM) after prior gains, while the current situation index eased to 12.3 (Feb: 14.7) and expectations fell sharply to 7.2, highlighting a broad weakening in global economic outlook assessments.

-

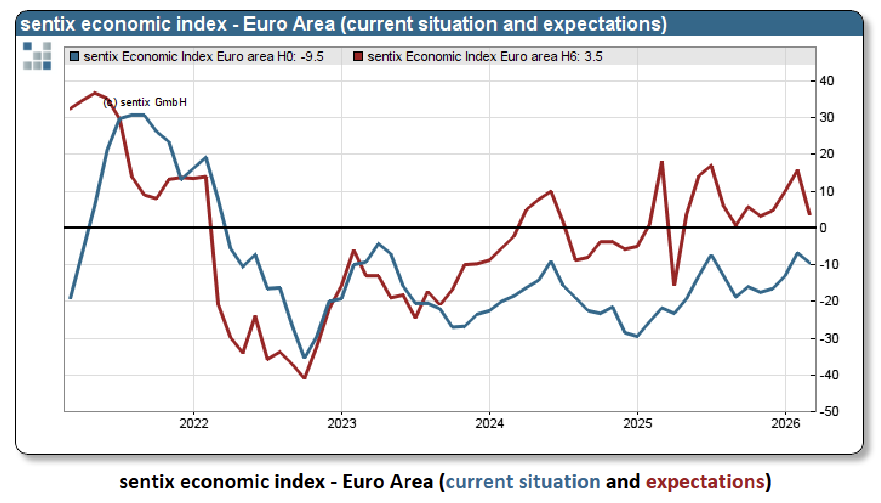

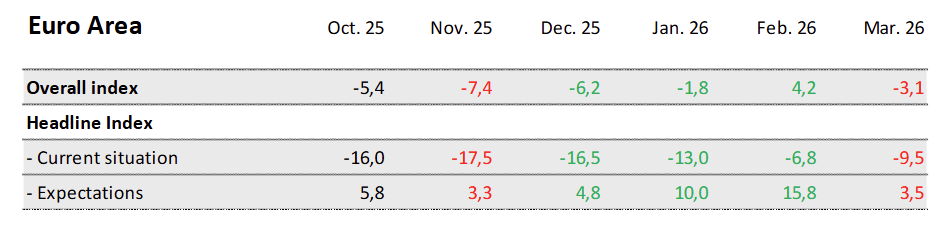

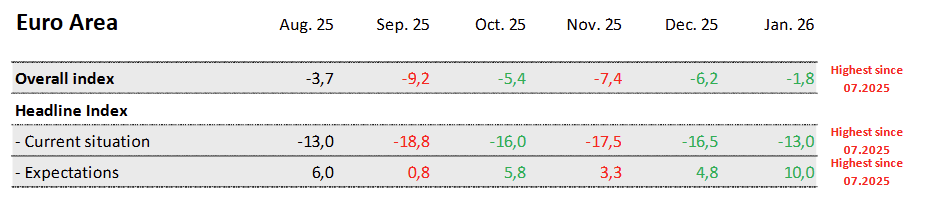

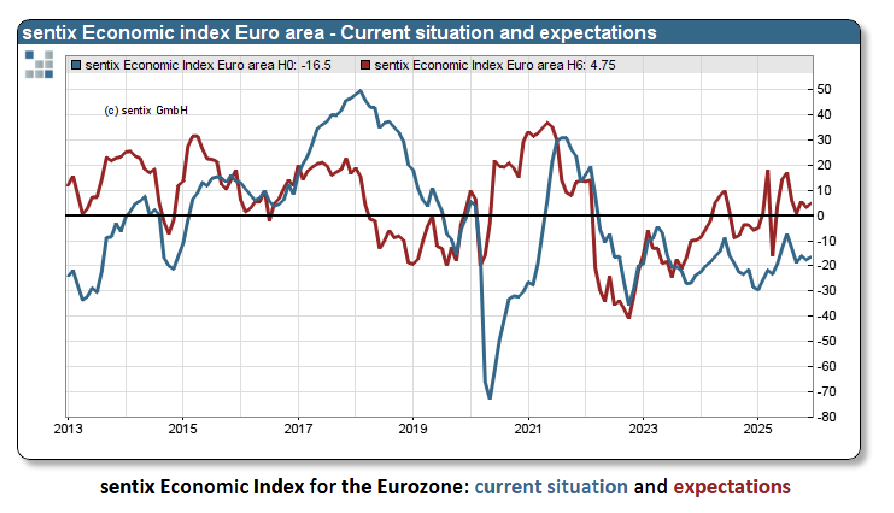

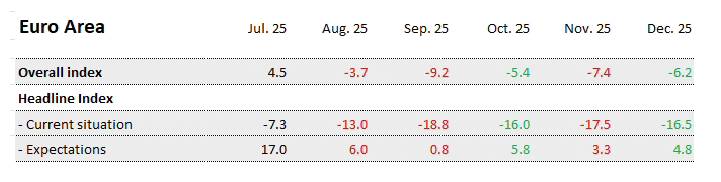

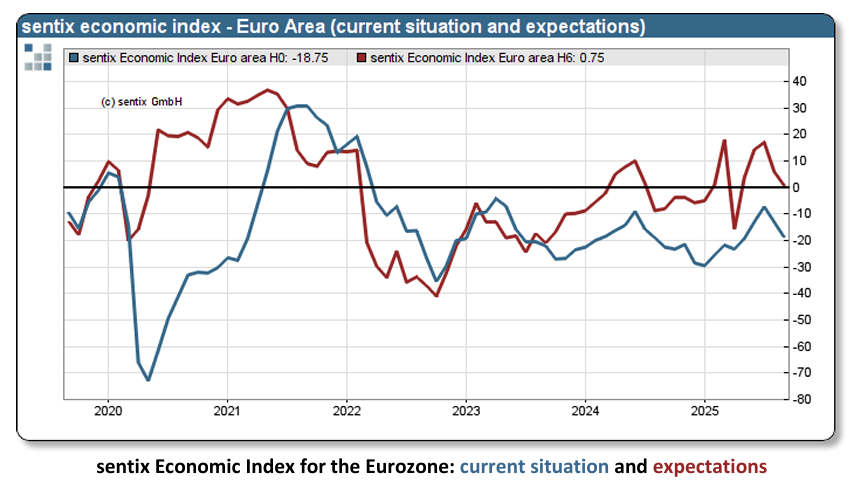

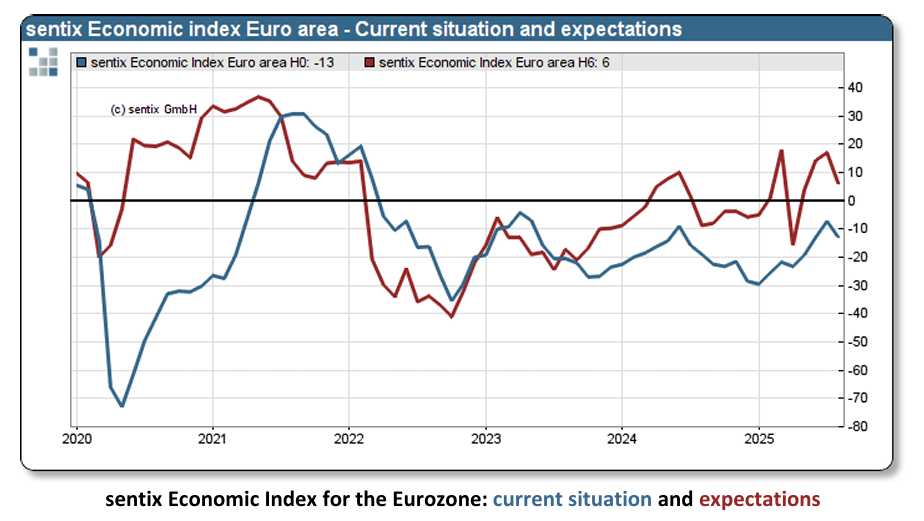

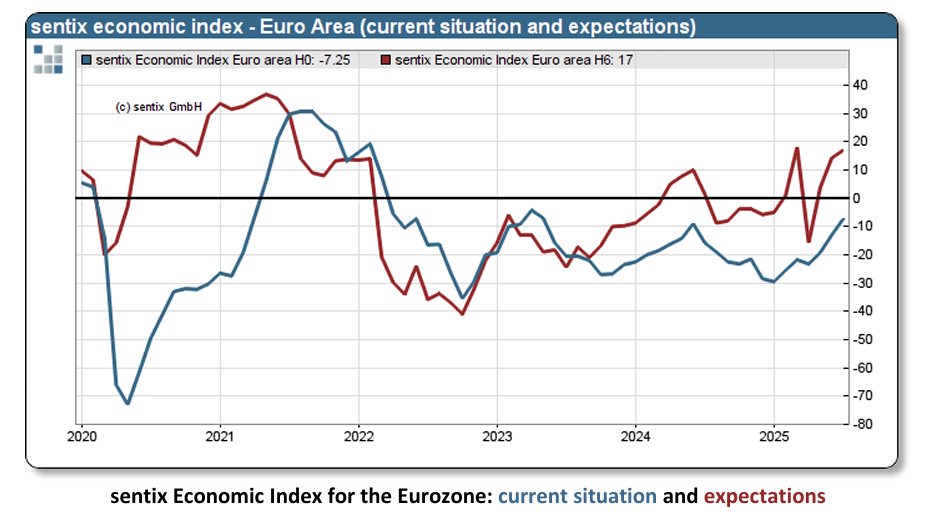

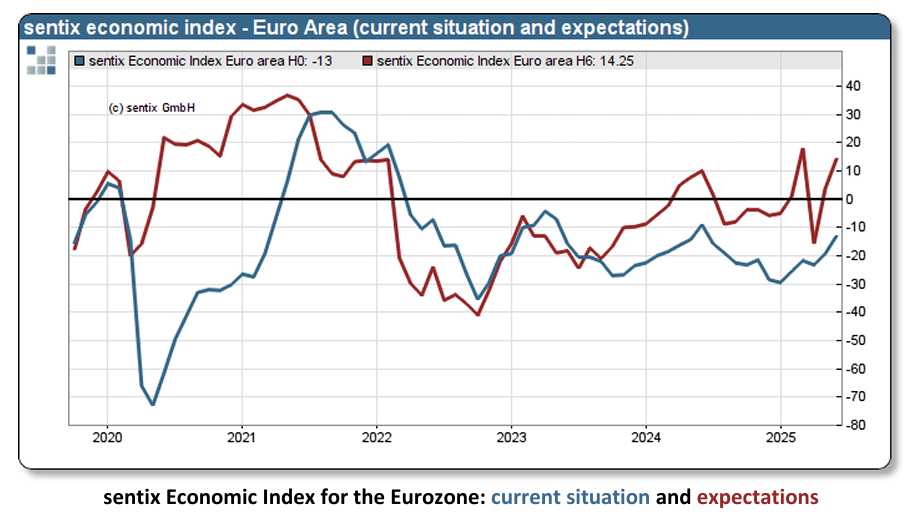

In the euro area, the overall index dropped to -3.1 (-7.3 pts MoM) after briefly returning to positive territory in February (+4.2), indicating a reversal of the recent improvement in investor sentiment.

-

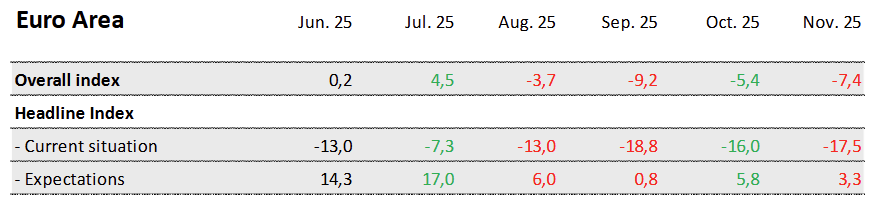

The euro area current situation index declined to -9.5 (Feb: -6.8), while expectations fell sharply to 3.5 from 15.8 (-12.3 pts), suggesting that forward-looking sentiment deteriorated significantly.

-

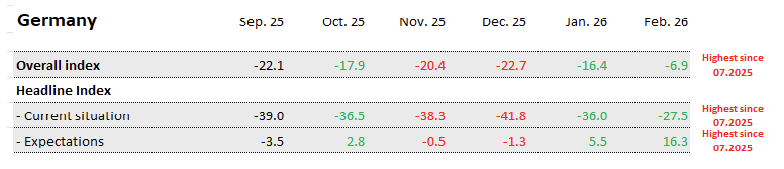

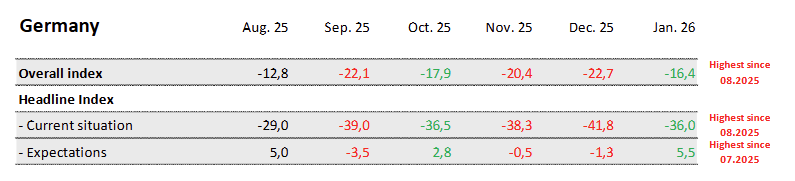

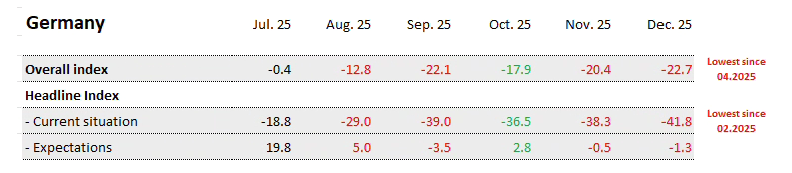

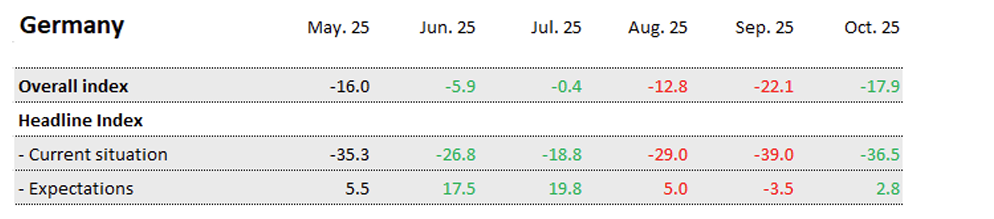

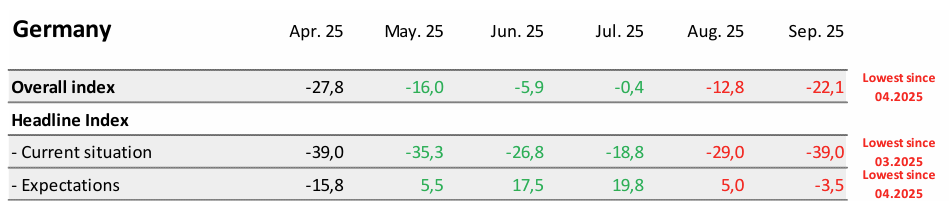

Germany’s overall Sentix index fell to -12.1 (-5.2 pts MoM), indicating renewed weakness in investor sentiment following the prior months’ improvement.

-

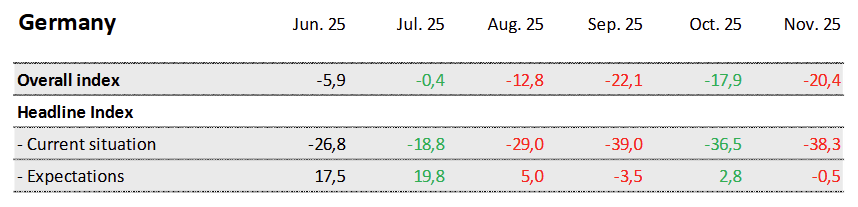

In Germany, the current situation index improved to -25.0 for the third consecutive month, the highest since July 2025, while expectations dropped sharply to 1.8 from 16.3 (-14.5 pts), showing a sharp pullback in forward-looking sentiment.

-

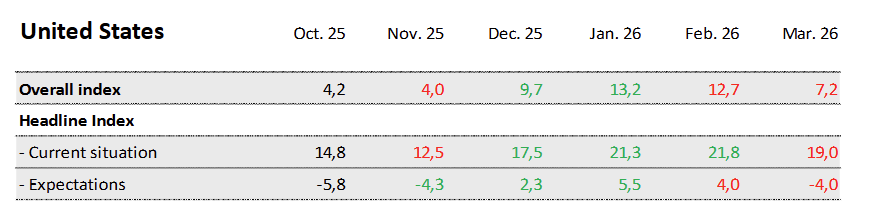

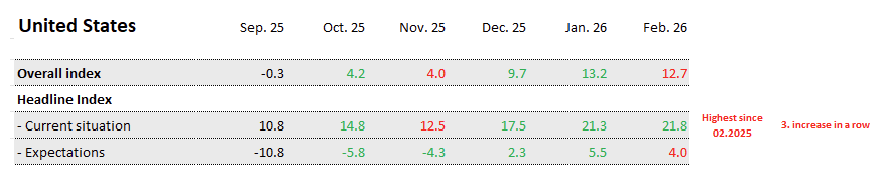

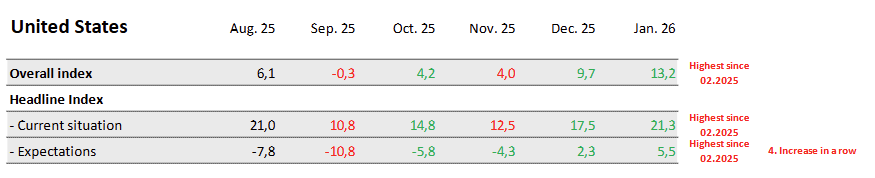

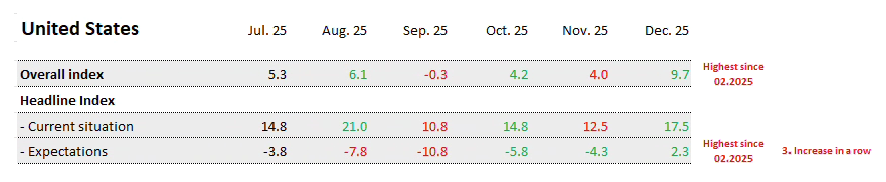

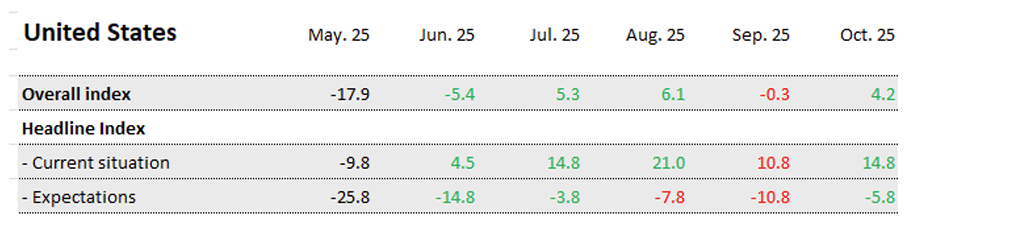

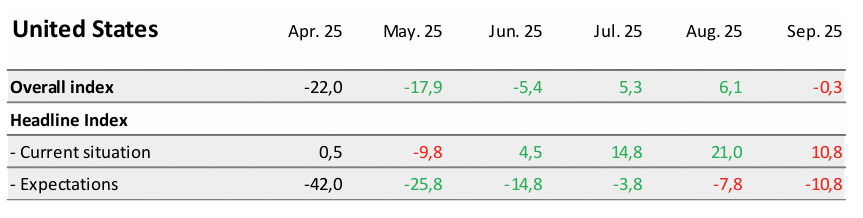

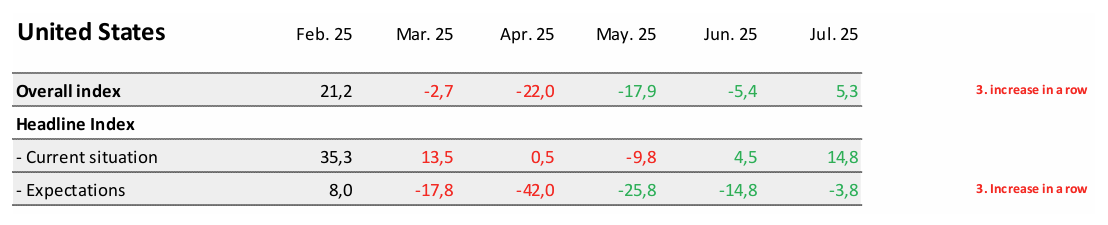

In the United States, the overall Sentix index fell to 7.2 (-5.5 pts MoM) after several months of gains, suggesting that sentiment softened following the prior improvement.

-

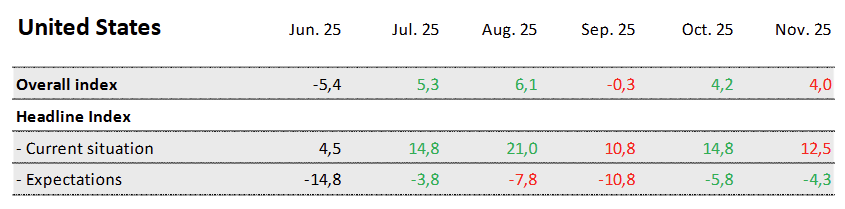

The US current situation index remained comparatively strong at 19.0 (Feb: 21.8), while expectations declined to -4.0 from 4.0 (-8.0 pts), moving back into negative territory and indicating weaker outlook assessments.

-

-

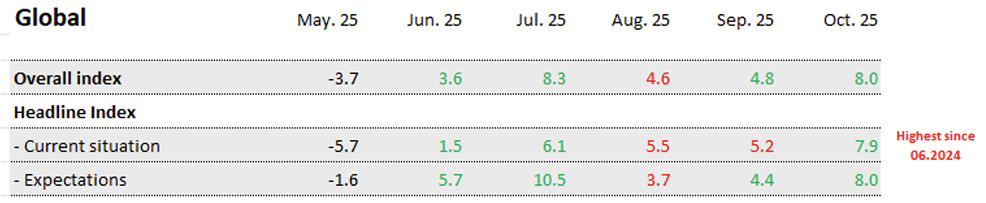

The Global Sentix Economic Index increased +2.4 pts to 15.2 in February, the highest since February 2022 and the sixth increase in a row. Both the Current Situation and Expectations indices advanced +2.7 pts to 14.7 and +2.1 pts to 15.7, respectively, both four year highs.

- Eurozone overall index rose +6.0 pts MoM to +4.2, with both the current situation (+6.2 pts to -6.8; highest since April 2023) and expectations (+5.8 pts to 15.8) improving for a third consecutive month, indicating a clear rebound in sentiment.

- Investor split in the eurozone showed institutional investors turning decisively more optimistic, with professional expectations rising to +24, while private investors remained comparatively cautious.

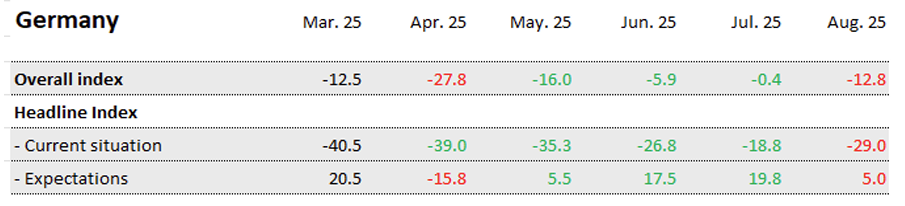

- Germany’s headline index surged by nearly +10 pts to +16.3, the highest since July 2025, driven by a sharp rise in expectations following stronger-than-expected industrial order intake.

- German expectations recorded a particularly large jump (+10.8 pts), while concerns around low gas storage levels did not materially weigh on sentiment in the survey.

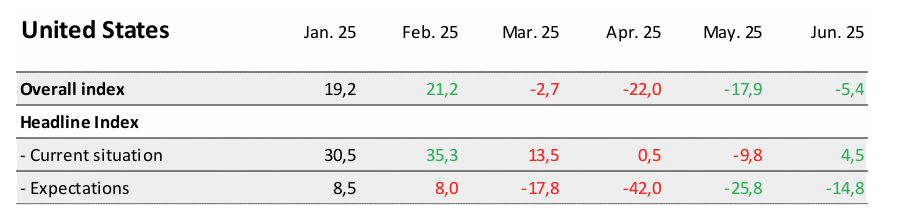

- United States sentiment lagged global trends, with the overall index slipping -0.5 pts to 12.7 in February and expectations down -1.5 pts to 4.0, reflecting investor concern over rising job losses despite otherwise solid activity indicators. The Current Situation index was most stable, rising 0.5 pts to 21.8, the highest in a year.

- Asia ex-Japan continued to lead globally, with the economic index rising for a sixth consecutive month to +23.9, reinforcing the region as the primary driver of the global upswing.

- Eastern Europe and Latin America both posted their third consecutive monthly increases, signaling sustained improvement in sentiment across several emerging regions.

-

The Sentix Global index increased to +12.8 in January, up from +10.4 in December, as the US and emerging markets helped to push the index up the highest since February 2022.

- The Global Current Situation index increased 2.2 pts to 12.0, and the Global Expectations index increased 2.5 pts to 13.6. Both indexes are at the highest since February 2022.

- Eurozone: The overall index improved to 1.8 (from 6.2), driven by expectations rising to 10.0 (from 4.8), while the current situation index improved to 13.0 (from 16.5), suggesting stabilization but limited momentum.

- Eurozone investor split: Sentix noted private investors had been more skeptical than professional investors, and while private sentiment is now improving, the historically large gap between groups narrowed only slightly, implying lingering disagreement about the outlook.

- Germany: The overall index climbed +6.3 pts to 16.4, with 6-month expectations improving to +5.5 (from 1.3), a “classic turnaround signal” per Sentix, though current conditions remained deeply weak at 36.0.

- United States: The overall index rose to 13.2 (from 9.7), the highest since February 2025, with the current situation improving to 21.3, highlighting continued perceived robustness despite political noise and the recent government shutdown.

- Asia ex-Japan: The index reached +21.7, the strongest momentum globally, with Sentix attributing strength to the ongoing technology and AI boom, reinforcing Asia as a key driver of global sentiment.

- Eastern Europe: The region moved back into positive territory at 0.6, with expectations rising to 13.6, exceeding the level seen before the outbreak of the Ukraine conflict, pointing to a sharp improvement in forward-looking sentiment.

- Latin America: The index rose to 6.4, benefiting from global recovery dynamics and stronger raw material demand, consistent with a broader upswing in emerging market sentiment.

-

The Sentix Global Economic Index rose +2.3 pts MoM to 10.4 in December 2025, its highest level since June 2024, reflecting a broad improvement led by Asia ex-Japan, Eastern Europe, and Latin America.

-

The Eurozone overall index increased +1.2 pts to -6.2, while the current situation remained weak at -16.5 and expectations edged up to 4.8, indicating continued stagnation despite modest stabilization.

-

Germany’s index deteriorated to -22.7 (lowest since April 2025), with the current situation falling to -41.8 and expectations slipping to -1.3, underscoring persistent recessionary pressure and a sharp divide between optimistic institutional investors and pessimistic private respondents.

-

In the United States, the overall index rose sharply to 9.7, the strongest since February 2025, with the current situation improving to 17.5 and expectations turning positive at 2.3, supported by sentiment gains following the end of the government shutdown.

-

The Global aggregate strengthened for a fourth month, reaching 10.4, while the current situation climbed to 9.8 (highest since March 2022) and expectations rose to 11.1 (highest since June 2024), signaling broadening optimism across regions.

-

Asia ex-Japan continued to lead global sentiment, marking a fourth consecutive increase and reaching its highest level since early 2022, with both situation and expectations readings improving further.

-

Overall, the December survey highlights a widening divergence: strong momentum in global and U.S. sentiment contrasts with persistent Eurozone weakness driven largely by Germany’s ongoing recession.

-

-

The Sentix Global Economic Index was basically unchanged at 8.1 in November 2025, reflecting ongoing global divergence, with persistent weakness in the Eurozone offset by continued optimism in Asia.

-

The overall index for the Eurozone declined -2.0 pts to -7.4, as both the current situation (-1.5) and expectations (-2.5) weakened, indicating that the region remains mired in a prolonged growth slump.

-

In Germany, the index dropped -2.4 pts, largely due to a -3.3 pt decline in expectations, while the current situation measure fell to -38.3, signaling continued recessionary conditions and limited near-term momentum.

-

Inflation concerns in the Eurozone eased notably, with the Sentix inflation barometer improving +9 pts to -11, which investors interpreted as a possible sign that central banks could take the weak economic backdrop into account in policy decisions.

-

Despite this improvement, fiscal sentiment remained deeply negative, as the fiscal policy barometer stayed at -32, reflecting ongoing worries about government debt sustainability.

-

In the United States, the headline index was largely unchanged (+0.2 pts), as a -2.3 pt drop in the current assessment was offset by a +1.5 pt rise in expectations, suggesting that while the government shutdown weighed on current conditions, longer-term sentiment remained more stable.

-

Japan stood out with a third consecutive improvement, as its overall index rose +4.9 pts to +12.2, with current conditions climbing +5.5 pts to +14.5 and expectations up +4.3 pts to +10.0, the strongest readings since April 2024.

-

The broader Asia ex-Japan region also extended its positive momentum, with the overall index up +0.6 pts to +18.7, reflecting sustained strength and steady optimism across regional economies.

-

Overall, the survey underscored how global sentiment in November remained divided, marked by persistent stagnation in Europe, resilience and policy-driven strength in Asia, and cautious steadiness in the United States despite fiscal disruptions.

-

-

The Eurozone index improved by +3.8 pts to -5.4 in September, with gains in both situation (+2.8 pts to -16.0) and expectations (+5.0 pts to 5.8), though readings remained below August levels, suggesting September pessimism had been overstated.

- Germany’s overall index rose to -17.9 (from -22.1), with Expectations turning slightly positive at +2.8, while the Current Situation stayed deeply negative at -36.5, highlighting persistent industrial weakness despite a small sentiment recovery.

- The US overall index rebounded to +4.2 (from -0.3), with the Current Situation improving to +14.8 (from +10.8), while Expectations remained subdued at -5.8, reflecting caution despite resilience amid the government shutdown.

- The Sentix Global Economic Index rose sharply to +8.0 in October 2025 (from +4.8 in September), marking its highest level since June 2024 and signaling renewed optimism across major economies.

-

The global Current Situation Index increased to +7.9 (from +5.2), indicating firmer perceptions of ongoing conditions.

-

The Expectations Index also strengthened to +8.0 (from +4.4), suggesting growing confidence in the outlook.

-

Sentix noted that Asia (excluding Japan) provided key momentum, with the regional index reaching +18.1, the best since February 2022.

-

Despite stronger sentiment, inflation remained a concern, and investors anticipated central banks would pause or slightly ease policy, reflecting hopes for stability amid elevated government debt levels.

-

The euro area Sentix Economic Index dropped -5.5 pts to -9.2 in September 2025, the lowest since April, reflecting renewed weakness in both current conditions and expectations.

-

The eurozone’s current situation index fell -5.8 pts to -18.8, while expectations declined -5.2 pts to 0.8, both at their weakest since April 2025.

-

Germany’s overall index dropped -9.3 pts to -22.1, the lowest since April, as sentiment deteriorated sharply.

-

Germany’s current situation plunged -10.0 pts to -39.0, matching the lowest level since March, underscoring a continued recessionary backdrop.

-

German expectations fell -8.5 pts to -3.5, the weakest since April, signaling little hope of near-term recovery.

-

Across the euro area, investor concerns centered on fiscal risks in France, trade frictions with the U.S., and the ongoing war in Ukraine.

-

Sentix noted that economic weakness is now severe enough that markets increasingly anticipate further ECB rate cuts.

-

The US headline index slid -6.4 pts to -0.3, after reaching positive territory in August. The current situation index fell -10.3 pts to 10.8, signaling a sharp loss of momentum, and the expectations index declined -3.0 pts to -10.8, showing rising concerns amid erratic trade policy and labor market strains.

-

The Global headline index edged up +0.2 pts to 4.8, holding in positive territory. The current situation index slipped -0.3 pts to 5.2, broadly stable vs August, and the expectations index rose +0.7 pts to 4.4, recovering slightly after last month’s decline.

-

-

The euro area Sentix Economic Index fell -11.0 pts to -3.7 in August 2025, reversing recent gains as investor sentiment deteriorated following the EU–US tariff deal.

- The eurozone’s current situation index dropped -5.8 pts to -13.0, and expectations plunged -11.0 pts to 6.0, pointing to renewed concerns over export sectors and rising debt.

- Germany’s index dropped -12.4 pts to -12.8, with the current situation down -10.2 pts to -29 and expectations sliding -14.8 pts to 5.0.

- The US index remained positive, rising 0.8 pts to 6.1, due to preemptive production boosts, though expectations fell -4.0 pts to -7.8, suggesting short-term support may fade.

- The global index eased 3.7 pts to 4.6 after rising for three straight months. The current situation index dropped -0.6 pts to 5.5, while the expectations index dropped -6.8 pts to 3.7.

-

The euro area Sentix Economic Index rose +4.4 pts to +4.5 in July 2025, marking the highest level since February 2022 and the third consecutive monthly gain.

- The current situation index increased +5.8 pts to -7.3 (highest since May 2023), while expectations rose +2.8 pts to +17.0.

- Germany’s overall index climbed to -0.4, the highest since February 2022 as well, with the current situation up +8.0 pts to -18.8 and expectations rising +2.3 pts to +19.8.

- The U.S. index surged +10.7 pts to +5.3 (+22.7 pts from April lows), with current conditions jumping +10.3 pts and expectations up +11.0 pts.

- Asia ex-Japan showed signs of an emerging boom, contributing to the third straight global improvement.

- The global overall index increased for the 3rd straight month, up +4.7 pts to 8.3, the highest since June 2024.

- Global current conditions rose to +6.1 and expectations climbed +4.8 pts, confirming broad-based recovery momentum.

-

The euro area Sentix Economic Index rose 8.3 pts to +0.2 in June 2025, the highest since June 2024, as investor sentiment improved on stronger German data and easing fears over U.S. tariffs.

- The eurozone expectations index jumped 10.5 pts to 14.3, while the current situation index rose 6.3 pts to -13.0.

- Germany’s overall index rose to -5.9, the highest since March 2022, with expectations at 17.5 and current conditions up to -26.8.

- The U.S. overall index improved to -5.4 from -17.9, led by a 14.3 pt rise in the current situation (to +4.5), but expectations remained weak at -14.8.

- Japan edged back into growth with an overall index of 1.9 (+2.4 pts), while Asia ex-Japan rose 6.2 pts to 11.2 on stronger sentiment in both current and expected conditions.

- The global index turned positive at 3.6 (+7.3 pts), as improving signals from Europe and Asia offset residual drag from the U.S. tariff shock.

-

The euro area Sentix Index rebounded 11.4 pts to -8.1 in May after seeing a sharp decline in April after the announcement of Trump’s broad reciprocal tariffs.

- The Current Situation index increased 4.0 pts to -19.3, the highest since August 2024, and the Expectations index swung 19.6 pts to 3.8.

- The German index improved 11.8 pts to -16.0 including the third straight increase in the Current Situation index to -35.3, the highest since July 2024.

- Sentix: “All in all, investors now have a more subdued but basically ‘calm’ view of the economy than they did in March. Against the backdrop of Donald Trump's unpredictability and signs of weakness in the US economy, this is a surprisingly relaxed assessment.”

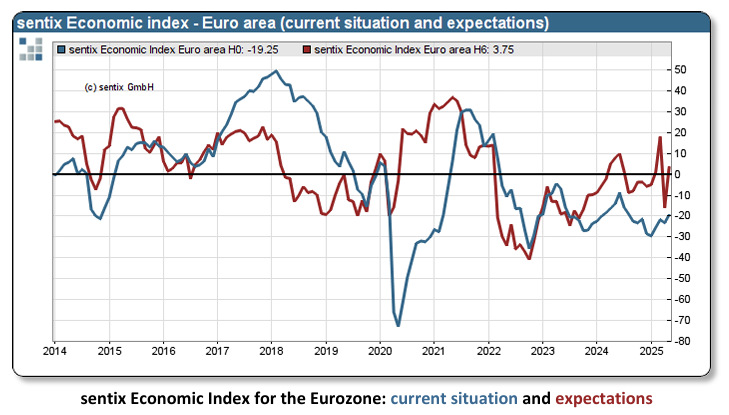

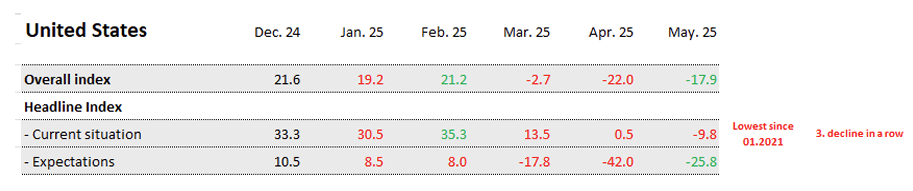

The US Sentix Index saw a smaller rebound of 4.1 pts to -17.9 as uncertainty from erratic trade policy continued to weigh on sentiment.

- The Current Situation index actually fell to the weakest reading since January 2021. down -10.3 pts to -9.8, while the Expectations index increased 16.2 pts to -25.8 (still down sharply from 10.5 in December 2024).

- Sentix: “Despite the weak economic data, however, a rapid response by the Fed is unlikely, because if there are negative inflationary effects from the US tariffs, then these should be reflected in the US data.”

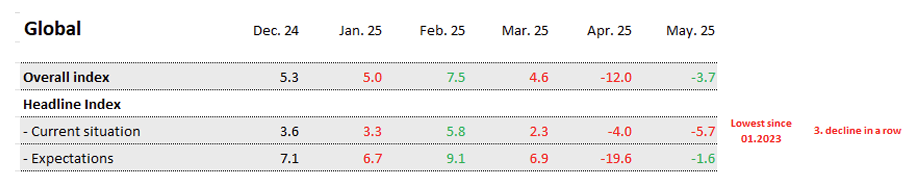

Due to the sharp decline in current conditions in the US, the global Current Situation index fell to the lowest since January 2023 even though expectations saw a significant improvement.