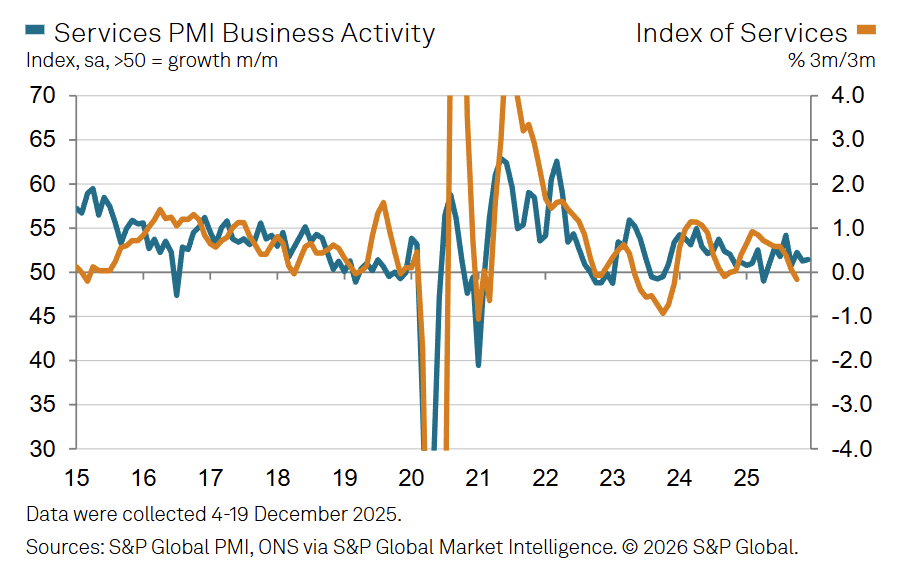

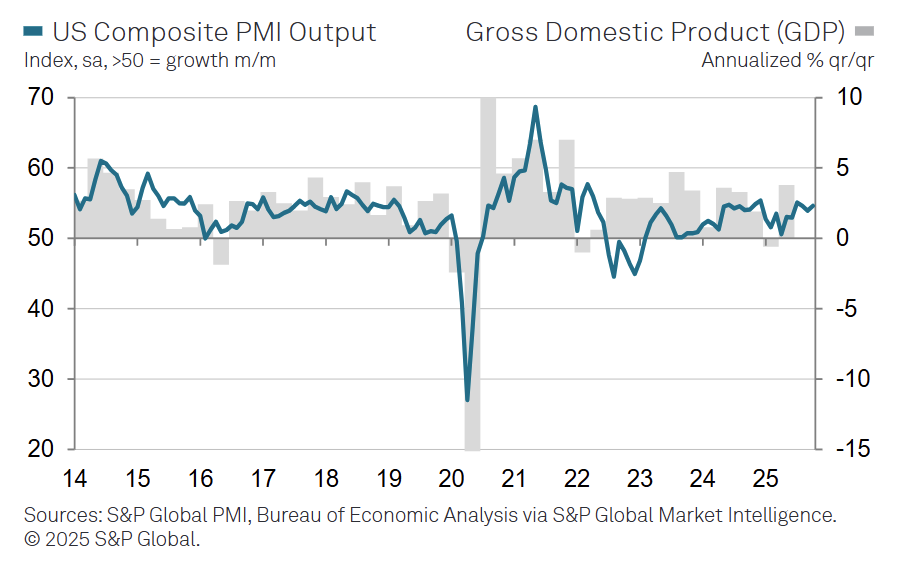

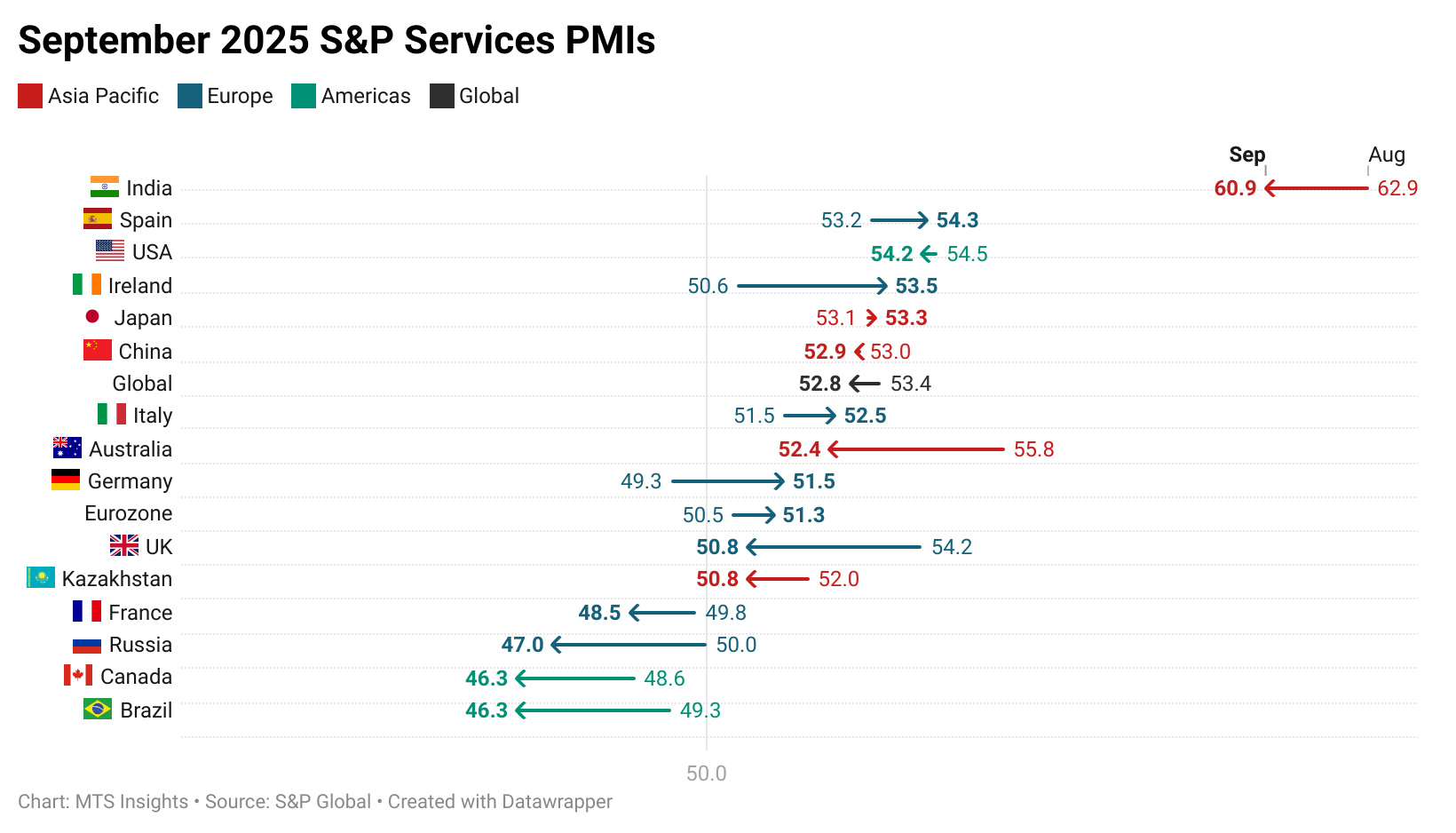

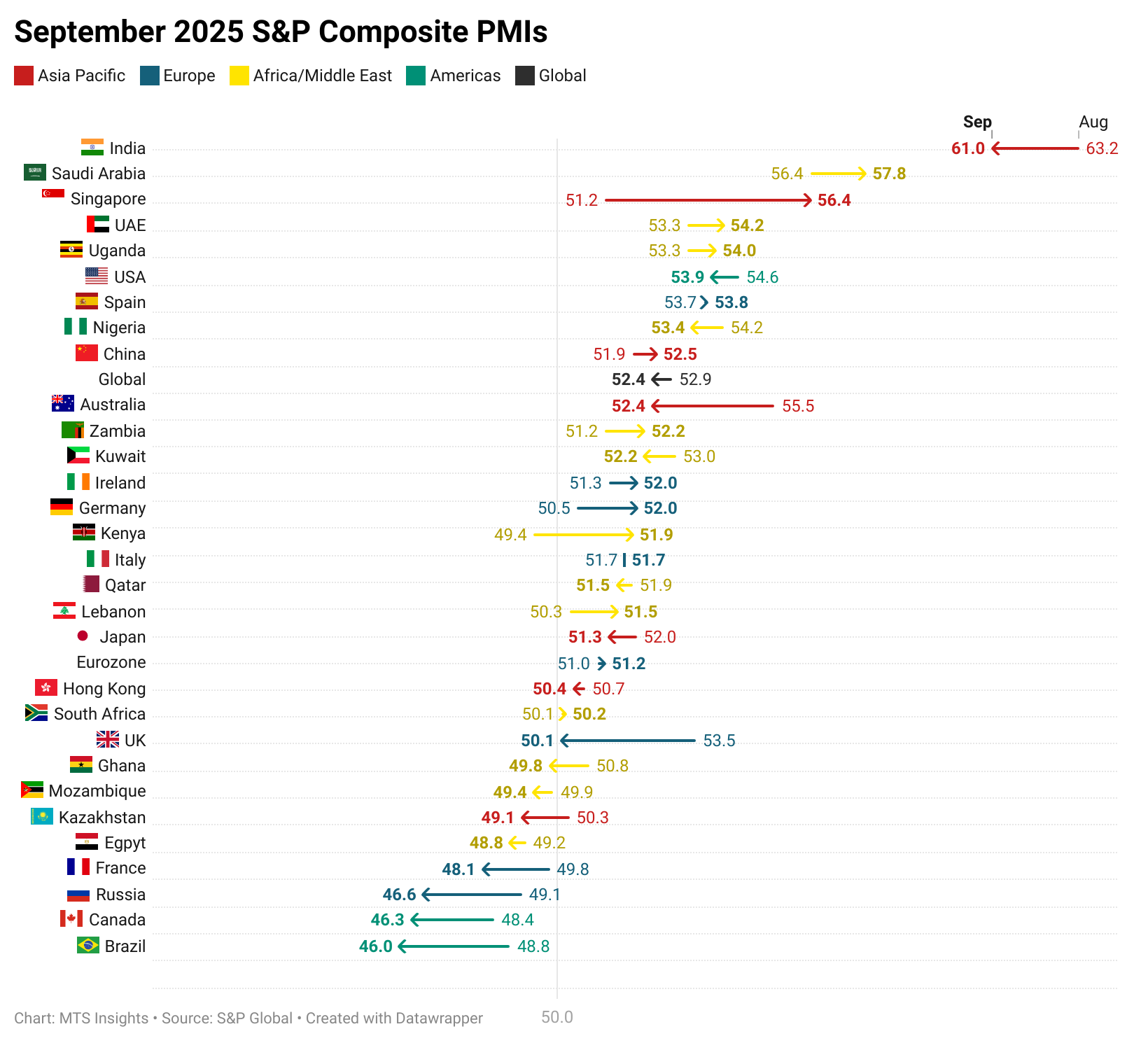

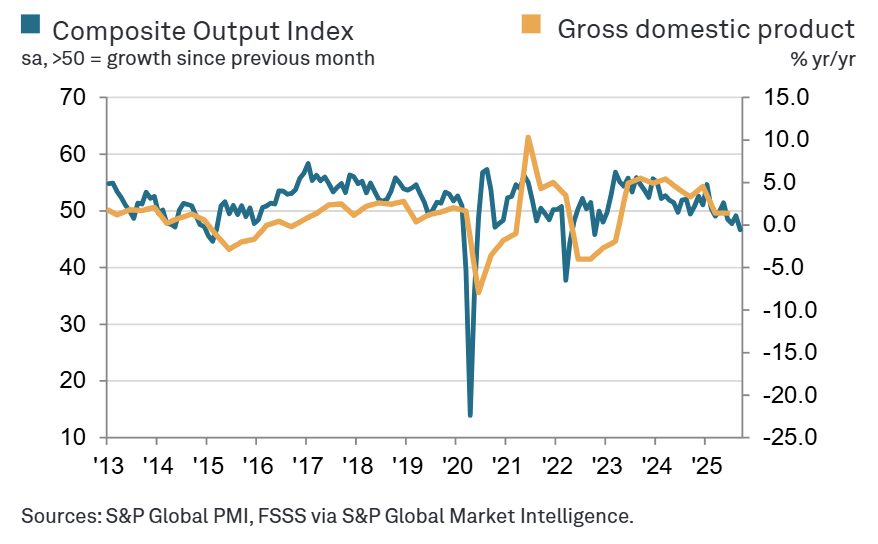

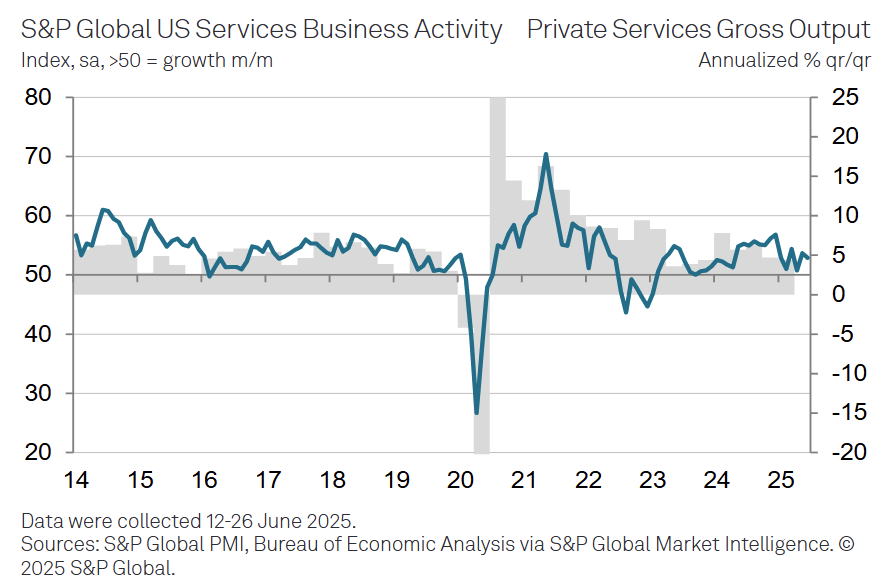

S&P Global Services PMIs

S&P Global Services PMIs

- Source

- S&P Global

- Source Link

- https://www.pmi.spglobal.com/

- Frequency

- Monthly

- Next Release(s)

- May 5th, 2026 12:00 AM

-

June 3rd, 2026 12:00 AM

-

July 6th, 2026 12:00 AM

-

August 5th, 2026 12:00 AM

-

September 3rd, 2026 12:00 AM

-

October 5th, 2026 12:00 AM

-

November 4th, 2026 12:00 AM

-

December 3rd, 2026 12:00 AM

-

January 6th, 2027 12:00 AM

-

February 3rd, 2027 12:00 AM

-

March 3rd, 2027 12:00 AM

-

April 5th, 2027 12:00 AM

Latest Updates

-

Asia Pacific Africa & Middle East Europe North & South America Australia - 4/3/2026 Nigeria* - 3/2/2026 Ireland - 4/3/2026 Brazil - 4/3/2026 Singapore* - 4/3/2026 Qatar* - 4/3/2026 Spain - 4/3/2026 Canada - 4/3/2026 Hong Kong* - 4/3/2026 Kuwait* - 4/3/2026 Italy - 4/3/2026 US - 4/3/2026 Japan - 4/3/2026 Egypt* - 4/3/2026 France - 4/3/2026 China - 4/3/2026 UAE* - 4/3/2026 Germany - 4/3/2026 Global - 4/3/2026 India - 4/3/2026 Uganda* - 4/3/2026 Eurozone - 4/3/2026 Russia - 3/4/2025 South Africa* - 4/3/2026 UK - 4/3/2026 Kazakhstan - 4/3/2026 Lebanon* - 4/3/2026 Ghana* - 4/3/2026 Zambia* - 4/3/2026 Saudi Arabia* - 4/3/2026 Mozambique* - 4/3/2026 Kenya* - 4/3/2026 * Composite only

-

Global - 3/4/2026

Asia Pacific Africa & Middle East Europe North & South America Australia - 3/4/2026 Nigeria* - 3/2/2026 Ireland - 3/4/2026 Brazil - 3/4/2026 Singapore* - 3/4/2026 Qatar* - 3/4/2026 Spain - 3/4/2026 Canada - 3/4/2026 Hong Kong* - 3/4/2026 Kuwait* - 3/4/2026 Italy - 3/4/2026 US - 3/4/2026 Japan - 3/4/2026 Egypt* - 3/4/2026 France - 3/4/2026 China - 3/4/2026 UAE* - 3/4/2026 Germany - 3/4/2026 India - 3/4/2026 Uganda* - 3/4/2026 Eurozone - 3/4/2026 Russia - 3/4/2025 South Africa* - 3/4/2026 UK - 3/4/2026 Kazakhstan - 3/4/2026 Lebanon* - 3/4/2026 Ghana* - 3/4/2026 Zambia* - 3/4/2026 Saudi Arabia* - 3/4/2026 Mozambique* - 3/4/2026 Kenya* - 3/4/2026 * Composite only

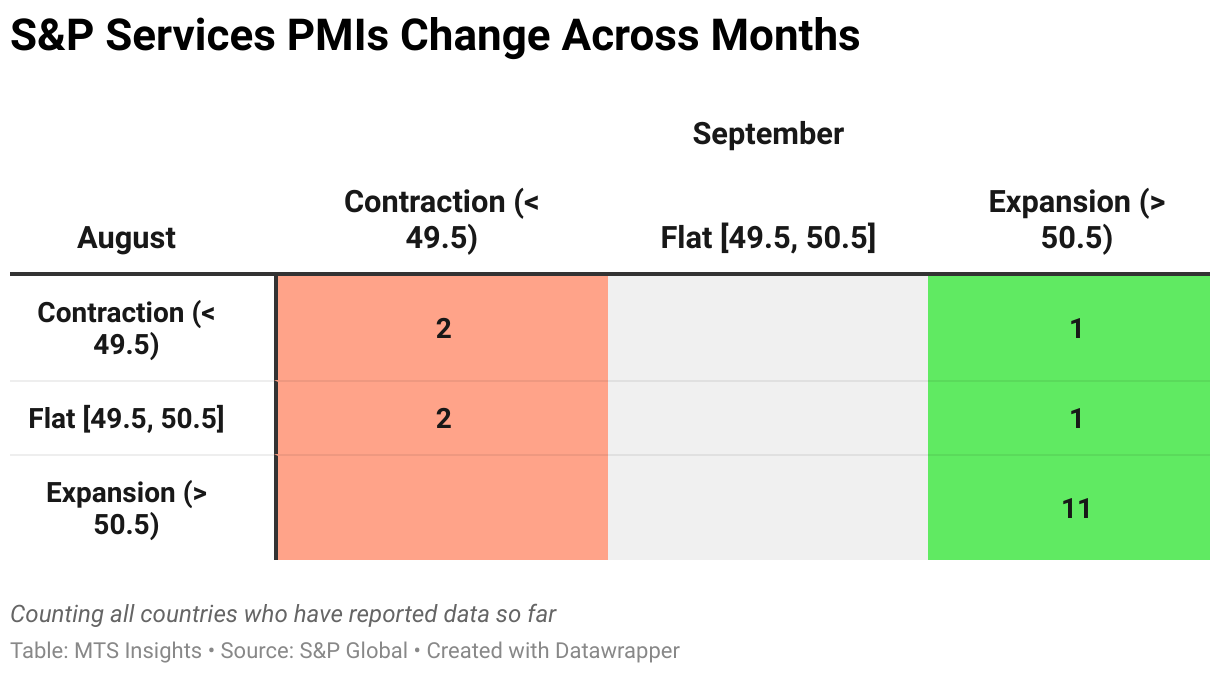

Key Results

Highs & Lows

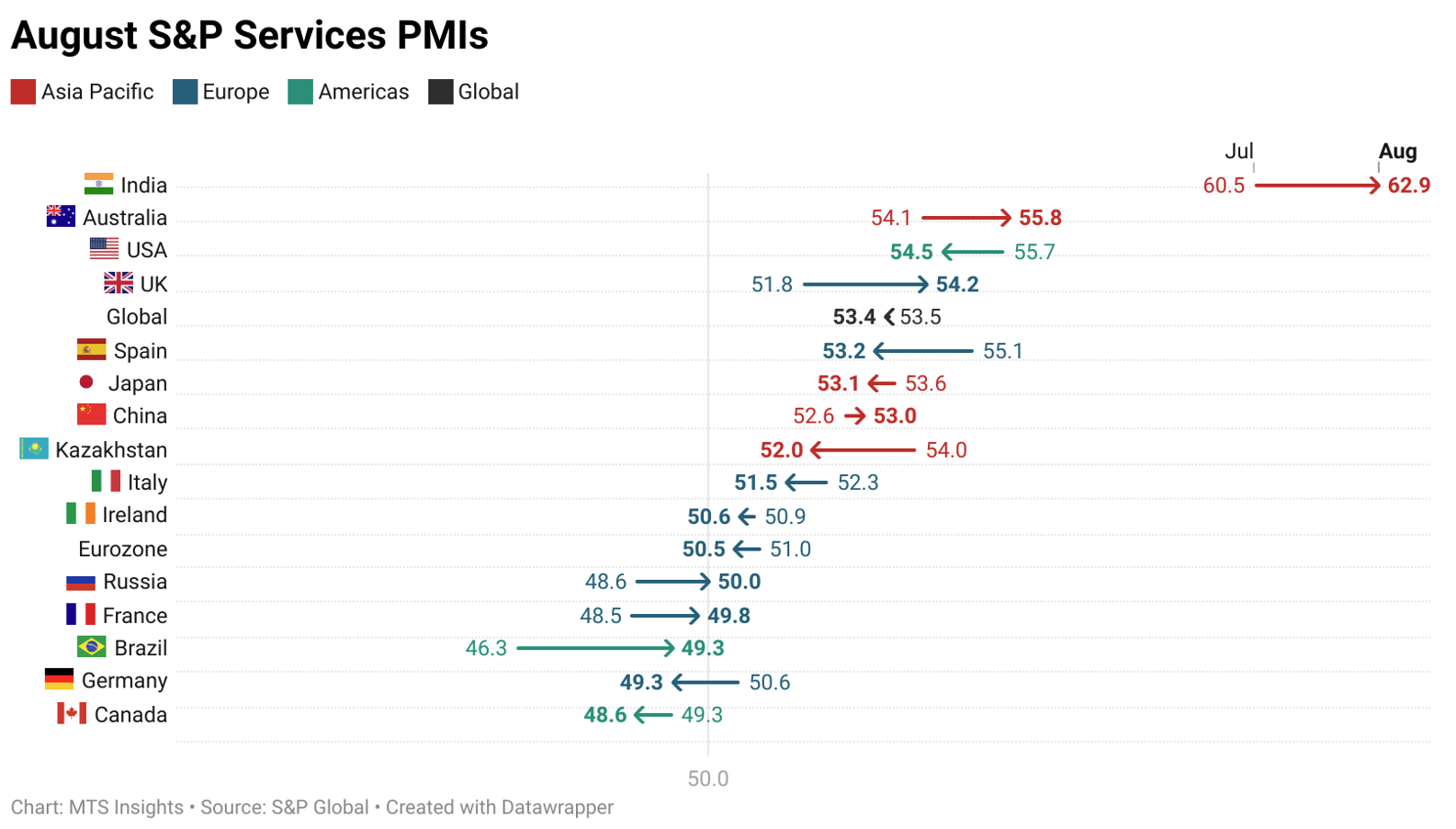

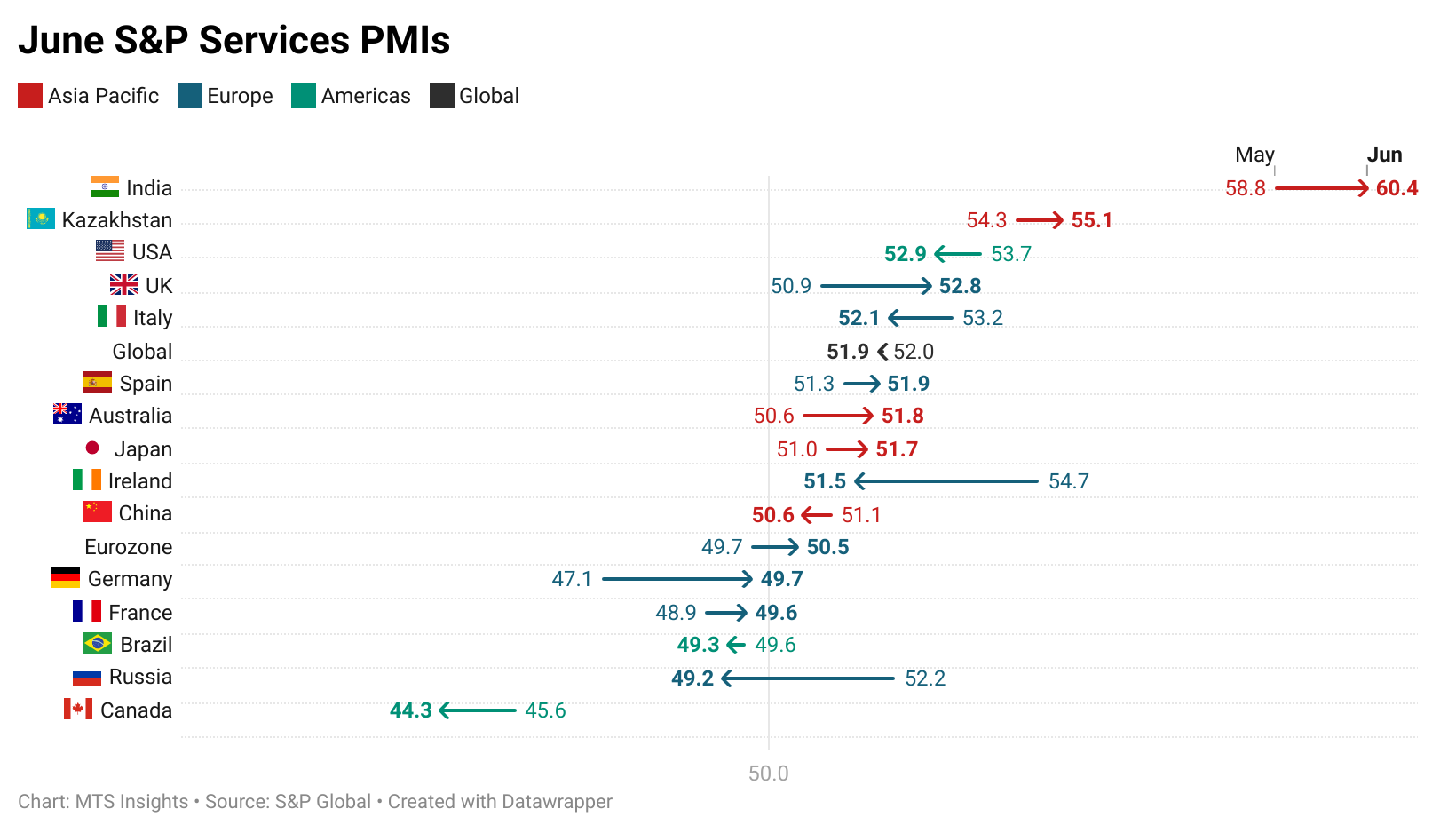

- Hong Kong (Composite) up 1.0 pt to 53.3, highest since March 2023.

- Singapore (Composite) up 2.4 pts to 59.2, highest since May 2022.

- China (Services) up 4.4 pts to 56.7, highest since May 2023.

- China (Composite) up 3.8 pts to 55.4, highest since May 2023.

- Kazakhstan (Services) down -2.5 pts to 48.0, lowest since February 2023.

- Kazakhstan (Composite) down -2.5 pts to 47.2, lowest since January 2022.

- US (Services) down -1.0 pt to 51.7, lowest since April 2025.

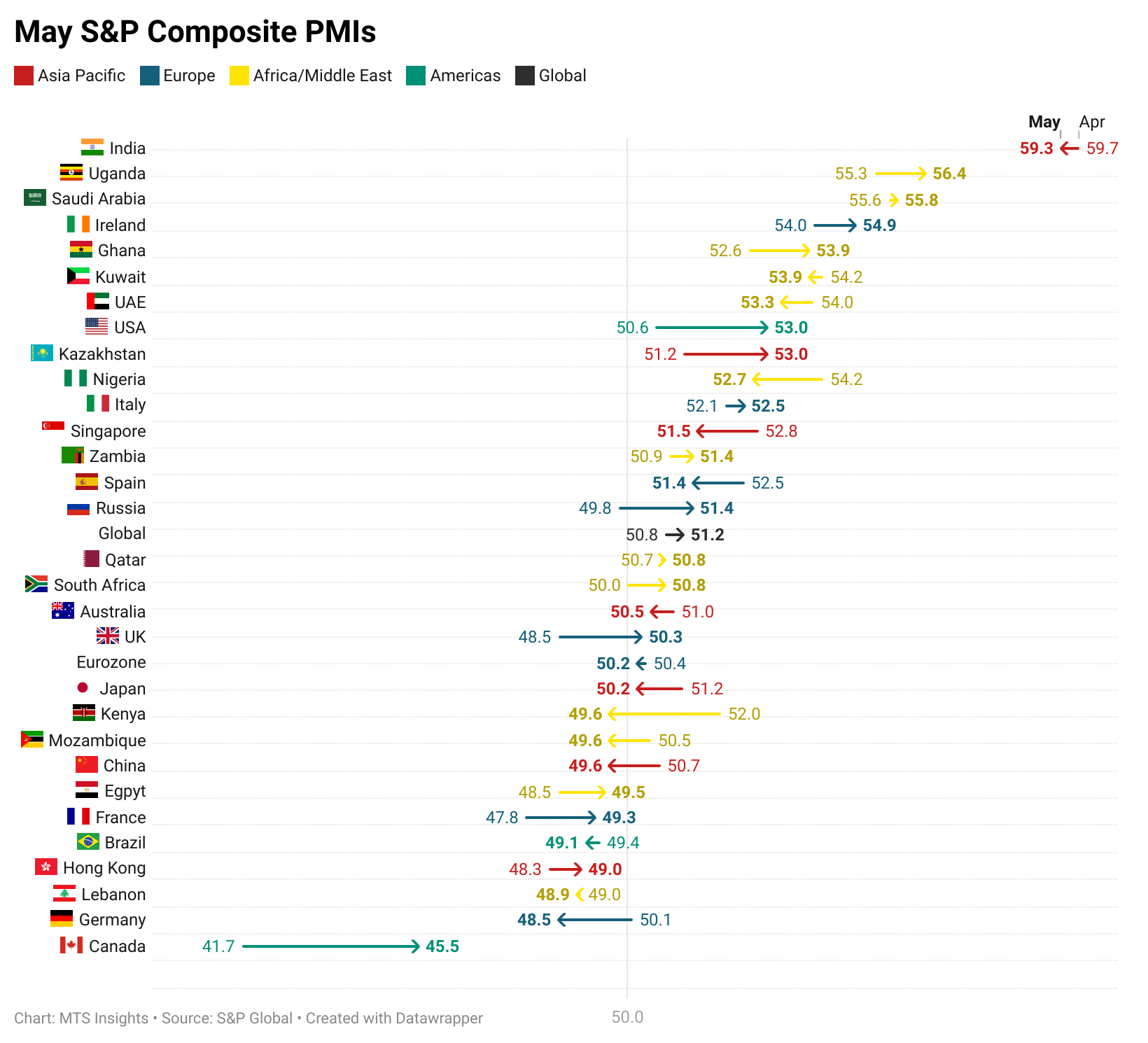

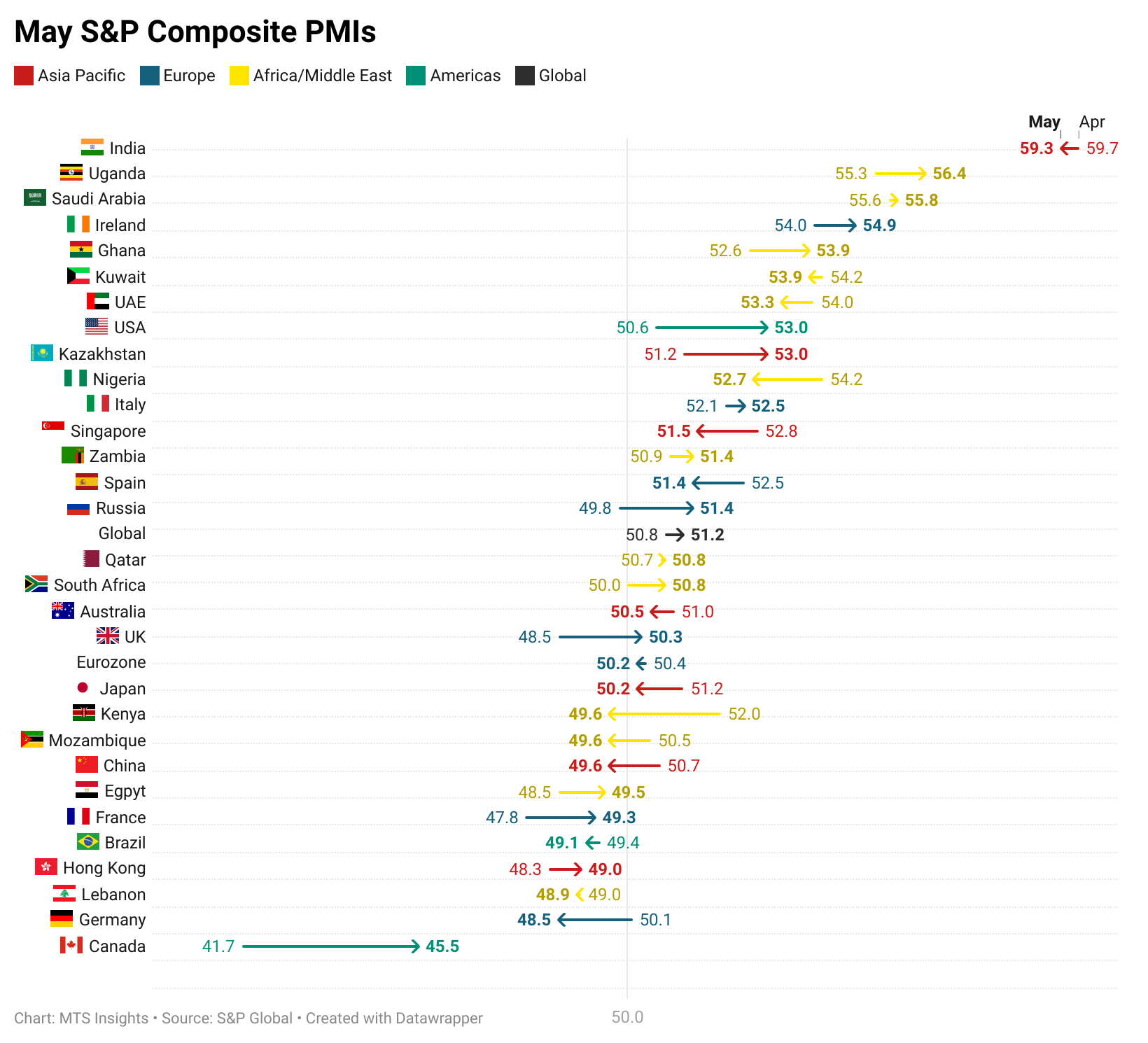

- Global (Composite) up 0.7 pts to 53.3, highest in 21 months.

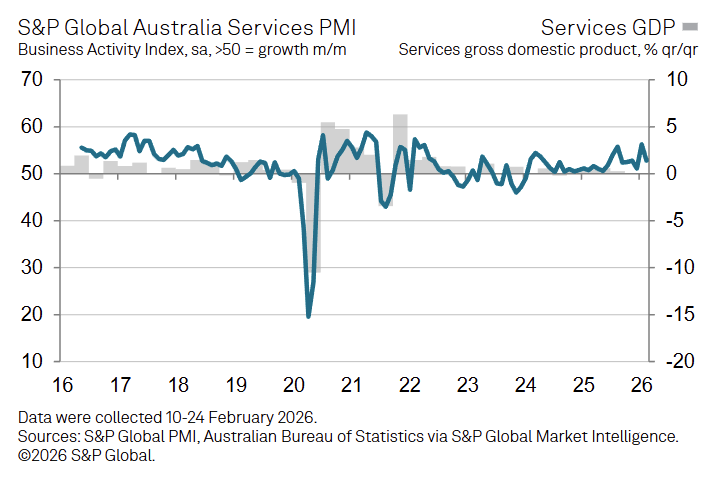

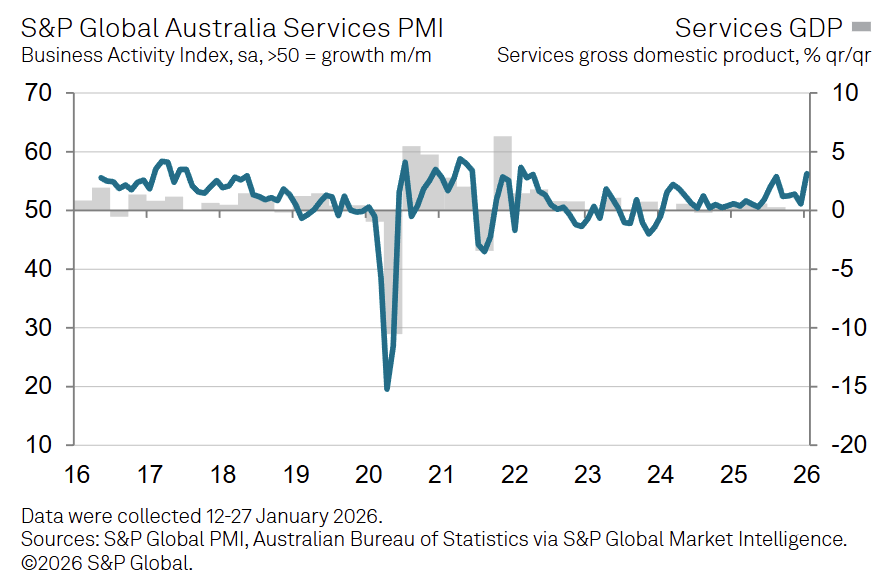

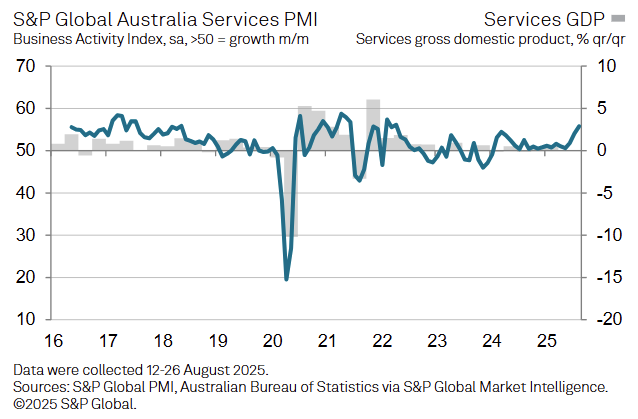

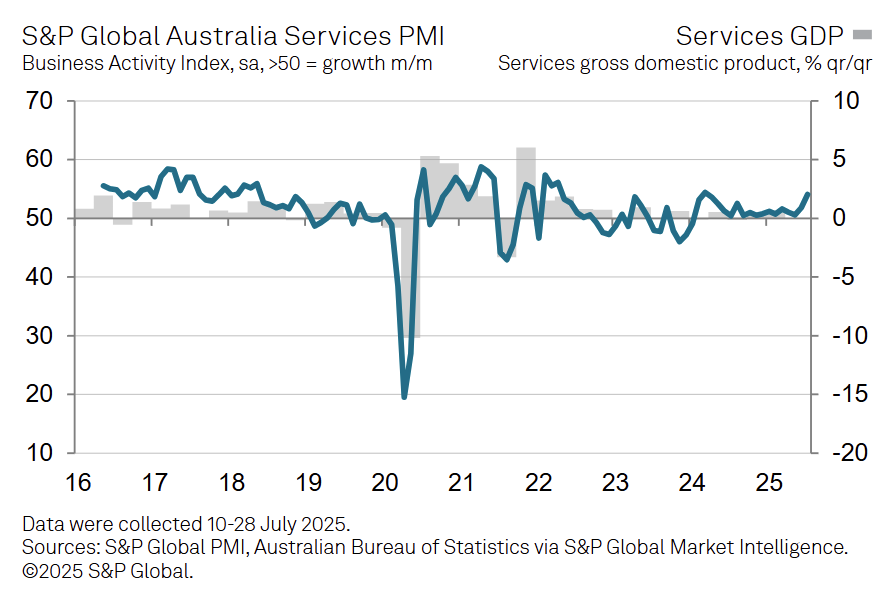

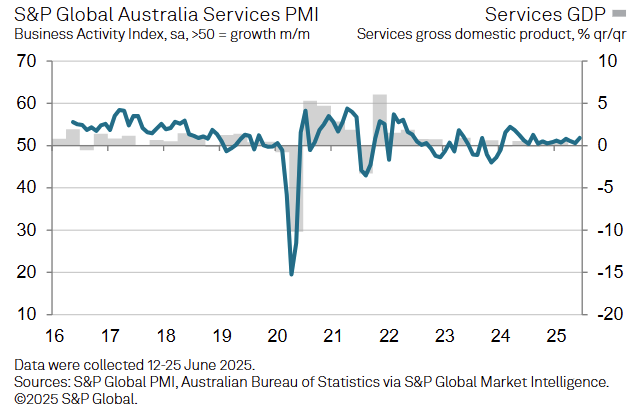

Australia

Australia’s Services PMI Business Activity Index eased to 52.8 in February (-3.5 pts MoM from 56.3) but remained above the 50 expansion threshold, extending the current services growth streak to just over two years.

-

Services activity remained in expansion at 52.8 in February (Jan: 56.3), indicating continued growth even as the pace slowed from an almost four-year high recorded at the start of the year.

-

New business continued to increase at a strong pace, though slower than in January, supported by new service launches and expanding customer bases among Australian service providers.

-

International demand for Australian services also rose further in February, although the rate of foreign demand growth moderated compared with the stronger increase seen earlier in the year.

-

Firms increased staffing levels at the fastest pace since April 2023 to manage rising workloads, reflecting stronger hiring activity across the services sector.

-

Outstanding business increased for a second consecutive month, indicating that demand continued to outpace firms’ capacity even as employment levels rose.

-

Input costs increased at a faster rate and reached the highest level in five months, with firms citing higher labor, electricity, and supply costs as the main drivers.

-

Output prices also increased more quickly, with the rate of charge inflation reaching the steepest level in six months and moving above the long-run average as firms passed higher costs onto clients.

-

Business confidence declined despite continued activity growth, indicating that firms remained cautious about the outlook even as demand conditions remained solid.

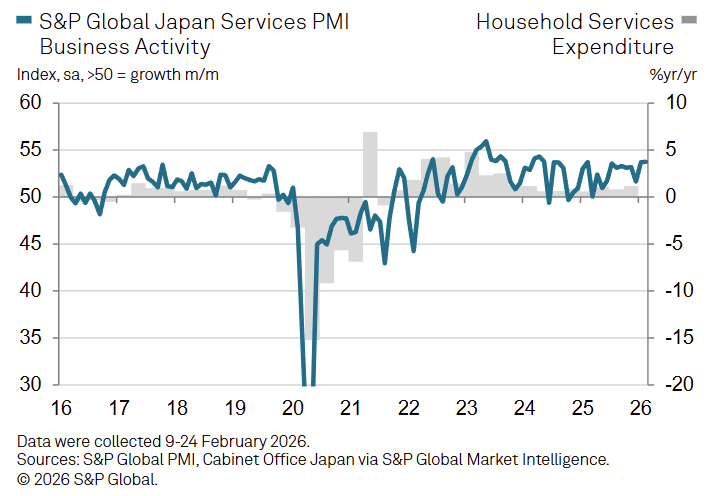

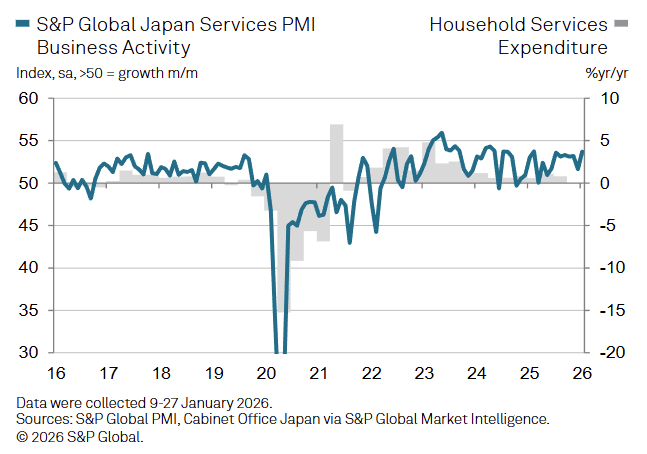

Japan

Japan’s Services PMI Business Activity Index edged up to 53.8 in February (+0.1 pts MoM from 53.7), marking the strongest services activity growth since May 2024 and extending the sector’s expansion streak to eleven consecutive months.

-

Services activity increased across all five monitored sub-industries, with Finance & Insurance recording the strongest gains and supporting the overall expansion in the sector.

-

New orders rose at the fastest pace since April 2024, reflecting stronger demand conditions and new client wins that lifted sales across service providers.

-

The increase in new business was driven largely by domestic demand, while new work from abroad rose only marginally, indicating limited contribution from international markets.

-

Staffing levels continued to increase but at a slower pace, with job creation easing to a three-month low as firms faced labor shortages, staff resignations, and difficulties filling vacancies.

-

Outstanding business increased at the fastest rate since June 2023, as stronger demand combined with slower hiring contributed to rising backlogs of work.

-

Input costs rose at a sharper and historically elevated pace, with firms reporting stronger cost pressures across the private sector.

-

Selling prices increased at the fastest rate since April 2014 as service providers passed higher costs on to customers, marking the steepest price increases in nearly twelve years.

-

The Composite PMI Output Index rose to 53.9 in February (Jan: 53.1), indicating the fastest expansion in Japan’s private sector activity in 33 months as both services and manufacturing output strengthened.

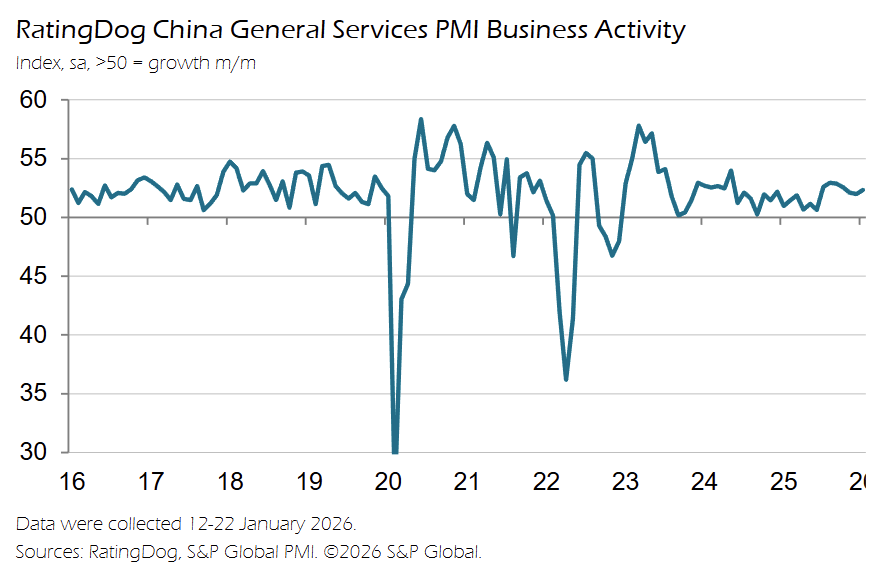

China

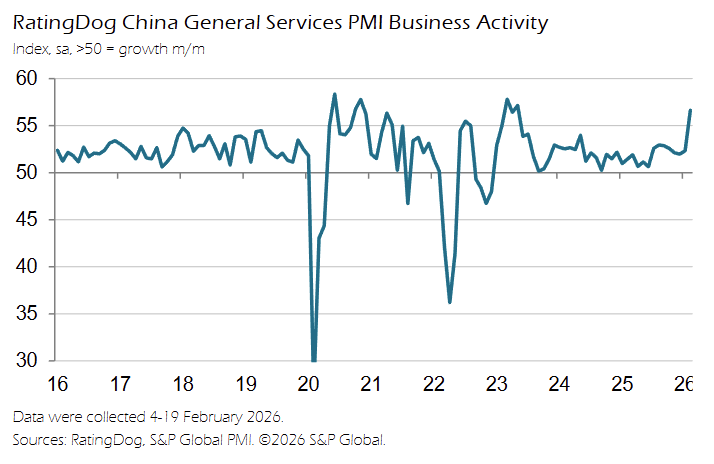

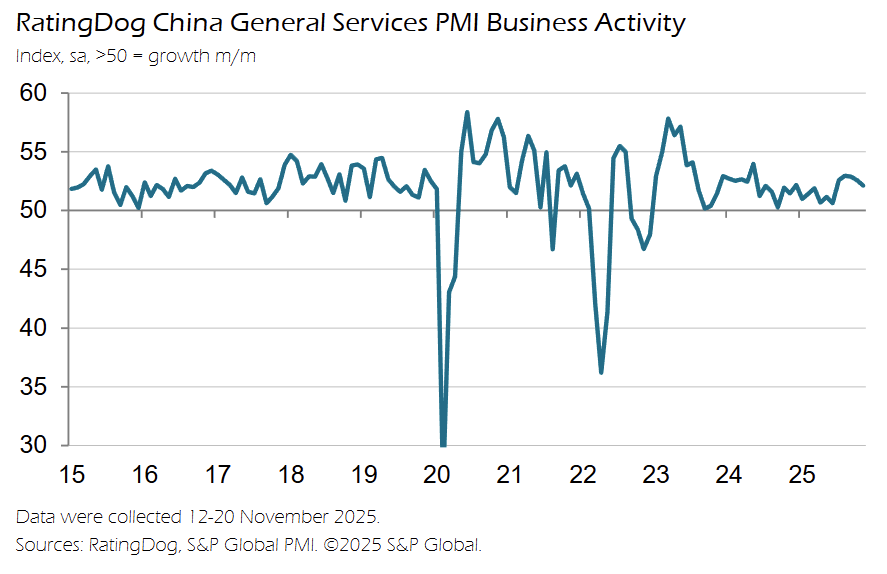

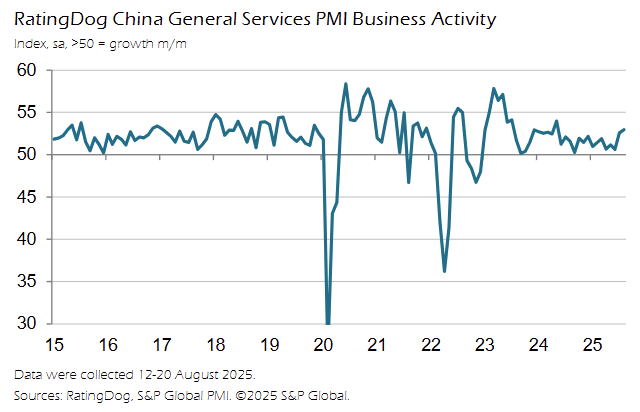

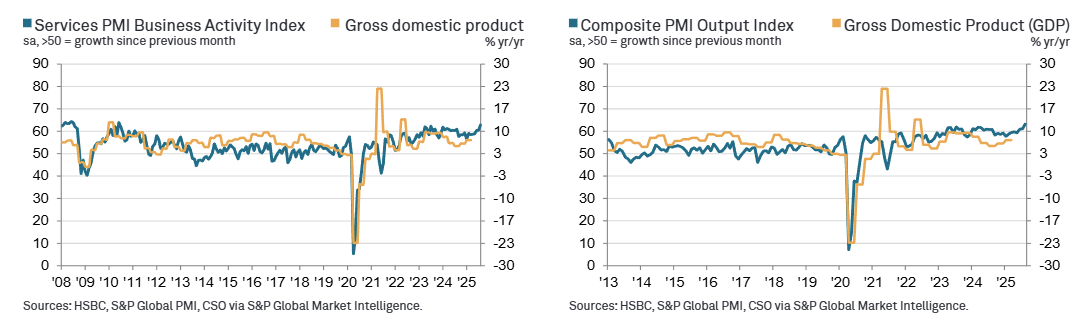

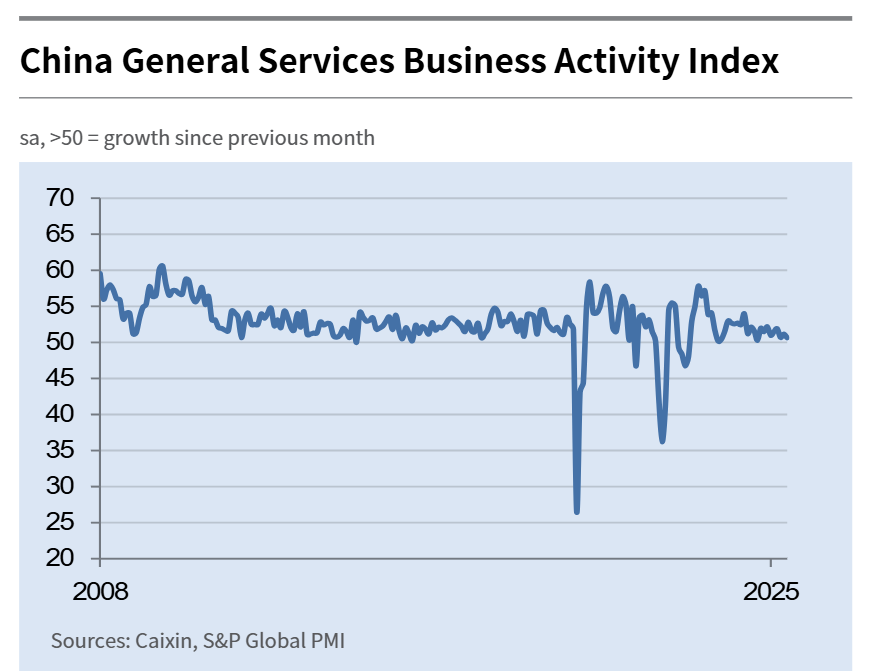

China’s Services PMI Business Activity Index rose to 56.7 in February (+4.4 pts MoM from 52.3), marking the strongest services activity growth in 33 months as stronger domestic and overseas demand lifted new business inflows.

-

Services activity expanded at 56.7 in February (Jan: 52.3), extending the current growth streak that began in January 2023 and representing the fastest expansion since May 2023.

-

Incoming new business increased at the joint-fastest pace since May 2024, driven by successful promotional efforts, rising client enquiries, and stronger overall demand conditions.

-

New export business also increased at the quickest pace in a year, reflecting improved overseas demand and stronger tourism-related activity.

-

Backlogs of work continued to accumulate as higher new business inflows lifted outstanding workloads, although the rate of backlog growth remained marginal and broadly similar to the previous two months.

-

Employment declined in February after a slight increase in January, as firms reduced staffing levels primarily for cost control amid rising operating expenses and limited capacity pressure.

-

Input costs increased at a faster rate than in January due to higher wage and energy expenses, indicating intensifying cost pressures across the services sector.

-

Selling prices increased for the first time in three months and rose at the fastest pace in 21 months as firms passed higher costs onto clients during a period of strengthening demand.

-

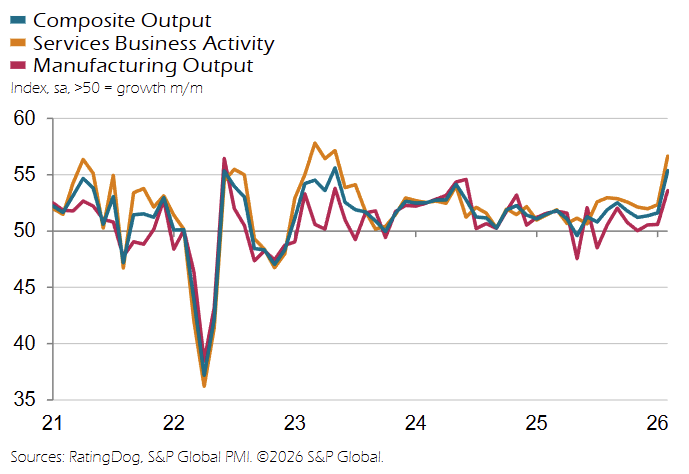

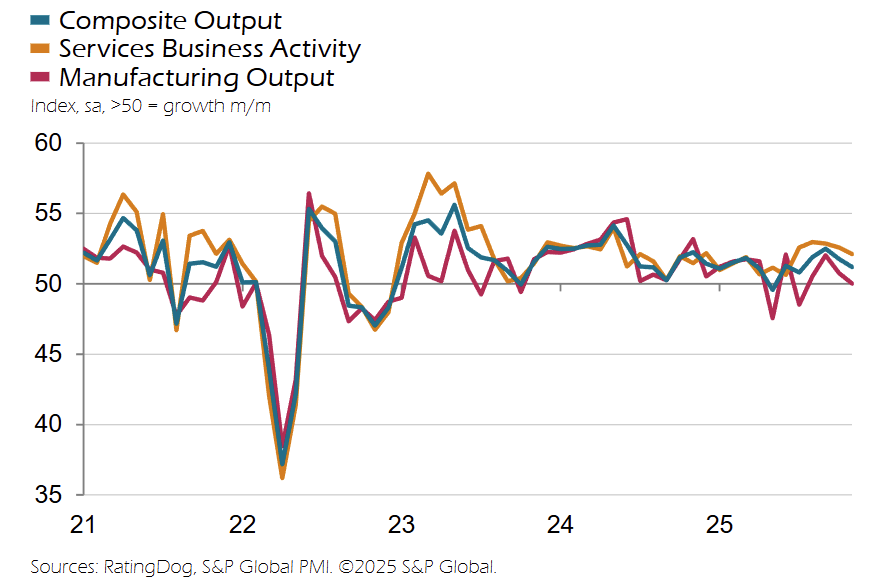

The Composite PMI Output Index rose to 55.4 in February (Jan: 51.6), signaling the fastest expansion in China’s private sector activity since May 2023 as both manufacturing and services output strengthened.

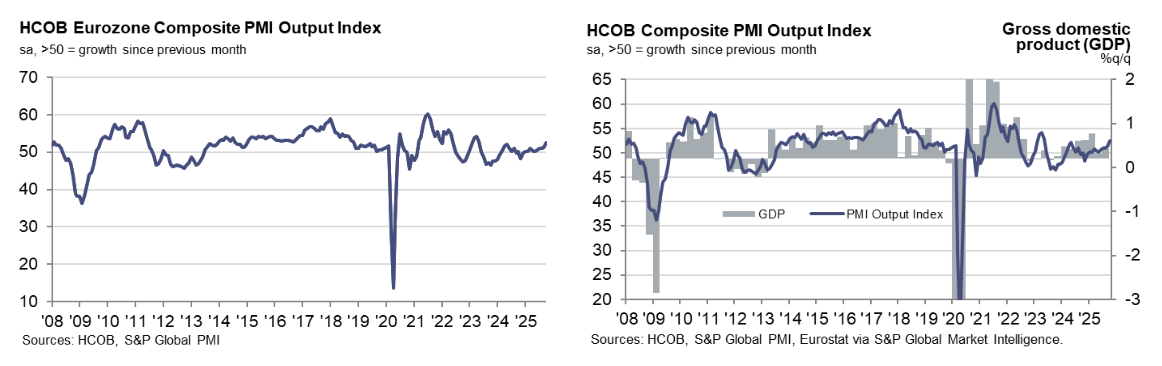

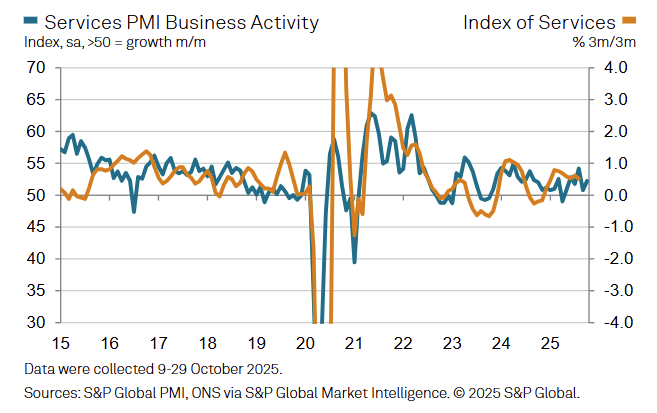

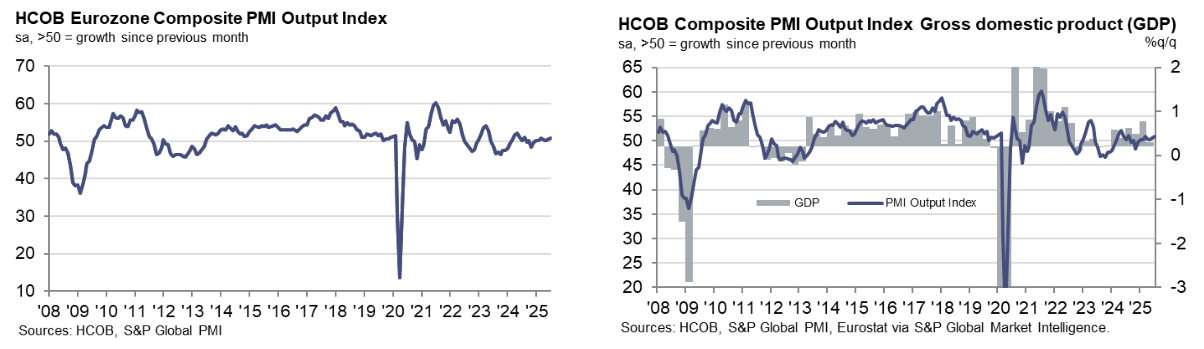

Euro Area

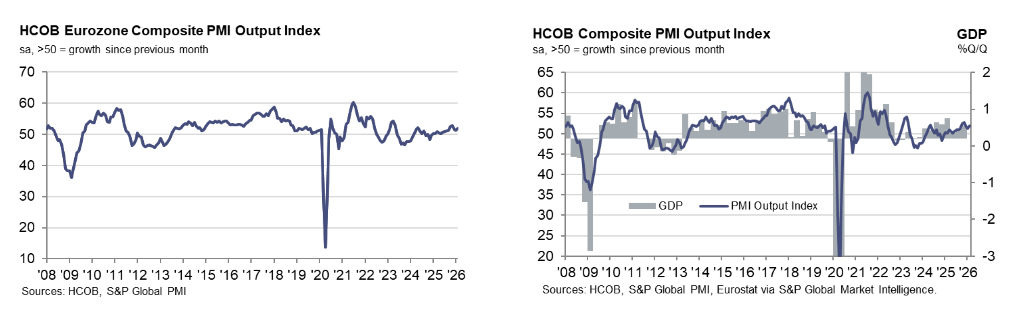

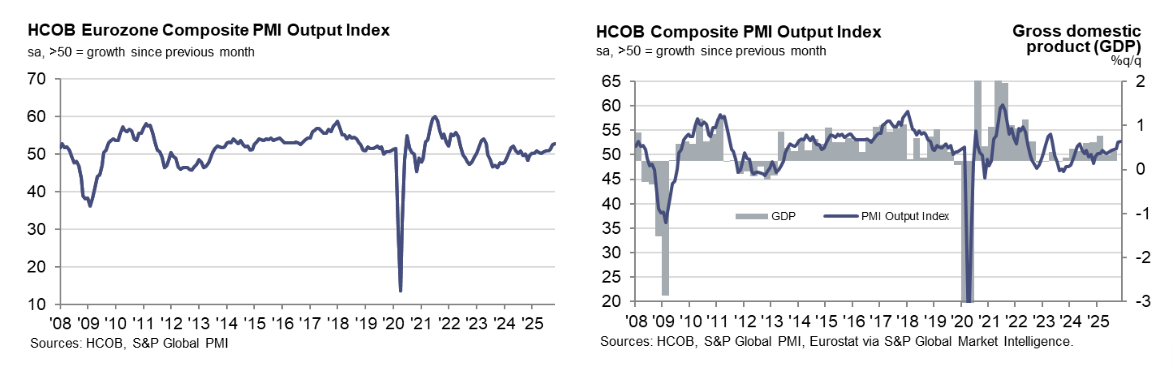

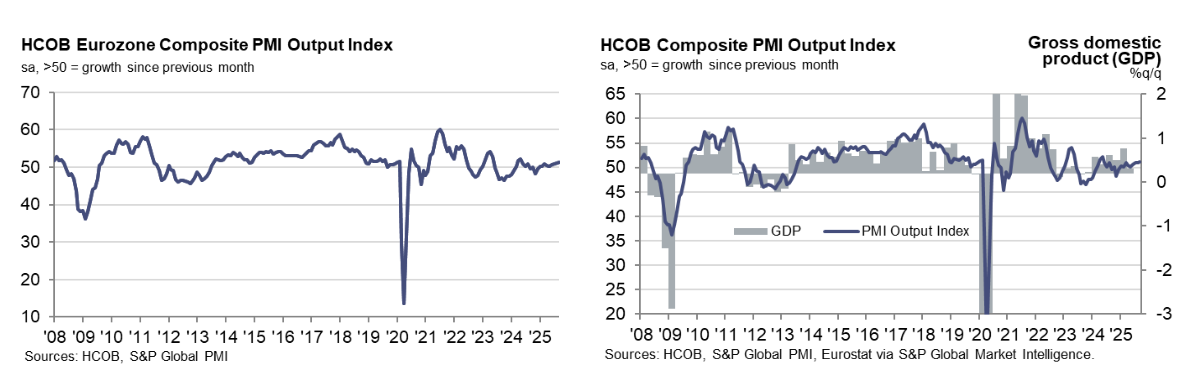

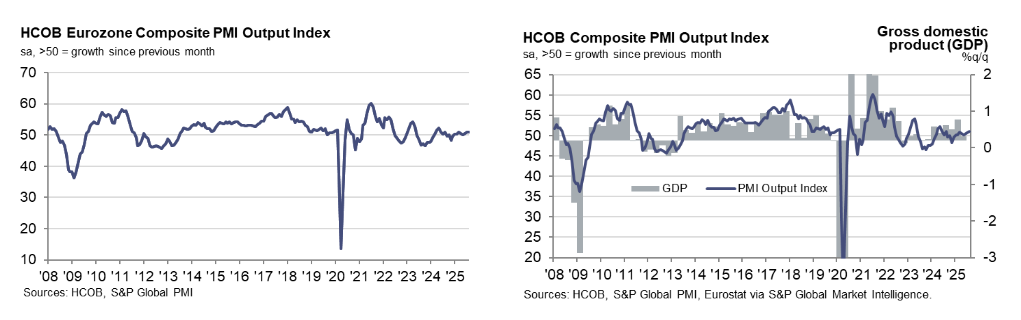

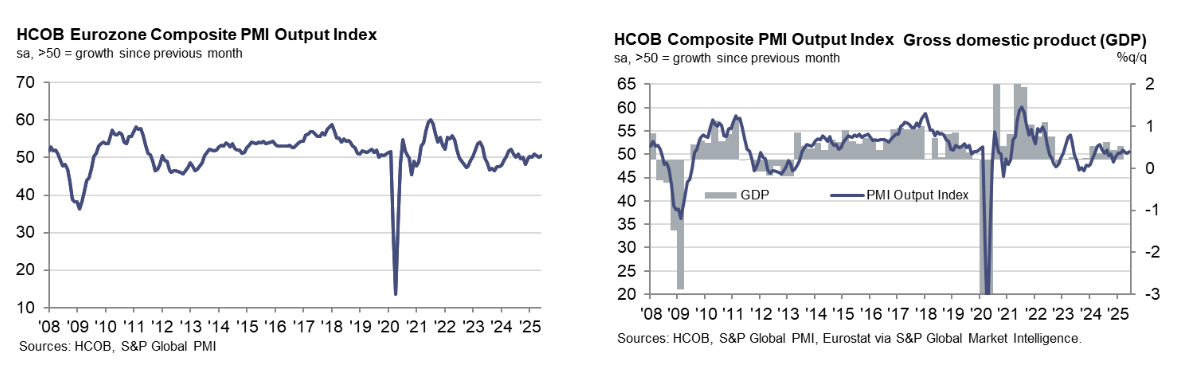

The HCOB Eurozone Composite PMI Output Index rose to 51.9 in February (+0.6 pts MoM from 51.3), a three-month high that signaled a slightly faster expansion in private sector activity as demand for goods and services improved.

-

The Composite PMI increased to 51.9 (Jan: 51.3), marking the quickest growth in three months and extending the eurozone’s current private sector expansion to 14 consecutive months.

-

Services activity strengthened modestly as the Services PMI Business Activity Index rose to 51.9 (Jan: 51.6), a two-month high, although the pace of expansion remained slightly below the survey’s long-run average.

-

New orders increased at a modest but faster pace in February, extending the current sequence of rising sales to seven months, with growth driven primarily by domestic demand.

-

New export business declined marginally again, indicating that external demand remained weak even as domestic order books improved.

-

Backlogs of work continued to decline, though only marginally and at the slowest rate since October, suggesting spare capacity persisted even as output expanded.

-

Employment levels were broadly unchanged across the eurozone private sector, marking another month with virtually no job creation despite continued growth in business activity.

-

Input costs rose at the fastest rate since April 2023, indicating intensifying cost pressures across the private sector as operating expenses accelerated for a fourth consecutive month.

-

Output price inflation eased slightly from January but remained the second-steepest in a year, while business confidence improved to its highest level since May 2024, reflecting stronger expectations for activity in the coming year.

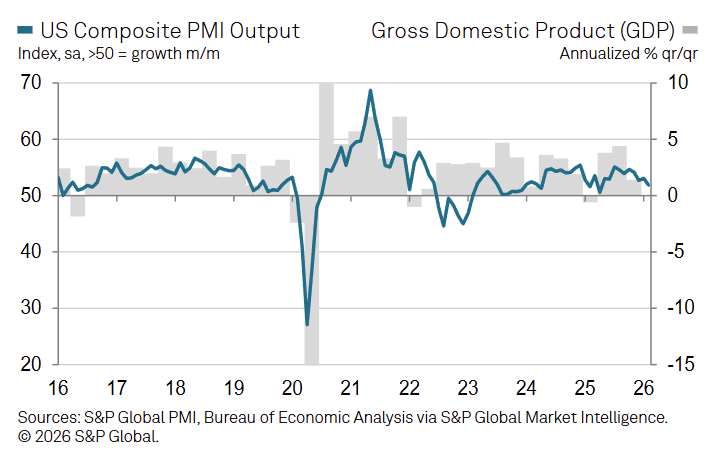

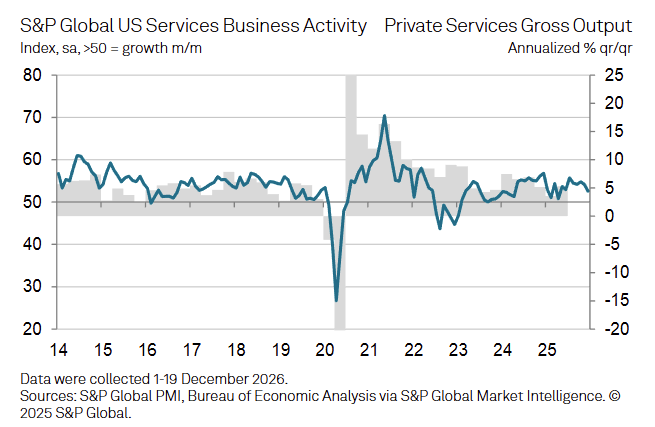

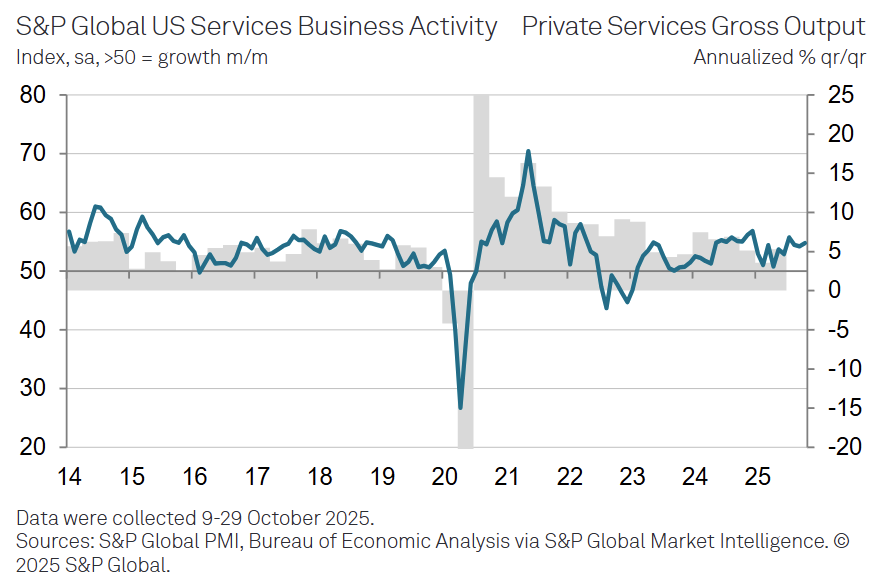

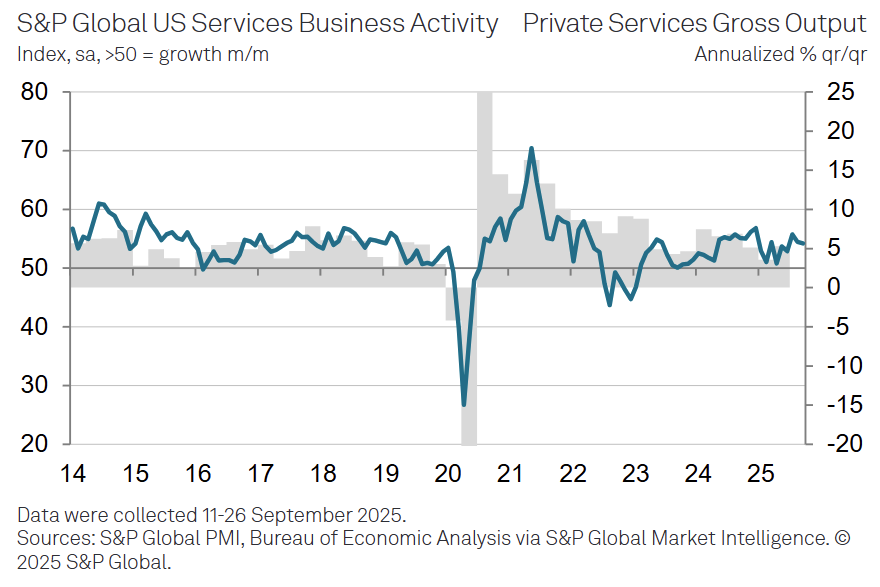

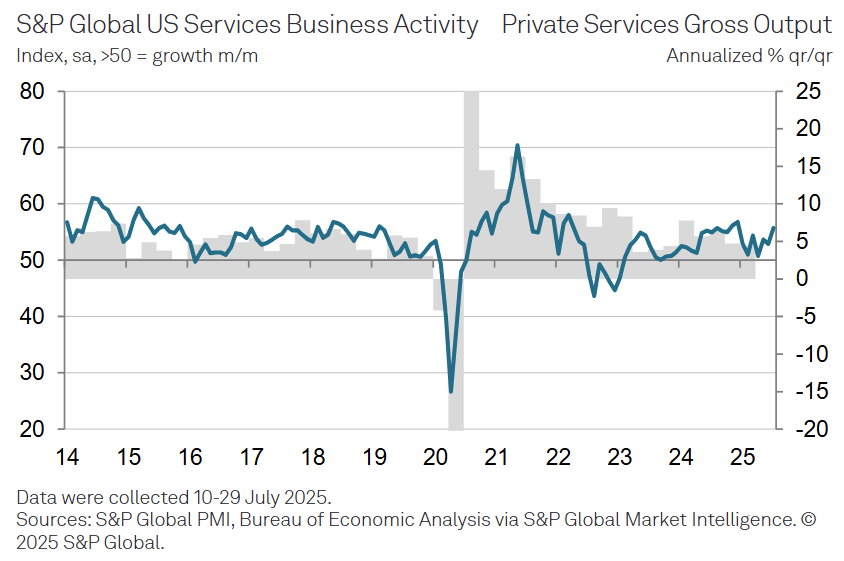

US

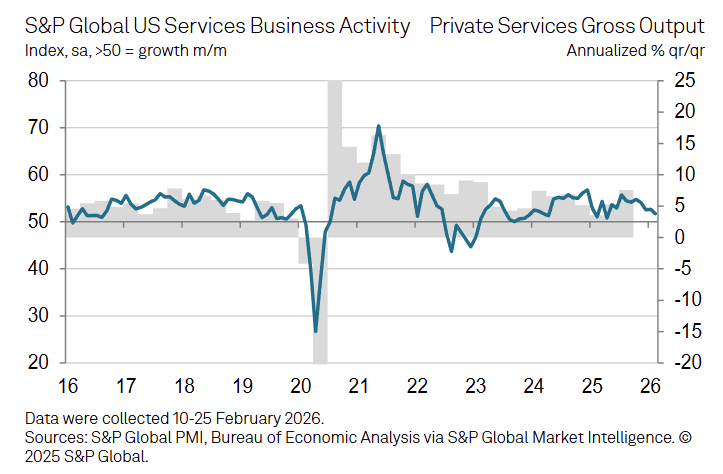

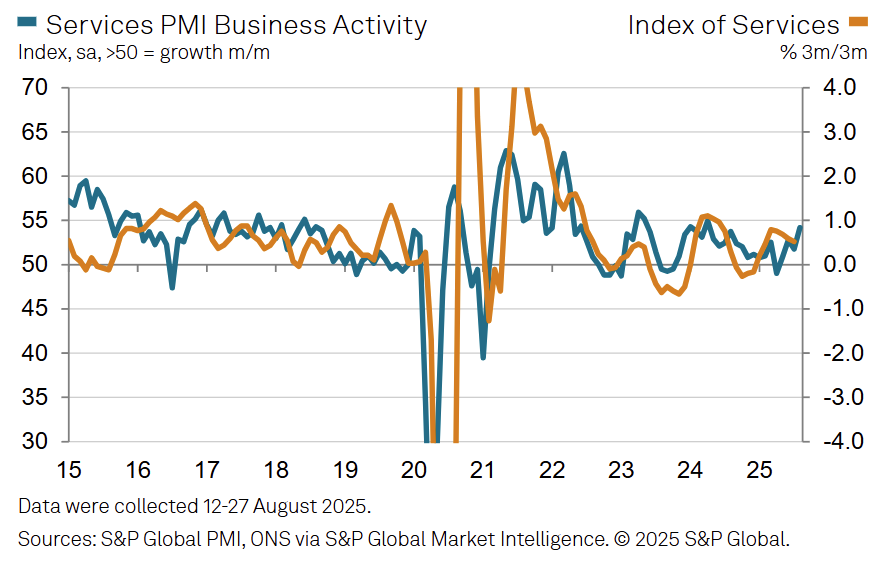

The S&P Global U.S. Services PMI Business Activity Index fell to 51.7 in February (-1.0 pts MoM from 52.7), signaling the slowest services sector expansion in ten months amid weaker demand and adverse weather effects.

-

Services activity slowed to 51.7 in February (Jan: 52.7) but remained above the 50 expansion threshold, extending the sector’s current growth streak to thirty-seven consecutive months.

-

New business increased for the twenty-second straight month, though the pace of growth cooled from January as adverse weather and uncertainty around tariffs and government policies constrained demand.

-

Export demand weakened further, with new export business declining marginally and extending the current contraction in international orders to three consecutive months.

-

Outstanding business increased at a steeper pace as activity growth lagged behind new orders, marking a continued accumulation of backlogs that has now persisted for one year.

-

Employment rose for a second successive month, but hiring remained fractional as firms primarily filled existing vacancies while broader hiring activity was limited by cost-cutting measures.

-

Input costs rose sharply in February, driven largely by higher labor-related expenses and tariff-related cost pressures reported by survey participants.

-

Selling prices increased at a faster pace during the month as service providers passed higher operating costs through to customers.

-

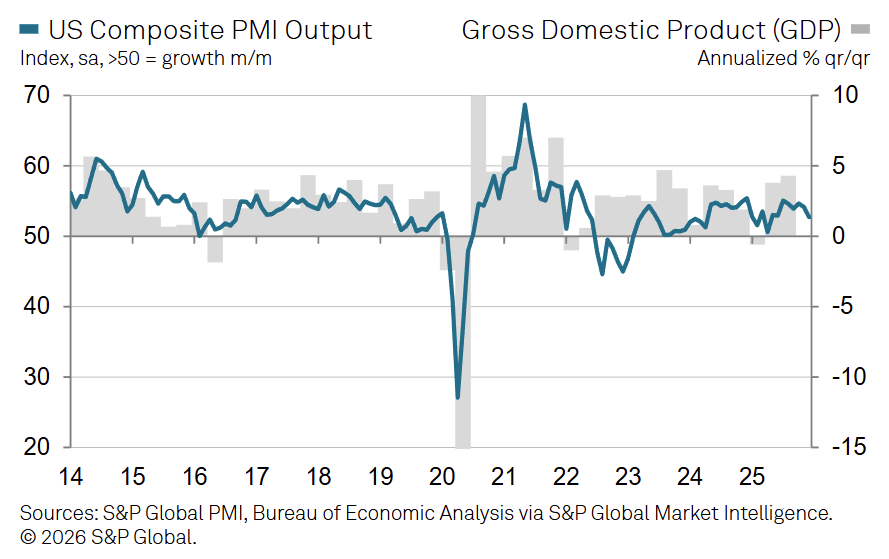

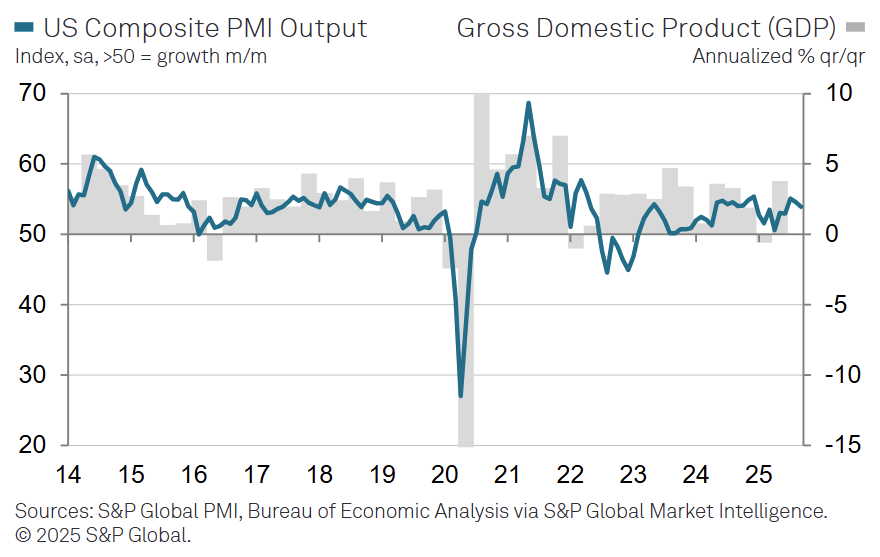

The S&P Global U.S. Composite PMI Output Index fell to 51.9 in February (Jan: 53.0), indicating slower overall private sector growth as both manufacturing and services output expansions moderated.

-

Global - 2/4/2026

Asia Pacific

- Australia - 2/4/2026

- Singapore (Composite only) - 2/4/2026

- Hong Kong (Composite only) - 2/4/2026

- Japan - 2/4/2026

- China - 2/4/2026

- India - 2/4/2026

- Russia - 2/4/2025

- Kazakhstan - 2/4/2026

Africa & Middle East

- Nigeria (Composite only) - 2/2/2026

- Qatar (Composite only) - 2/4/2026

- Kuwait (Composite only) - 2/4/2026

- Egypt (Composite only) - 2/4/2026

- UAE (Composite only) - 2/4/2026

- Uganda (Composite only) - 2/4/2026

- South Africa (Composite only) - 2/4/2026

- Lebanon (Composite only) - 2/4/2026

- Ghana (Composite only) - 2/4/2026

- Zambia (Composite only) - 2/4/2026

- Saudi Arabia (Composite only) - 2/4/2026

- Mozambique (Composite only) - 2/5/2026

- Kenya (Composite only) - 2/4/2026

Europe

- Ireland - 2/5/2026

- Spain - 2/4/2026

- Italy - 2/4/2026

- France - 2/4/2026

- Germany - 2/4/2026

- Eurozone - 2/4/2026

- UK - 2/4/2026

North & South America

Key Results

Australia

Australia’s Services PMI rose +5.2 pts MoM to 56.3 in January, the highest level since February 2022, extending the expansion streak to two consecutive years.

-

New business increased at the fastest pace since April 2022 for a third straight month, supported by stronger domestic demand and improved overseas orders.

-

Employment growth accelerated to its strongest rate since September, as firms added staff to manage higher workloads and rising outstanding work.

-

Backlogs of work increased again despite higher staffing levels, indicating labour constraints alongside stronger demand conditions.

-

Input costs continued to rise but inflation eased to the lowest level in 14 months, reflecting softer cost pressures than in December.

-

Output price inflation also slowed to a two-month low, pointing to reduced pass-through of costs to customers.

-

Business confidence declined to its lowest level since October 2024, despite stronger activity, reflecting concerns about the economic outlook and competition.

-

The Composite Output Index climbed to 55.7 (Dec: 51.0), the strongest expansion in 45 months, showing broad-based private sector growth driven by both services and manufacturing.

Japan

Japan’s Services PMI jumped to 53.7 in January, up from 51.6 in December, the strongest expansion in 11 months, indicating a solid acceleration in service sector output.

-

Business activity increased for a tenth consecutive month, showing a sustained run of monthly growth across Japanese services firms.

-

New business expanded at the fastest pace in four months, supported by marketing efforts, new client wins, and a more pronounced improvement in foreign demand.

-

Backlogs of work rose at the quickest rate since September, reflecting stronger inflows of new orders and rising pressure on existing capacity.

-

Employment continued to increase solidly, as firms added staff to manage higher workloads, extending the recent trend of job creation in services.

-

Input cost inflation eased to the softest pace in nearly two years, pointing to a cooling in expense pressures despite still-elevated costs.

-

Selling price inflation accelerated to a seven-month high, suggesting firms were increasingly passing higher costs through to customers.

-

Business sentiment remained positive but slipped to the lowest level since July, with concerns cited around global conditions, labour shortages, and tourism trends.

-

The Composite PMI increased to 53.1 in January, up from 51.1 in December, such that overall business activity expanded at the fastest rate since May 2023.

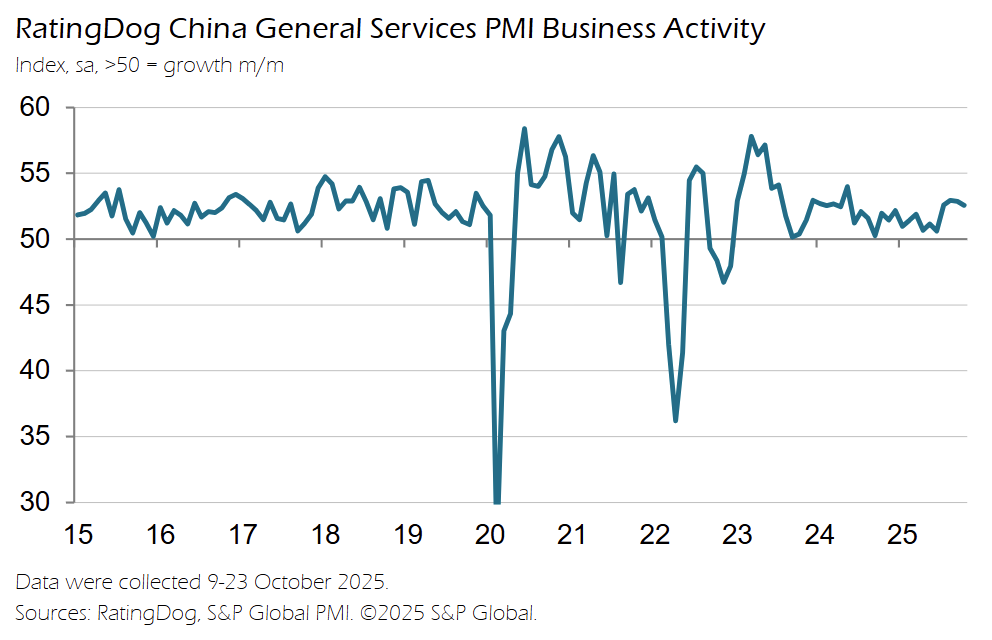

China

China’s General Services PMI increased to 52.3 in January, up from 52.0 in December, marking the fastest rise in services activity in three months and extending the expansion streak to just over three years.

-

New business growth accelerated for the first time in three months, supported by promotional activity, stronger client interest, and a renewed expansion in new export orders.

-

New export business returned to expansion after contracting in December, indicating a marginal recovery in external demand for Chinese services.

-

Employment rose for the first time in six months, representing only the fourth month of job growth over the past year as firms responded to stronger new work inflows.

-

Outstanding business continued to accumulate at a marginal pace, as increased labor capacity helped prevent a sharper build-up despite faster new order growth.

-

Input costs increased for an eleventh consecutive month but eased to a five-month low in inflation pace, pointing to softer cost pressures early in the year.

-

Output charges were broadly stable in January, showing little change in selling prices even as input costs continued to rise.

-

The Composite Output Index climbed to 51.6 (Dec: 51.3), reflecting a modest acceleration in overall business activity across both manufacturing and services, alongside a first rise in composite output prices in 14 months.

Euro Area

The HCOB Eurozone Composite PMI Output Index fell -0.2 pts MoM to 51.3 in January, a four month low, indicating continued expansion but at the weakest pace since September as services growth softened.

-

The Services PMI Business Activity Index declined to 51.6 (Dec: 52.4), also a four month low, pointing to more modest growth in services output early in the year.

-

New business across the eurozone barely rose in January, with services new orders increasing at the weakest pace since August, reflecting near-flat demand conditions.

-

Backlogs of work decreased at the fastest rate in eight months, showing firms cleared outstanding orders more quickly as sales momentum slowed.

-

Private sector employment virtually stagnated, as manufacturing job losses offset a mild increase in services hiring after three months of overall expansion.

-

Input cost inflation accelerated for a third straight month to an 11 month high, indicating a renewed build-up in cost pressures across the eurozone economy.

-

Output charge inflation rose to the strongest rate in nearly a year, suggesting firms increased selling prices more aggressively alongside rising costs.

-

Business expectations improved to the strongest level since May 2024, even as confidence remained below the long-run average.

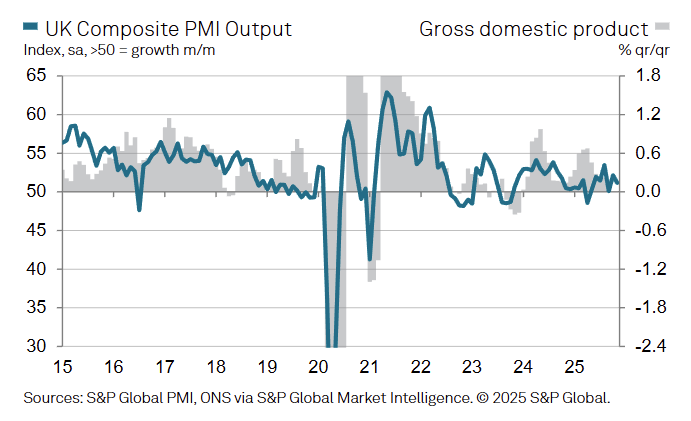

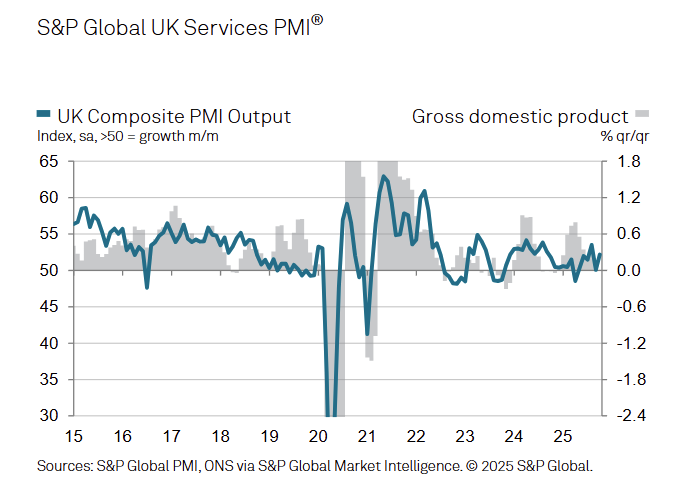

UK

The S&P Global UK Services PMI rose to 54.0 in January, up from 51.4 in December, the fastest expansion since August 2025 and a clear acceleration from the subdued pace seen in Q4 2025.

-

Total new business increased at a solid pace and reached a three-month high, indicating stronger order inflows even though growth remained below the long-run survey average.

-

New export orders rose modestly, posting the second fastest increase since October 2024, with firms citing stronger demand from European clients, particularly Ireland.

-

Employment continued to decline for a fourth consecutive month, extending the longest period of service sector job shedding in 16 years, with the pace of workforce reductions faster than in December.

-

Input cost inflation remained sharp but eased slightly from December’s seven-month high, driven primarily by higher payroll, technology, and raw material costs.

-

Output charges increased at the fastest rate since August 2025, showing firms raised prices more aggressively to offset rising business expenses.

-

Business optimism improved to the highest level since October 2024, with over half of firms expecting higher activity over the next 12 months despite ongoing concerns about costs and demand conditions.

-

The UK Composite PMI Output Index climbed to 53.7 (Dec: 51.4), the strongest reading since August 2024, reflecting faster growth across both services and manufacturing.

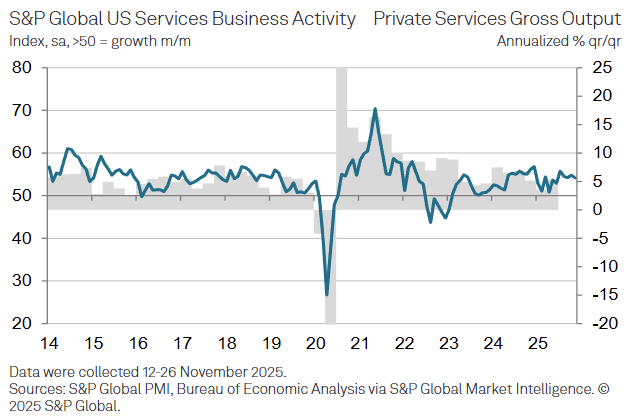

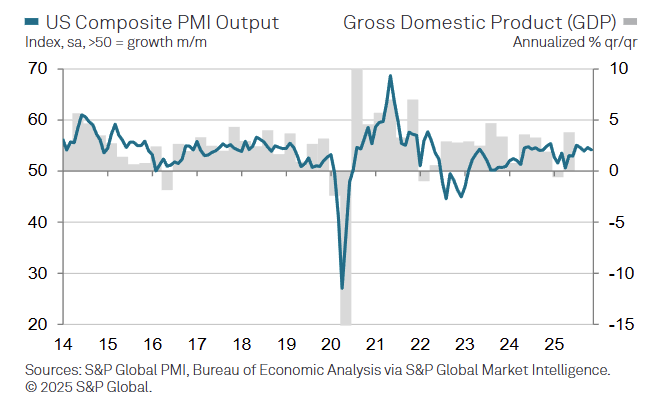

US

The S&P Global US Services PMI rose to 52.7 in January, up from 52.5 in December, extending the expansion streak to exactly three years, though growth remained below typical 2025 levels.

-

New business inflows strengthened at the start of 2026, supported by new client wins and improved domestic demand, even as low consumer confidence and uncertainty limited overall gains.

-

New export business fell sharply to the weakest level since November 2022, reflecting a steep reduction in foreign demand linked to tariffs and an uncertain trading environment.

-

Backlogs of work increased solidly for an eleventh consecutive month and at the fastest pace since July, indicating ongoing capacity pressures across service providers.

-

Employment rose marginally after December’s slight decline, showing modest hiring that remained weak relative to the long-term survey trend.

-

Input cost inflation remained elevated but eased to the slowest pace since October, driven by tariffs alongside higher payroll and supplier costs.

-

Output charges continued to rise but at a softer rate than in December, pointing to slower price increases amid competition despite still-high cost pressures.

-

The US Composite PMI Output Index increased to 53.0 (Dec: 52.7), signaling a firmer overall expansion across both services and manufacturing.

-

Global - 1/6/2026

Asia Pacific

- Australia - 1/5/2026

- Singapore (Composite only) - 1/6/2026

- Hong Kong (Composite only) - 1/6/2026

- Japan - 1/7/2026

- China - 1/5/2026

- India - 1/6/2026

- Russia - 12/30/2025

- Kazakhstan - 1/6/2026

Africa & Middle East

- Nigeria (Composite only) - 1/2/2026

- Qatar (Composite only) - 1/6/2026

- Kuwait (Composite only) - 1/6/2026

- Egypt (Composite only) - 1/6/2026

- UAE (Composite only) - 1/6/2026

- Uganda (Composite only) - 1/6/2026

- South Africa (Composite only) - 1/6/2026

- Lebanon (Composite only) - 1/7/2026

- Ghana (Composite only) - 1/6/2026

- Zambia (Composite only) - 1/6/2026

- Saudi Arabia (Composite only) - 1/5/2026

- Mozambique (Composite only) - 1/6/2026

- Kenya (Composite only) - 1/6/2026

Europe

- Ireland - 1/6/2026

- Spain - 1/6/2026

- Italy - 1/6/2026

- France - 1/6/2026

- Germany - 1/6/2026

- Eurozone - 1/6/2026

- UK - 1/6/2026

North & South America

Key Results

China

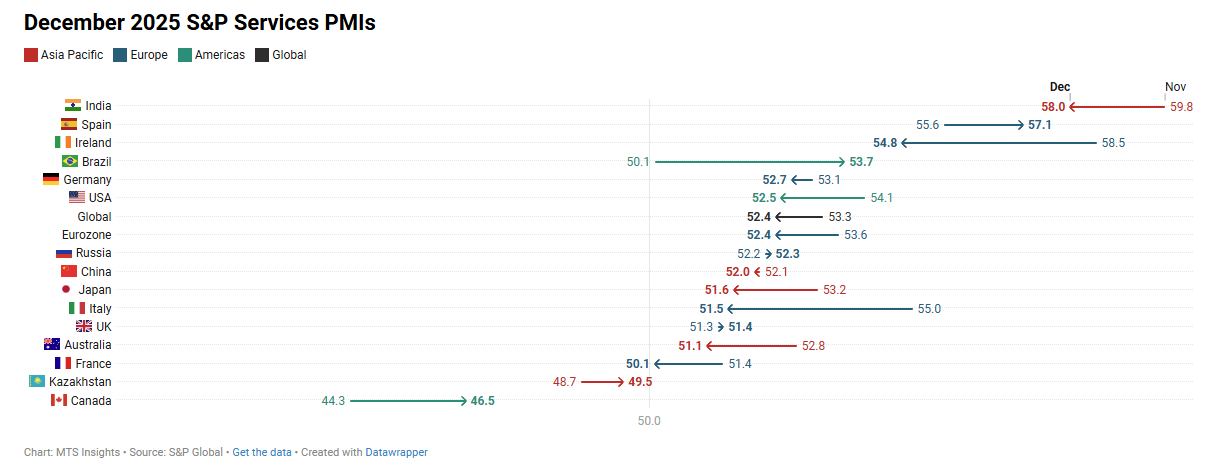

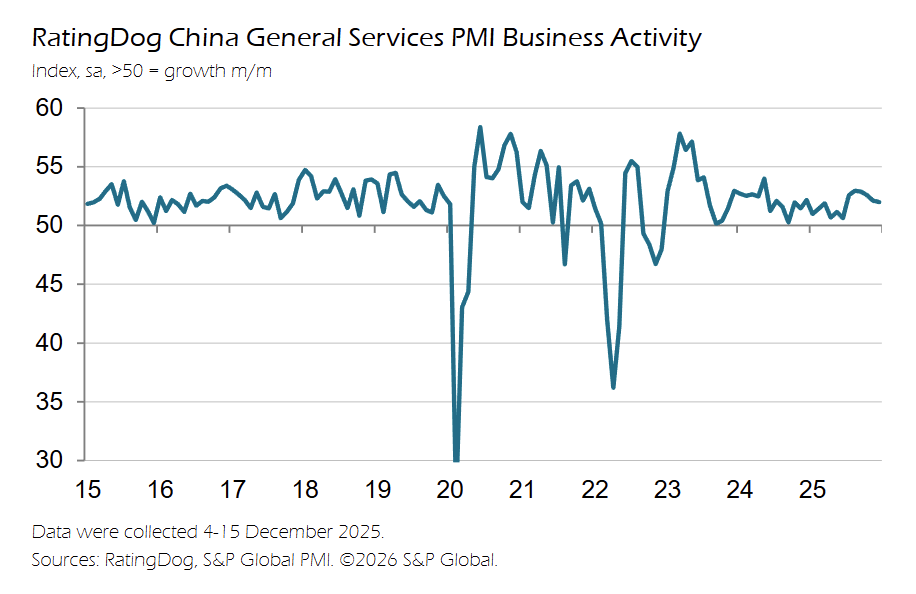

China’s RatingDog General Services Business Activity Index eased to 52.0 in December (from 52.1 in November), marking the slowest services expansion since June amid softer new orders growth and continued job shedding.

-

Services activity remained in expansion at 52.0 (Nov: 52.1), extending the services growth run to three years, but with a modest pace that was the softest in six months.

-

New business increased again, supported by promotions and improved customer interest, but the rate of growth slowed to a six-month low as new export business contracted after a brief improvement in November.

-

New export business fell in December, with respondents citing reduced tourist numbers, contrasting with the prior month’s increase in overseas sales.

-

Employment declined for a fifth straight month, with firms citing cost concerns and restructuring, and the reduced workforce capacity contributed to a slight rise in outstanding business.

-

Input prices rose for a tenth consecutive month, driven by higher raw material and wage costs, with inflation described as among the highest seen in 2025 despite remaining modest.

-

Output charges declined as firms lowered prices to support sales amid intense competition, indicating limited pricing power even as input costs increased.

-

Business sentiment improved to a nine month high, linked to expectations of stronger market conditions and expansion plans for 2026, though confidence remained below the survey’s long run average.

-

The Composite Output Index edged up to 51.3 (Nov: 51.2), indicating a seventh consecutive month of overall private sector expansion supported by higher services activity and a renewed increase in factory production, while overall selling prices continued to fall despite slightly firmer cost pressures.

Euro Area

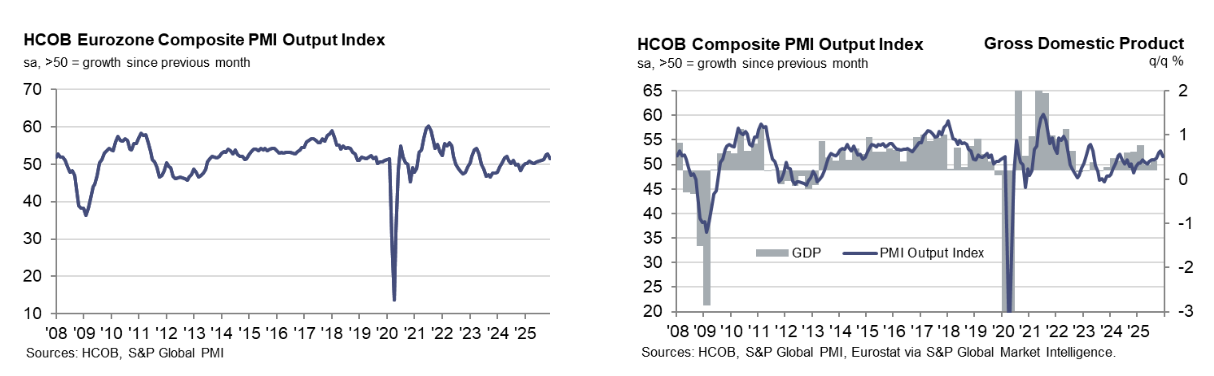

The HCOB Eurozone Composite PMI Output Index eased to 51.5 in December (from 52.8 in November), marking slower private-sector growth but rounding out the strongest quarterly expansion since Q2 2023.

-

The Composite PMI fell -1.3 pts MoM to 51.5, a three-month low, indicating continued expansion but at the weakest pace since September as momentum softened late in the year.

-

The three-month average Composite PMI for Q4 stood at 52.3, the highest since Q2 2023, underscoring that December’s slowdown followed a solid quarter overall.

-

Services activity remained expansionary but cooled, with the Services PMI Business Activity Index slipping to 52.4 (from 53.6), also a three-month low, reflecting softer demand growth.

-

New business rose for a fifth consecutive month, but the pace slowed to the weakest since September, as faster declines in manufacturing orders offset a softer increase in services sales.

-

New export business contracted more sharply, falling to the greatest extent since March 2025, indicating weaker demand from non-domestic clients.

-

Backlogs of work declined at the fastest pace in three months, showing firms made quicker progress clearing outstanding orders amid softer demand pressures.

-

Employment increased marginally and at a slightly faster rate than in November, with job gains in services offset by continued cutbacks in manufacturing.

-

Input cost inflation accelerated to a nine-month high, while output price inflation was unchanged from November and remained among the weakest since October 2024, indicating rising cost pressures without faster pass-through.

UK

The S&P Global UK Services PMI edged up to 51.4 in December (from 51.3 in November), indicating continued but marginal expansion amid subdued demand conditions.

-

Business activity rose for an eighth consecutive month, but at 51.4 remained well below the long-run average of 54.2 and slightly weaker than the earlier flash estimate of 52.1, showing persistently soft growth momentum.

-

Total new work returned to expansion after a marginal decline in November, with the pace of growth modest but faster than the 2025 average, pointing to a tentative improvement in demand.

-

New export business increased moderately, ending a three-month contraction, with respondents citing stronger demand from the US but continued weakness in EU markets.

-

Backlogs of work increased for the first time since May 2023, reflecting higher-than-expected new business and some renewed capacity pressures, including supplier delays.

-

Employment fell for a fifteenth consecutive month, as around 21% of firms reported staff reductions versus 12% reporting increases, though the pace of job cuts eased compared with November.

-

Input cost inflation accelerated to a seven-month high, driven mainly by wage pressures and higher fuel costs, indicating rising cost burdens across the service sector.

-

Output charges rose at the fastest pace in four months, rebounding from November’s near five-year low despite reports of squeezed margins and limited pricing power.

-

The UK Composite PMI Output Index ticked up to 51.4 (from 51.2), marking an eighth straight month of private-sector expansion, supported by a modest rebound in total new work but ongoing declines in employment.

US

The S&P Global US Services PMI fell to 52.5 in December (from 54.1 in November), signaling slower services activity growth amid cooling demand late in the year.

-

Business activity remained in expansion for a 35th consecutive month, but December marked the slowest growth rate in eight months, reflecting softer momentum as 2025 closed.

-

New business rose only marginally, the weakest increase in 20 months, as firms cited squeezed client budgets, demand uncertainty, and tariff-related instability, particularly for foreign orders.

-

New export business declined for the second time in three months, with the pace of contraction the steepest since May, highlighting external demand softness.

-

Employment edged down slightly, ending a nine-month run of job growth, as cost pressures, budget constraints, and slower demand limited hiring despite modest increases in backlogs.

-

Input cost inflation accelerated to a seven-month high, driven by tariffs, higher supplier charges, and labor-related expenses, remaining well above the historical average.

-

Selling prices rose at a faster pace as firms attempted to pass through higher costs, marking the strongest increase since August and underscoring margin pressure.

-

The US Composite PMI eased to 52.7 (Nov: 54.2), consistent with slower growth across both services and manufacturing while remaining above the 50 threshold.

-

Global - 12/3/2025

Asia Pacific

- Australia - 12/2/2025

- Singapore (Composite only) – 12/3/2025

- Hong Kong (Composite only) – 12/3/2025

- Japan – 12/3/2025

- China – 12/3/2025

- India – 12/3/2025

- Russia – 12/3/2025

- Kazakhstan – 12/3/2025

Africa & Middle East

- Nigeria (Composite only) - 12/1/2025

- Qatar (Composite only) - 12/3/2025

- Kuwait (Composite only) - 12/3/2025

- Egypt (Composite only) - 12/3/2025

- UAE (Composite only) - 12/5/2025

- Uganda (Composite only) – 12/3/2025

- South Africa (Composite only) – 12/3/2025

- Lebanon (Composite only) – 12/4/2025

- Ghana (Composite only) – 12/3/2025

- Zambia (Composite only) – 12/3/2025

- Saudi Arabia (Composite only) – 12/3/2025

- Mozambique (Composite only) – 12/3/2025

- Kenya (Composite only) – 12/3/2025

Europe

- Ireland – 12/3/2025

- Spain – 12/3/2025

- Italy – 12/3/2025

- France – 12/3/2025

- Germany – 12/3/2025

- Eurozone – 12/3/2025

- UK – 12/3/2025

North & South America

Key Results

Highlights and lowlights:

- Kenya's private sector growth was the strongest in over five years in November with its S&P Composite PMI at 55.0.

- Egypt's S&P Composite PMI increased to 51.1 in November, up from 49.2 in October and the highest reading since October 2020. S&P: "Historically, a PMI reading of 51.1 correlates with gross domestic product growing at an annual rate of more than 5%."

- The Italian service sector saw the strongest expansion in 2.5 years with an S&P Services PMI reading up 1.0 pt to 55.0 in November. Additionally, new business growth was the strongest in 19 months. A strong services reading led the S&P Composite PMI to rise 0.7 pts to 53.8, the strongest in over 2.5 years.

- France's S&P Services and Composite PMIs return to expansion territory for the first time in 15 months, rising 3.4 pts to 51.4 and 2.7 pts to 50.4, respectively.

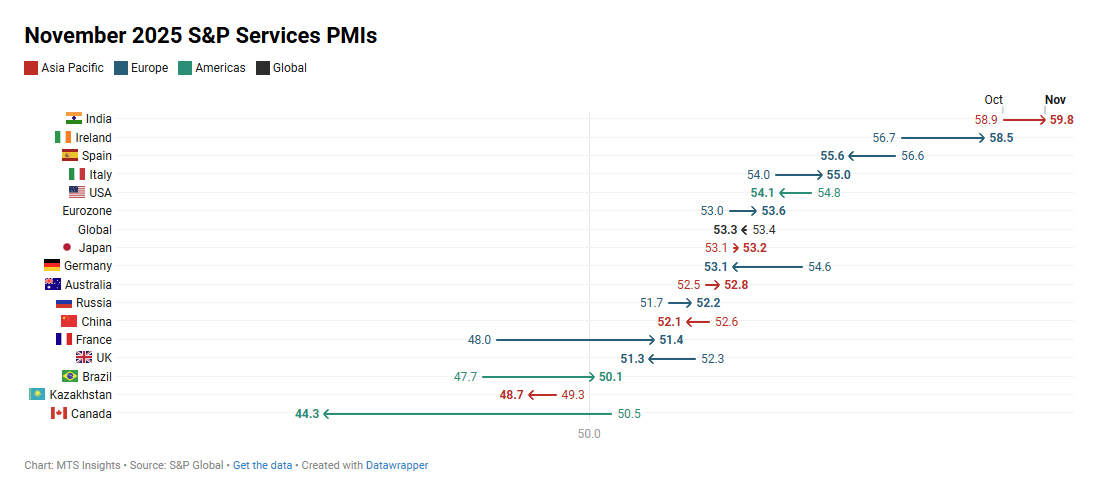

China

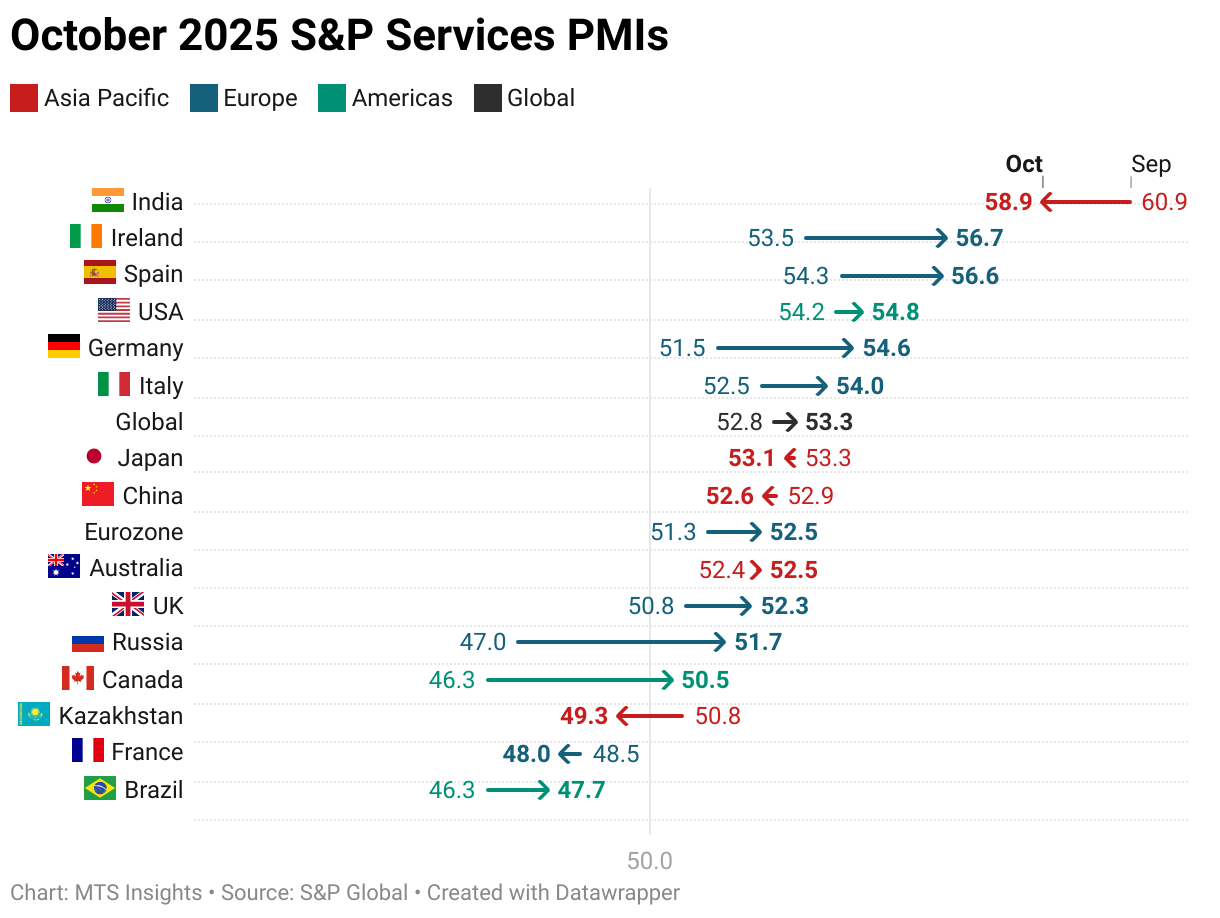

China’s RatingDog General Services Business Activity Index slipped to 52.1 in November (from 52.6 in October), marking the softest expansion in five months but still indicating ongoing growth in services activity.

-

New business rose at a slower pace, though growth remained solid, supported by increased client enquiries and renewed strength in new export orders after a mild decline in October.

-

Employment contracted again as firms cited non-replacement of leavers and cost-driven redundancies, contributing to a further rise in outstanding work, which accumulated at the fastest rate in three months.

-

Input prices increased for the ninth consecutive month, driven by higher materials, office supplies, and energy costs; providers raised output charges only fractionally to ease cost pressures.

-

Business confidence stayed positive but fell to one of the lowest levels on record, even as firms expressed hopes for better market conditions and expansion plans in the year ahead.

The Composite Output Index eased to 51.2 (from 51.8), showing a sixth straight month of growth but at a four-month low as manufacturing output stagnated and services growth moderated.

-

Total new business rose more slowly in the composite survey as well, despite another increase in new export orders, pointing to softer demand momentum late in the year.

-

Composite input costs increased for a fifth consecutive month, while output charges continued to fall, indicating persistent margin pressure across the broader private-sector economy.

Euro Area

The HCOB Eurozone Composite PMI rose to 52.8 in November (from 52.5 in October), a 30-month high that reflects the fastest private sector expansion since mid-2023.

-

The Services PMI strengthened to 53.6 (from 53.0), also a 30-month high, showing the strongest services output growth since May 2023 and faster demand gains for a fourth straight month.

-

New business increased again at a solid rate, matching October’s two-and-a-half-year high, with all of the expansion concentrated in services as manufacturing orders fell slightly.

-

Backlogs of work declined after stabilizing in October, with manufacturers seeing a sharper depletion than services firms due to weaker factory demand.

-

Employment rose for the eighth time in nine months but at only a fractional pace; job creation was entirely driven by services while factory employment fell at the fastest rate since April.

-

Business confidence improved across both sectors, though expectations remained below their long-run average, indicating firms were cautiously optimistic.

-

Input price inflation picked up to an eight-month high amid rising manufacturing costs and faster services-sector expenses, while output charge inflation eased to a six-month low as firms made smaller price increases.

-

Country detail showed broad expansion: Ireland led at 55.8, Spain followed at 55.1, Italy reached a 31-month high at 53.8, Germany moderated to 52.4, and France posted its first expansion in 15 months at 50.4.

UK

The S&P Global UK Services PMI fell -1.0 pt to 51.3 in November (from 52.3 in October), indicating only marginal growth amid softer demand and rising cost pressures.

-

New business declined for the first time since July, with firms citing subdued domestic confidence and weaker foreign demand; export sales fell at the fastest rate since June due to global competition and geopolitical uncertainty.

-

Employment dropped at the quickest pace since February, extending the sequence of workforce reductions that began in October 2024 as firms cut staff amid lower workloads and elevated payroll costs.

-

Input cost inflation accelerated, driven by higher salaries, food and raw materials, energy, fuel, and insurance costs; around 29% of firms reported rising cost burdens versus 2% reporting declines.

-

Output charges rose only marginally, and prices charged inflation eased to the lowest reading since January 2021, reflecting intense price competition and weak sales pipelines.

-

Business confidence remained positive overall, with about half expecting higher activity over the next year, but optimism slipped below the post-pandemic trend due to policy uncertainty and concerns over the UK outlook.

The UK Composite PMI edged down to 51.2 (from 52.2), marking slower private sector expansion as modest service-sector growth and rising manufacturing output were offset by a fractional drop in total new work.

-

Backlogs continued to fall and contributed to reduced hiring, while firms noted delays in investment decisions ahead of the Budget as a headwind to business activity.

US

The S&P Global US Services PMI slipped -0.7 pts to 54.1 in November (from 54.8 in October), marking a five-month low but still signaling solid above-trend expansion.

-

New business rose at the strongest pace since December 2024, supported by more favorable market conditions, although export growth remained marginal and continued to lag amid international uncertainty.

-

Confidence improved noticeably, with firms citing the end of the government shutdown and expectations of higher federal spending, alongside plans for new products and increased advertising.

-

Employment increased at the fastest rate since June, extending the hiring streak that began in March; backlogs rose for a ninth month, indicating ongoing capacity pressure despite slower accumulation than over the summer.

-

Input cost inflation accelerated to a six-month high, driven by higher labor costs and tariff-related expenses, and remained above trend for a second month.

-

Output prices rose at a faster pace as firms attempted to pass through higher operating costs, though competitive pressures continued to limit pricing power.

The US Composite PMI registered 54.2 (vs 54.6 in October), little changed overall and consistent with trend private-sector growth, with similar expansion across services and manufacturing.

-

Composite new business posted the strongest increase in three months, while input cost inflation reached a four-month high and output charges rose at a firmer rate.

-

Global - 11/5/2025

Asia Pacific

- Australia - 11/4/2025

- Singapore (Composite only) – 11/5/2025

- Hong Kong (Composite only) – 10/6/2025

- Japan – 11/6/2025

- China – 11/5/2025

- India – 11/6/2025

- Russia – 11/6/2025

- Kazakhstan – 11/5/2025

Africa & Middle East

- Nigeria (Composite only) - 11/3/2025

- Qatar (Composite only) - 11/4/2025

- Kuwait (Composite only) - 11/4/2025

- Egypt (Composite only) - 11/4/2025

- UAE (Composite only) - 11/5/2025

- Uganda (Composite only) – 11/5/2025

- South Africa (Composite only) – 11/5/2025

- Lebanon (Composite only) – 11/5/2025

- Ghana (Composite only) – 11/5/2025

- Zambia (Composite only) – 11/5/2025

- Saudi Arabia (Composite only) – 11/4/2025

- Mozambique (Composite only) – 11/5/2025

- Kenya (Composite only) – 11/5/2025

Europe

- Ireland – 11/5/2025

- Spain – 11/5/2025

- Italy – 11/5/2025

- France – 11/5/2025

- Germany – 11/5/2025

- Eurozone – 11/5/2025

- UK – 11/5/2025

North & South America

Key Results

China

China’s RatingDog General Services Business Activity Index eased -0.3 pts to 52.6 in October 2025 (from 52.9 in September), marking continued but softer expansion; the Composite Output Index also slipped to 51.8 (from 52.5), indicating slower overall private sector growth.

-

New business growth accelerated, supported by new product launches and client wins, but new export orders fell modestly amid greater global trade uncertainty.

-

Backlogs of work declined for the first time in seven months, with firms citing better efficiency and reduced capacity pressure.

-

Employment contracted again as companies avoided replacing leavers and implemented selective redundancies driven by cost concerns.

-

Input prices rose for an eighth straight month and at the fastest pace in a year, reflecting higher raw material and wage costs.

-

Output charges fell fractionally, the second drop in three months, as firms absorbed costs and discounted to compete.

-

Business confidence remained positive but weakened slightly, with firms still expecting growth while noting tougher competition and trade risks.

-

Composite detail: total new business expanded at a slower rate, job shedding persisted for a third month, cost pressures intensified, and both goods and services producers lowered selling prices, pointing to margin pressure across the private economy.

Euro Area

The HCOB Eurozone Composite PMI rose +1.3 pts to 52.5 in October 2025 (from 51.2 in September), marking the fastest private sector expansion since May 2023, supported by stronger domestic demand and rising employment.

-

Services PMI climbed to 53.0 (from 51.3), a 17-month high, signaling robust growth in the services sector and solid acceleration in new business volumes.

-

New business expanded at the sharpest pace in 2½ years, entirely driven by services as manufacturing orders were stagnant but improved from September’s decline.

-

Employment growth quickened to a 16-month high, driven by stronger hiring in services that offset faster factory job shedding.

-

Outstanding orders were unchanged, suggesting firms managed workloads effectively amid higher capacity.

-

Input cost inflation eased for the second month and fell below its long-term average, but output prices rose at the fastest rate in seven months as firms lifted charges more aggressively.

-

Business confidence stayed positive but softened slightly across both manufacturing and services, reflecting some caution despite stronger growth.

-

By country, Spain (56.0) led the euro area with the sharpest 10-month activity increase, followed by Germany (53.9), Ireland (53.7), and Italy (53.1), while France (47.7) fell further into contraction.

-

HCOB’s chief economist noted that the eurozone’s recovery is broadening, led by Germany’s sharp service-sector rebound and resilient growth across other economies, though France remains a drag amid political uncertainty.

UK

The S&P Global UK Services PMI rose +1.5 pts to 52.3 in October 2025 (from 50.8 in September), marking the strongest expansion in six months as domestic demand strengthened and business confidence improved to a 12-month high.

-

New business increased at the second-fastest pace since October 2024, driven by rising domestic orders, marketing efforts, and new product launches; however, export sales declined for a second month due to weak global demand.

-

Employment fell slightly, but the rate of decline was the slowest in a year, with firms noting better order books and some resumption of hiring amid cost controls.

-

Input cost inflation eased to its lowest level since November 2024, though wage, energy, and food costs remained elevated.

-

Output prices rose at the weakest pace since June, as firms limited price increases amid stronger competition and reduced cost pressure.

-

Business confidence reached its highest level since October 2024, supported by lower borrowing costs, investment in new technologies, and improved sales pipelines.

-

The Composite PMI climbed to 52.2 (from 50.1), confirming the sixth consecutive month of overall private-sector growth, with services leading and manufacturing output rising for the first time in a year.

-

S&P Global’s Tim Moore noted that October’s rebound reflected resilient domestic demand, slower job cuts, and easing inflation, though uncertainty around the broader UK outlook continued to weigh on sentiment.

US

The S&P Global US Services PMI rose +0.6 pts to 54.8 in October 2025 (from 54.2 in September), marking the 33rd straight month of expansion and signaling solid momentum in service activity at the start of Q4.

-

New business increased at a slightly faster rate, supported by stronger client demand and inquiries, though new export orders declined marginally for the sixth time in seven months amid trade-related uncertainty.

-

Backlogs of work rose for an eighth month but only marginally, the slowest increase since March, suggesting firms managed workloads effectively amid rising activity.

-

Employment expanded for the eighth consecutive month, with hiring focused on sales and project support, though overall growth was modest due to cost controls and limited replacement of departing staff.

-

Input costs continued to rise sharply—driven by tariffs and labor expenses—but at the slowest pace in six months, easing overall cost pressure.

-

Selling price inflation moderated to the weakest since April, as firms absorbed cost increases amid competitive pricing and customer resistance to higher charges.

-

Business confidence fell to a six-month low, reflecting political and economic uncertainty, though firms noted that recent Fed rate cuts had improved sentiment slightly.

The S&P Global US Composite PMI rose +0.7 pts to 54.6 in October 2025 (from 53.9 in September), marking a modest acceleration in private sector growth driven by concurrent gains in manufacturing and services output.

-

New business expanded solidly, providing the main support to overall activity growth during the month.

-

Employment increased for a second month, though only modestly, as firms remained cautious amid weaker confidence in the outlook.

-

Business confidence fell to a six-month low, reflecting persistent uncertainty despite continued expansion in output and demand.

-

Input costs and selling prices both recorded their slowest increases since April, suggesting easing inflationary pressures across the private sector.

-

S&P Global’s Chris Williamson said the PMI data indicate that Q4 GDP growth is tracking near a 2.5% annualized rate, with financial and tech sectors leading expansion but profitability constrained by limited pricing power.

-

Global - 10/3/2025

Asia Pacific

- Australia - 10/2/2025

- Singapore (Composite only) – 10/3/2025

- Hong Kong (Composite only) – 10/6/2025

- Japan – 10/3/2025

- China – 10/3/2025

- India – 10/6/2025

- Russia – 10/3/2025

- Kazakhstan – 10/3/2025

Africa & Middle East

- Nigeria (Composite only) - 10/1/2025

- Qatar (Composite only) - 10/6/2025

- Kuwait (Composite only) - 10/6/2025

- Egypt (Composite only) - 10/6/2025

- UAE (Composite only) - 10/3/2025

- Uganda (Composite only) – 10/3/2025

- South Africa (Composite only) – 10/3/2025

- Lebanon (Composite only) – 10/3/2025

- Ghana (Composite only) – 10/3/2025

- Zambia (Composite only) – 10/6/2025

- Saudi Arabia (Composite only) – 10/3/2025

- Mozambique (Composite only) – 10/3/2025

- Kenya (Composite only) – 10/3/2025

Europe

- Ireland – 10/3/2025

- Spain – 10/3/2025

- Italy – 10/3/2025

- France – 10/3/2025

- Germany – 10/3/2025

- Eurozone – 10/3/2025

- UK – 10/3/2025

North & South America

Key Results

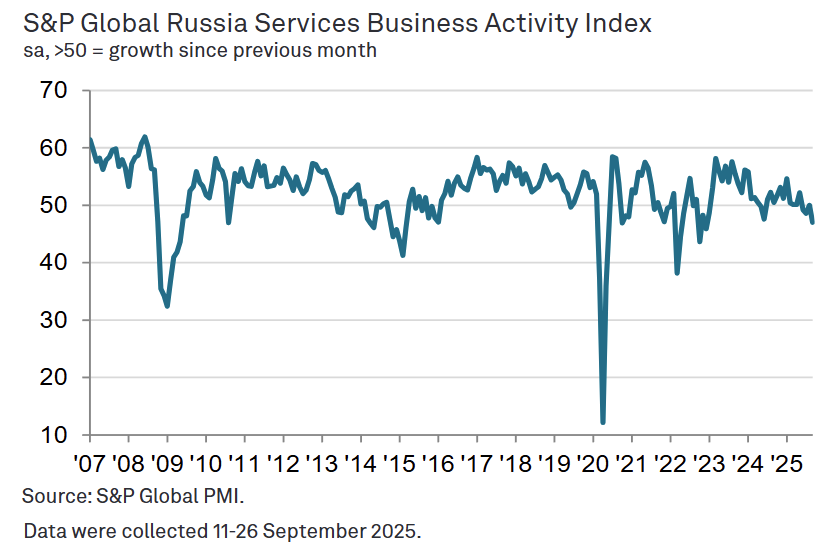

Russia

The S&P Global Russia Services PMI fell to 47.0 in September (from 50.0 in August), marking the sharpest services contraction since December 2022 amid a steep decline in new orders.

-

Business activity decreased for the third time in four months, with subdued client demand and weaker purchasing power weighing on output.

-

New orders contracted at the fastest pace since December 2022, highlighting sustained weakness in sales volumes.

-

Despite falling demand, service firms raised employment at the quickest pace since January 2024, with some citing efforts to clear backlogs.

-

Backlogs of work fell for the first time in 11 months, with the rate of depletion the steepest since December 2022.

-

Input costs rose at the fastest rate in five months on higher supplier, wage, and utility expenses, though firms moderated selling price increases due to competitive pressures.

-

Business confidence improved from August but remained below the long-run trend, supported by hopes of greater economic stability and stronger customer numbers.

The Russia Composite PMI Output Index fell to 46.6 in September (from 49.1 in August), the steepest contraction in private sector activity since October 2022.

-

Sharper contractions in both manufacturing and services new orders drove the fastest fall in total private sector sales since May 2022.

-

Workforce numbers rose at the strongest pace since August 2024, as services hiring offset renewed declines in manufacturing jobs.

-

Backlogs of work shrank for the third month in a row, reflecting broad-based weakness in demand across sectors.

-

Input costs and output charges both increased at faster rates, pointing to rising cost pressures despite soft demand conditions.

-

Overall business confidence improved from August but remained below the historical average, signaling only cautious optimism.

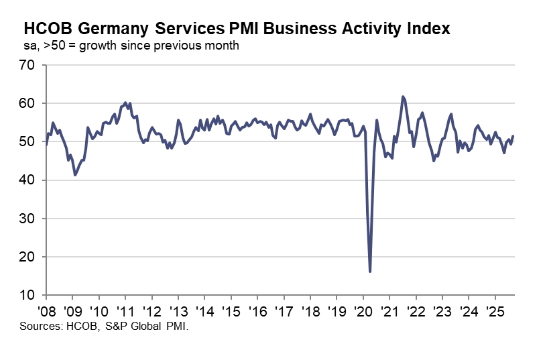

Germany

The HCOB Germany Services PMI rose to 51.5 in September (from 49.3 in August), its highest in eight months, signaling a modest rebound in activity despite fragile demand conditions.

-

Business activity expanded for the first time since July, supported by the completion of outstanding projects, though it remained below the long-run average of 52.7.

-

New business fell for the second month in a row, with firms citing customer budget cuts and weaker export sales; however, the pace of decline eased compared to August.

-

Backlogs of work continued to shrink, extending a depletion trend since May 2024.

-

Employment fell at the sharpest rate since June 2020, reflecting weak demand and limited pipeline work.

-

Input costs rose steeply, driven mainly by wage pressures, while output price inflation edged up to a four-month high and remained above the long-run trend.

-

Business confidence strengthened slightly to its highest level since May 2024, as firms expressed optimism about improving economic conditions.

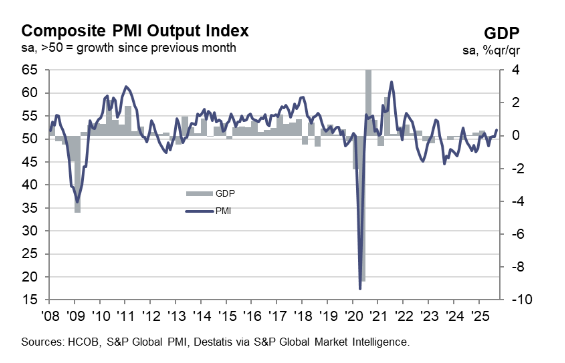

The Germany Composite PMI Output Index rose to 52.0 in September (from 50.5), the strongest expansion in 16 months, driven by gains in both manufacturing and services.

-

New work declined across both sectors, with manufacturing orders falling for the first time in four months and services orders contracting at a softer pace.

-

Employment fell in both sectors, producing the steepest overall workforce decline since November 2024, as capacity pressures eased further.

-

Backlogs of work dropped broadly, reinforcing signs of weak demand despite higher output levels.

-

Output price inflation accelerated to a four-month high, even as input cost growth slowed slightly, pointing to persistent cost pressures.

Eurozone

The HCOB Eurozone Composite PMI rose to 51.2 in September (from 51.0 in August), a 16-month high, signaling continued though muted private sector growth across the bloc.

-

The Eurozone Services PMI increased to 51.3 (from 50.5), its highest in eight months, marking a modest rebound in activity.

-

New business rose for the first time since May 2024, though the improvement was mild and driven by domestic demand, while new export orders continued to decline.

-

Backlogs of work fell for the 17th consecutive month, with the pace of depletion the quickest in three months, reflecting limited demand pressures.

-

Employment edged lower in September, marking the first overall workforce reduction since February, though the scale of job losses was marginal.

-

Input cost inflation eased to below the historical average, while output charges rose at the weakest pace since May, signaling softer price pressures.

-

Business confidence strengthened to an 11-month high in services and the second-highest overall since July 2024, supported by expectations of improved economic conditions.

-

Country detail: Spain led with a Composite PMI of 53.8, followed by Germany (52.0), Ireland (52.0), and Italy (51.7), while France remained an outlier at 48.1, signaling faster contraction.

USA

The S&P Global US Services PMI slipped to 54.2 in September (from 54.5 in August), marking the second straight monthly decline though still indicating solid expansion, with Q3 growth the strongest so far in 2025.

-

Business activity continued to expand for the 32nd consecutive month, though the pace slowed from July’s year-to-date peak.

-

New business growth softened to a three-month low, with tariffs and uncertainty weighing on demand; however, new export sales rose for the first time since March.

-

Backlogs of work increased solidly for the seventh consecutive month, underscoring ongoing capacity pressures.

-

Employment edged up only marginally, reflecting firms’ reluctance to add staff despite continued expansion; payroll growth has nonetheless now extended to seven months.

-

Input costs rose sharply, driven by tariffs, higher supplier charges, and wages, marking a slight acceleration in cost pressures.

-

Selling prices increased at the slowest rate in five months, as weaker demand and competition limited pricing power despite elevated costs.

-

Business confidence strengthened to its highest since May, supported by lower interest rates and expectations of supportive government policies.

The S&P Global US Composite PMI fell to 53.9 in September (from 54.6 in August), marking the slowest pace of growth in three months as both manufacturing and services saw softer expansions.

-

Output growth moderated across both sectors, reflecting slower gains in new business.

-

Employment rose only marginally, showing limited hiring momentum despite continued expansion.

-

Business confidence strengthened noticeably, indicating greater optimism for future activity.

-

Input cost inflation remained elevated but eased to a five-month low, suggesting some relief in price pressures.

-

Output charges followed a similar trend, with selling price inflation also softening to its weakest level in five months.

-

Global - 9/4/2025

Asia Pacific

- Australia - 9/2/2025

- Singapore (Composite only) – 9/3/2025

- Hong Kong (Composite only) – 9/3/2025

- Japan – 9/3/2025

- China – 9/3/2025

- India – 9/3/2025

- Russia – 9/3/2025

- Kazakhstan – 9/3/2025

Africa & Middle East

- Nigeria (Composite only) - 9/1/2025

- Qatar (Composite only) - 9/3/2025

- Kuwait (Composite only) - 9/3/2025

- Egypt (Composite only) - 9/3/2025

- UAE (Composite only) - 9/3/2025

- Uganda (Composite only) – 9/3/2025

- South Africa (Composite only) – 9/3/2025

- Lebanon (Composite only) – 9/3/2025

- Ghana (Composite only) – 9/3/2025

- Zambia (Composite only) – 8/6/2025

- Saudi Arabia (Composite only) – 9/3/2025

- Mozambique (Composite only) – 9/3/2025

- Kenya (Composite only) – 9/3/2025

Europe

- Ireland – 9/3/2025

- Spain – 9/3/2025

- Italy – 9/3/2025

- France – 9/3/2025

- Germany – 9/3/2025

- Eurozone – 9/3/2025

- UK – 9/3/2025

North & South America

Key Results

Australia

The S&P Global Australia Services PMI rose to 55.8 in August (from 54.1 in July), marking the strongest services expansion since April 2022 and extending the growth streak to 19 months.

-

New business rose sharply, with export orders increasing for the first time since February and at the fastest pace since June 2022, while domestic demand remained robust.

-

Employment growth accelerated to its highest in four months, as firms hired to manage workloads and ease capacity pressures, though backlogs continued to decline only fractionally.

-

Input costs, including supplies, fuel, and labour, increased again but at a slower pace than July; output prices also rose at a weaker rate, signaling softer inflationary pressures.

-

Business confidence improved, supported by expectations of continued sales growth and firmer global demand conditions.

-

The Composite Output Index, which includes both manufacturing and services, climbed to 55.5 (from 53.8), the fastest pace of private-sector growth since April 2022.

China

China’s General Services PMI rose to 53.0 in August (from 52.6 in July), the fastest expansion since May 2024, with stronger domestic and export demand offset by weaker employment trends.

-

New business expanded at the quickest pace since May 2024, with new export orders rising at the fastest rate since February, driven by better market conditions, tourism, and business development.

-

Backlogs of work increased for the fifth consecutive month, with growth accelerating compared to July, highlighting sustained pressure on capacity.

-

Employment declined at the sharpest pace in five months, as firms reported redundancies and non-replacement of leavers amid cost concerns.

-

Input costs continued to rise for the sixth straight month on higher wages and raw materials, though the pace of increase softened; output charges fell back into contraction, signaling persistent margin pressures.

-

The Composite Output Index climbed to 51.9 (from 50.8), the strongest expansion since November 2024, supported by services-led growth and improved business confidence, though manufacturing remained weaker.

India

India’s Services PMI rose to 62.9 in August (from 60.5 in July), marking the steepest expansion since June 2010, supported by surging demand and strong international sales.

-

New orders expanded for the 49th straight month, reaching their highest rate in over 15 years; export orders also rose sharply, recording the third-strongest increase since the series began in 2014.

-

Employment increased moderately, aided by part-time hiring, while strong recent job creation ensured firms had sufficient capacity, keeping backlogs nearly stable.

-

Input costs rose at the fastest pace since November 2024, driven mainly by higher wages and overtime payments, while some firms also cited transport and material costs.

-

Output charges increased at the steepest rate since July 2012, reflecting firms’ ability to pass higher expenses onto clients amid robust demand.

-

The Composite PMI climbed to 63.2 (from 61.1), a 17-year high, indicating broad-based acceleration across both services and manufacturing.

Eurozone

The HCOB Eurozone Composite PMI edged up to 51.0 in August from 50.9 in July, a 12-month high, signalling a slight acceleration in growth.

-

Services PMI eased to 50.5 (down from 51.0) while manufacturing recorded its strongest production rise in almost 3½ years, showing growth constrained mainly by services.

-

Total new orders rose for the first time since May 2024, but new export orders fell at the quickest pace since March, indicating demand was domestically led.

-

Employment increased for a sixth month at the fastest pace in 14 months, though factory headcounts continued to shrink; backlogs were reduced only slightly, the softest depletion in nearly 2½ years.

-

Input cost inflation accelerated to the fastest since March and firms raised output charges at the greatest rate in four months; in services, input costs hit a 3-month high and charges rose at the fastest pace since March.

-

Country detail: Spain 53.7 (2-month low), Italy 51.7 (3-month high), Ireland 51.3 (14-month low), Germany 50.5 (2-month low), and France 49.8 (12-month high but still <50).

UK

UK Services PMI rose to 54.2 in August (from 51.8 in July), a 16-month high, while the Composite Output Index increased to 53.5 (from 51.5), marking a one-year high and signalling firmer momentum.

-

New orders returned to growth, rising at the strongest pace since Sep 2024; export orders increased for the first time since March, indicating demand improved both domestically and abroad.

-

Backlogs were depleted for the 27th straight month and at a solid pace, suggesting firms retained sufficient capacity despite stronger workloads.

-

Employment fell for the 11th consecutive month amid hiring freezes, non-replacement of leavers, and redundancies, reflecting margin pressure from rising payroll costs.

-

Input cost inflation re-accelerated to a 3-month high on higher wages (incl. NI contributions), food, and technology costs; output charge inflation hit its highest since April, showing persistent pricing pressures.

-

Business optimism rose to a 10-month high (49% expect higher activity vs 14% expecting a decline), supported by lower borrowing costs and improved sales pipelines, though policy uncertainty remains a headwind.

-

Global - 8/5/2025

Asia Pacific

- Australia - 8/4/2025

- Singapore (Composite only) – 8/5/2025

- Hong Kong (Composite only) – 8/5/2025

- Japan – 8/5/2025

- China – 8/5/2025

- India – 8/5/2025

- Russia – 8/5/2025

- Kazakhstan – 8/5/2025

Africa & Middle East

- Nigeria (Composite only) - 8/1/2025

- Qatar (Composite only) - 8/5/2025

- Kuwait (Composite only) - 8/5/2025

- Egypt (Composite only) - 8/5/2025

- UAE (Composite only) - 8/5/2025

- Uganda (Composite only) – 8/5/2025

- South Africa (Composite only) – 8/5/2025

- Lebanon (Composite only) – 8/5/2025

- Ghana (Composite only) – 8/5/2025

- Zambia (Composite only) – 8/6/2025

- Saudi Arabia (Composite only) – 8/5/2025

- Mozambique (Composite only) – 8/5/2025

- Kenya (Composite only) – 8/5/2025

Europe

- Ireland – 8/5/2025

- Spain – 8/5/2025

- Italy – 8/5/2025

- France – 8/5/2025

- Germany – 8/5/2025

- Eurozone – 8/5/2025

- UK – 8/5/2025

North & South America

Key Results

Australia

The S&P Global Australia Services PMI rose to 54.1 in July from 51.8 in June, marking the fastest pace of expansion in services activity since March 2024 and extending the current growth streak to 18 months.

- New business rose at the sharpest pace since April 2022, driven by stronger domestic demand and a stabilizing export sector.

- Employment growth accelerated, with firms hiring to support workloads and reduce backlogs.

- Input cost inflation reached a 10-month high, while output charges rose at the fastest rate in 23 months.

- Business confidence remained positive but fell to a 9-month low amid concerns over future growth.

- The Composite Output Index rose to 53.8 (from 51.6 in June), reflecting broader gains in both services and manufacturing.

China

The S&P Global China General Services PMI rose to 52.6 in July from 50.6 in June, marking the fastest pace of services activity growth since May 2024 and extending the current expansion streak to over 2.5 years.

- New business rose at the quickest rate in a year, supported by improving domestic demand and the first rise in export orders in three months.

- Employment rebounded, with staffing levels increasing at the fastest pace since July 2024 after a decline in June.

- Output charges rose for the first time since January, while input cost inflation also picked up, though both remained below historical averages.

- Business confidence improved to a four-month high but stayed below the series average.

- The Composite Output Index edged down to 50.8 (from 51.3 in June), with services growth offsetting a decline in manufacturing output.

Russia

The S&P Global Russia Services PMI fell to 48.6 in July from 49.2 in June, signaling a sharper decline in services activity and the steepest contraction since June 2024.

- New business fell for the first time in 12 months, with the fastest drop since January 2023, driven by weak client demand and lower customer numbers.

- Employment rose at the fastest pace since February, supported by improved business confidence and expectations of future growth.

- Input and output price inflation accelerated from June but remained below long-run averages, with limited pricing power due to soft demand.

- Backlogs of work rose only fractionally, reflecting reduced capacity pressures.

- The Composite Output Index fell to 47.8 (from 48.5 in June), marking the sharpest contraction in private sector activity since October 2022.

Eurozone

The HCOB Eurozone Services PMI rose to 51.0 in July from 50.5 in June, marking a 4-month high and the strongest pace of services activity growth since March 2025.

- The Composite PMI Output Index rose to 50.9 in July (from 50.6 in June), driven by services as manufacturing growth slowed.

- New business remained flat MoM, with export orders falling for the 26th consecutive month.

- Employment rose for a fifth straight month, at the fastest rate in over a year, despite weak demand.

- Input cost inflation eased to its softest pace since October 2024, while output prices saw a mild acceleration to a 3-month high.

- Among major economies, Spain led with a Composite PMI of 54.7, followed by Italy (51.5); France contracted further to 48.6.

US

The S&P Global US Services PMI rose to 55.7 in July from 52.9 in June, the highest reading year-to-date, signaling the strongest pace of expansion in the service sector since January.

- New orders grew at the fastest rate since January, extending the current growth streak to 15 months.

- Input and output price inflation accelerated, with firms citing tariff-related cost pressures and wage increases.

- Backlogs of work rose for the fifth straight month, at the fastest pace since May 2022.

- Employment rose modestly for the fifth consecutive month, with most hiring reported as part-time or temporary.

- Business confidence remained positive but eased to a three-month low amid rising costs and subdued export demand.

- The Composite PMI rose to 55.1 from 52.9 in June, driven by stronger services growth and a modest rise in manufacturing output.

- Composite new orders grew at a faster pace, while employment and selling price inflation both picked up.

- Inflationary pressures intensified, with selling prices rising at the fastest pace since August 2022.

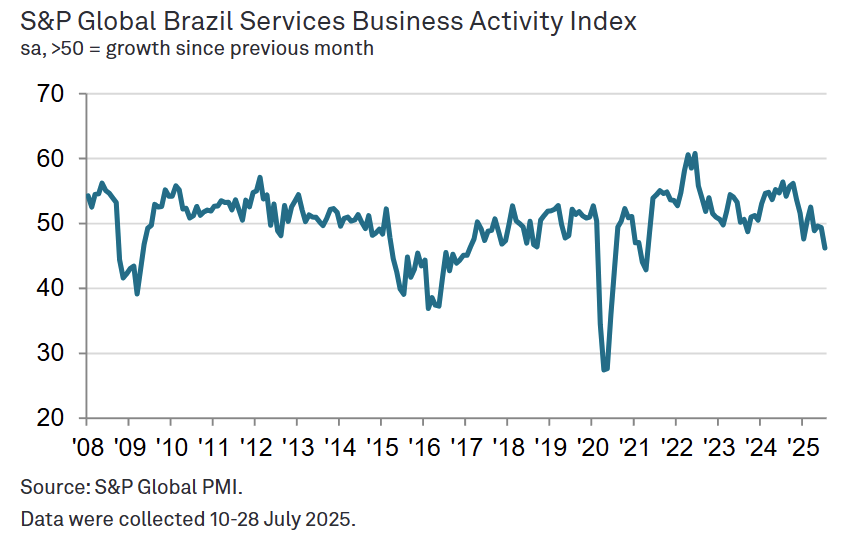

Brazil

The S&P Global Brazil Services PMI fell to 46.3 in July from 49.3 in June, marking the sharpest decline in services activity since April 2021 and the fourth consecutive month of contraction.

- New business dropped for the fourth straight month and at the fastest pace in 51 months.

- Employment declined for the first time since October 2024, ending an 8-month growth streak.

- Business confidence fell to its lowest level since mid-2020 amid political and financial uncertainty.

- Input cost inflation eased to an 8-month low, but output charges rose at the fastest pace since February.

- The Composite PMI fell to 46.6 (from 48.7), as both manufacturing and services saw accelerated declines in activity.

-

Global - 7/3/2025

Asia Pacific

- Australia - 7/2/2025

- Singapore (Composite only) – 7/3/2025

- Hong Kong (Composite only) – 7/3/2025

- Japan – 7/3/2025

- China – 7/3/2025

- India – 7/3/2025

- Russia – 7/3/2025

- Kazakhstan – 7/3/2025

Africa & Middle East

- Nigeria (Composite only) - 7/1/2025

- Qatar (Composite only) - 7/3/2025

- Kuwait (Composite only) - 7/3/2025

- Egypt (Composite only) - 7/3/2025

- UAE (Composite only) - 7/3/2025

- Uganda (Composite only) – 7/3/2025

- South Africa (Composite only) – 7/3/2025

- Lebanon (Composite only) – 7/3/2025

- Ghana (Composite only) – 7/3/2025

- Zambia (Composite only) – 7/3/2025

- Saudi Arabia (Composite only) – 7/3/2025

- Mozambique (Composite only) – 7/3/2025

- Kenya (Composite only) – 7/3/2025

Europe

- Ireland – 7/3/2025

- Spain – 7/3/2025

- Italy – 7/3/2025

- France – 7/3/2025

- Germany – 7/3/2025

- Eurozone – 7/3/2025

- UK – 7/3/2025

North & South America

Key Results

Australia

Australia’s S&P Services PMI increased 1.2 pts to 51.8 in June, the highest since May 2024.

- New orders increased, driven by domestic sources of demand, while foreign demand contracted at the sharpest pace in 3.5 years.

- Services firms saw optimism rise to the highest level since May 2022.

China

The Caixin China General Services PMI fell -0.5 pts to 50.6 in June, the lowest in 9 months, indicating a softening in services activity.

- New business growth slowed, with new export orders falling at the fastest pace since December 2022.

- Employment declined for the third time in four months, contributing to the largest backlog buildup in a year.

- Input costs rose marginally, but output prices were cut at the sharpest pace since April 2022 due to competitive pressures.

- Business sentiment improved for a second month but remained well below the historical average.

- Composite PMI rose to 51.3 (from 49.6), as manufacturing rebounded and offset weaker services growth; selling prices fell at the fastest pace in over two years.

India

The S&P India Services PMI rose 1.6 pts to 60.4 in June, the highest in 10 months, signaling strong growth in activity driven by robust domestic and export demand.

- New orders expanded at the fastest pace since August 2024, with export orders remaining strong despite slowing modestly.

- Employment rose for the 37th straight month, though job creation softened from May’s record.

- Input cost inflation eased to a 10-month low, while output charge inflation also moderated but remained above the long-run average.

- Backlogs rose slightly, reflecting mild capacity pressures.

- Business optimism stayed positive but fell to its lowest level since mid-2022, below the long-run trend.

- The Composite PMI climbed to 61.0 (from 59.3), the strongest in 14 months, as manufacturing and services both contributed to broad-based private sector expansion.

Eurozone

The S&P Eurozone Composite PMI rose to 50.6 in June from 50.2 in May, a 3-month high, signaling modest expansion in private sector output as both manufacturing and services activity increased.

- The Services PMI rose to 50.5 (from 49.7), also a 3-month high, with growth driven by employment gains and improved sentiment.

- New business fell for the 13th consecutive month, but the rate of contraction was the weakest in over a year.

- Input price inflation held at a 6-month low; services saw sustained cost pressures, while manufacturing input costs declined.

- Output charges rose at the fastest pace in 3 months, with services firms increasing prices more than manufacturers.

- Business confidence improved to its highest level since July 2024, though it remained below the long-run average.

UK

The S&P Global UK Services PMI rose to 52.8 in June, up from 50.9in May, the highest in 10 months, reflecting the fastest pace of growth since August 2024 amid a rebound in domestic demand.

- New orders increased for the first time in three months, led by domestic sales; export sales fell for the third straight month.

- Employment declined for a ninth consecutive month, with job shedding slightly faster than in May due to cost concerns and weak capacity pressures.

- Input cost inflation eased to a 6-month low, while output charge inflation slowed to the weakest pace since February 2021.

- Business confidence remained positive but softened from May amid concerns over UK economic prospects and geopolitical risks.

- The Composite PMI rose to 52.0 (from 50.3), marking the fastest private sector growth since September 2024.

US

The S&P Global US Services PMI fell -0.8 pts to 52.9 in June, indicating slower but still solid growth in services activity as tariffs and policy uncertainty weighed on momentum.

- New business rose at a softer pace, while export sales declined for the third straight month, marking the steepest quarterly drop since late 2022.

- Input and output prices remained elevated, though inflation eased slightly from May’s near 2-year highs.

- Employment growth accelerated to a 5-month high, driven by rising workloads and improved hiring success.

- Business confidence stayed positive but softened further, remaining below the long-run average amid trade and policy concerns.

- The Composite PMI held nearly flat at 52.9 (vs 53.0 in May), with manufacturing rebounding and supporting overall private sector output.

-

Global - 6/5/2025

Asia Pacific

- Australia - 6/3/2025

- Singapore (Composite only) – 6/4/2025

- Hong Kong (Composite only) – 6/4/2025

- Japan – 6/4/2025

- China – 6/5/2025

- India – 6/4/2025

- Russia – 6/4/2025

- Kazakhstan – 6/6/2025

Africa & Middle East

- Nigeria (Composite only) - 6/2/2025

- Qatar (Composite only) - 6/3/2025

- Kuwait (Composite only) - 6/3/2025

- Egypt (Composite only) - 6/3/2025

- UAE (Composite only) - 6/4/2025

- Uganda (Composite only) – 6/5/2025

- South Africa (Composite only) – 6/4/2025

- Lebanon (Composite only) – 6/4/2025

- Ghana (Composite only) – 6/4/2025

- Zambia (Composite only) – 6/4/2025

- Saudi Arabia (Composite only) – 6/3/2025

- Mozambique (Composite only) – 6/4/2025

- Kenya (Composite only) – 6/5/2025

Europe

- Ireland – 6/5/2025

- Spain – 6/4/2025

- Italy – 6/4/2025

- France – 6/4/2025

- Germany – 6/4/2025

- Eurozone – 6/4/2025

- UK – 6/4/2025

North & South America

-

Global - 5/5/2025

Asia Pacific

- Australia - 5/4/2025

- Singapore (Composite only) – 5/6/2025

- Hong Kong (Composite only) – 5/6/2025

- Japan – 5/6/2025

- China – 5/6/2025

- India – 5/6/2025

- Russia – 5/7/2025

- Kazakhstan – 5/6/2025

Africa & Middle East

- Nigeria (Composite only) - 5/2/2025

- Qatar (Composite only) - 5/5/2025

- Kuwait (Composite only) - 5/5/2025

- Egypt (Composite only) - 5/6/2025

- UAE (Composite only) - 5/5/2025

- Uganda (Composite only) – 5/6/2025

- South Africa (Composite only) – 5/6/2025

- Lebanon (Composite only) – 5/6/2025

- Ghana (Composite only) – 5/6/2025

- Zambia (Composite only) – 5/6/2025

- Saudi Arabia (Composite only) – 5/5/2025

- Mozambique (Composite only) – 5/6/2025

- Kenya (Composite only) – 5/6/2025

Europe

- Ireland – 5/6/2025

- Spain – 5/6/2025

- Italy – 5/6/2025

- France – 5/6/2025

- Germany – 5/6/2025

- Eurozone – 5/6/2025

- UK – 5/6/2025

North & South America

Key Results

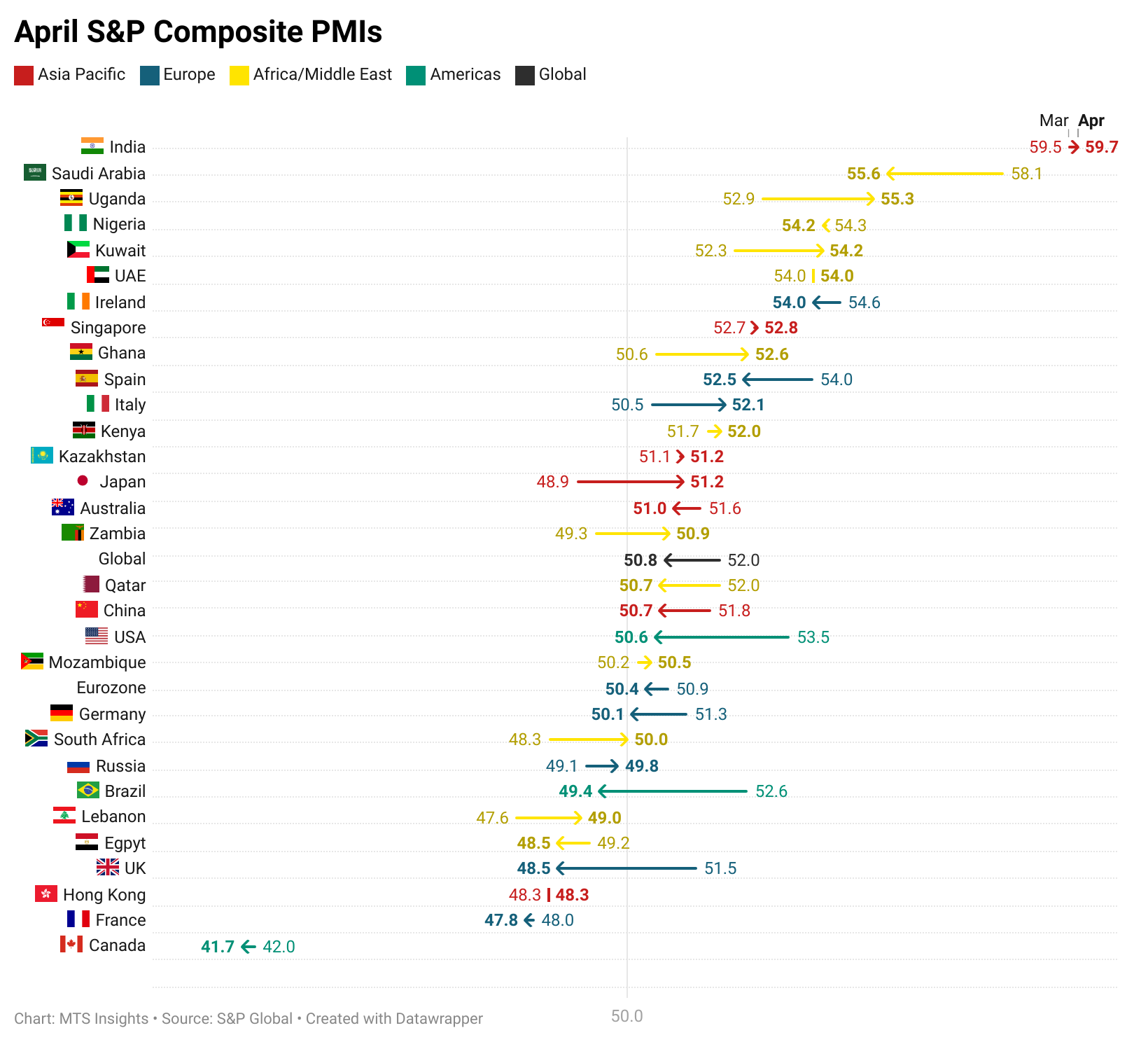

Saudi Arabia

Saudi Arabia’s non-oil private sector expansion drops to the weakest since August 2024, down -2.5 pts to 55.6 in April. Despite the drop, growth was still occurring at a strong pace.

China

China’s service sector activity fell to the slowest expansion in 7-months as the PMI fell -1.2 pts to 50.7 in April. Notably, business confidence fell to the 2nd-lowest on record, and new order growth was the lowest in 28 months.

Eurozone

The service sector in the euro area moved back to stagnation as the PMI dropped -0.9 pts to 50.1 in April. New orders contracted for the third straight month, and the level of positive sentiment dropped to the lowest in almost 2.5 years.

UK

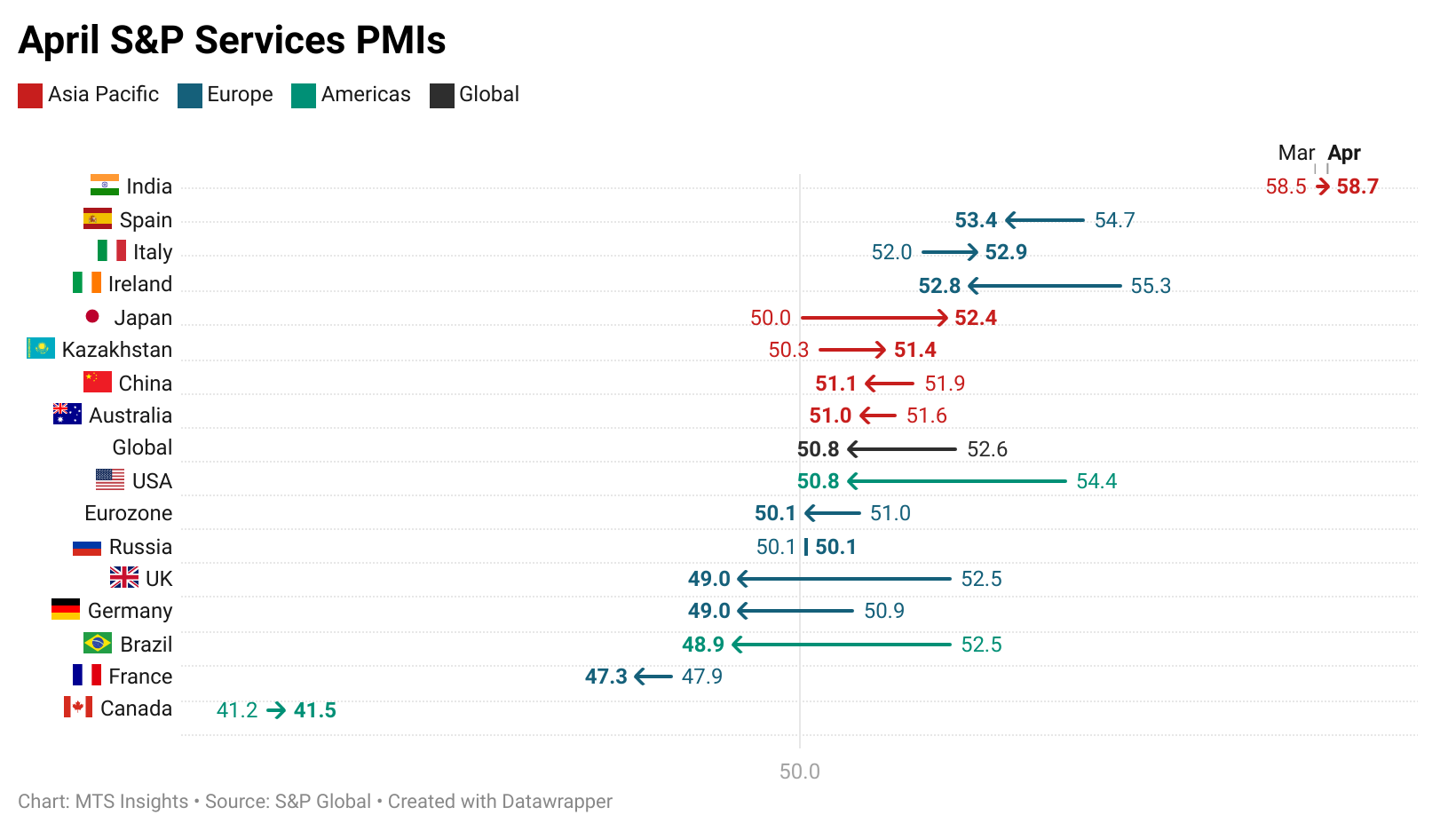

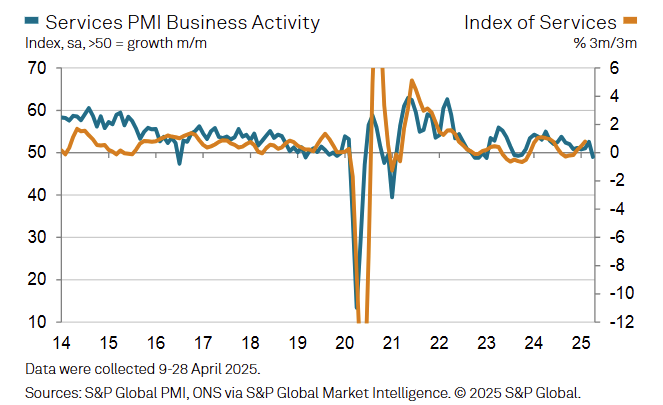

The UK S&P Services PMI fell -3.5 pts to 49.0 in April, the lowest since January 2023.

- New orders contracted for the third time in four months as US tariffs impacted activity.

- New export orders declined at the sharpest rate since February 2021.

- Input cost inflation was the highest since July 2023 as 43% of businesses reported an increase.

- Total private sector growth turned negative for the first time in 1.5 years as the Composite PMI fell -3.0 pts to 48.5.