S&P Global Manufacturing PMIs

S&P Global Manufacturing PMIs

- Source

- S&P Global

- Source Link

- https://www.pmi.spglobal.com/

- Frequency

- Monthly

- Next Release(s)

- May 1st, 2026 12:00 AM

-

June 1st, 2026 12:00 AM

-

July 1st, 2026 12:00 AM

-

August 3rd, 2026 12:00 AM

-

September 1st, 2026 12:00 AM

-

October 1st, 2026 12:00 AM

-

November 2nd, 2026 12:00 AM

-

December 1st, 2026 12:00 AM

-

January 4th, 2027 12:00 AM

-

February 1st, 2027 12:00 AM

-

March 1st, 2027 12:00 AM

-

April 1st, 2027 12:00 AM

Latest Updates

-

Asia Pacific Europe North & South America Australia - 3/31/2026 Austria - 3/27/2026 Brazil - 4/1/2026 Malaysia - 4/1/2026 Ireland - 4/1/2026 Canada - 4/1/2026 ASEAN - 4/1/2026 Netherlands - 4/1/2026 US - 4/1/2026 Myanmar - 4/1/2026 Romania - 4/1/2026 Colombia - 4/1/2026 Philippines - 4/1/2026 Turkiye - 4/1/2026 Mexico - 4/1/2026 Thailand - 4/1/2026 Poland - 4/1/2026 Vietnam - 4/1/2026 Spain - 4/1/2026 Global - 4/1/2026 Indonesia - 4/1/2026 Czechia - 4/1/2026 Japan - 4/1/2026 Italy - 4/1/2026 Taiwan - 4/1/2026 France - 4/1/2026 China - 4/1/2026 Germany - 4/1/2026 India - 4/2/2026 Eurozone - 4/1/2026 Russia - 4/1/2025 Greece - 4/1/2026 Kazakhstan - 4/1/2026 UK - 4/1/2026 South Korea - 4/1/2026 Switzerland - 4/1/2026 (procure.ch) Pakistan - 4/1/2026 -

Global - 3/4/2026

Asia Pacific Europe North & South America Australia - 3/1/2026 Austria - 2/25/2025 Brazil - 3/2/2026 Malaysia - 3/2/2026 Ireland - 3/2/2026 Canada - 3/2/2026 ASEAN - 3/3/2026 Netherlands - 3/2/2026 US - 3/2/2026 Myanmar - 3/3/2026 Romania - 3/2/2026 Colombia - 3/2/2026 Philippines - 3/2/2026 Turkiye - 3/2/2026 Mexico - 3/2/2026 Thailand - 3/2/2026 Poland - 3/2/2026 Vietnam - 3/2/2026 Spain - 3/2/2026 Indonesia - 3/2/2026 Czechia - 3/2/2026 Japan - 3/2/2026 Italy - 3/2/2026 Taiwan - 3/2/2026 France - 3/2/2026 China - 3/4/2025 Germany - 3/2/2026 India - 3/2/2026 Eurozone - 3/2/2026 Russia - 3/2/2025 Greece - 3/2/2026 Kazakhstan - 3/2/2026 UK - 3/2/2026 South Korea - 3/3/2026 Switzerland - 3/2/2026 (procure.ch) Pakistan - 3/2/2026 Key Results

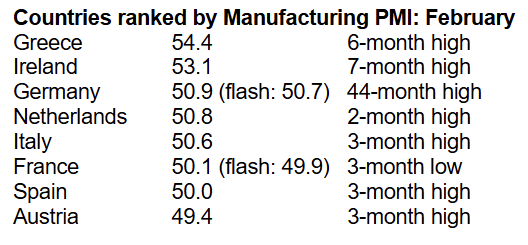

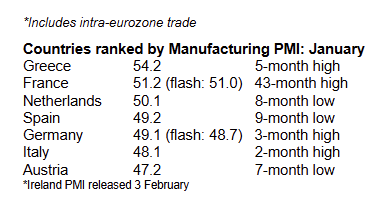

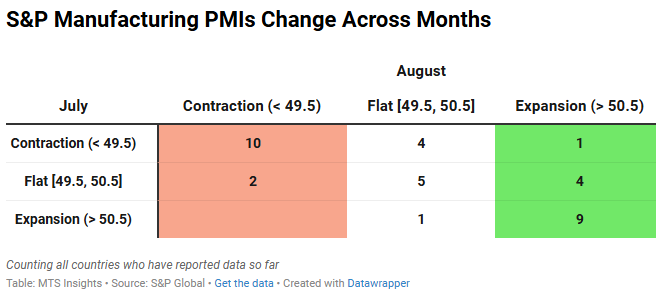

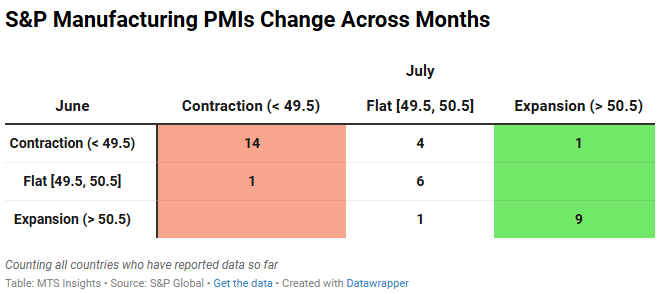

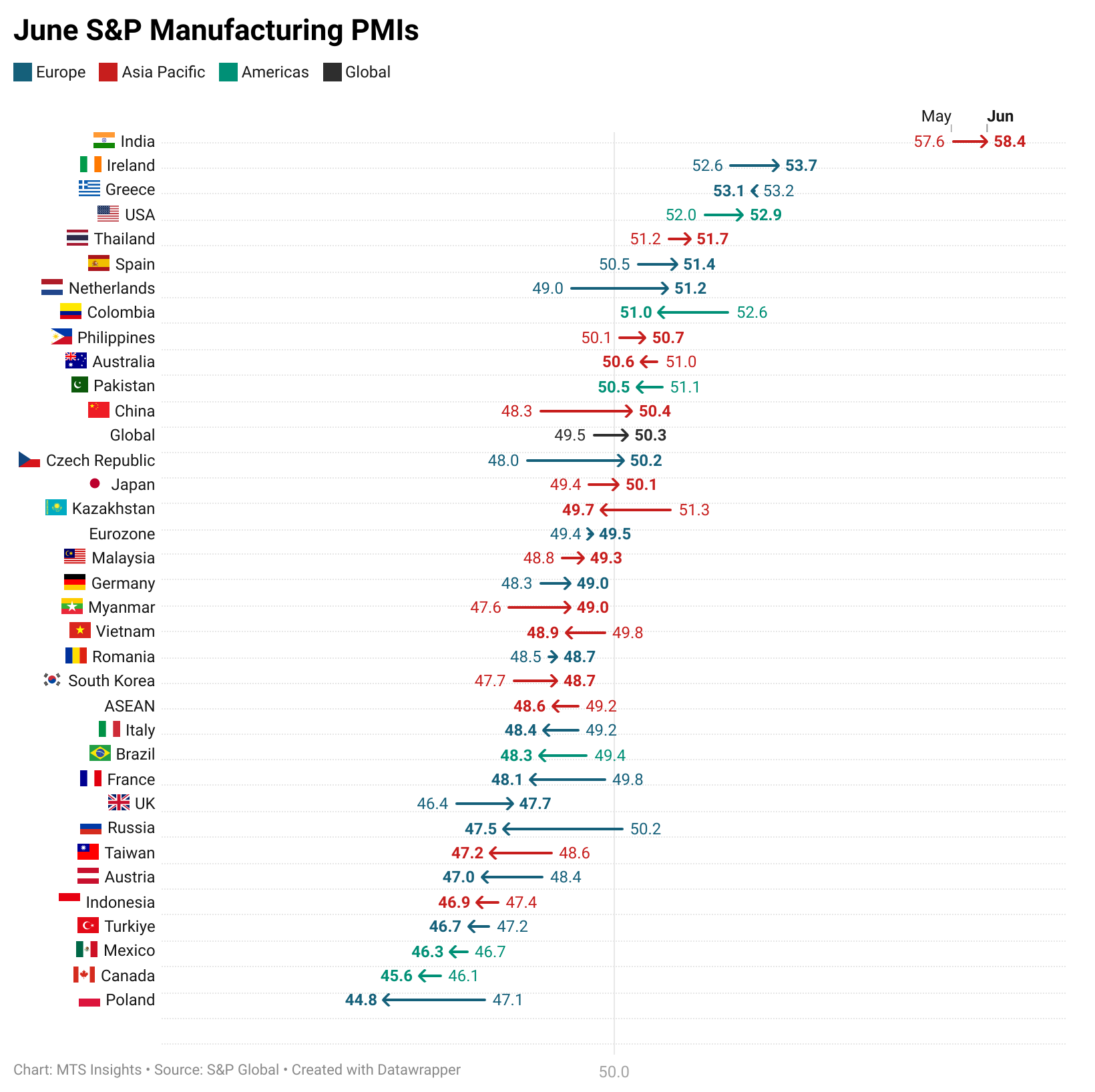

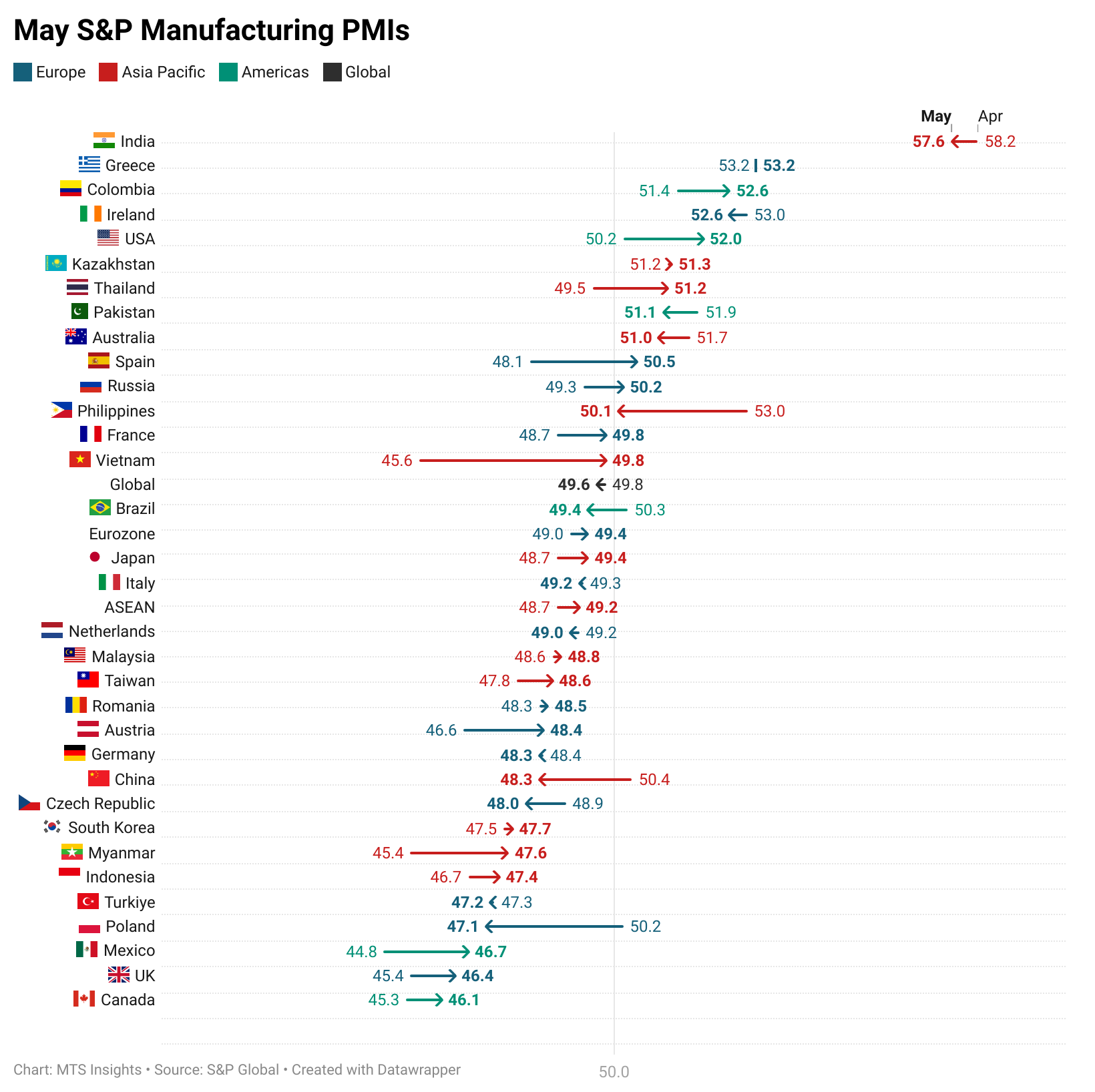

Highs & Lows

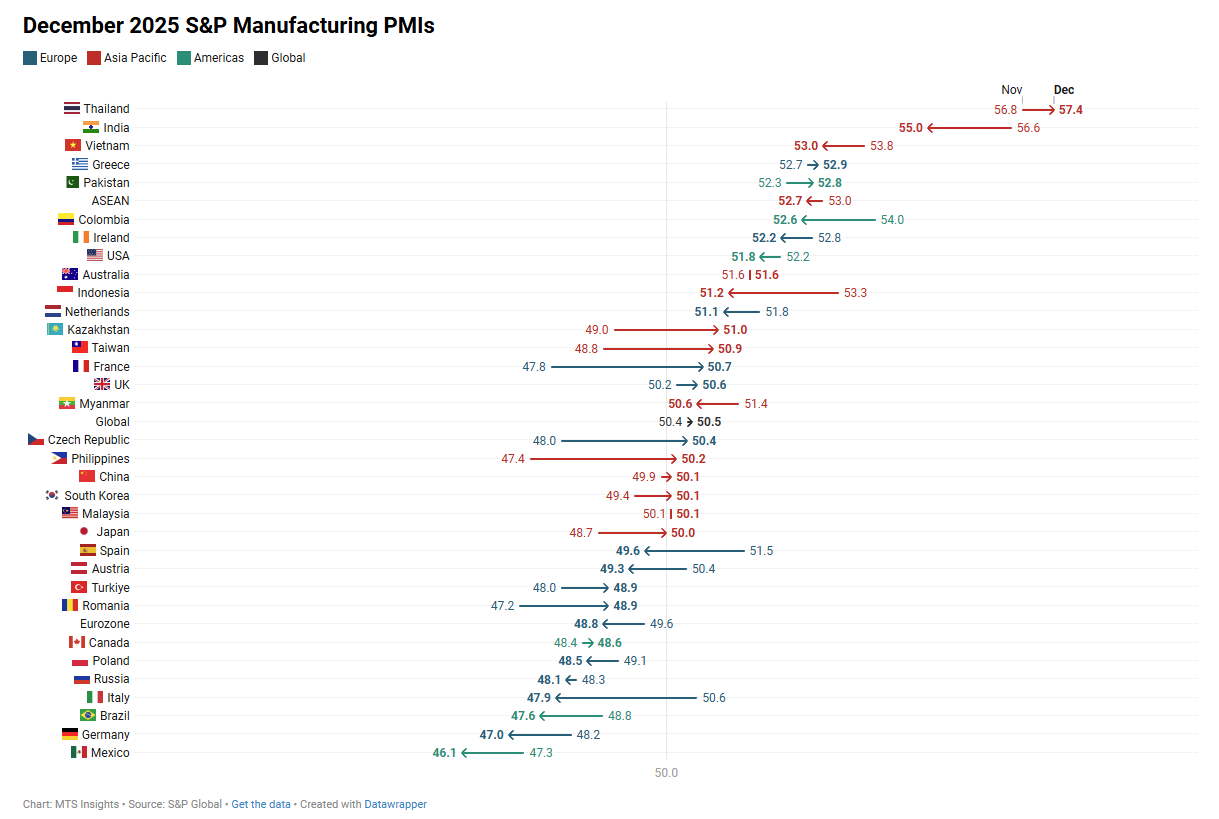

- Indonesia up 1.2 pts to 53.8, highest in nearly two years.

- Taiwan up 3.5 pts to 55.2, highest since December 2021.

- Japan up 1.5 pts to 53.0, highest since mid-2022.

- China up 1.8 pts to 52.1, highest since December 2020.

- The Philippines up 1.7 pts to 54.6, one of the strongest readings since November 2017.

- ASEAN region up 1.0 pts to 53.8, the highest on record.

- Turkey up 1.2 pts to 49.3, highest in 22 months.

- Germany up 1.8 pts to 50.9, highest in 44 months.

- Eurozone up 1.3 pts to 50.8, highest in 44 months.

- Canada up 0.6 pts to 51.0, highest in 13 months.

- Romania down -2.8 pts to 45.3, lowest on record.

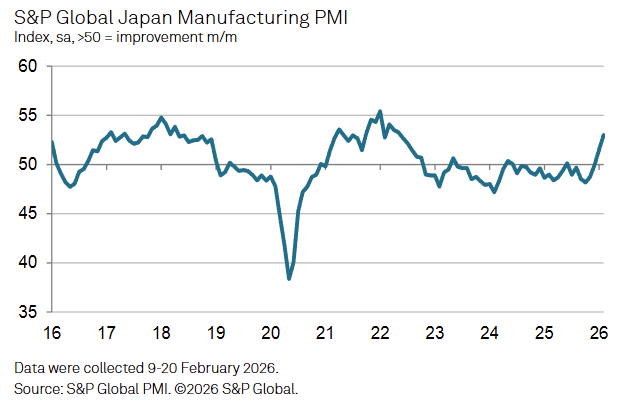

Japan

Japan’s Manufacturing PMI rose to 53.0 in February (Jan: 51.5), marking the strongest improvement in operating conditions since mid 2022.

-

Output expanded at the fastest rate in just over four years, with firms attributing the increase primarily to higher volumes of new business.

-

Total new orders grew at the quickest pace since January 2022, while export orders increased at the fastest rate since June 2021, reflecting stronger demand from Europe and other parts of Asia.

-

Employment increased for a 15th consecutive month and at the fastest pace in over four years as firms expanded headcounts to meet rising production needs.

-

Purchasing activity rose for a second straight month and at the quickest rate since May 2022, while inventories of inputs and finished goods declined slightly, indicating cautious stock management.

-

Backlogs of work continued to rise, though only marginally, signaling ongoing capacity pressure within the sector.

-

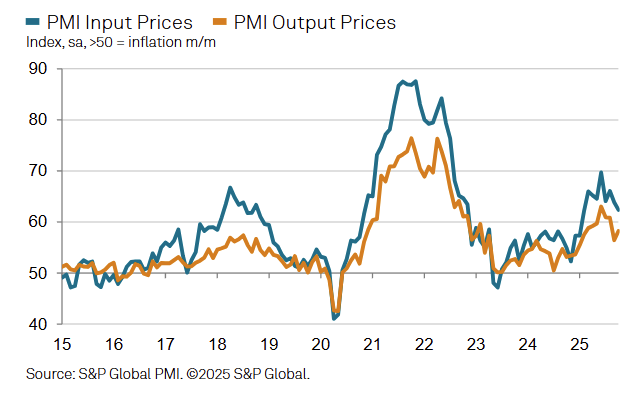

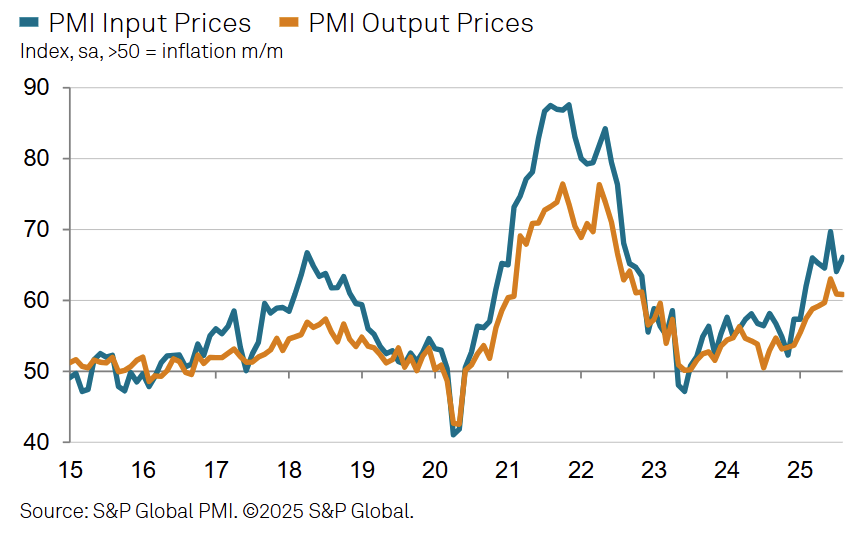

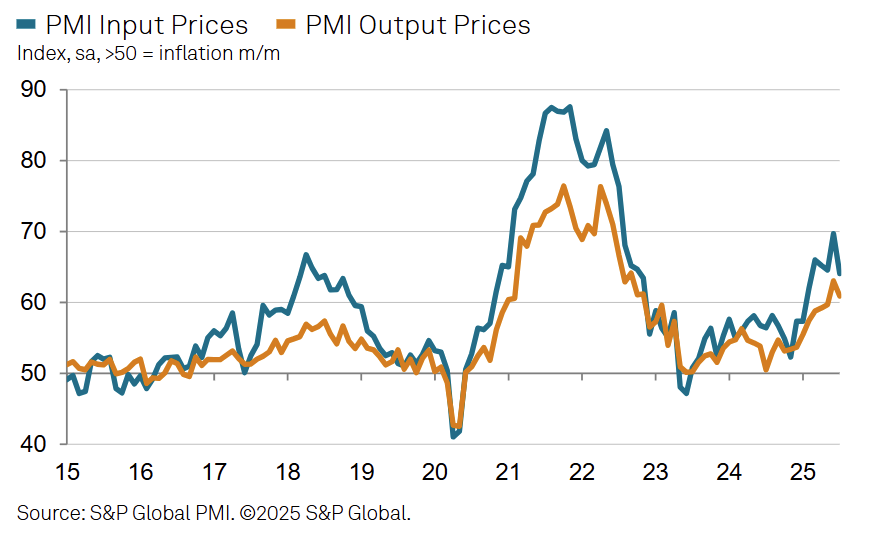

Input price inflation eased from January but remained historically elevated, and firms continued to raise selling prices despite a slower pace of charge inflation.

-

Business confidence improved to a 20 month high with expectations of stronger global demand and new product releases supporting output in the year ahead.

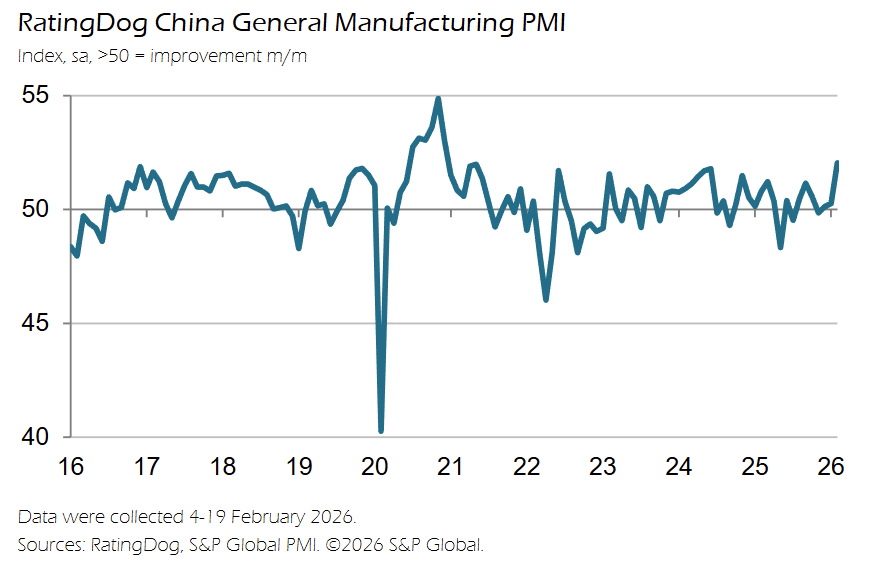

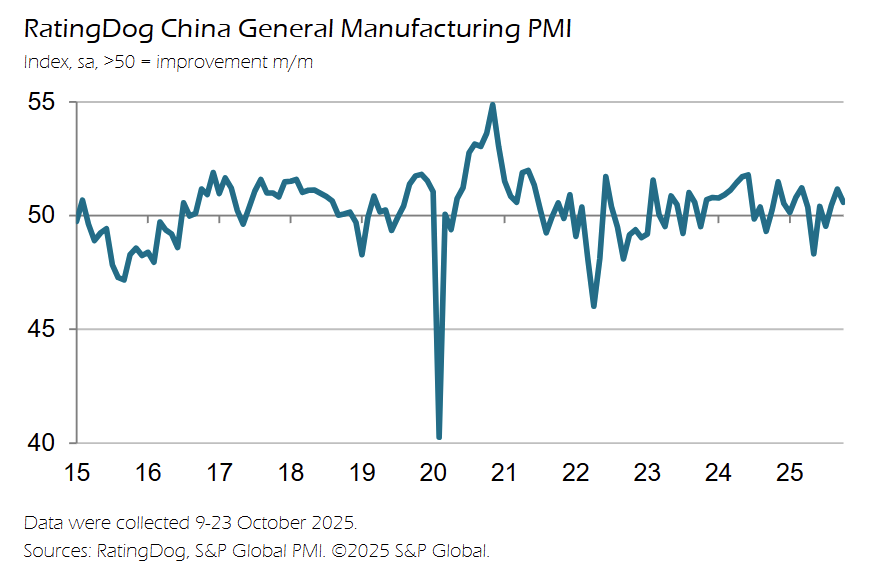

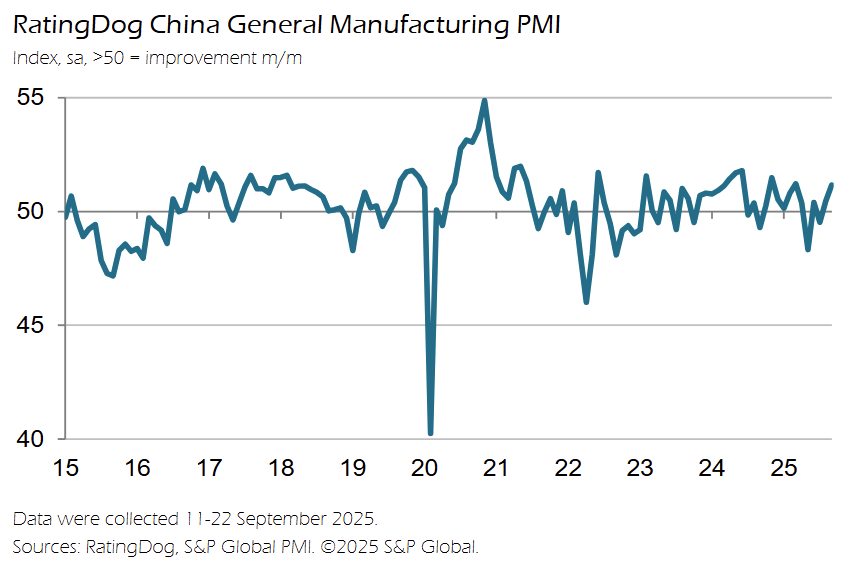

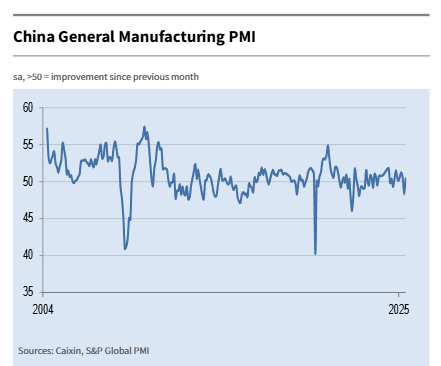

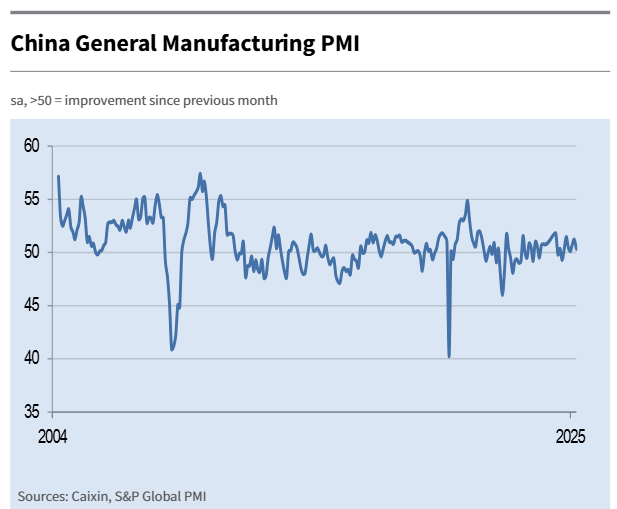

China

China’s S&P Global General Manufacturing PMI rose to 52.1 in February (Jan: 50.3), marking the strongest improvement in manufacturing operating conditions since December 2020 as demand, production, and purchasing activity accelerated.

-

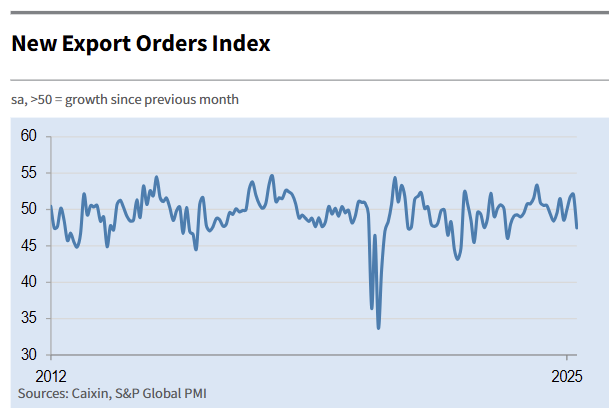

Total new orders increased for the ninth consecutive month and expanded at the fastest pace since December 2020, with particularly strong growth in export demand as new export orders rose at the quickest rate since September 2020.

-

Manufacturing output growth accelerated alongside stronger demand, with production expanding at the fastest rate since June 2024, while firms stepped up purchasing activity to meet the higher inflow of new work.

-

The volume of inputs purchased increased for a second straight month and at the fastest rate since November 2024, with buying activity running comfortably above the survey’s long-run average and broad-based across sectors.

-

Despite faster production growth, backlogs of work rose in February after manufacturers had previously cleared outstanding business in January, indicating that demand growth outpaced current production capacity.

-

Employment rose only fractionally for the second consecutive month, marking the first back-to-back increases in staffing since mid 2021, but highlighting continued caution among firms when expanding headcounts.

-

Input cost inflation accelerated to the highest level since June 2022, driven in part by stronger demand for raw materials and rising metal prices, although the rate of inflation remained below the long-run survey trend.

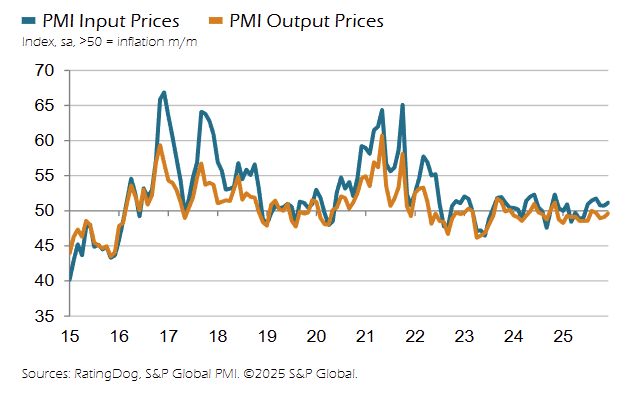

-

Output prices increased for the second consecutive month and reached a 15-month high for charge inflation, suggesting that firms continued to pass some of the higher input costs through to customers.

-

Business confidence strengthened to an 11-month high, with firms citing stronger market demand, new production lines, and improvements in production capacity and efficiency as supporting expectations for higher future output.

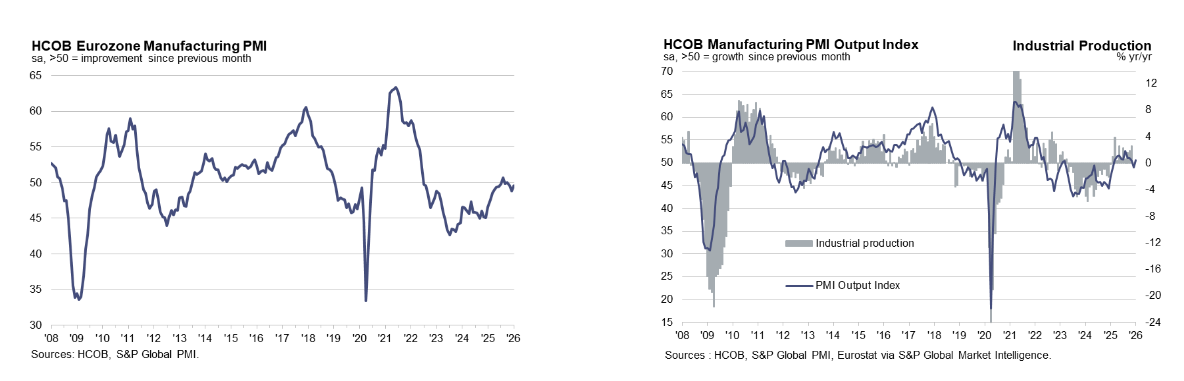

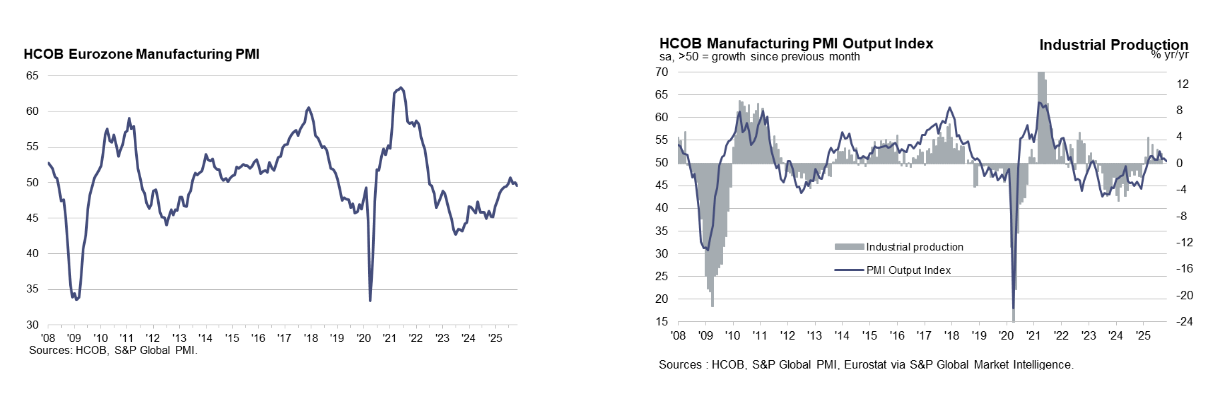

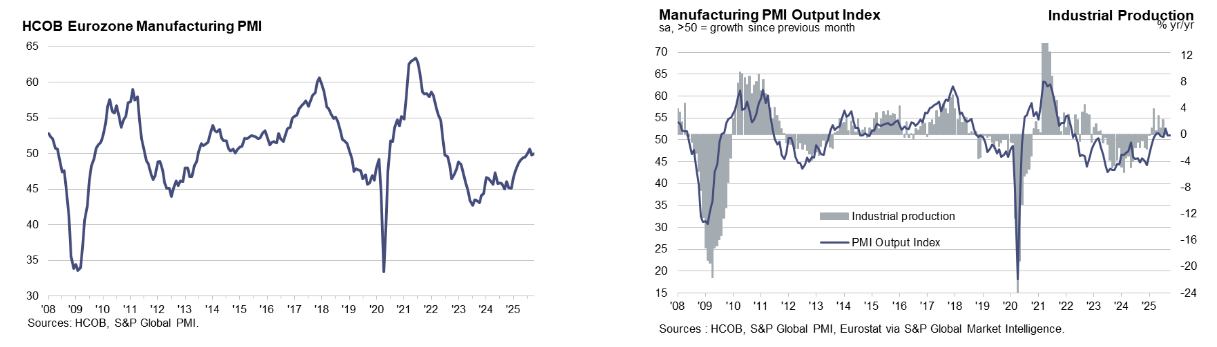

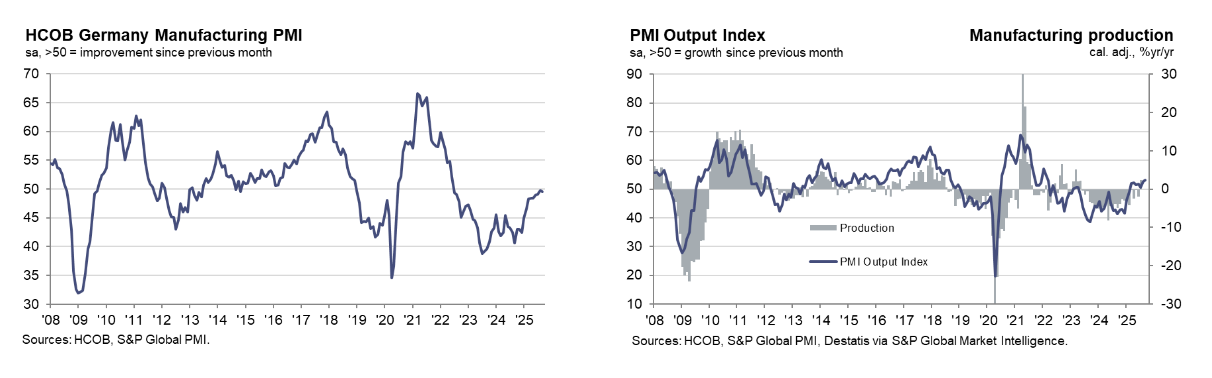

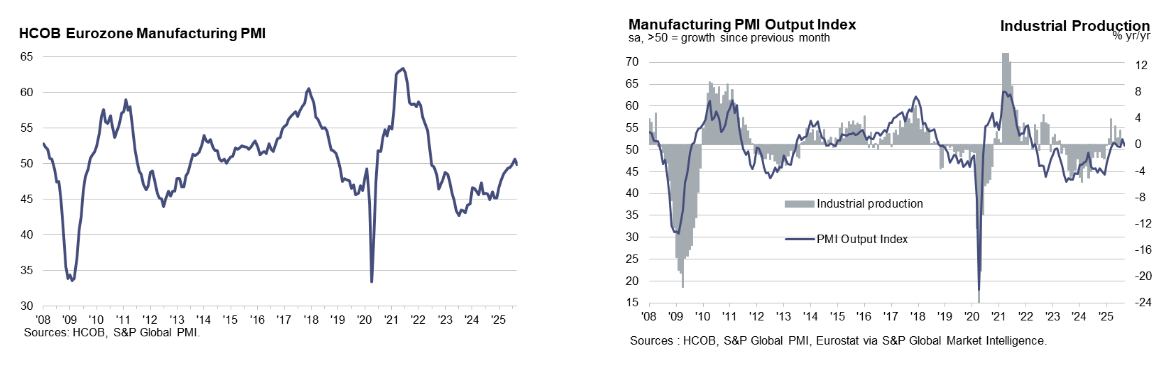

Eurozone

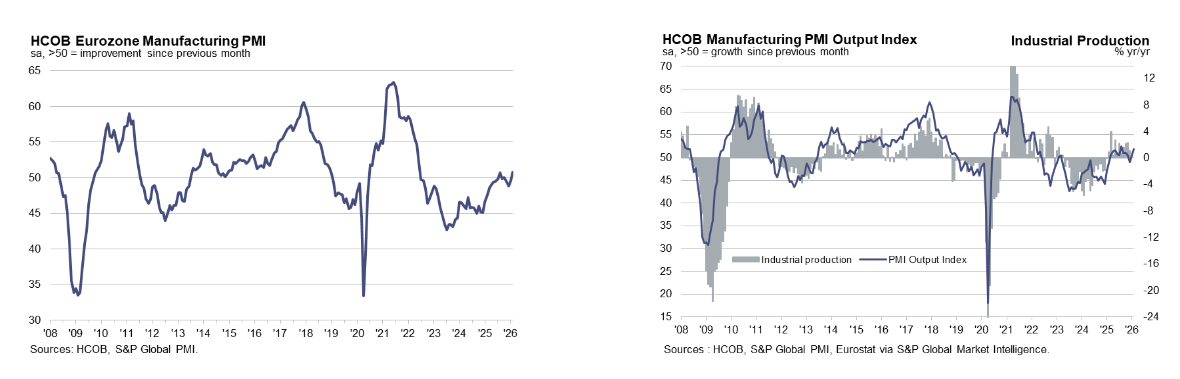

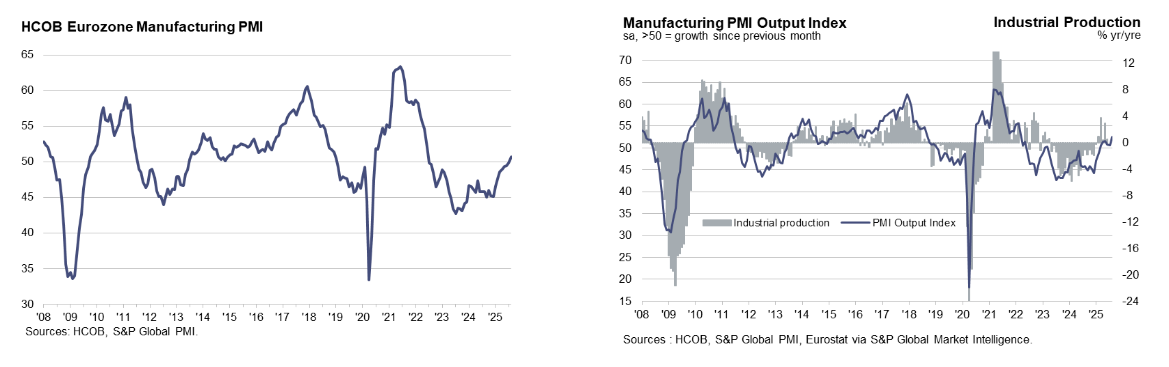

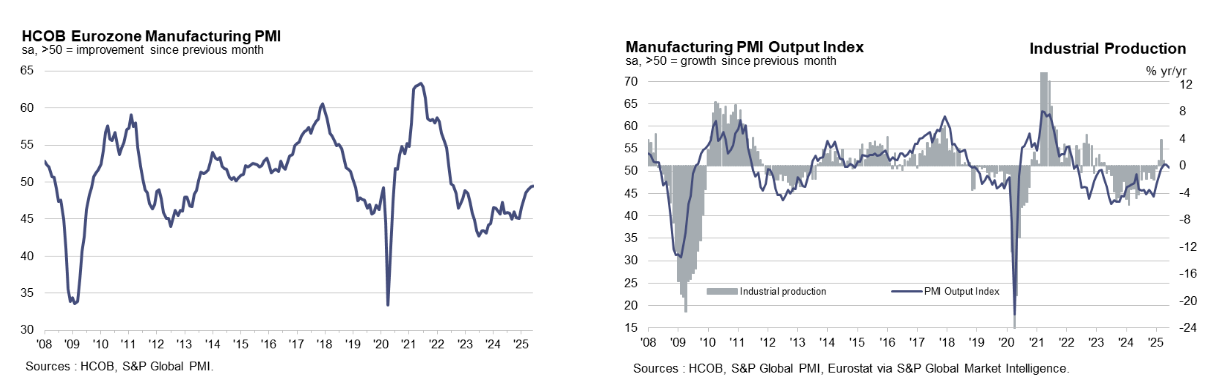

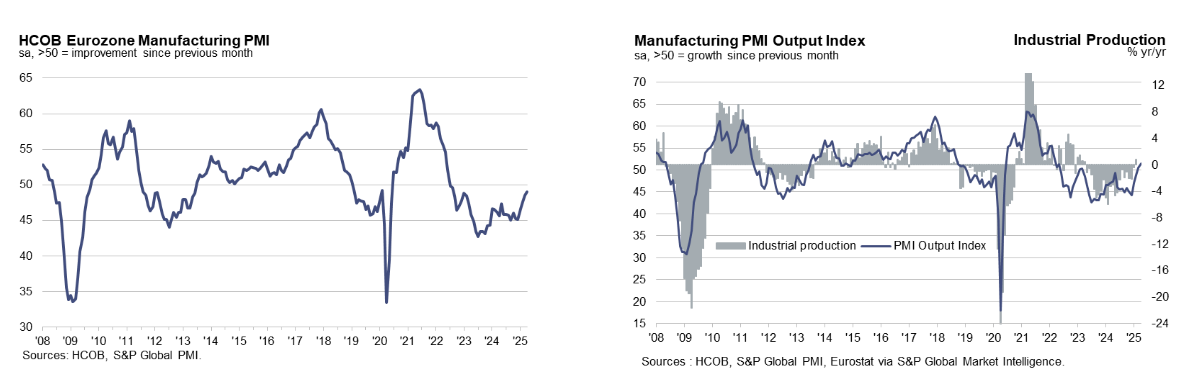

The HCOB Eurozone Manufacturing PMI rose to 50.8 in February (Jan: 49.5), moving back into expansion territory and reaching a 44-month high as improving demand supported broader operating conditions.

-

The Output Index increased to 51.9 (Jan: 50.5), a 6-month high, indicating production growth strengthened alongside improving order flows.

-

New orders expanded for only the second time in nearly four years and at the fastest pace since April 2022, showing a clear demand improvement after a prolonged weak period, while export declines moderated to the mildest contraction in three months.

-

Six of eight monitored countries recorded expansion, including Germany posting its strongest improvement in almost four years, whereas France stalled and Spain and Austria lagged, highlighting uneven regional performance.

-

Manufacturing employment continued to decline, consistent with the trend since June 2023, but backlog reductions slowed to the weakest pace in over three-and-a-half years as rising new work reduced the need to run down existing orders.

-

Purchasing activity nearly stabilised after a prolonged contraction and delivery times lengthened for a ninth straight month, while input inventories still fell but at the slowest rate since early-2023, suggesting supply and demand conditions were balancing.

-

Input cost inflation accelerated for a third consecutive month to a 38-month high, and output prices rose for a second straight month at the fastest rate since March 2023, indicating building inflation pressures within the sector.

-

Business confidence strengthened to a four-year high, the most optimistic outlook since early-2022, reflecting improved expectations for year-ahead production growth.

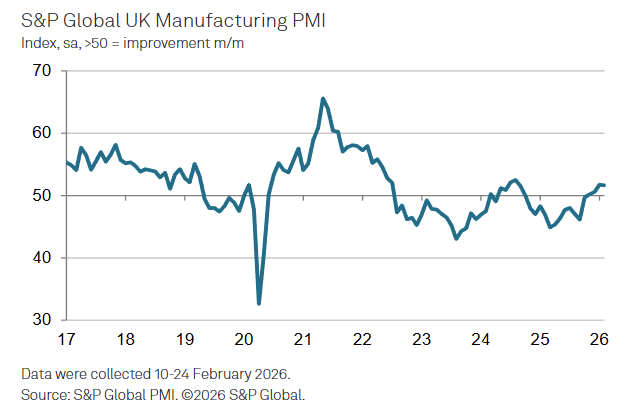

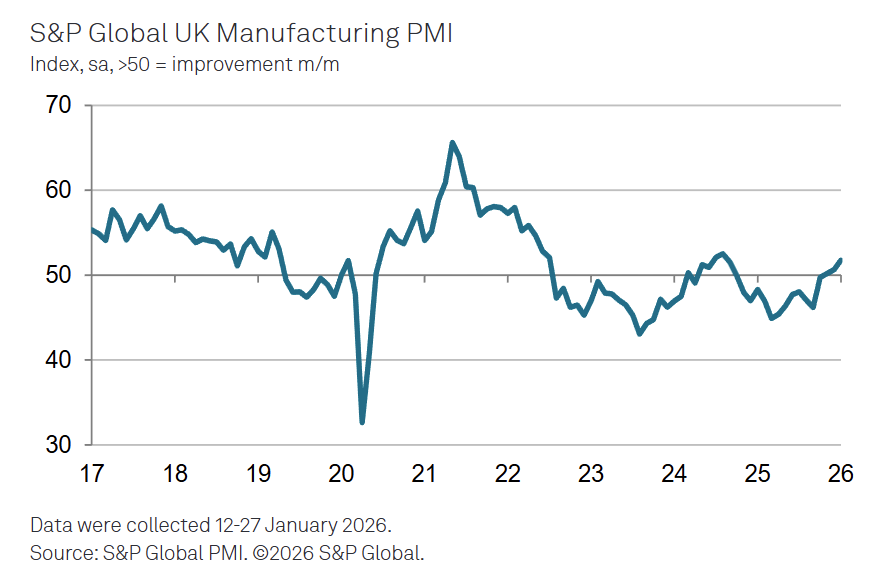

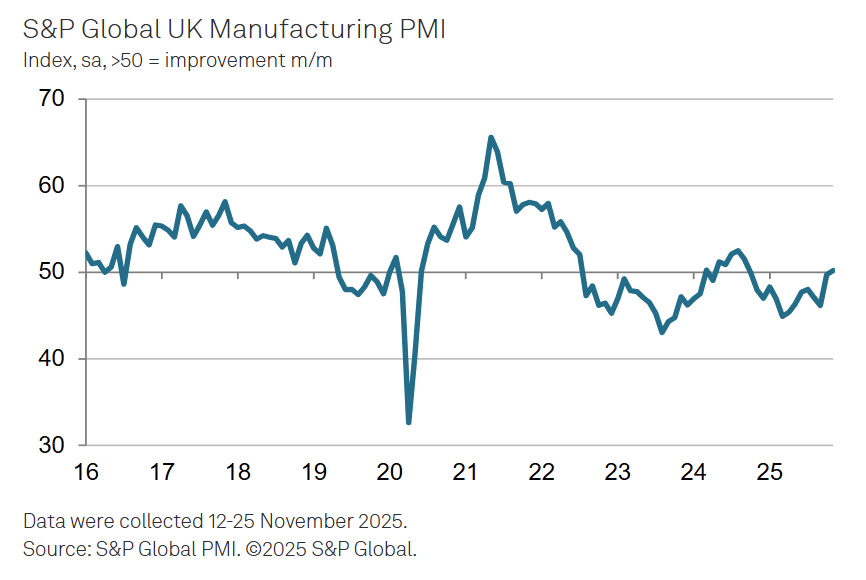

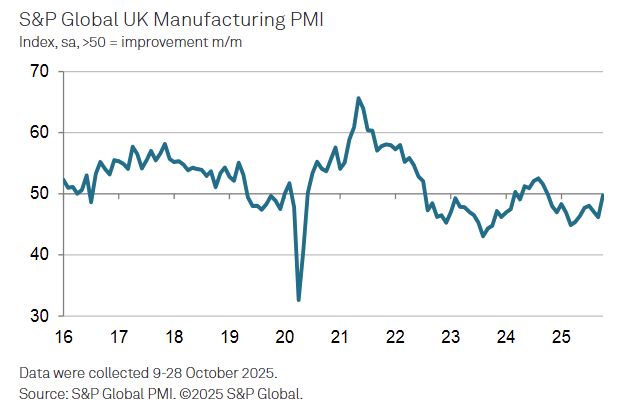

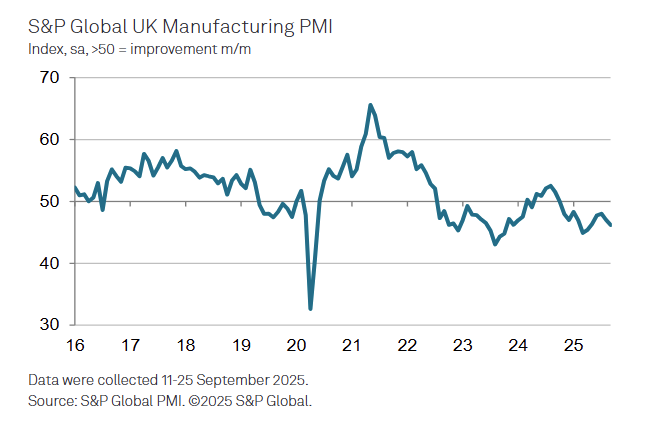

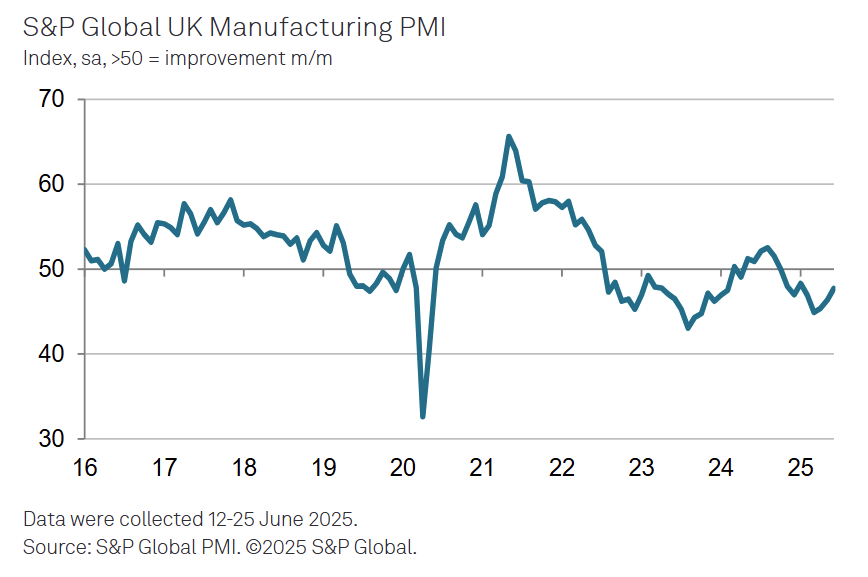

UK

The S&P Global UK Manufacturing PMI registered 51.7 in February (Jan: 51.8), remaining in expansion for a fourth straight month as stronger domestic and overseas demand supported production momentum.

-

Manufacturing output rose for the fifth consecutive month and at a 17-month high, reflecting higher new business inflows and slightly improved client confidence.

-

New export orders increased at the fastest pace in four-and-a-half years, with demand strengthening across mainland China, the EU, the Middle East and North America, indicating broad-based external demand support.

-

Three of the five PMI components improved operating conditions, while employment and stocks of purchases declined, showing growth occurring alongside ongoing inventory and labour adjustments.

-

Business optimism stayed close to January’s recent high, with nearly three-fifths of firms expecting output growth over the next 12 months, supported by product launches, investment plans and improving client confidence.

-

Employment fell for a sixteenth consecutive month but only mildly, the slowest decline of the current downturn, suggesting labour market conditions were stabilising.

-

Input cost inflation accelerated for a third straight month to a six-month high, and selling prices rose for a third consecutive month, though at a slightly softer pace than January, indicating continued but moderated pass-through.

-

Supply chains remained stretched as vendor delivery times lengthened for a 26th consecutive month, while small firms saw contracting output and orders even as medium and large firms expanded.

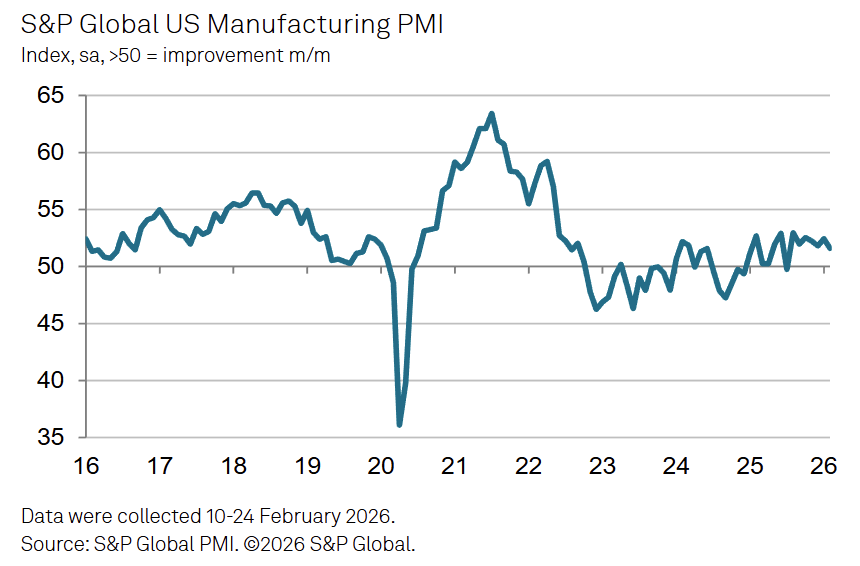

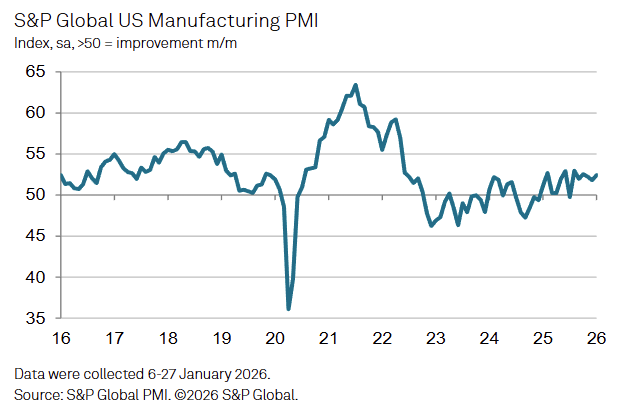

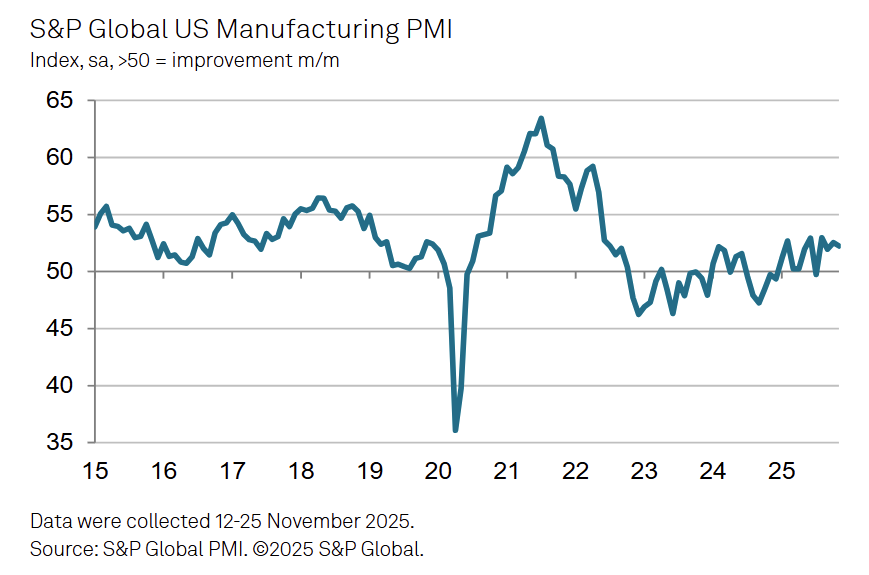

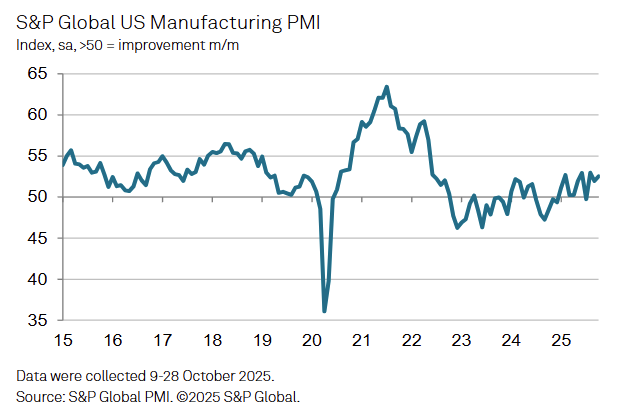

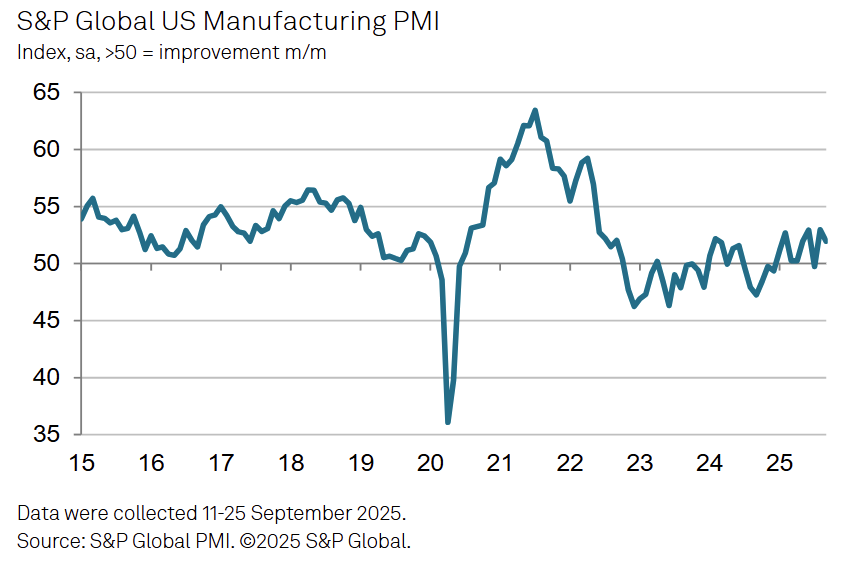

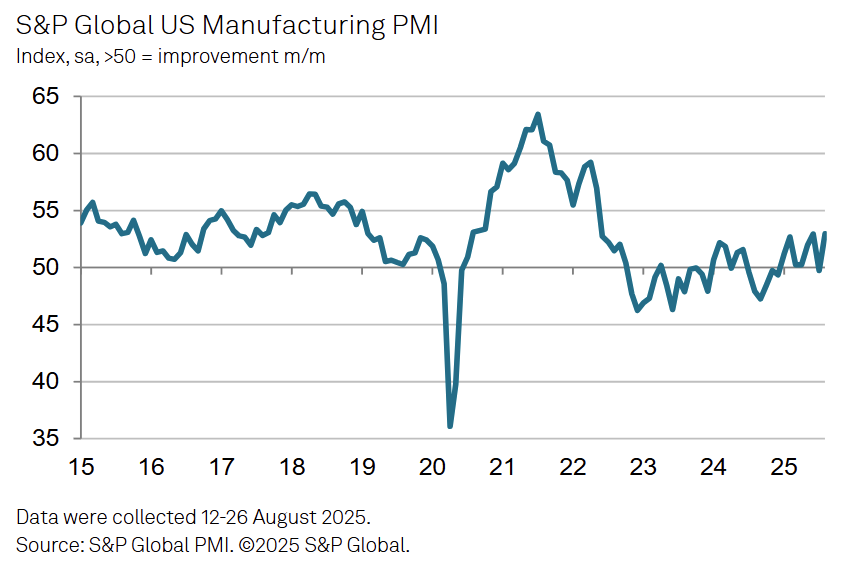

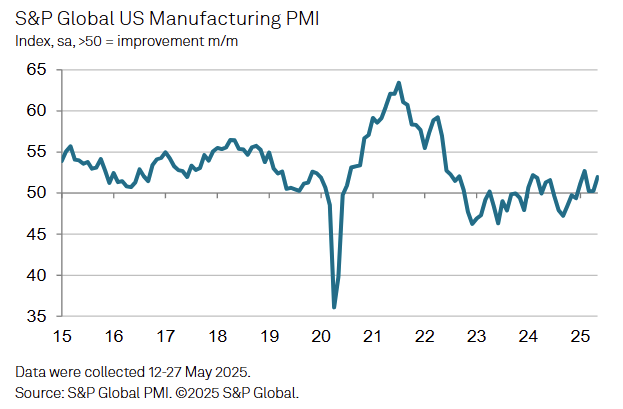

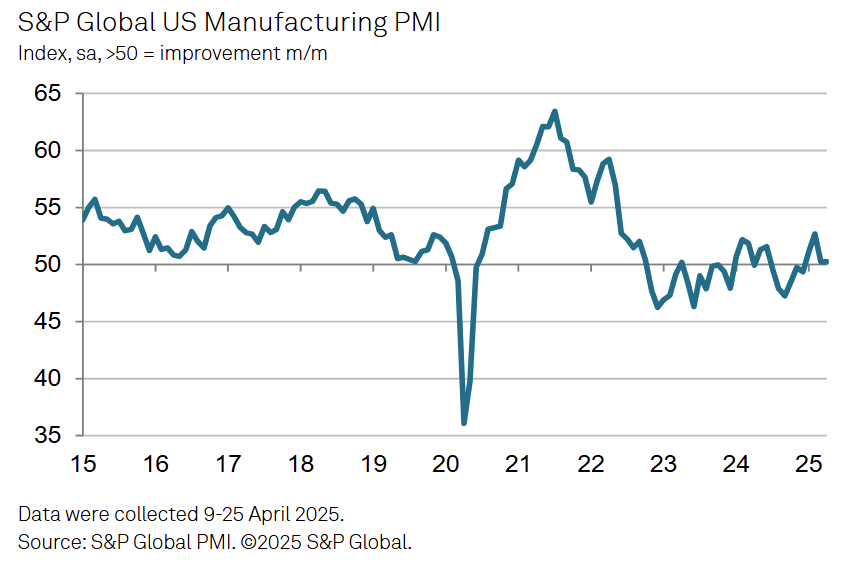

US

The S&P Global US Manufacturing PMI edged down to 51.6 in February (Jan: 52.4), marking the weakest expansion in seven months as slower orders and export declines moderated overall growth.

-

Output and new orders both increased but at softer rates, with production rising at the slowest pace since last September and new work only marginally higher as tariffs, high prices and extreme weather weighed on demand.

-

New export orders fell for an eighth consecutive month and at the sharpest rate since April 2025, particularly reflecting weaker sales to Canada, showing continued reliance on domestic demand.

-

Employment growth was minimal as firms showed restraint in hiring due to concerns about order book health and declining backlogs, indicating excess capacity limited workforce expansion.

-

Inventories of finished goods were unchanged, ending a six-month accumulation phase, while firms also reduced pre-production inventories for the first time in seven months as part of cost control efforts.

-

Supplier performance deteriorated with transportation delays and low stock availability, and purchasing activity rose more slowly than in January, indicating ongoing supply constraints.

-

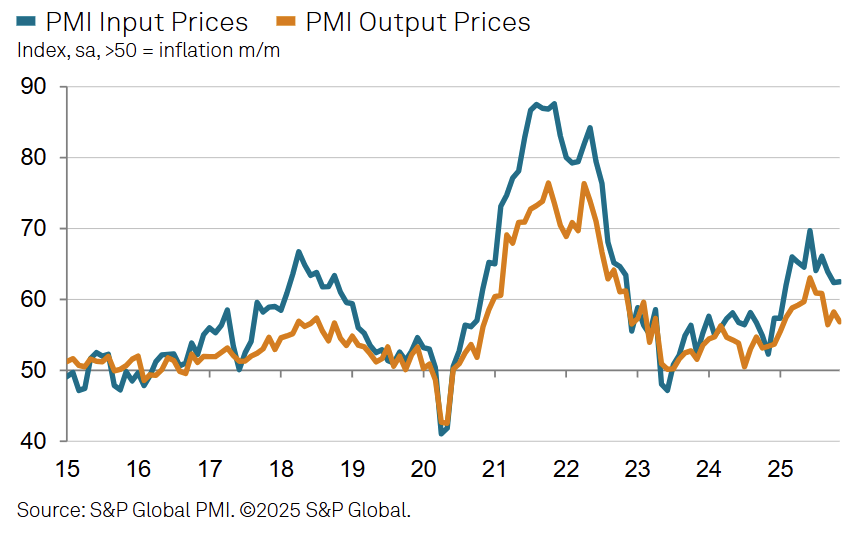

Input cost inflation remained elevated but below 2025 peaks due to tariffs and raw material prices, while selling price inflation slowed to a 14-month low as competitive pressures limited pass-through.

-

Business optimism strengthened to an eight-month high, supported by expectations for product launches and expansion plans despite uncertainty surrounding tariffs and the broader political environment.

-

Global - 2/2/2026

Asia Pacific

- Australia - 2/1/2026

- Malaysia - 2/2/2026

- ASEAN - 2/2/2026

- Myanmar - 2/2/2026

- Philippines - 2/2/2026

- Thailand - 2/2/2026

- Vietnam - 2/2/2026

- Indonesia - 2/2/2026

- Japan - 2/2/2026

- Taiwan - 2/2/2026

- China - 2/2/2025

- India - 2/2/2026

- Russia - 2/2/2025

- Kazakhstan - 2/2/2026

- South Korea - 2/2/2026

- Pakistan - 2/2/2026

Europe

- Austria - 1/28/2025

- Ireland - 2/2/2026

- Netherlands - 2/2/2026

- Romania - 2/2/2026

- Turkiye - 2/2/2026

- Poland - 2/2/2026

- Spain - 2/2/2026

- Czechia - 2/2/2026

- Italy - 2/2/2026

- France - 2/2/2026

- Germany - 2/2/2026

- Eurozone - 2/2/2026

- Greece - 2/2/2026

- UK - 2/2/2026

North & South America

Key Results

Japan

Japan’s Manufacturing PMI increased +1.5 pts MoM to 51.5 in January, returning manufacturing conditions to expansion for the first time since June and at the fastest pace since August 2022.

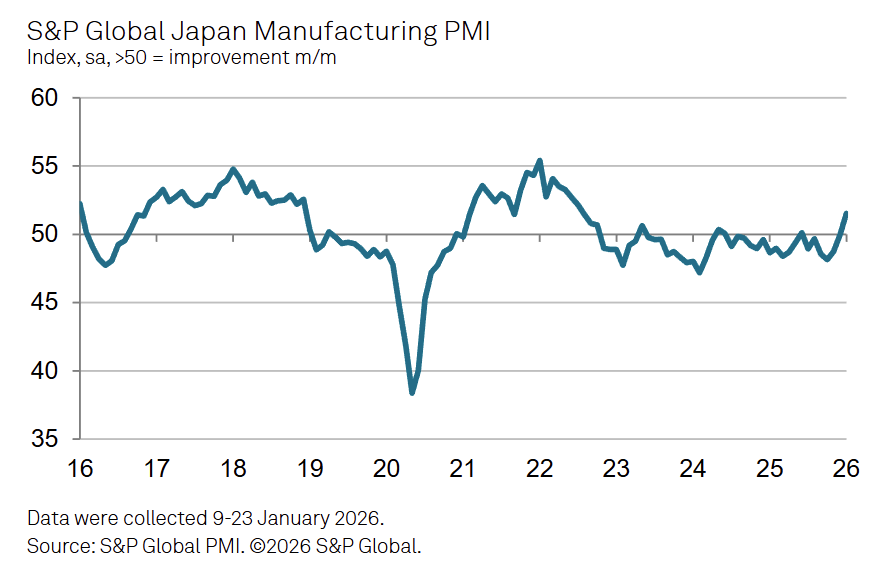

-

Total new orders rose for the first time since May 2023 and at the strongest rate in nearly four years, indicating a broad pickup in demand.

-

New export orders increased for the first time since February 2022, reflecting improved overseas demand, including from the U.S. and Taiwan.

-

Output expanded for the first time since June, with growth the fastest since April 2022 and above the long-run average.

-

Backlogs of work rose for the first time in three-and-a-half years, signaling increased pressure on manufacturing capacity.

-

Employment increased at the fastest pace in roughly 40 months, alongside the first rise in purchasing activity since September 2024.

-

Input costs accelerated at the sharpest rate in nearly a year, while selling price inflation reached a 19-month high as firms passed higher costs to customers.

China

China’s Manufacturing PMI rose +0.2 pts MoM to 50.3 in January, marking a second consecutive month above 50 and the quickest growth rate in three months.

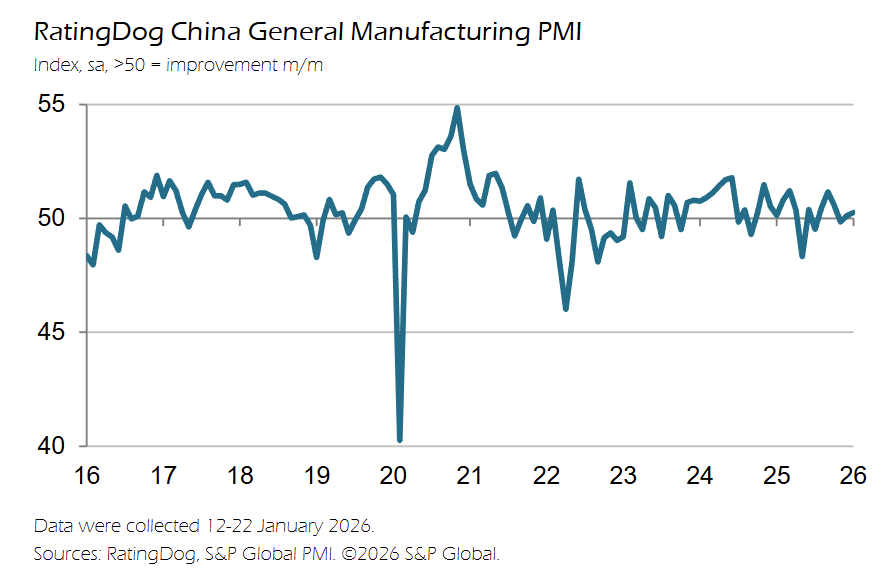

-

Manufacturing output expanded at a faster rate than in December, supported by higher inflows of new business.

-

Total new orders increased again, including a fresh rise in new export orders after December’s contraction, with demand notably strengthening from Southeast Asia.

-

Employment rose for the first time in three months as firms added staff to manage rising workloads and production needs.

-

Outstanding business declined for the first time in eight months, reflecting improved capacity alongside workforce expansion and efficiency gains.

-

Purchasing activity increased and stocks of purchases rose for a second straight month, while inventories of finished goods continued to fall as orders were fulfilled.

-

Input prices climbed for a seventh consecutive month and at the fastest pace since September 2025, contributing to the first rise in output charges since November 2024, with price increases among the strongest in roughly 18 months.

Eurozone

The Eurozone HCOB Manufacturing PMI increased +0.7 pts MoM to 49.5 in January, reaching a two-month high but remaining below the 50 expansion threshold for a third consecutive month.

-

The Output Index climbed to 50.5 (from 48.9), a three-month high, reinstating production growth after December’s first output decline in ten months.

-

New orders fell for a third straight month, though the contraction slowed and was described as marginal, while new export orders also continued to decline in line with the trend since last July.

-

Employment declined for a thirty-second consecutive month, but the pace of job losses eased to the softest since September 2025, indicating slower workforce reductions.

-

Purchasing activity and inventories both decreased again, with firms cutting buying volumes modestly and accelerating drawdowns in both pre- and post-production stocks.

-

Input price inflation accelerated to a three-year high, reflecting stronger cost pressures, while output charges were broadly unchanged MoM, signaling limited pricing power.

-

Business confidence improved to its highest level since February 2022, pointing to a more optimistic 12-month production outlook despite ongoing near-term weakness.

UK

The UK S&P Global Manufacturing PMI rose +1.2 pts MoM to 51.8 in January, a 17-month high and the third consecutive month above the 50 expansion threshold.

-

Manufacturing production increased for a fourth straight month, reaching its joint-fastest pace since September 2024, supported by export demand, stable domestic conditions, and customer restocking.

-

New orders grew at the quickest pace in nearly four years, with gains across consumer, intermediate, and investment goods, signaling broad-based demand improvement.

-

New export orders rose for the first time in four years, with higher sales reported to Europe, the US, China, and several emerging markets.

-

Employment continued to decline for a fifteenth consecutive month, but the rate of job losses slowed to the weakest since cuts began, pointing to easing labor contraction.

-

Purchasing activity increased at the fastest pace in over three and a half years, while supplier delivery performance deteriorated further, indicating stretched supply chains.

-

Input costs and selling prices both accelerated mildly, with firms citing higher raw material and supplier-passed costs, alongside a second consecutive monthly rise in output charges.

US

The US S&P Manufacturing PMI increased +0.6 pts MoM to 52.4 in January, marking a faster pace of manufacturing expansion broadly in line with the survey average.

-

Manufacturing output surged at the joint-sharpest rate since May 2022 and the strongest since August, pointing to a notable upturn in production momentum.

-

New orders returned to expansion but rose only modestly and remained below the survey average, indicating limited underlying demand growth.

-

New export orders fell for a seventh consecutive month, with tariffs and trade uncertainty cited as weighing on overseas demand, particularly from Europe and South America.

-

Finished goods inventories increased for a sixth straight month, though at the slowest pace of the sequence, reflecting production continuing to outpace sales.

-

Backlogs of work rose modestly after four months of decline, suggesting slightly higher workload pressures as order inflows improved.

-

Employment increased again, but only modestly and at the slowest pace in three months, showing cautious hiring despite stronger output.

-

Input cost inflation accelerated due to tariff-related price increases from suppliers, while output charges rose at their fastest rate since August, signaling intensifying price pressures.

-

Global - 1/2/2026

Asia Pacific

- Australia - 1/1/2026

- Malaysia - 1/2/2026

- ASEAN - 1/5/2026

- Myanmar - 1/5/2026

- Philippines - 1/2/2026

- Thailand - 1/5/2026

- Vietnam - 1/2/2026

- Indonesia - 1/2/2026

- Japan - 1/5/2026

- Taiwan - 1/2/2026

- China - 12/31/2025

- India - 1/2/2026

- Russia - 12/29/2025

- Kazakhstan - 1/5/2026

- South Korea - 1/2/2026

- Pakistan - 1/2/2026

Europe

- Austria - 12/29/2025

- Ireland - 1/2/2026

- Netherlands - 1/2/2026

- Romania - 1/5/2026

- Turkiye - 1/2/2026

- Poland - 1/2/2026

- Spain - 1/2/2026

- Czechia - 1/2/2026

- Italy - 1/2/2026

- France - 1/2/2026

- Germany - 1/2/2026

- Eurozone - 1/2/2026

- Greece - 1/2/2026

- UK - 1/2/2026

North & South America

Key Results

China

China’s Manufacturing PMI rose to 50.1 in December (from 49.9 in November), signaling a marginal return to expansion at year-end.

-

Manufacturing output returned to growth after stalling in late Q4, supported by higher inflows of new work and improved domestic demand conditions.

-

Total new orders expanded again, marking a seventh consecutive month of growth, while new export orders fell for a second time in three months, indicating demand strength was domestically driven.

-

Purchasing activity was unchanged, reflecting reports that firms held sufficient raw material and semi-finished goods inventories.

-

Stocks of purchases increased after a November decline, while supplier delivery times shortened, pointing to improved vendor performance and logistics coordination.

-

Employment declined for a second consecutive month, with firms citing restructuring efforts and cost pressures as drivers of lower staffing levels.

-

Input price inflation intensified, rising for a sixth straight month and at the fastest pace since September, driven largely by higher raw material and metal prices.

-

Output prices continued to fall as manufacturers cut selling prices to support sales and reduce inventories, though export prices rose for the first time in three months.

-

Business sentiment remained positive but eased from November and stayed below its historical average, indicating cautious optimism about growth prospects in 2026.

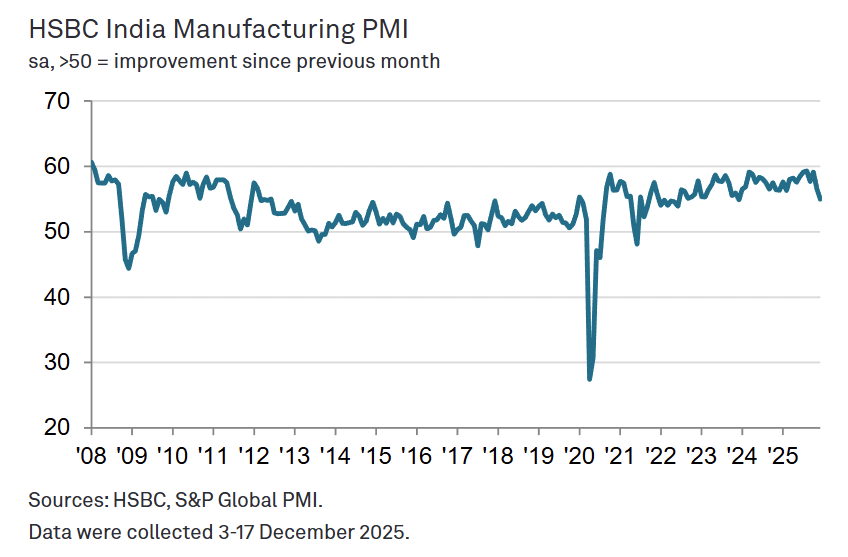

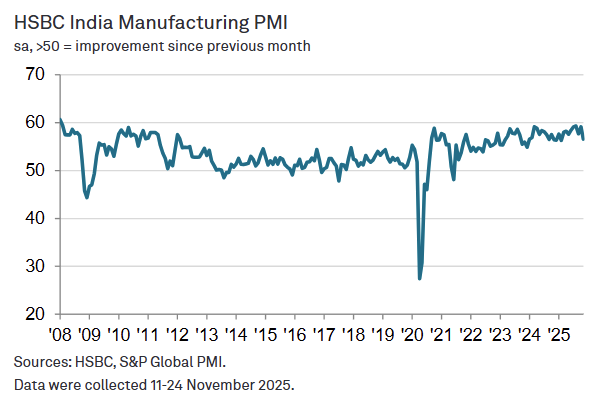

India

India’s HSBC Manufacturing PMI fell to 55.0 in December (from 56.6 in November), marking easing growth momentum while remaining firmly in expansion.

-

New business intakes rose sharply but at the weakest pace since December 2023, indicating continued demand growth with some loss of momentum.

-

Manufacturing output expanded at its slowest rate since October 2022, reflecting softer sales growth and competitive pressures despite ongoing expansion.

-

New export orders increased at the mildest pace in 14 months, showing a moderation in external demand even as gains were reported across Asia, Europe, and the Middle East.

-

Purchasing activity rose but slowed to a two-year low, as firms limited input buying in response to softer growth in new orders.

-

Employment increased only marginally, with job creation at the slowest pace in the current 22-month expansion, pointing to reduced pressure on operating capacity.

-

Input cost inflation remained historically subdued and little changed from November, while output price inflation eased to a nine-month low, signaling limited pricing pressures.

-

Input inventories rose sharply, while finished goods inventories declined at one of the fastest rates in eight months, indicating reliance on existing stock to meet demand.

-

Business confidence eased to its lowest level in nearly three-and-a-half years, despite expectations for higher output in 2026.

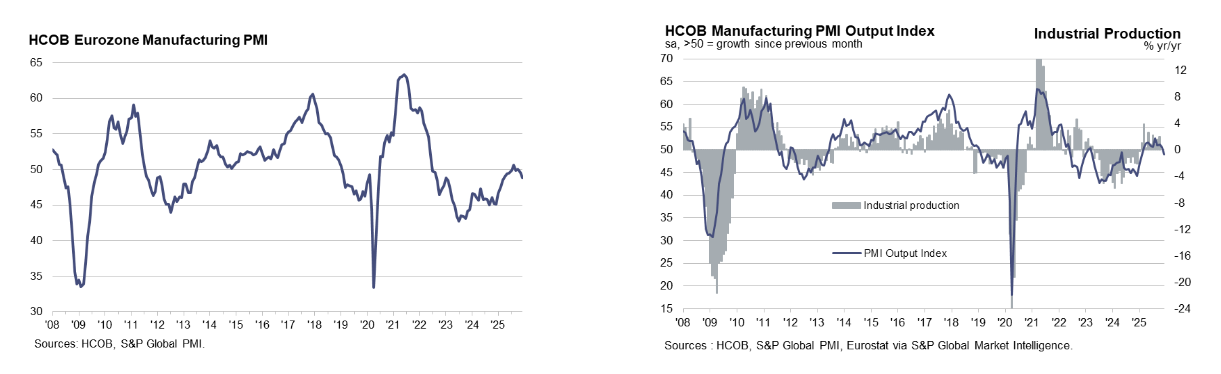

Eurozone

Eurozone manufacturing activity weakened further in December, with the HCOB Eurozone Manufacturing PMI falling to 48.8 (from 49.6 in November), reflecting a renewed decline in output and faster demand deterioration.

-

Factory output declined for the first time since February 2025, as the Output Index fell to 48.9 (from 50.4), its weakest reading in 10 months.

-

New orders fell at the fastest pace in nearly a year, marking a second consecutive monthly decline and pointing to worsening demand conditions.

-

New export orders drove much of the weakness, with international demand contracting at the sharpest rate in 11 months.

-

Purchasing activity was cut at the strongest pace since March 2024, while stocks of raw materials and intermediate goods declined sharply, indicating active retrenchment.

-

Finished goods inventories continued to fall, though at the slowest pace since September 2024, suggesting ongoing reliance on existing stock to meet demand.

-

Input cost inflation accelerated to a 16-month high amid lengthening supplier delivery times, while output prices fell for the seventh time in eight months, highlighting continued discounting.

-

Employment declined for a 30th consecutive month, but backlogs of work were reduced, indicating sufficient capacity despite falling staffing levels.

-

Despite current weakness, business confidence improved, with year-ahead production expectations reaching their highest level since February 2022.

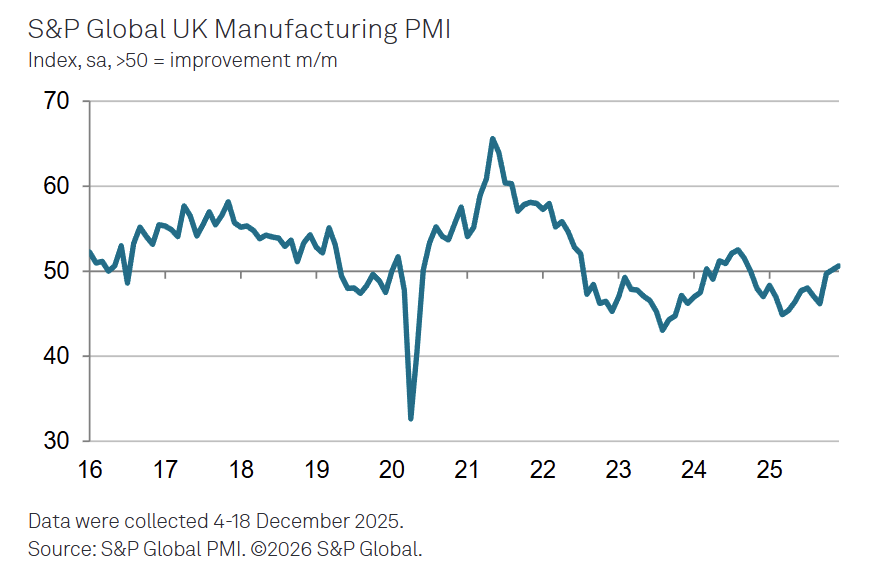

UK

The UK Manufacturing PMI rose to 50.6 in December (from 50.2 in November), marking a 15-month high and signaling continued, modest expansion.

-

Manufacturing output increased for a third consecutive month, supported largely by stock building and efforts to clear backlogs rather than a strong acceleration in demand.

-

New orders rose for the first time since September 2024, indicating a tentative improvement in demand conditions after a prolonged downturn.

-

Growth was uneven by firm size, with large manufacturers driving gains while small and medium-sized firms continued to report contraction in both output and new orders.

-

Domestic demand remained the main source of support, while new export orders fell for a forty-seventh straight month, though the pace of decline was among the weakest in that sequence.

-

Employment declined for a fourteenth consecutive month, but the rate of job losses slowed to its weakest pace over that period, suggesting easing labor market contraction.

-

Purchasing activity and stocks of purchases continued to fall, albeit less sharply than in November, pointing to ongoing caution in inventory management.

-

Input price inflation accelerated in December, reflecting higher costs for energy, metals, electronics, and packaging, while output prices rose again after a brief decline in November.

-

Business optimism slipped from November’s nine-month high, with firms citing concerns over high costs, taxation, competitiveness, and policy uncertainty despite recent stabilization signs.

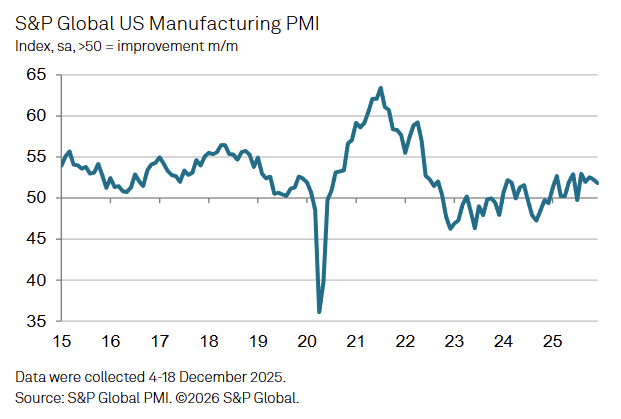

US

The US S&P Manufacturing PMI eased to 51.8 in December (from 52.2 in November), marking a slower pace of expansion as demand weakened despite continued output growth.

-

New orders declined for the first time in exactly one year, signaling a mild but notable softening in demand conditions after a prolonged expansion.

-

Output continued to grow but at the slowest pace in three months, as production remained solid even amid weaker sales momentum.

-

New export orders fell for a seventh consecutive month, with tariffs cited as a key factor weighing on international demand, particularly exports to Canada.

-

Finished goods inventories increased for a fifth straight month, though the pace of accumulation slowed sharply from November’s record, indicating production continued to outpace sales.

-

Employment growth strengthened to its most pronounced level since August, reflecting firms filling vacancies in anticipation of stronger conditions in 2026.

-

Backlogs of work declined for a fourth consecutive month, pointing to expanding labor capacity and limited workload pressures.

-

Input cost inflation moderated to an 11-month low but remained historically elevated, while output price inflation also slowed to its weakest rate since early 2025, still reflecting tariff-related cost pressures.

-

Business confidence remained positive but eased from November, as firms cited uncertainty around tariffs and insufficient new orders to replace existing demand.

-

Global - 12/1/2025

Asia Pacific

- Australia - 11/30/2025

- Malaysia - 12/1/2025

- ASEAN - 12/1/2025

- Myanmar - 12/1/2025

- Philippines - 12/1/2025

- Thailand - 12/1/2025

- Vietnam - 12/1/2025

- Indonesia - 12/1/2025

- Japan - 12/1/2025

- Taiwan - 12/1/2025

- China - 12/1/2025

- India - 12/1/2025

- Russia - 11/1/2025

- Kazakhstan - 12/1/2025

- South Korea - 12/1/2025

- Pakistan - 12/1/2025

Europe

- Austria - 11/26/2025

- Ireland - 12/1/2025

- Netherlands - 12/1/2025

- Romania - 12/1/2025

- Turkiye - 12/1/2025

- Poland - 12/1/2025

- Spain - 12/1/2025

- Czechia - 12/1/2025

- Italy - 12/1/2025

- France - 12/1/2025

- Germany - 12/1/2025

- Eurozone - 12/1/2025

- Greece - 12/1/2025

- UK - 12/1/2025

North & South America

Key Results

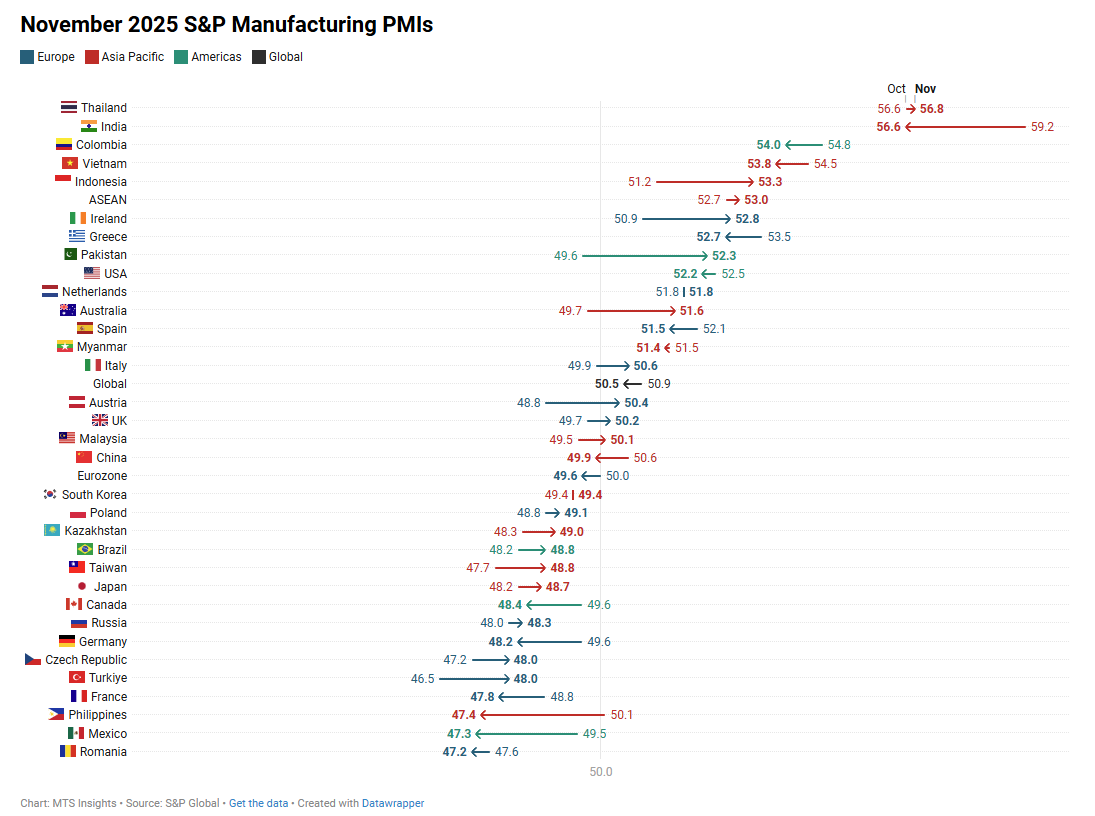

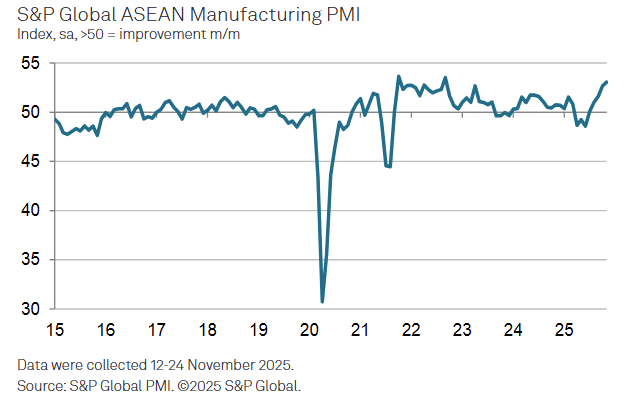

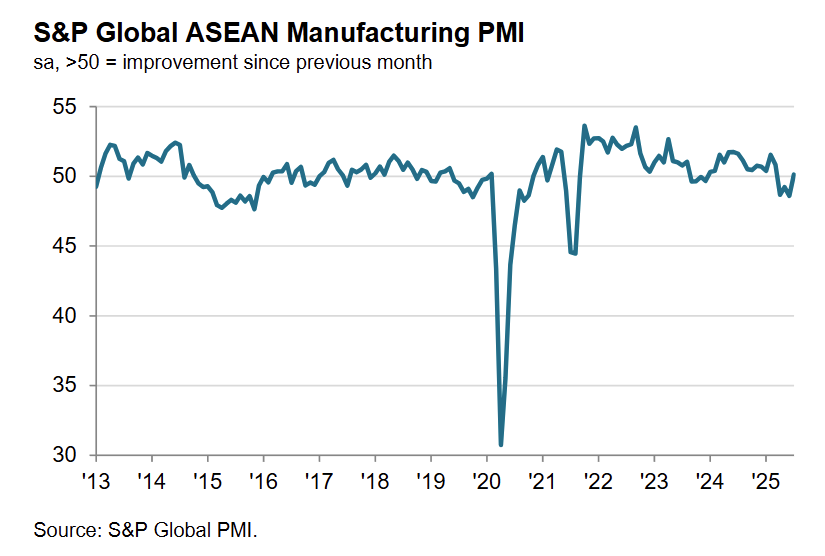

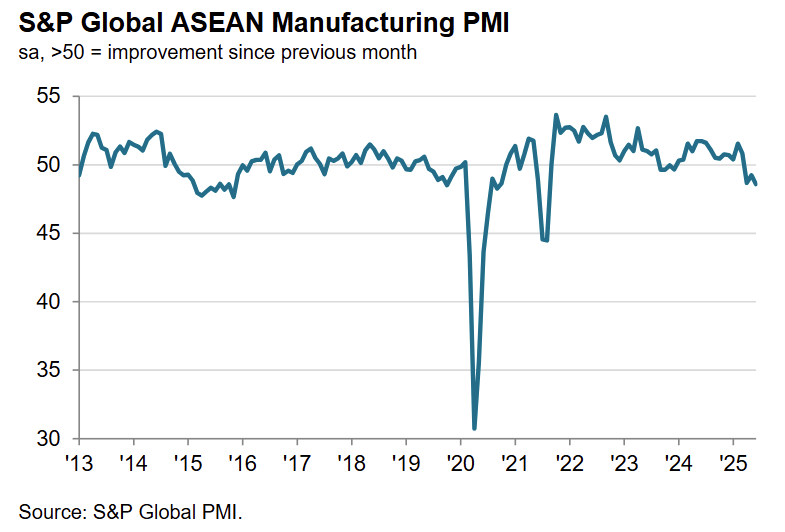

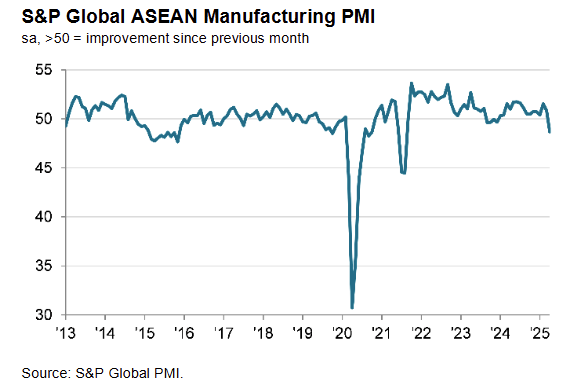

ASEAN

The S&P ASEAN Manufacturing PMI rose to 53.0 in November (from 52.7 in October), marking the third-strongest reading on record and signaling a clear acceleration in regional factory activity.

-

Output and new orders both expanded at faster and historically strong rates, underscoring broad momentum in domestic demand.

-

International orders declined again, showing that external demand lagged even as total new business strengthened.

-

Purchasing activity grew at the fastest pace since March 2024, extending its expansion streak to four months as firms supported rising production needs.

-

Employment increased for the third consecutive month, but gains were only fractional, contributing to capacity pressures and a record rise in backlogs.

-

Input costs rose sharply and at the fastest pace in nearly a year, prompting firms to raise output prices, though both inflation rates remained historically subdued.

-

Business confidence stayed positive and little changed compared with October, but remained below the long-run average, reflecting cautious optimism about future output.

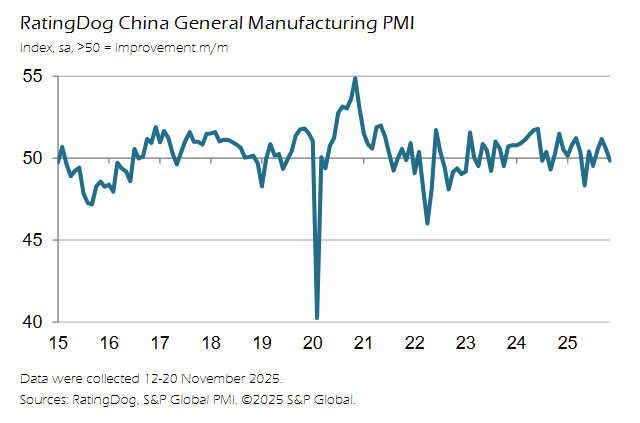

China

China’s Manufacturing PMI fell to 49.9 in November (from 50.6 in October), marking a slight contraction as production stalled and new orders slowed to near-neutral levels.

-

Output growth came to a halt after three months of expansion, reflecting softer new business inflows and weaker momentum in domestic demand.

-

Total new orders were broadly unchanged, while new export orders rose at the fastest pace in eight months, supported by improved overseas demand and new product launches.

-

Employment returned to contraction, with staffing levels declining marginally as firms cut costs through both resignations and redundancies.

-

Purchasing activity fell for the first time since June, and stocks of purchases dropped at the quickest pace since December 2023, showing caution toward inventory accumulation.

-

Finished goods inventories declined at the fastest rate in nearly three years, indicating firms were reducing holdings amid softer demand conditions.

-

Input costs continued to rise, driven largely by higher metal prices, though the rate of inflation eased to a five-month low; output prices fell further as manufacturers offered discounts.

-

Supplier delivery times shortened, helped by reduced purchasing volumes and better coordination with suppliers.

-

Business confidence improved compared with October, with firms citing expected support from government policies and upcoming product launches as reasons for optimism about future output.

India

India’s S&P Manufacturing PMI fell to 56.6 in November (from 59.2 in October), marking the slowest improvement since February but still indicating strong expansion relative to long-run norms.

-

New orders rose at a substantial pace but eased to a nine-month low, with firms citing challenging market conditions, delayed project starts and stronger competition.

-

Output expanded sharply but at the weakest rate since February, as softer demand for some product lines tempered gains from efficiency improvements and new business.

-

New export orders increased at the mildest pace in over a year despite broader strength across Africa, Asia, Europe and the Middle East, showing a clear loss of external momentum.

-

Employment rose for the 21st straight month but at the slowest rate in the current expansion, as firms adjusted hiring in line with softer sales growth.

-

Input cost inflation eased to a nine-month low and output charge inflation to an eight-month low, allowing firms to limit price increases.

-

Purchasing activity continued to grow, supporting another accumulation of input inventories, though the pace of stock-building slowed to a nine-month low.

-

Finished goods inventories fell as firms met demand directly from existing stocks, reflecting relatively subdued pressure on capacity.

-

Business confidence declined to its lowest level since mid-2022, with survey evidence pointing to concerns about competition and weaker demand conditions.

Eurozone

The Eurozone S&P Manufacturing PMI slipped to 49.6 in November (from 50.0 in October), marking a renewed but mild contraction amid softer demand and weaker conditions in Germany and France.

-

The Output Index eased to 50.4 (from 51.0), its weakest reading in nine months, showing that production growth persisted but at a slower and marginal pace.

-

New orders declined again after stabilising in October, reflecting fresh demand headwinds; new export orders also fell for a fifth straight month.

-

Employment fell at the sharpest rate since April, while purchasing activity and inventories contracted more quickly, indicating more aggressive retrenchment across factories.

-

Stocks of finished goods dropped at the fastest pace in almost four and a half years, suggesting firms relied heavily on inventories to support output.

-

Supplier delivery times lengthened to the greatest extent since October 2022, with firms reporting material shortages and difficulties sourcing internationally.

-

Input prices rose at the strongest rate since March following months of stability, yet output charges declined slightly, pointing to limited pricing power.

-

Business confidence improved and moved above its long-run average, with sentiment reaching the highest level since June despite ongoing operational softness.

-

Country performance was uneven: Ireland, Greece, the Netherlands, Spain, Italy, and Austria all recorded expansion, while Germany (48.2) and France (47.8) fell to nine-month lows and deeper into contraction.

UK

The UK Manufacturing PMI rose to 50.2 in November (from 49.7 in October), marking a 14-month high as production increased again and new orders stabilized after more than a year of declines.

-

Output expanded for a second straight month, though the rise was modest and driven mainly by investment goods; consumer and intermediate goods output continued to contract.

-

New orders were unchanged after a 13-month contraction, supported by stronger domestic demand, while new export orders fell for the forty-sixth month but at the slowest rate in a year.

-

Employment declined for the thirteenth month, with firms cutting full-time, part-time, agency and temporary roles amid cost pressures and uncertainty ahead of the Budget.

-

Backlogs fell at the quickest pace since April, highlighting excess capacity despite the upturn in production.

-

Supplier delivery times deteriorated at the fastest rate in almost a year due to vendor shortages, transport disruptions and customs delays.

-

Factory gate prices fell for the first time in more than two years as firms faced weak market conditions and discount pressure, while input cost inflation eased to its slowest pace since October 2024.

-

Stocks of purchases contracted and finished goods inventories were trimmed further, indicating ongoing caution in inventory management.

-

Business optimism rose to a nine-month high, with 56 percent of firms expecting higher output over the next year amid hopes for market stabilization, new technologies and planned expansions.

US

The US S&P Manufacturing PMI eased to 52.2 in November (from 52.5 in October), marking a fourth month of expansion but with softer demand growth and a record rise in finished-goods inventories.

-

Output rose at the fastest pace since August, supported by gains in both new and existing client orders, though the overall rise in demand was much slower than in October.

-

New export orders fell for a fifth straight month and at the steepest pace since July, reflecting ongoing tariff-related weakness in international sales.

-

Finished-goods inventories increased at the sharpest rate in the survey’s 18-year history, as production outpaced sales and firms reported weaker-than-expected demand.

-

Employment grew at the strongest pace in three months as firms filled vacancies and prepared for expected increases in production and sales.

-

Backlogs fell for a third month, indicating ample capacity and reinforcing that recent output gains were not driven by workload pressures.

-

Input buying rose only marginally, as earlier stockbuilding reduced the need for additional purchases; vendor delivery times lengthened for the third month amid border and tariff-related disruptions.

-

Input costs remained elevated, with metals frequently cited as a driver of price increases; selling price inflation eased and was among the lowest of the year as competition limited pass-through.

-

Business confidence improved to the highest level since June, supported by expectations of policy support, new product launches and increased government spending following the end of the shutdown.

-

Global - 11/3/2025

Asia Pacific

- Australia - 11/2/2025

- Malaysia - 11/3/2025

- ASEAN - 11/3/2025

- Myanmar - 11/3/2025

- Philippines - 11/3/2025

- Thailand - 11/3/2025

- Vietnam - 11/3/2025

- Indonesia - 11/3/2025

- Japan - 11/3/2025

- Taiwan - 11/3/2025

- China - 11/3/2025

- India - 11/3/2025

- Russia - 11/1/2025

- Kazakhstan - 11/3/2025

- South Korea - 11/3/2025

- Pakistan - 11/3/2025

Europe

- Austria - 10/29/2025

- Ireland - 11/3/2025

- Netherlands - 11/3/2025

- Romania - 11/3/2025

- Turkiye - 11/3/2025

- Poland - 11/3/2025

- Spain - 11/3/2025

- Czechia - 11/3/2025

- Italy - 11/3/2025

- France - 11/3/2025

- Germany - 11/3/2025

- Eurozone - 11/3/2025

- Greece - 11/3/2025

- UK - 11/3/2025

North & South America

Key Results

China

China’s Manufacturing PMI eased to 50.6 in October 2025 (from 51.2 in September), marking a slower but continued expansion in factory activity amid softer domestic demand and renewed weakness in exports.

-

New orders expanded for the fifth consecutive month but at a slower pace, as domestic sales growth was partially offset by a sharper fall in new export orders, which contracted at the fastest rate since May.

-

Output rose modestly, with firms citing slower inflows of new work and trade uncertainty as key drags on production growth.

-

Employment increased for the first time since March and at the fastest pace in over two years, as manufacturers added staff to handle existing workloads despite softer output growth.

-

Purchasing activity grew for the fourth straight month, though the rate of increase moderated; input and finished goods inventories both continued to rise, indicating sustained restocking momentum.

-

Input costs climbed at a slower rate than in September, driven by higher prices for metals and tighter supply conditions, while output prices declined for the second month in a row as firms discounted to stay competitive.

-

Business confidence fell to a six-month low, with survey respondents citing rising trade uncertainty, weaker external demand, and softer expectations for future growth.

-

The overall PMI composition showed only employment improving month-on-month, while production, new orders, and purchasing activity all eased, signaling a moderation in the pace of recovery heading into year-end.

Euro Area

The Eurozone Manufacturing PMI held at 50.0 in October 2025 (from 49.8 in September), marking a near-stagnation in factory activity as modest output growth continued to offset weak demand and ongoing job cuts.

-

Manufacturing output rose for the eighth straight month, with the Output Index at 51.0 (from 50.9), but the pace of expansion remained mild and below average for the year.

-

New orders were flat for the second consecutive month, continuing a weak trend as demand for euro area goods has risen in only one of the past 42 months; new export orders declined for the fourth month in a row.

-

Employment fell again, extending the run of job losses to nearly two and a half years, with the October decline the sharpest since June.

-

Inventories of both inputs and finished goods declined further, continuing a prolonged period of stock drawdowns as firms sought to manage weak demand and excess capacity.

-

Input costs were unchanged from September, while selling prices rose marginally for the first time since April, suggesting limited pricing power despite stable costs.

-

Supplier delivery times lengthened for the third straight month, with the extent of delays the most widespread in three years amid lingering supply chain disruptions.

-

Business sentiment remained positive but slipped for the second month in a row, staying below its long-term average as firms cited weak demand and geopolitical uncertainty.

-

By country, Greece (53.5) and Spain (52.1) led growth, while Germany (49.6), France (48.8), and Austria (48.8) remained in contraction, highlighting uneven recovery across the euro area.

UK

The UK Manufacturing PMI rose to 49.7 in October 2025 (from 46.2 in September), marking a 12-month high and the first rise in output in a year, driven partly by the restart of auto production following a cyber-attack at JLR.

-

Output increased across consumer and intermediate goods sectors, while investment goods output fell for a twelfth month, though at the slowest pace in the current downturn.

-

New orders contracted for a thirteenth straight month, but at a slower rate, with all sectors still seeing declines amid continued weakness in both domestic and overseas demand.

-

New export orders fell for the forty-fifth consecutive month, with manufacturers citing weaker demand from the US, EU, Asia, and the Middle East, alongside ongoing tariff uncertainty and competitiveness issues.

-

Employment declined for the twelfth consecutive month, though at the weakest pace in the current sequence, as firms relied on attrition and hiring freezes to manage costs amid subdued demand and high labor expenses.

-

Input costs rose at the slowest pace so far in 2025, easing in consumer and intermediate goods but rising for investment goods; higher prices were reported for energy, commodities, and shipping.

-

Selling prices increased modestly as some firms passed on higher costs, though overall inflationary pressures continued to moderate.

-

Business optimism improved to an eight-month high but remained below its long-run average, as firms balanced hopes for economic recovery and new product launches against concerns over fiscal policy, tariffs, and geopolitical uncertainty.

US

The US Manufacturing PMI rose to 52.5 in October 2025 (from 52.0 in September), marking a third consecutive month of expansion and the fastest pace of demand growth in 20 months.

-

New orders increased at the quickest rate in 20 months, supported by stronger domestic demand, while new export orders fell for the fourth straight month and at the sharpest pace since July amid ongoing tariff impacts.

-

Output grew solidly, driven by rising domestic orders and sufficient production capacity, though some manufacturers reported excess output relative to workloads.

-

Employment rose modestly for the third consecutive month but remained limited by weak confidence and spare capacity; backlogs of work declined at the fastest rate since April.

-

Inventories of finished goods surged to a survey-record high, marking a third straight month of accumulation, as firms built up stock due to slower-than-expected sales.

-

Input prices continued to rise steeply, with tariffs cited as a key driver, though the rate of inflation was the lowest since February; selling prices were raised at a faster pace than in September.

-

Supplier delivery times lengthened again, reflecting ongoing transportation delays, import challenges, and low stock availability among suppliers.

-

Business confidence fell to its lowest level since April, weighed down by trade policy uncertainty, the federal shutdown, and concerns about consumer demand, despite some optimism linked to reshoring and future investment.

-

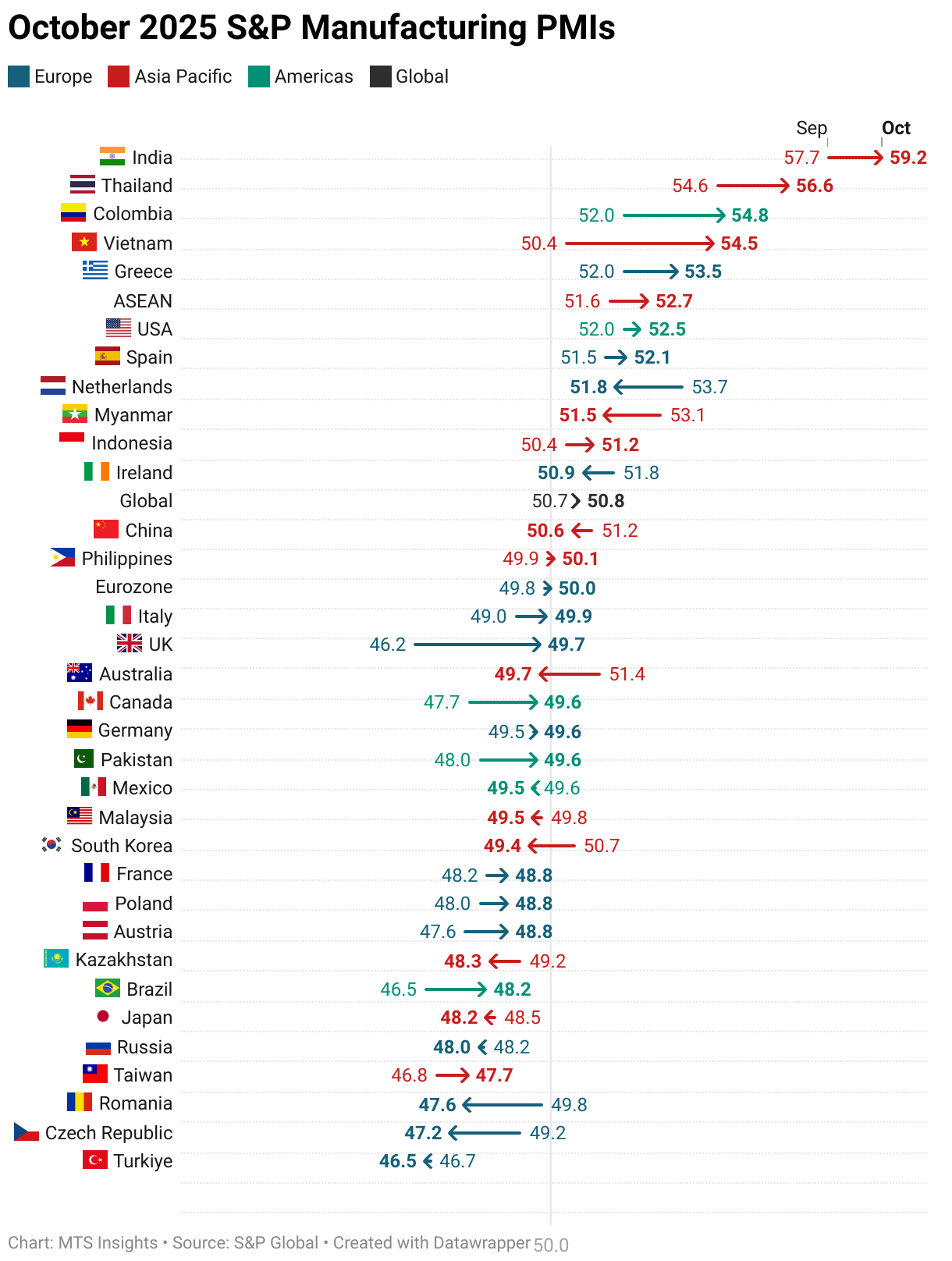

Global - 10/1/2025

Asia Pacific

- Australia - 9/30/2025

- Malaysia - 10/1/2025

- ASEAN - 10/1/2025

- Myanmar - 10/1/2025

- Philippines - 10/1/2025

- Thailand - 10/1/2025

- Vietnam - 10/1/2025

- Indonesia - 10/1/2025

- Japan - 10/1/2025

- Taiwan - 10/1/2025

- China - 9/30/2025

- India - 10/1/2025

- Russia - 10/1/2025

- Kazakhstan - 10/1/2025

- South Korea - 10/1/2025

- Pakistan - 10/1/2025

Europe

- Austria - 9/26/2025

- Ireland - 10/1/2025

- Netherlands - 10/1/2025

- Romania - 10/1/2025

- Turkiye - 10/1/2025

- Poland - 10/1/2025

- Spain - 10/1/2025

- Czechia - 10/1/2025

- Italy - 10/1/2025

- France - 10/1/2025

- Germany - 10/1/2025

- Eurozone - 10/1/2025

- Greece - 10/1/2025

- UK - 10/1/2025

North & South America

Key Results

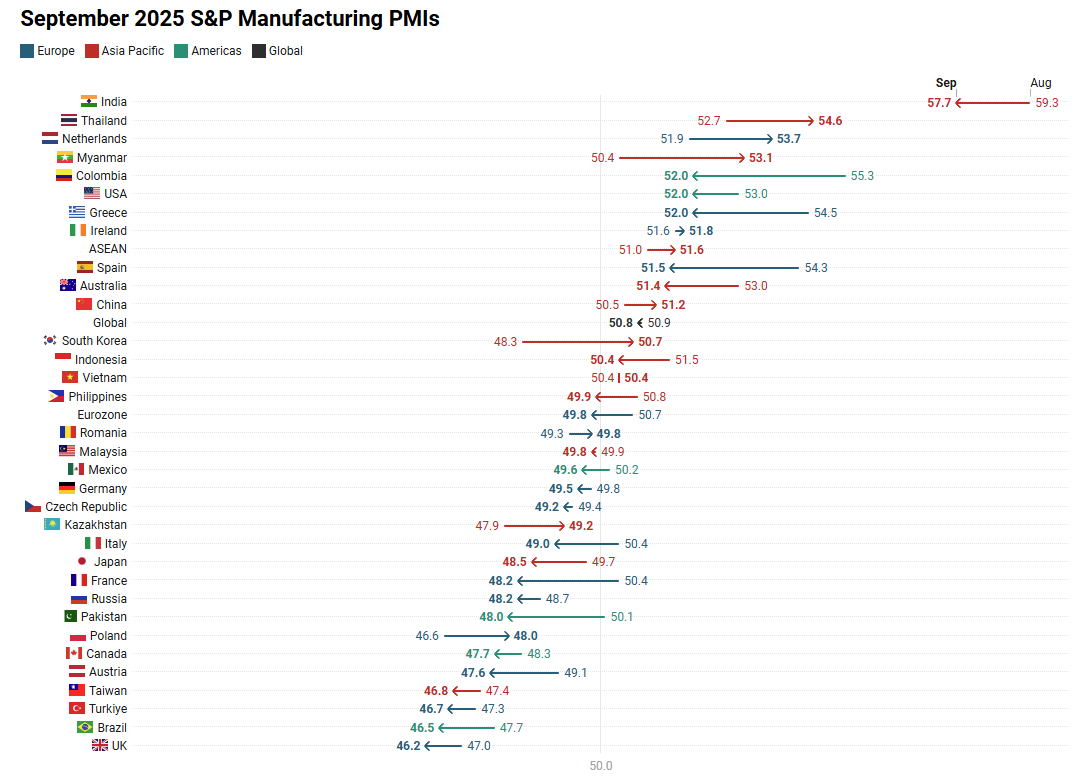

China

China’s Manufacturing PMI rose to 51.2 in September 2025 (from 50.5 in August), marking the fastest pace of expansion in six months, supported by stronger new orders and rising export demand.

-

New orders increased at the quickest pace since February, driven by better domestic demand, promotional efforts, and new product launches; new export orders grew slightly for the first time since March.

-

Production rose at the fastest rate in three months, reflecting stronger inflows of new work and continued capacity pressure.

-

Purchasing activity expanded solidly, the strongest since November 2024, leading to further inventory accumulation in both inputs and finished goods.

-

Backlogs of work grew at the quickest rate in several months, highlighting persistent strain on operating capacity.

-

Employment continued to decline, but the pace of job shedding eased as firms responded to rising workloads.

-

Input costs rose at the fastest rate in ten months, with metals and meat cited as key drivers; however, selling prices fell modestly as firms absorbed costs amid competitive pressures.

-

Business confidence improved to the highest level since March, with firms hopeful that demand, policy support, and business development will sustain growth, though sentiment remains below its long-run average.

Germany

Germany’s Manufacturing PMI slipped to 49.5 in September 2025 (from 49.8 in August), a two-month low that underscores persistent contraction, though output growth reached its strongest pace since early 2022.

-

Output rose for the seventh straight month and at the fastest rate since March 2022, led by investment goods, though much of the support came from working through backlogs.

-

New orders fell for the first time in four months, with firms citing weak demand, foreign competition, and US tariffs; export sales were little changed after declining in August.

-

Employment declined further, with job cuts accelerating to the quickest pace since June 2025, extending a retrenchment trend that began in mid-2023.

-

Purchasing activity fell for the second consecutive month and at the fastest rate since March, while input inventories contracted more slowly and post-production inventories nearly stabilized.

-

Supplier delivery times lengthened for the first time since October 2022, reflecting delays in Asian shipments and supplier capacity constraints.

-

Input costs dropped at the fastest rate in three months, helped by a strong euro and supplier switching, while output prices fell modestly, with the decline easing to its weakest since May.

-

Business expectations for the year ahead fell to a nine-month low, weighed by geopolitical risks, external competition, and concerns over the domestic economy, keeping confidence below its long-run average.

Euro Area

The HCOB Eurozone Manufacturing PMI fell back into contraction at 49.8 in September 2025 (from 50.7 in August), as new orders declined sharply and job cuts accelerated, though output growth persisted at a slower pace.

-

Output expanded for a seventh straight month, but the Output Index eased to 50.9 (from 52.5), signaling a softer pace of growth.

-

New orders decreased at the fastest rate in six months, reversing August’s rebound, with export demand falling for a third consecutive month.

-

Employment contracted at the quickest pace in three months, with firms also making deeper cuts to backlogged work.

-

Purchasing activity declined more rapidly, leading to the steepest reduction in input demand since April, while both pre- and post-production inventories continued to shrink.

-

Supplier delivery times lengthened for the first time in nearly three years, highlighting renewed supply chain pressures.

-

Input costs fell for the first time since June, though only marginally, while output prices declined for a fifth straight month amid ongoing discounting.

-

Business confidence remained positive overall but slipped to its weakest since April, as manufacturers grew more cautious about the outlook.

UK

The S&P Global UK Manufacturing PMI fell to 46.2 in September 2025 (from 47.0 in August), a five-month low that underscored deeper contraction as output and new orders dropped more sharply.

-

Output declined for the eleventh straight month, with the fastest contraction since March, spanning consumer, intermediate, and investment goods.

-

New orders fell for the twelfth consecutive month and at one of the steepest rates in two years, weighed down by weak domestic demand, subdued client confidence, US tariff uncertainty, and higher costs.

-

Export orders contracted sharply, among the fastest declines in over two years, with reduced demand from the US, EU, Middle East, and Asia.

-

Employment fell for the eleventh straight month, with job losses across all categories of staff as firms cut costs in response to rising taxes and energy expenses.

-

Inventories of finished goods rose for the first time since January, driven by intermediate goods, while backlogs of work continued to shrink.

-

Supplier delivery times lengthened for the twenty-first month in a row, reflecting port congestion, shipping delays, supplier capacity issues, and shortages.

-

Price pressures eased, with both input cost and output charge inflation slowing to nine-month lows across all major product categories.

-

Business confidence stayed relatively subdued, as weak demand, policy uncertainty, and global trade headwinds weighed on the outlook, despite hopes that lean inventories and new product launches might support a future recovery.

US

The S&P Global US Manufacturing PMI fell to 52.0 in September (from 53.0 in August), indicating a slower pace of expansion amid softer demand and ongoing tariff pressures.

-

New orders rose for a ninth straight month but only modestly, marking growth below the survey average, while export sales declined for a third month in a row due to tariff impacts, particularly with Canada and Mexico.

-

Output expanded for a fourth consecutive month, though at a weaker pace than August, with production exceeding new orders and leading to a buildup of finished goods inventories.

-

Employment rose solidly as firms filled vacancies and expanded labor capacity, contributing to the steepest drop in backlogs in five months.

-

Input costs remained elevated as tariffs pushed vendor prices higher, though the rate of input price inflation eased slightly compared with August.

-

Selling price inflation slowed to an eight-month low, as weaker demand and competitive pressures limited firms’ ability to pass on costs.

-

Supplier delivery times lengthened further in September due to tariff-related delays, reinforcing ongoing supply-side uncertainty.

-

Business confidence improved modestly compared to August, supported by expectations for reshoring and stronger demand, despite concerns about trade policy and federal uncertainty.

-

Global - 9/2/2025

Asia Pacific

- Australia - 8/31/2025

- Malaysia - 9/2/2025

- ASEAN - 9/2/2025

- Myanmar - 9/1/2025

- Philippines - 9/1/2025

- Thailand - 9/1/2025

- Vietnam - 9/1/2025

- Indonesia - 9/1/2025

- Japan - 9/1/2025

- Taiwan - 9/1/2025

- China - 9/1/2025

- India - 9/1/2025

- Russia - 9/1/2025

- Kazakhstan - 9/1/2025

- South Korea - 9/1/2025

- Pakistan - 9/1/2025

Europe

- Austria - 8/27/2025

- Ireland - 9/1/2025

- Netherlands 9/1/2025

- Romania - 9/1/2025

- Turkiye - 9/1/2025

- Poland - 9/1/2025

- Spain - 9/1/2025

- Czechia - 9/1/2025

- Italy - 9/1/2025

- France - 9/1/2025

- Germany - 9/1/2025

- Eurozone - 9/1/2025

- Greece - 9/1/2025

- UK - 9/1/2025

North & South America

Key Results

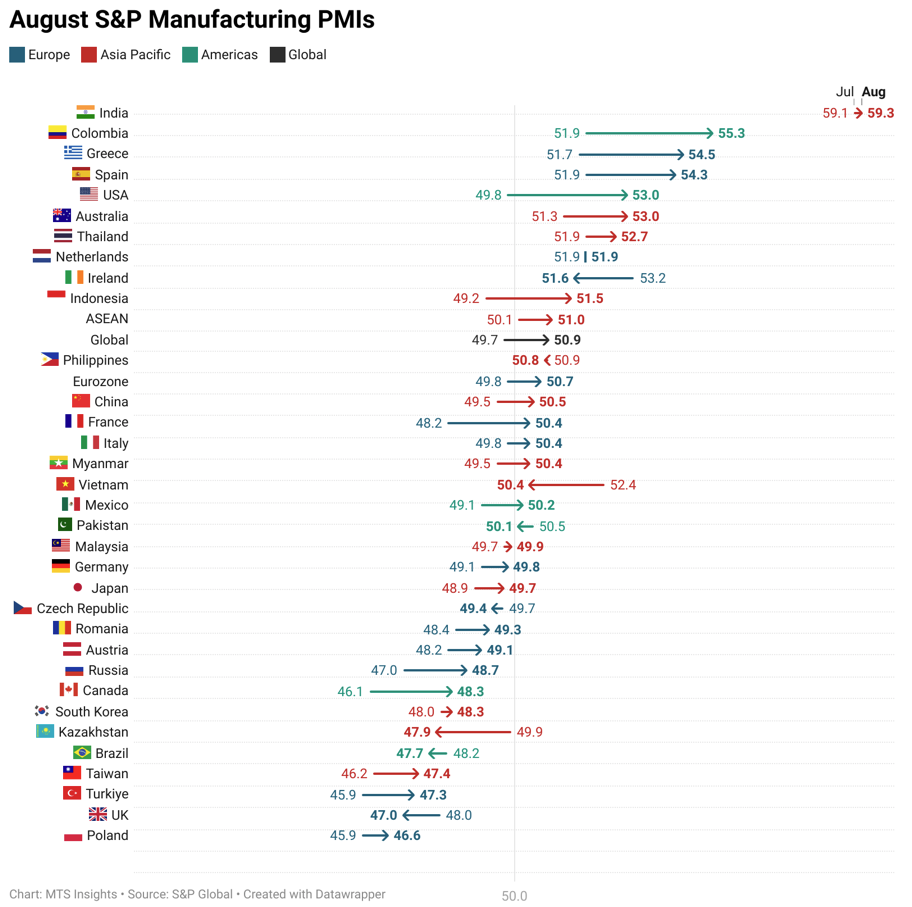

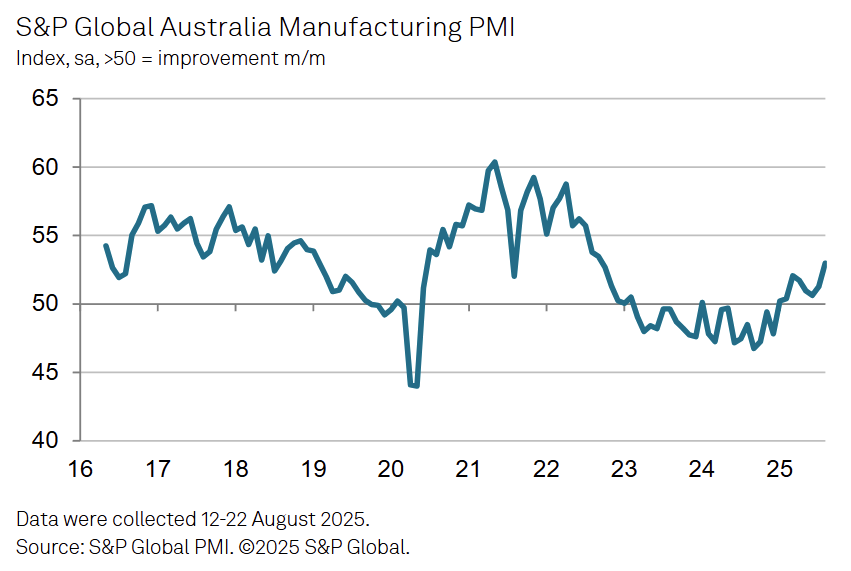

Australia

Australia’s Manufacturing PMI rose to 53.0 in August 2025 (from 51.3 in July), the fastest pace of expansion since September 2022, supported by stronger demand and renewed export growth.

-

Production expanded at the quickest rate since April 2022, driven by a sharp increase in new orders, which rose at the fastest pace in nearly three years.

-

New export orders returned to growth for the first time since May, providing additional support to demand.

-

Employment rose marginally for a sixth straight month, helping firms reduce backlogs of outstanding work.

-

Purchasing activity increased for the first time since April, with stocks of purchases and finished goods both recording their strongest gains since mid-2022.

-

Input and output prices rose modestly, but inflationary pressures remained historically subdued, while business confidence surged to its highest level since early 2022.

China

China’s General Manufacturing PMI rose to 50.5 in August 2025 (from 49.5 in July), the highest in five months, signaling a return to expansion in operating conditions.

-

New orders grew at the quickest pace since March, driving a modest rebound in output after July’s decline.

-

New export orders remained in contraction but eased, while backlogs of work increased at the fastest rate in six months.

-

Purchasing activity and inventories expanded, with raw material and semi-finished goods holdings rising at the strongest pace since November 2020.

-

Employment declined for a fifth straight month, as firms remained cautious on staffing despite stronger workloads.

-

Input costs rose at the steepest pace in nine months, but output prices stabilized, ending an eight-month streak of declines.

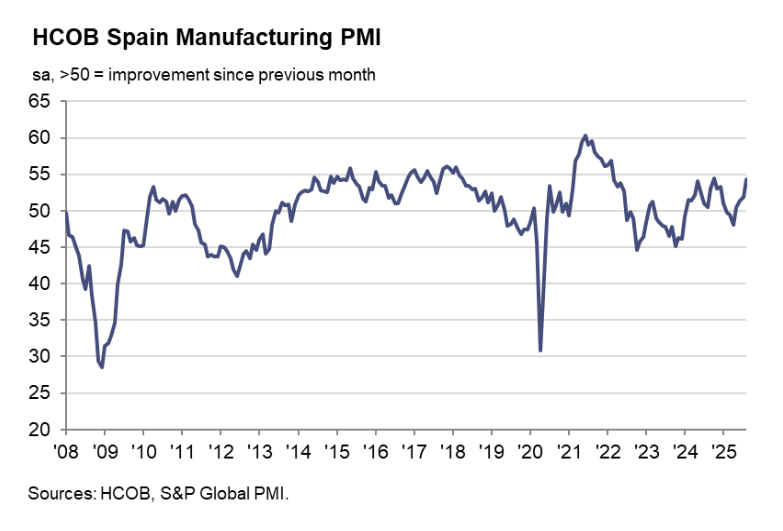

Spain

Spain’s Manufacturing PMI rose to 54.3 in August 2025 (from 51.9 in July), marking the fastest pace of expansion since October 2024 and the fourth straight month of growth.

-

Output and new orders expanded at the sharpest rates since October 2024 and May 2024, supported by stronger domestic demand and marketing campaigns.

-

New export orders grew modestly, the strongest increase so far in 2025, though still limited compared with domestic demand.

-

Backlogs of work rose at the fastest pace in 10 months, prompting firms to raise employment at the quickest rate since December 2024.

-

Input purchases increased marginally after seven months of declines, but vendor performance worsened to the greatest extent this year amid shortages and transport delays.

-

Input and output prices both rose modestly, with inflationary pressures remaining contained despite reaching a five-month high.

Italy

Italy’s Manufacturing PMI rose to 50.4 in August 2025 (from 49.8 in July), moving back into expansion for the first time in nearly 18 months, led by a sharp rebound in output.

-

Production volumes rose at the fastest pace in almost two-and-a-half years, outpacing modest gains in new orders.

-

Total order books increased slightly, the first rise in 18 months, though export sales continued to decline at a sharper rate.

-

Backlogs of work fell at the quickest pace since March, reflecting spare capacity, while employment decreased marginally for a fifth month.

-

Input purchases and inventories dropped, with pre-production stocks declining at the sharpest rate so far in 2025.

-

Input and output prices both edged down modestly, aided by lower energy costs and favorable exchange rate movements.

Germany

Germany’s Manufacturing PMI rose to 49.8 in August 2025 (from 49.1 in July), a 38-month high, though still below the 50 threshold, signaling continued mild contraction despite the strongest output growth in over three years.

-

The Output Index climbed to 52.9 (from 50.6), marking the fastest expansion since March 2022, while new orders rose for a third straight month.

-

Export sales fell for the first time in five months, tempering the overall demand recovery.

-

Employment declined at a quicker pace than in July, with firms reducing contractors and not replacing departing staff.

-

Purchasing activity fell for the first time in three months, with both pre- and post-production inventories contracting at solid rates.

-

Input costs and output prices continued to decline; factory gate charges fell at the steepest pace in six months due to competitive pressures and lower costs.

Eurozone

The Eurozone Manufacturing PMI rose to 50.7 in August 2025 (from 49.8 in July), the first expansion since June 2022, driven by the strongest output growth in over three years and a rebound in new orders.

The Eurozone Manufacturing PMI rose to 50.7 in August 2025 (from 49.8 in July), the first expansion since June 2022, driven by the strongest output growth in over three years and a rebound in new orders.-

The Output Index climbed to 52.5 (from 50.6), marking the sharpest production increase since March 2022.

-

New orders rose for the first time in nearly three-and-a-half years, supported by domestic demand, while export sales declined for a second month.

-

Backlogs of work fell for a 39th straight month, and employment continued to decline, though job losses were marginal and among the softest in over two years.

-

Both pre- and post-production inventories contracted at the quickest pace since March, alongside a renewed fall in purchasing activity.

-

Input costs rose slightly for the first time since March, while output prices fell modestly as firms maintained competitive discounting.

US

The S&P Global US Manufacturing PMI rose to 53.0 in August 2025 (from 49.8 in July), the highest since May 2022, signaling the strongest improvement in operating conditions in over three years.

-

Manufacturing production surged at the steepest pace since May 2022, supported by higher new orders and inventory building.

-

New orders rose for the eighth straight month, driven mainly by domestic demand, while export sales declined marginally for a second month.

-

Finished goods inventories increased at the fastest pace in 13 months as firms stockpiled amid tariff-related cost concerns and potential supply constraints.

-

Input cost inflation accelerated to the second-highest rate in three years, with tariffs overwhelmingly cited as the driver; output charges also rose sharply.

-

Employment expanded solidly as firms added staff to address capacity pressures, with backlogs of work increasing at the fastest rate since September 2022.

-

Supplier delivery times improved slightly despite stronger purchasing activity, while business confidence strengthened on expectations of continued domestic demand and planned investments.

-

Global - 8/1/2025

Asia Pacific

- Australia - 7/31/2025

- Malaysia - 8/1/2025

- ASEAN - 8/1/2025

- Myanmar - 8/1/2025

- Philippines - 8/1/2025

- Thailand - 8/1/2025

- Vietnam - 8/1/2025

- Indonesia - 8/1/2025

- Japan - 8/1/2025

- Taiwan - 8/1/2025

- China - 8/1/2025

- India - 8/1/2025

- Russia - 8/1/2025

- Kazakhstan - 8/1/2025

- South Korea - 8/1/2025

- Pakistan - 8/1/2025

Europe

- Austria - 7/29/2025

- Ireland - 8/1/2025

- Netherlands - 8/1/2025

- Romania - 8/1/2025

- Turkiye - 8/1/2025

- Poland - 8/1/2025

- Spain - 8/1/2025

- Czechia - 8/1/2025

- Italy - 8/1/2025

- France - 8/1/2025

- Germany - 8/1/2025

- Eurozone - 8/1/2025

- Greece - 8/1/2025

- UK - 8/1/2025

North & South America

Key Results

ASEAN

The S&P ASEAN Manufacturing PMI rose to 50.1 in July from 48.6 in June, indicating the first expansion in output since March and signaling a modest improvement in operating conditions.

- Output rose at a solid pace, marking the end of a three-month decline, while new orders fell only marginally—suggesting easing demand weakness.

- Employment continued to decline, but the pace of job losses slowed; purchasing activity stabilized after three months of cuts.

- Input costs and output prices rose at the fastest pace in four and five months, respectively, though still below long-run averages.

- Business confidence fell to a five-year low, with firms expecting only modest growth in output over the next year.

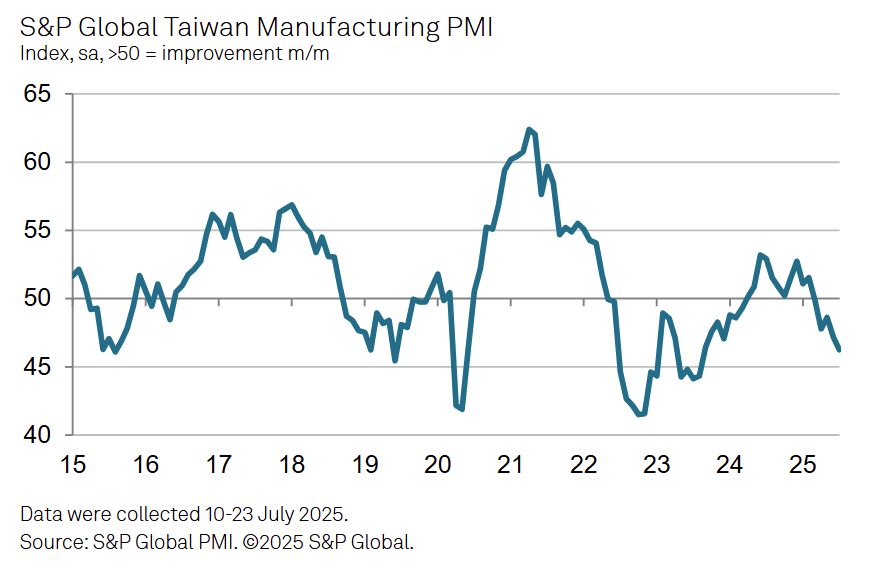

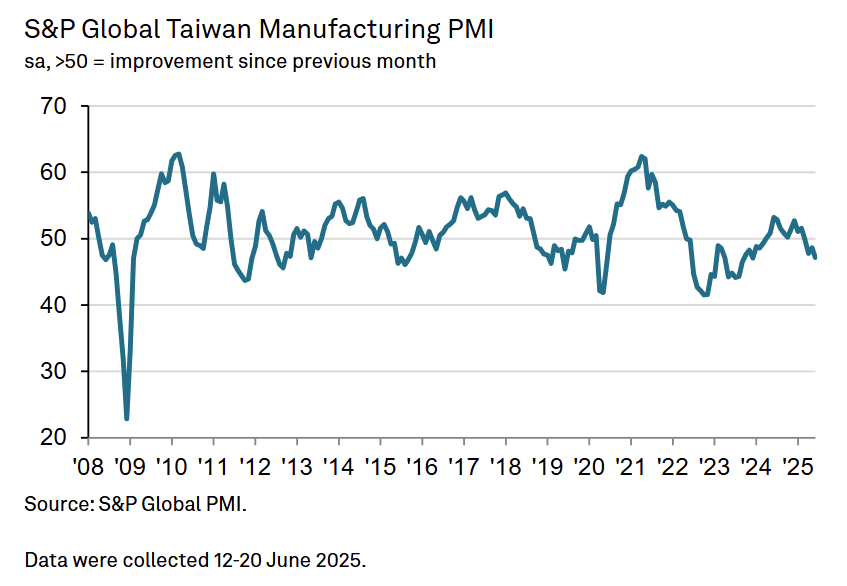

Taiwan

The S&P Taiwan Manufacturing PMI fell to 46.2 in July (from 47.2 in June), marking the steepest deterioration in operating conditions since August 2023 and the fifth consecutive month in contraction.

- Output, new orders, and export sales all declined at their fastest rates in nearly two years due to weak demand and uncertainty over US trade tariffs.

- Purchasing activity dropped at the sharpest pace since August 2023, while employment continued to fall amid hiring freezes and attrition.

- Input costs rose modestly on higher raw material prices (notably metals), but output prices declined slightly due to competitive pressure.

- Business sentiment slipped to its lowest level in two and a half years, reflecting subdued forecasts for year-ahead production.

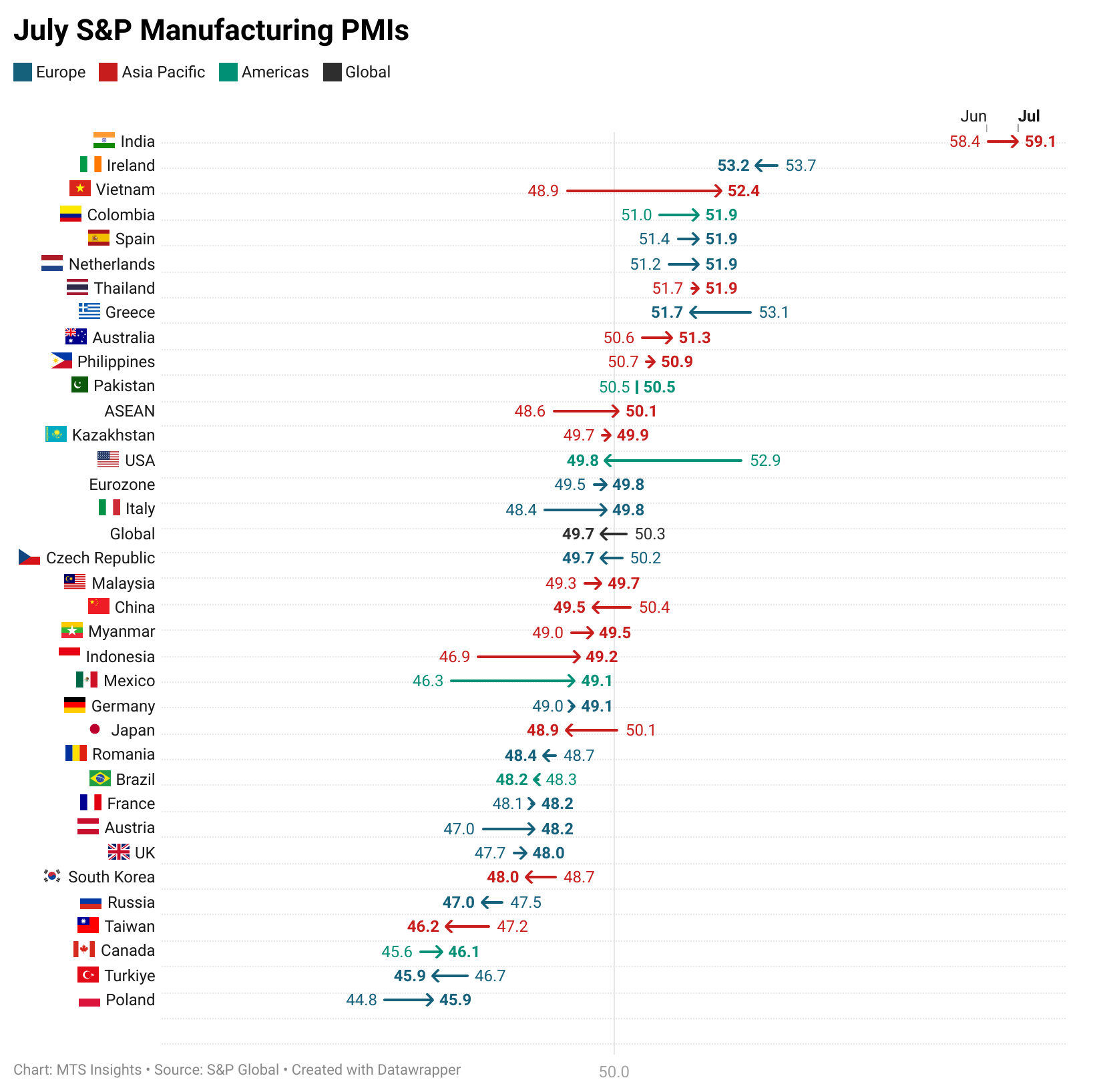

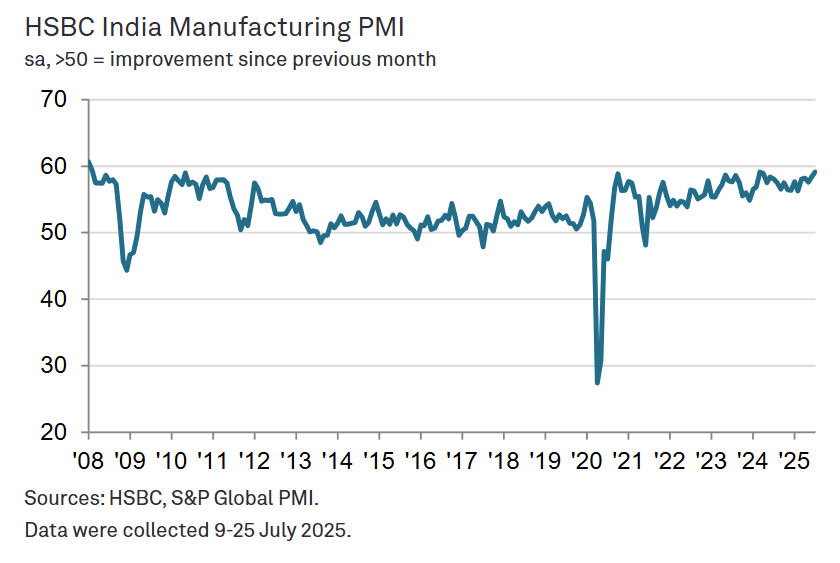

India

The HSBC India Manufacturing PMI rose to 59.1 in July (from 58.4 in June), marking a 16-month high and signaling the strongest improvement in sector conditions since March 2024.

- New orders expanded at the fastest pace in nearly five years, while output growth reached a 15-month high, driven by intermediate goods producers.

- Export growth remained strong, though slightly below June’s pace; inventories of inputs rose at the fastest rate in 15 months.

- Employment growth slowed to the weakest since November 2024 as most firms reported adequate staffing.

- Input costs rose at a faster rate due to higher raw material prices (aluminum, rubber, steel), and output prices rose above trend levels due to strong demand.

- Business confidence fell to a three-year low amid concerns over inflation and competitive pressures.

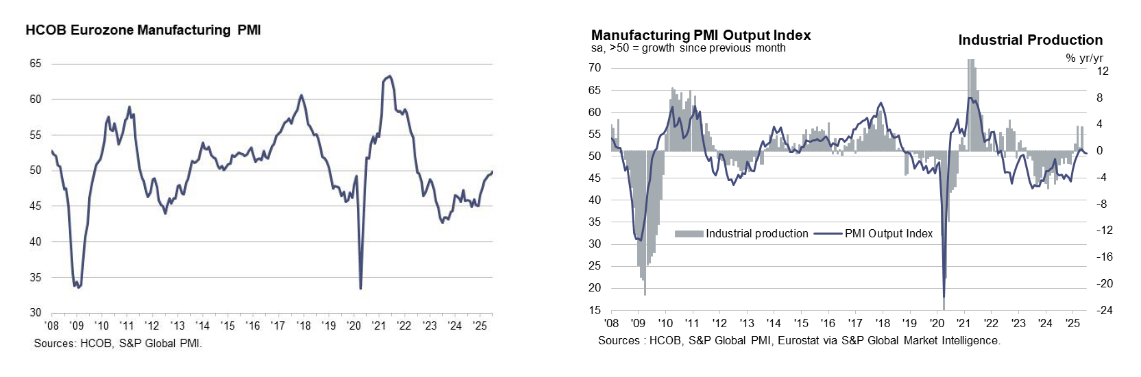

Eurozone

The HCOB Eurozone Manufacturing PMI rose to 49.8 in July (from 49.5 in June), a 36-month high that signals near-stabilization in factory conditions, though still just below the 50.0 expansion threshold.

- Output rose for a fifth consecutive month but slowed to a four-month low (50.6) as new orders fell again, particularly from foreign clients.

- Input costs and output prices were broadly unchanged after recent declines, indicating muted price pressures.

- Employment and purchasing activity declined at the slowest pace in nearly two years, showing signs of stabilizing.

- Supply chain pressures ticked up, with input lead times lengthening to the greatest extent since November 2022.

- Business confidence dipped slightly from June but remained above the long-run average, supported by smaller economies like Spain, the Netherlands, and Ireland.

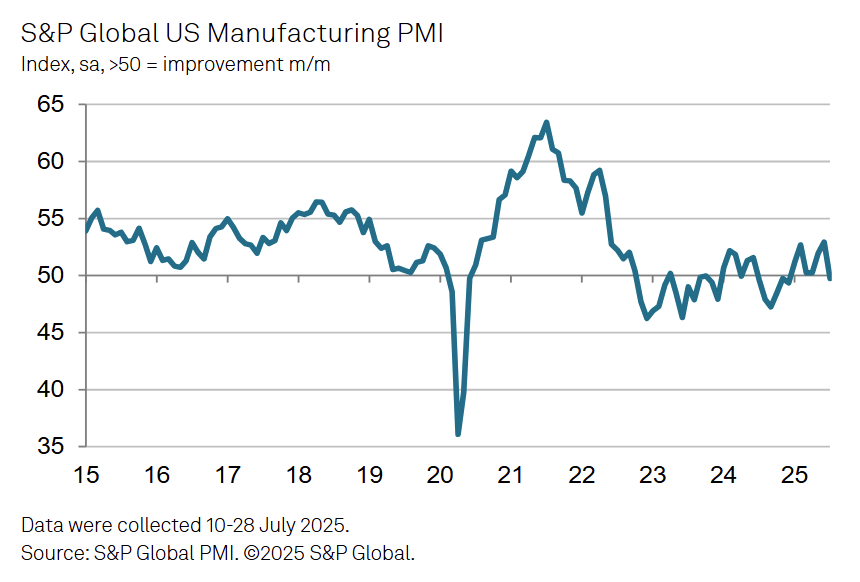

US

The S&P Global US Manufacturing PMI fell to 49.8 in July (from 52.9 in June), the first sub-50 reading of 2025 and a signal that operating conditions worsened slightly amid soft demand and tariff-related uncertainty.

- New orders were broadly flat, with export orders falling for the first time in three months amid weaker demand from China, the EU, and Japan.

- Employment declined modestly for the first time since April as firms cited cost concerns and excess capacity.

- Input costs remained elevated due to tariffs, but inflation eased from June’s near three-year high; selling prices still rose at the second-fastest pace since Nov 2022.

- Inventories were drawn down for the first time in three months as firms slowed purchasing and relied on existing stockpiles.

- Supplier delivery times improved significantly, marking the best performance in over a year as supply constraints eased.

-

Global - 7/1/2025

Asia Pacific

- Australia - 6/30/2025

- Malaysia - 7/1/2025

- ASEAN - 7/1/2025

- Myanmar - 7/1/2025

- Philippines - 7/1/2025

- Thailand - 7/1/2025

- Vietnam - 7/1/2025

- Indonesia - 7/1/2025

- Japan - 7/1/2025

- Taiwan - 7/1/2025

- China - 7/1/2025

- India - 7/1/2025

- Russia - 7/1/2025

- Kazakhstan - 7/1/2025

- South Korea - 7/1/2025

- Pakistan - 7/1/2025

Europe

- Austria - 6/26/2025

- Ireland - 7/1/2025

- Netherlands - 7/1/2025

- Romania - 7/1/2025

- Turkiye - 7/1/2025

- Poland - 7/1/2025

- Spain - 7/1/2025

- Czechia - 7/1/2025

- Italy - 7/1/2025

- France - 7/1/2025

- Germany - 7/1/2025

- Eurozone - 7/1/2025

- Greece - 7/1/2025

- UK - 7/1/2025

North & South America

Key Results

ASEAN

The S&P Global ASEAN Manufacturing PMI fell 0.6 pts to 48.6 in June, the lowest reading since August 2021, signaling the sharpest deterioration in operating conditions in nearly four years.

- New orders declined at the fastest pace since August 2021, with export demand weakening further for the eighth consecutive month.

- Employment dropped at the steepest rate in 44 months, while input purchasing also saw a deeper contraction.

- Output contracted for a third month, though the rate of decline remained marginal and consistent with May.

- Input price inflation eased to its lowest in over five years, while output prices rose only modestly.

- Business confidence softened to the second-lowest level since July 2020, pointing to a muted outlook for future output.

Taiwan

The S&P Taiwan Manufacturing PMI dropped 1.4 pts to 47.2 in June, marking the sharpest deterioration in factory activity in 18 months amid deepening declines in output and new orders.

- Output fell at the fastest pace since December 2023, while new orders and new export work posted their steepest drops since August 2023.

- Employment declined again as firms cut staff and purchasing in response to weaker demand and tariff-related uncertainty.

- Supplier delivery times lengthened at the fastest rate this year, while input costs rose modestly after falling in May.

- Factory gate prices were reduced for the fourth straight month despite rising input costs, reflecting efforts to support sales.

- Business confidence remained subdued for the third consecutive month, with many firms expecting output to decline over the coming year.

China

The Caixin China Manufacturing PMI rose 2.1 pts to 50.4 in June, returning to expansion territory and signaling the eighth improvement in nine months, as output and new orders rebounded modestly.

- Output expanded at the fastest rate since November 2024, supported by stronger domestic demand and promotional efforts.

- New orders rose slightly, but new export orders fell for a third consecutive month, weighed down by weak global demand and U.S. tariffs.

- Employment declined for the ninth time in ten months, with workforce reductions leading to a marginal increase in backlogs.

- Input costs fell for the fourth straight month, but output prices dropped at the fastest pace in five months amid fierce competition.

- Business confidence softened from May and remained below average, with firms cautious due to weak external demand and policy uncertainty.

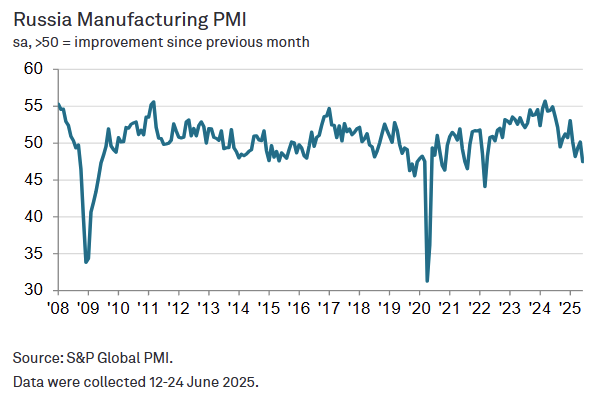

Russia

The S&P Russia Manufacturing PMI fell -2.7 pts to 47.5 in June, the third straight decline in the last four months and the steepest drop since March 2022.

- New export orders contracted by the sharpest rate since November 2022.

- The fall in staffing levels was the second in the last three months, with the pace of job shedding the sharpest since April 2022.

- The level of optimism was stronger than the series average, but ticked down to the lowest since October 2022 amid concerns regarding global economic uncertainty.

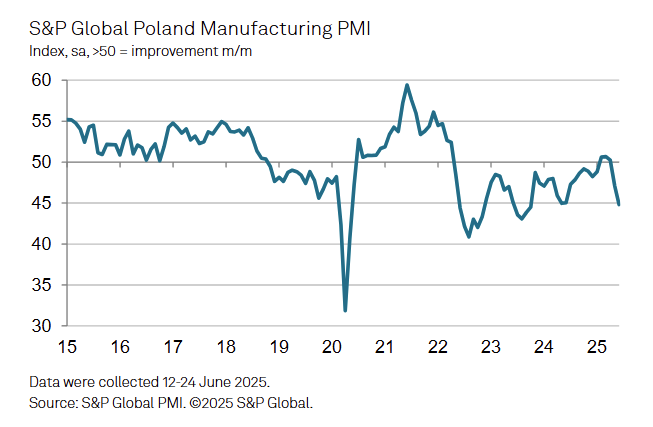

Poland

The S&P Poland Manufacturing PMI dropped -2.3 pts to 44.8 in June, the sharpest deterioration in the Polish manufacturing sector since October 2023.

- The headline figure has fallen by -5.4 pts since April, the steepest two-month drop since mid-2022.

- New orders contracted at the strongest rate since October 2023 with new export orders contracting at the strongest rate since November 2022.

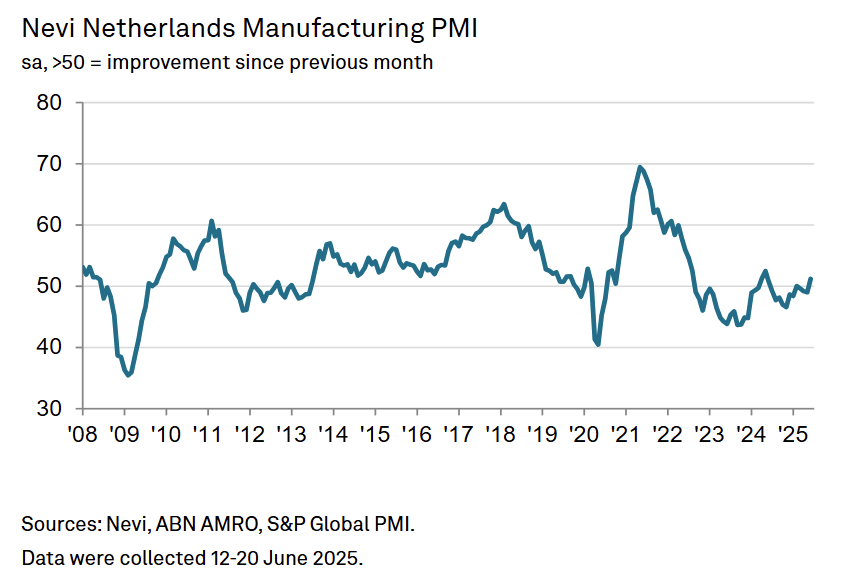

Netherlands

The S&P Netherlands Manufacturing PMI increased 2.2 pts to 51.2 in June, the first time conditions have improved in a year.

- New export orders expanded for the first time since May 2024.

- Employment across the manufacturing industry rose for the first time in nearly a year, albeit modestly.

- Average input cost inflation continued to soften in June, with the latest uptick in expenses the least pronounced in seven months.

Germany

The S&P Germany Manufacturing PMI increased 0.7 pts to 49.0 in June, the highest in 34 months.

- The New Orders index was in expansionary territory for the third time in four months, and growth was the strongest since March 2022.

- Goods producers' purchases of raw materials and other inputs meanwhile rose for the first time in three years as expectations towards future output improved.

- June's survey indicated a slight improvement in manufacturers' growth expectations for the coming year. Confidence was the highest since February 2022, reflecting the plans for increased public sector spending and hopes of a wider economic upturn.

Eurozone

The S&P Eurozone Manufacturing PMI edged up 0.1 pts to 49.5 in June, the highest in 34 months, signaling a marginal downturn but hinting at growing stabilization across the sector.

- Output Index slowed -0.5 pts to 50.8, still in expansion but at a 3-month low, supported by stable order books and backlog clearing.

- New orders and export sales stabilized, ending a 37-month streak of declining demand.

- Confidence rose to its highest level since February 2022, though job shedding and reduced input buying continued.

- Delivery times lengthened for the first time since January, while purchasing costs and output prices declined for a third straight month.

- National divergence persists: Greece, Ireland, Spain, and the Netherlands saw improvement, while France, Italy, Austria, and Germany remained in contraction.

UK

The S&P UK Manufacturing PMI increased 1.3 pts to 47.7 in June, unchanged from the flash estimate and up slightly from prior months, marking the highest reading in five months but still indicating contraction in the sector.

- Output, new orders, and employment all declined for another month but at slower rates, with optimism rising to a 4-month high.

-

Global - 6/3/2025

Asia Pacific

- Australia - 6/1/2025

- Malaysia - 6/3/2025

- ASEAN - 6/4/2025

- Myanmar - 6/2/2025

- Philippines - 6/2/2025

- Thailand - 6/4/2025

- Vietnam - 6/2/2025

- Indonesia - 6/2/2025

- Japan - 6/2/2025

- Taiwan - 6/2/2025

- China - 6/3/2025

- India - 6/2/2025

- Russia - 6/2/2025

- Kazakhstan - 6/2/2025

- South Korea - 6/2/2025

- Pakistan - 6/2/2025

Europe

- Austria - 5/27/2025

- Ireland - 6/3/2025

- Netherlands - 6/2/2025

- Romania - 6/2/2025

- Turkiye - 6/2/2025

- Poland - 6/2/2025

- Spain - 6/2/2025

- Czechia - 6/2/2025

- Italy - 6/2/2025

- France - 6/2/2025

- Germany - 6/2/2025

- Eurozone - 6/2/2025

- Greece - 6/2/2025

- UK - 6/2/2025

North & South America

Key Results

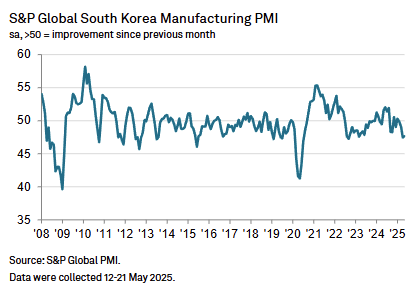

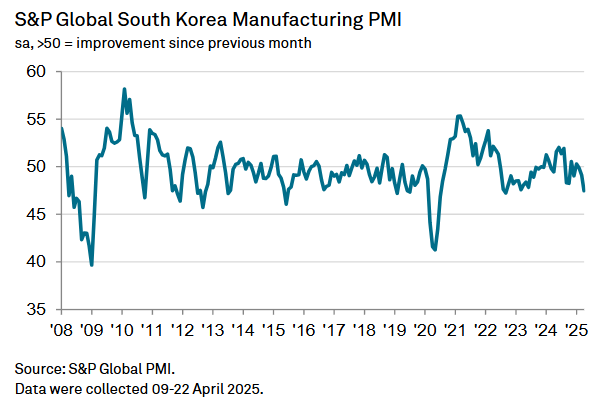

South Korea

South Korea’s S&P Manufacturing PMI remained weak in May, improving only 0.2 pts to 47.5.

- While the headline index saw a slight improvement, the decline in new orders fell to the steepest since June 2020, and output declined at the sharpest rate in 31 months.

- Despite that, employment was the strongest since September 2023, and confidence improved on hopes that trade tensions would be resolved.

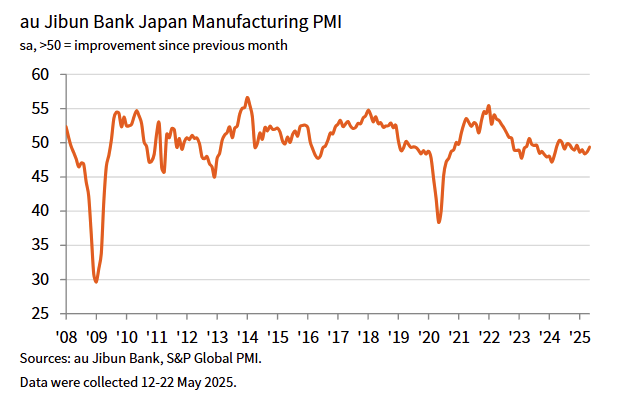

Japan

Japanese manufacturing conditions improved to the best so far in 2025 as its S&P Manufacturing PMI increased 0.7 pts to 49.4 in May, ahead of expectations of a smaller rise to 49.0.

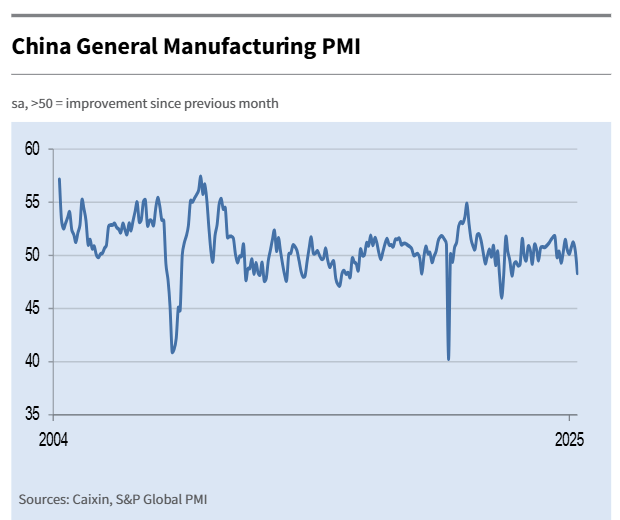

China

China’s S&P Manufacturing PMI fell -2.1 pts to 50.4 in May, the lowest since September 2022 and the first contraction since September 2024.

- Manufacturing output fell for the first time in 19 months as new orders contracted at the sharpest pace in about 2.5 years.

- Average input costs and output charges continued to decline midway through the second quarter of 2025.

- Despite weak conditions, sentiment became more optimistic on hopes that trade conditions would improve

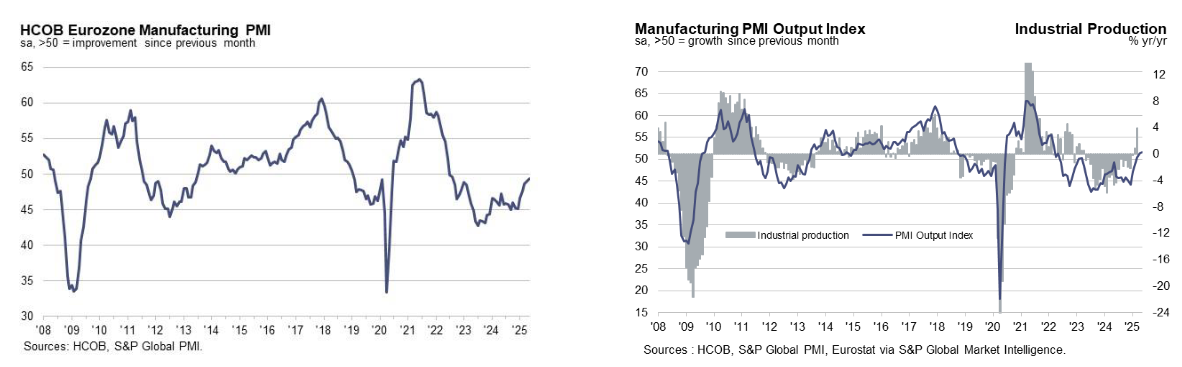

Eurozone

The S&P Eurozone Manufacturing PMI reached its highest in 33 months in May, up 0.4 pts to 49.4.

- France and Austria were the major drivers of the new high as their PMIs increased to 28-month and 32-month highs, respectively.

- Output growth (though it was only slight) was the joint-fastest since March 2022.

- Despite that, backlogs fell at the weakest rate since June 2022, and employment still declined (but at the weakest rate since September 2023).

- The level of positive sentiment rose to its highest since February 2022 and was above its long-term average.

US

The S&P US Manufacturing PMI increased 1.8 pts to 52.0 in May, mostly in line with expectations and the best since February.

- The outlook improved to a 3-month high on hopes that trade policy would stabilize.

- Growth was driven partly by a record increase in input inventories. New order growth was low, but still the strongest in the last three months.

- Raw material price inflation remained high and drove selling price inflation to the highest since November 2022.

-

Global - 5/1/2025

Asia Pacific

- Australia - 4/30/2025

- Malaysia - 5/2/2025

- ASEAN - 5/5/2025

- Myanmar - 5/2/2025

- Philippines - 5/2/2025

- Thailand - 5/2/2025

- Vietnam - 5/5/2025

- Indonesia - 5/2/2025

- Japan - 5/1/2025

- Taiwan - 5/2/2025

- China - 4/30/2025

- India - 5/2/2025

- Russia - 5/5/2025

- Kazakhstan - 5/2/2025

- South Korea - 5/2/2025

- Pakistan - 5/2/2025

Europe

- Austria - 4/28/2025

- Ireland - 5/1/2025

- Netherlands - 5/2/2025

- Romania - 5/2/2025

- Turkiye - 5/2/2025

- Poland - 5/2/2025

- Spain - 5/2/2025

- Czechia - 5/2/2025

- Italy - 5/2/2025

- France - 5/2/2025

- Germany - 5/2/2025

- Eurozone - 5/2/2025

- Greece - 5/2/2025

- UK - 5/1/2025

North & South America

Key Results

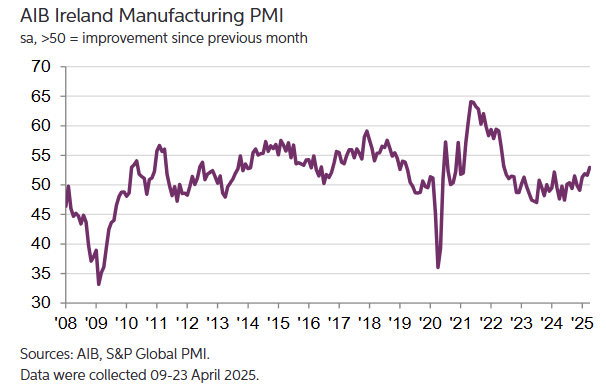

Ireland

Ireland's S&P Manufacturing PMI jumped 1.4 pts to 53 as manufacturing output increased at the strongest pace in almost three years.

China

China’s Manufacturing PMI fell -0.8 pts to 50.4, the lowest since January.

- New export orders declined for the first time in three months as a result of higher US tariffs causing overall order growth to be the weakest in 7 months.

- Business confidence slipped to the third-lowest since this series began in April 2012 due to trade uncertainty.

South Korea

South Korea’s S&P Manufacturing PMI fell -1.6 pts to 47.5 in April, the lowest since September 2022.

- Sharpest falls in output and new orders since mid-2023.

- Employment decreases at sharpest rate since September 2020.

- Business sentiment among weakest in series history.

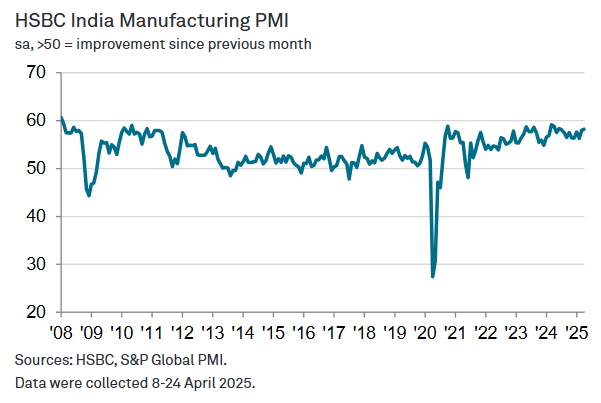

India

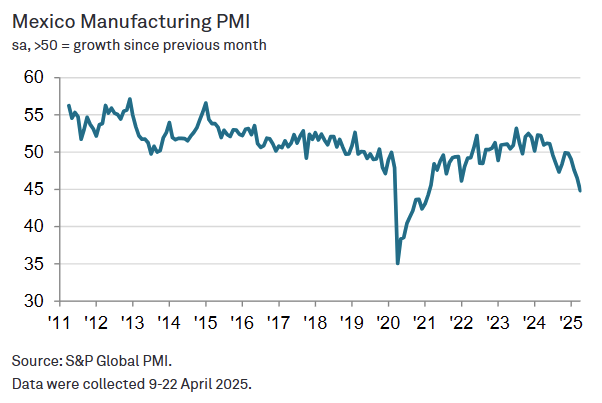

India’s manufacturing sector remained strong in April with a PMI reading of 58.2. Notably, foreign demand increased at the strongest rate in over 14 years. This intensified selling price inflation to the highest since October 2013.

ASEAN

The S&P ASEAN Manufacturing PMI fell -2.1 pts to 48.7 in April, the first deterioration in the manufacturing sector in 16 months and the lowest reading since August 2021.

- The declines in new orders and production were the worst in 44 months.

- Business confidence was the lowest since July 2020.

Euro Area

The Eurozone Manufacturing PMI increased 0.4 pts to 49.0 in April, a 32-month high, with the output index up 1.0 pt to 51.5, a 37-month high.

- Demand growth was close to flat on the month as the New Orders Index increased to a three-year high just below the 50.0 threshold.

- The drop in new orders from non-domestic customers was its shallowest since April 2022.

- The PMI was supported by weaker declines in France and Germany where their indexes were at 27-month and 32-month highs, respectively, but both still below 50.0.

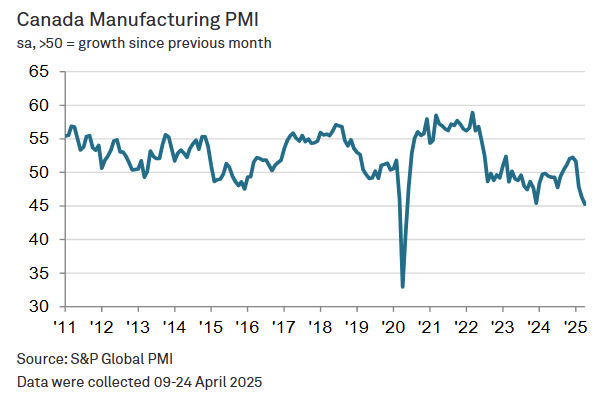

Canada