Paychex Small Business Employment Watch

Paychex Small Business Employment Watch

- Source

- Paychex

- Source Link

- https://www.paychex.com/

- Frequency

-

Monthly

the 2nd Tues following the Thurs between the 17th and 23rd of the reference month, prior to the monthly BLS report.

- Next Release(s)

- May 5th, 2026 8:30 AM

-

June 2nd, 2026 8:30 AM

-

June 30th, 2026 8:30 AM

-

August 4th, 2026 8:30 AM

-

September 1st, 2026 8:30 AM

-

September 29th, 2026 9:00 AM

-

November 3rd, 2026 8:30 AM

-

December 1st, 2026 8:30 AM

-

January 5th, 2027 8:30 AM

Latest Updates

-

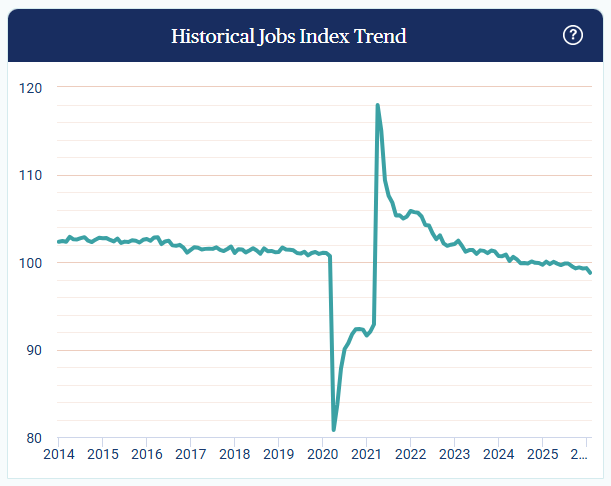

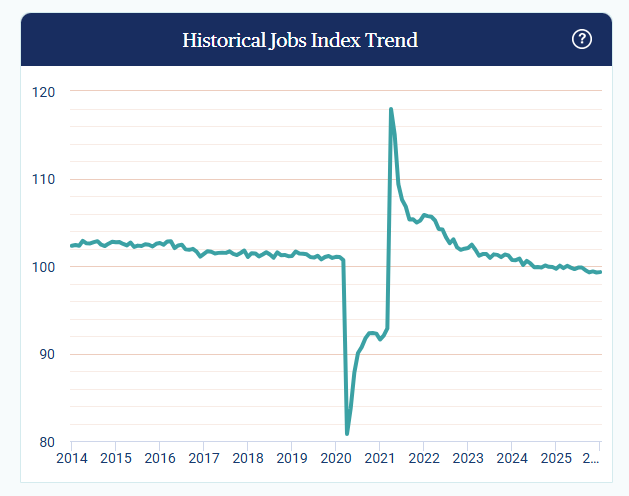

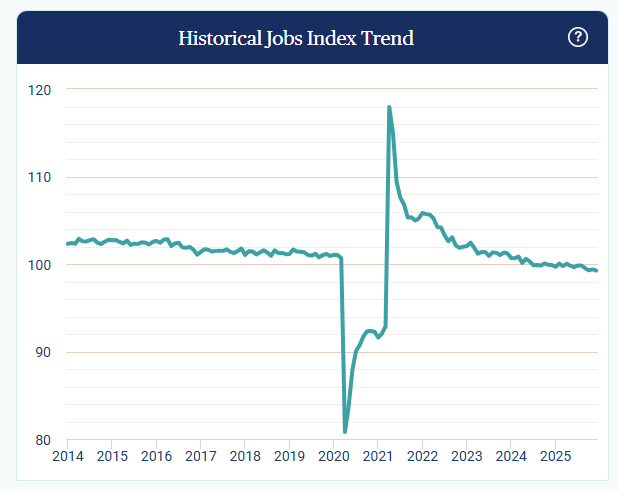

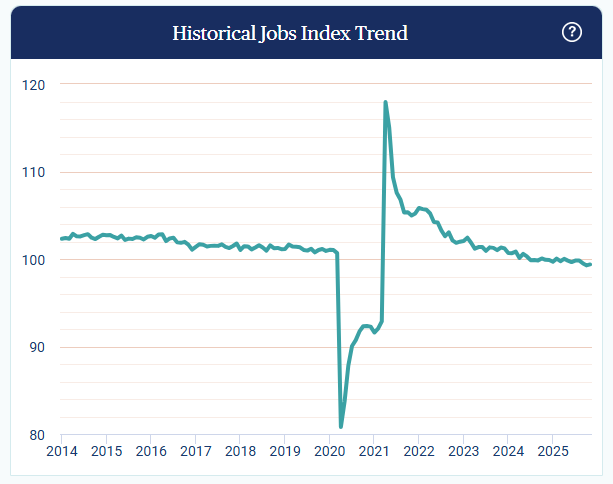

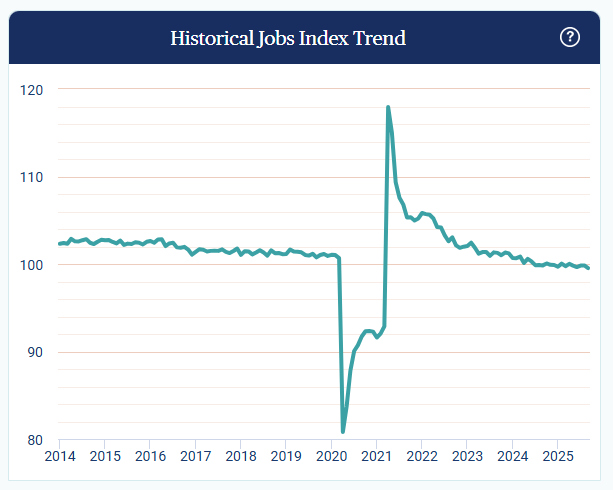

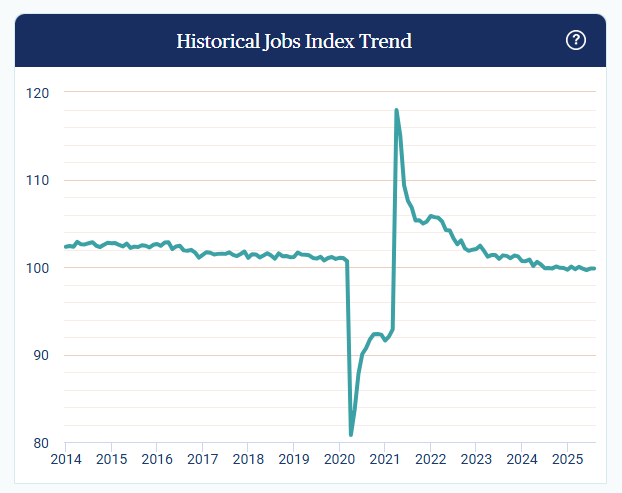

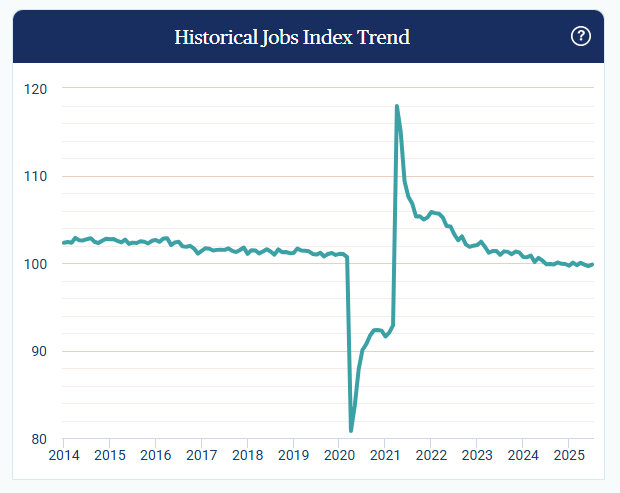

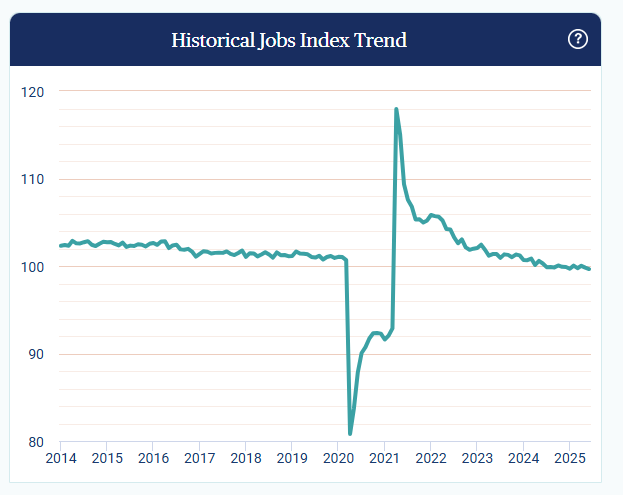

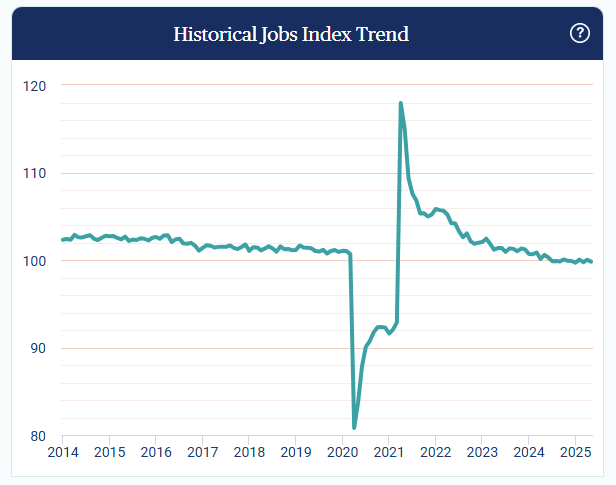

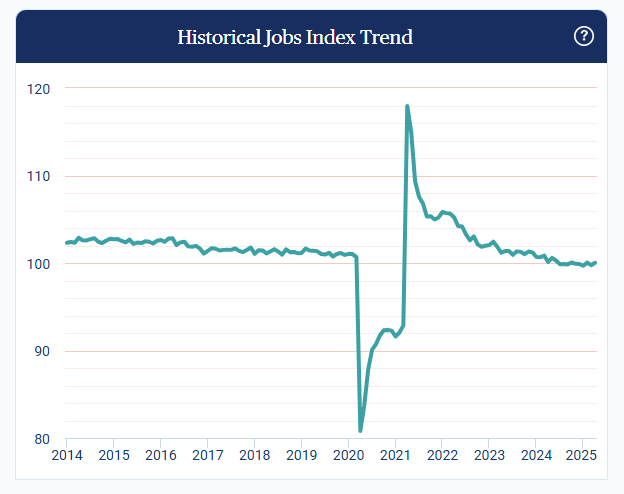

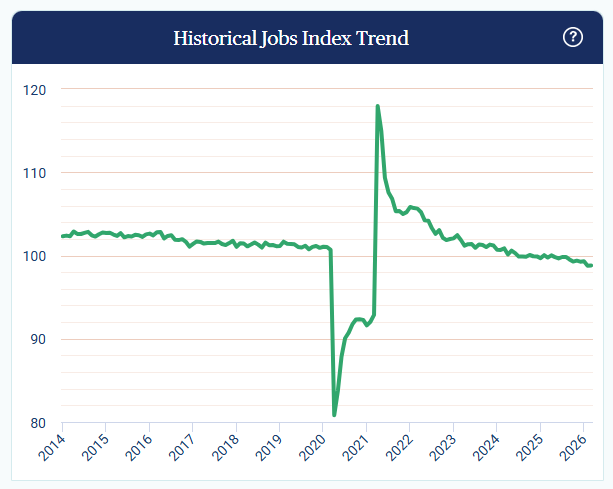

The Paychex Small Business Jobs Index edged up +0.04 pts MoM to 98.81 in March 2026 but remained -0.94 pts YoY lower, indicating stable but subdued small business hiring below the 100 baseline.

-

The national index rose slightly to 98.81 (+0.04 pts MoM), showing marginal stabilization in employment growth, though still below the neutral 100 level that signals expansion.

-

On a YoY basis, the index declined from 99.75 to 98.81 (-0.94 pts YoY), indicating a slower pace of small business job growth compared to March 2025.

-

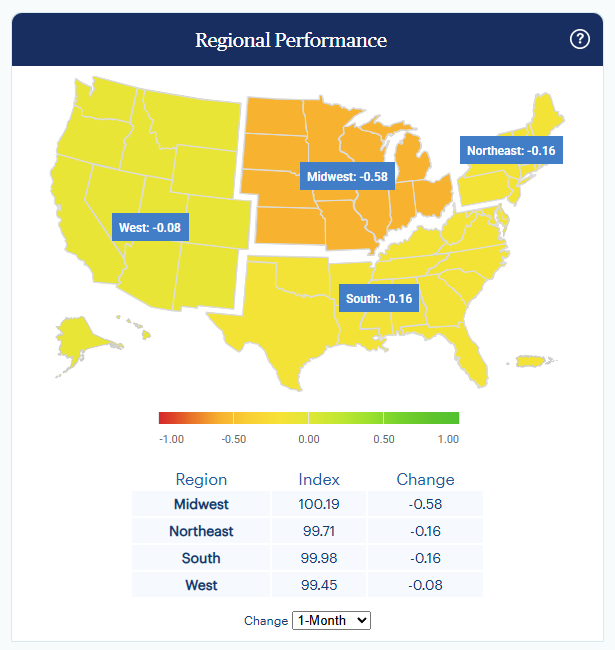

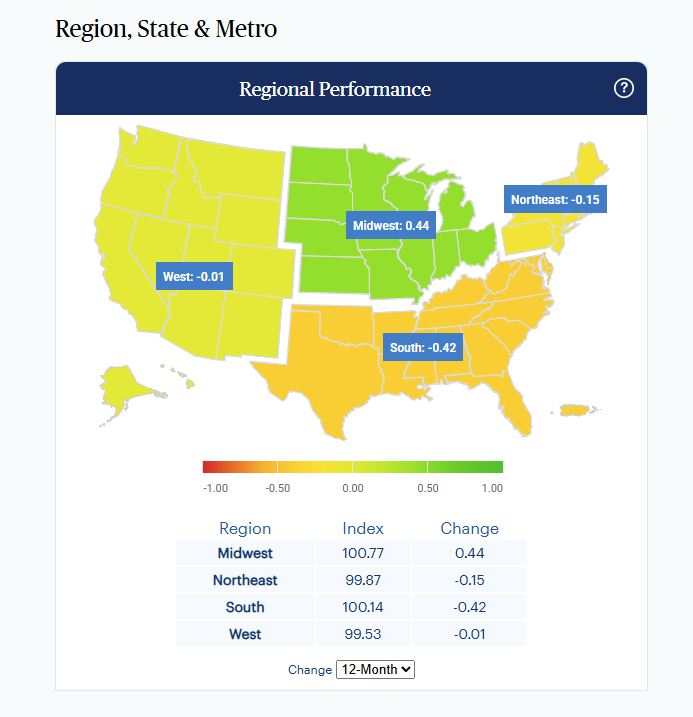

The Midwest remained the top-performing region for the 22nd consecutive month, rising +0.24 pts MoM to 99.52, continuing to lead despite remaining just below 100.

-

The West remained the weakest region at 98.05 (-0.11 pts MoM; -1.47 pts YoY), highlighting persistent underperformance relative to other regions.

-

At the state level, Wisconsin increased +0.93 pts to 100.42, ranking first and moving above the 100 threshold, while Washington fell to 96.58, the lowest among states, with a -3.26 pt decline over the past quarter.

-

California posted a reading of 97.89 and has remained below 100 for two years, indicating sustained YoY job losses in small business employment.

-

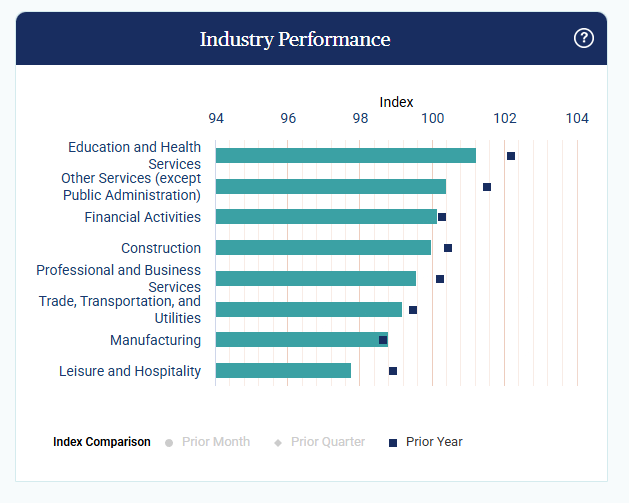

Education and Health Services rose +0.32 pts to move back above 100, maintaining its position as a relatively stronger sector after briefly dipping below the expansion threshold.

-

Financial Activities declined -0.86 pts to 99.04, its lowest level in five years, while Leisure and Hospitality remained the weakest sector at 97.86 despite being the only sector to improve YoY, indicating continued sectoral divergence.

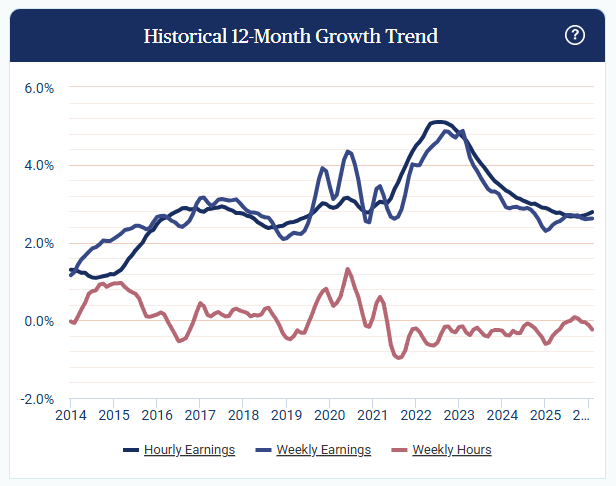

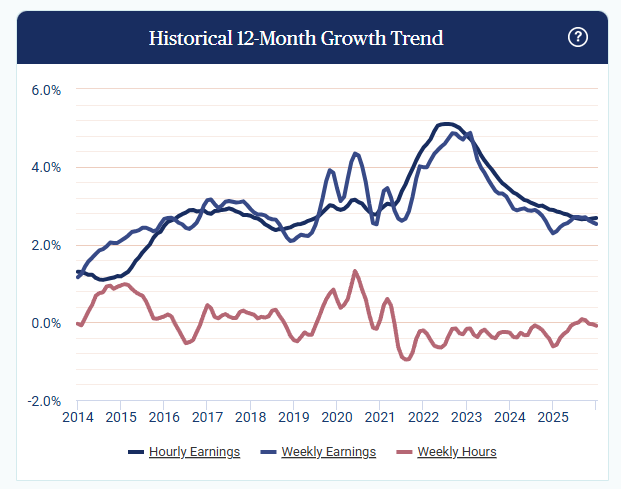

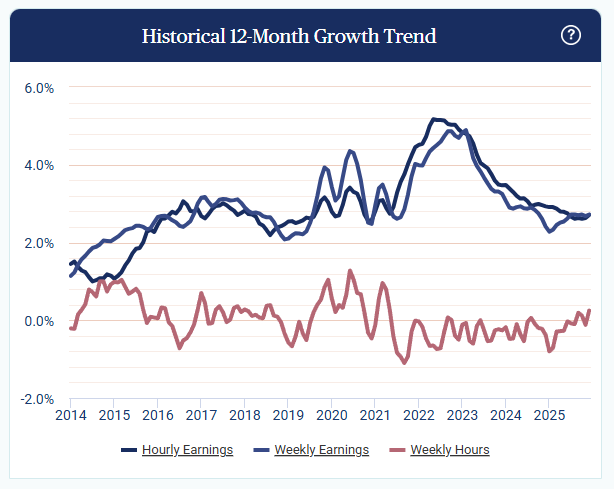

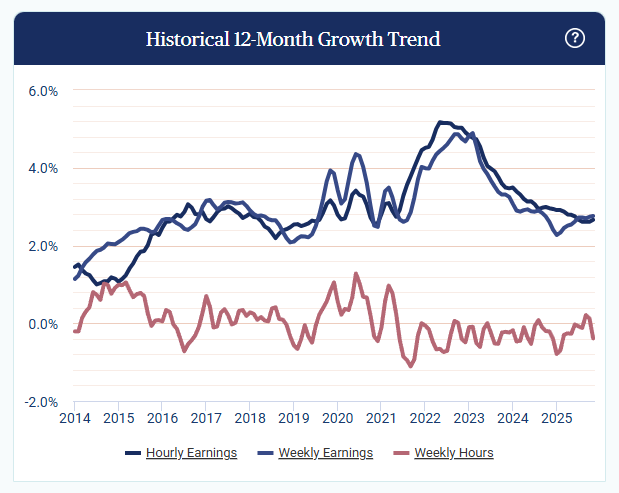

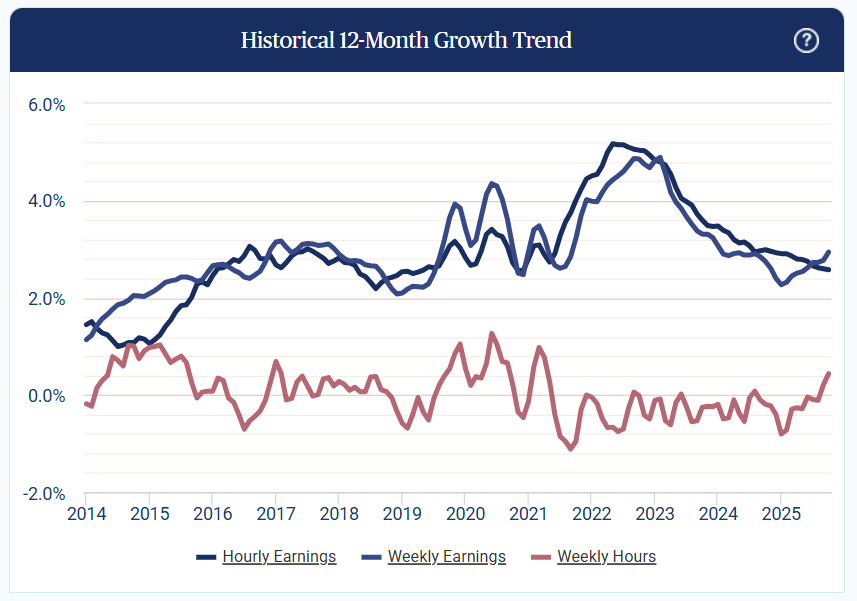

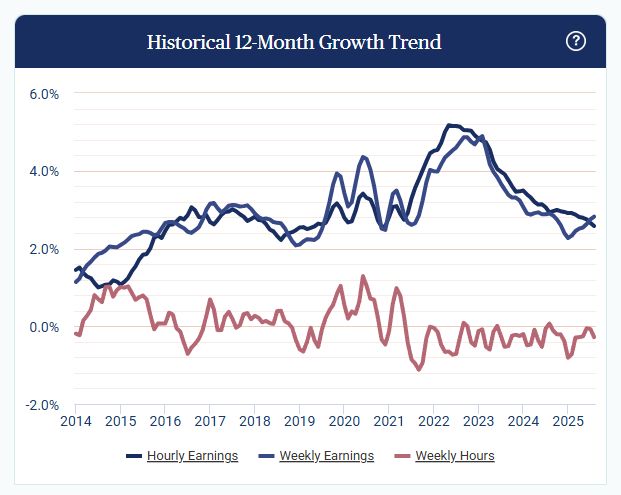

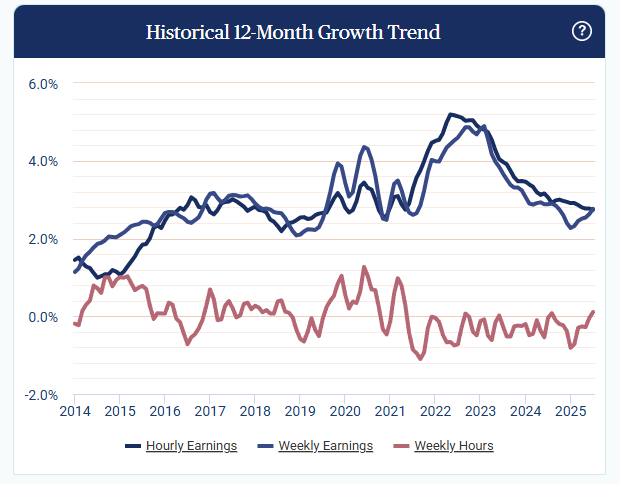

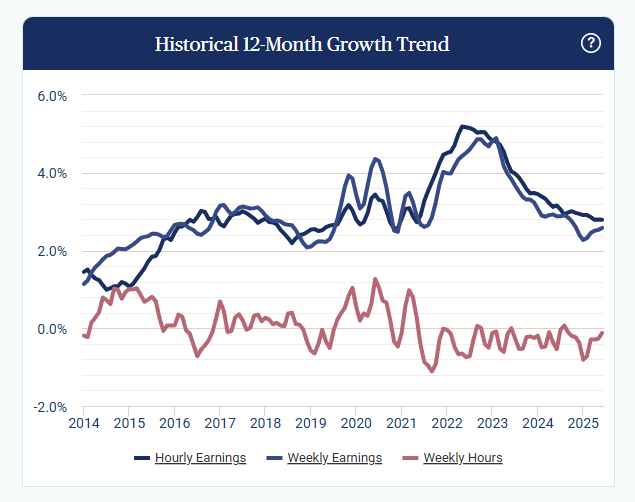

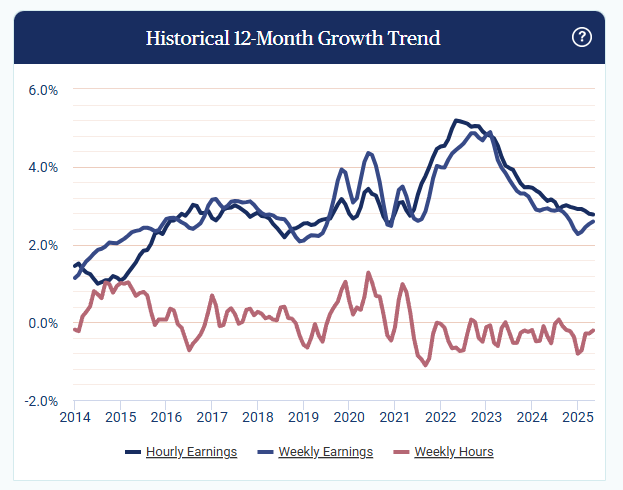

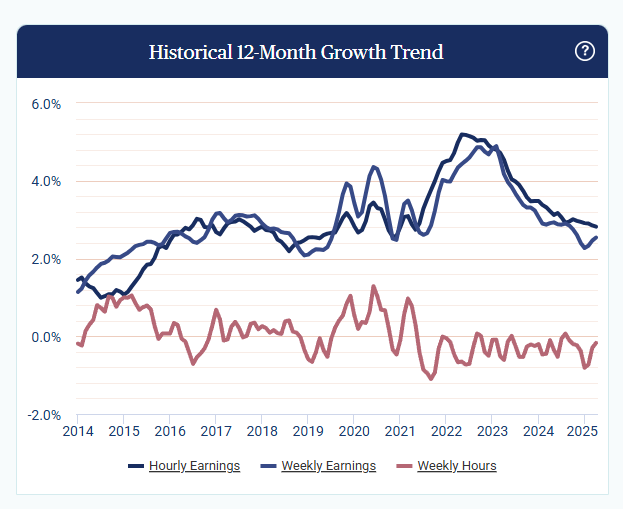

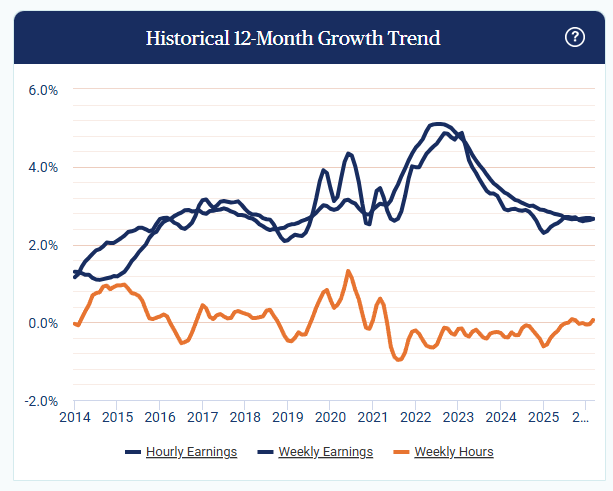

Hourly earnings growth held at +2.66% YoY in March while weekly earnings rose +2.63% YoY and weekly hours worked increased +0.06% YoY, reflecting steady wage gains alongside modest improvement in labor utilization.

-

Hourly earnings growth remained at +2.66% YoY in March, staying below 3% for the 17th consecutive month, indicating a prolonged period of moderate wage growth.

-

Weekly earnings growth edged up to +2.63% YoY, while one-month annualized growth accelerated to +3.84%, matching a three-year high and pointing to a near-term pickup in earnings momentum.

-

Weekly hours worked increased +0.06% YoY, marking only the third positive reading since April 2021, suggesting a tentative improvement in labor utilization after a long period of contraction.

-

Regionally, the Northeast led hourly earnings growth at +3.02% YoY for the first time since June 2021, while the South lagged at +2.45% YoY for the tenth consecutive month, highlighting persistent regional divergence.

-

The West (+0.29% YoY) and South (+0.27% YoY) recorded the strongest gains in weekly hours worked, indicating relatively firmer labor utilization trends in those regions.

-

At the state level, Indiana led with +4.36% YoY hourly earnings growth and +4.43% YoY weekly earnings growth, followed by Tennessee (+4.17% and +3.99%), showing concentrated strength in select states.

-

Virginia posted the weakest hourly earnings growth at +1.85% YoY, while Georgia slowed to +1.89% YoY, its lowest since March 2019, indicating softness in certain regional labor markets.

-

By sector, Other Services led hourly earnings growth at +3.26% YoY, while Education and Health Services lagged at +2.20% YoY, and Construction recorded the strongest weekly hours worked growth at +0.39% YoY, reflecting sector-specific variation in wage and hours trends.

-