NRA Restaurant Performance Index

NRA Restaurant Performance Index

- Source

- National Restaurant Association

- Source Link

- https://restaurant.org/

- Frequency

-

Monthly

Last business day of month

- Next Release(s)

- April 30th, 2026 9:00 AM

Latest Updates

-

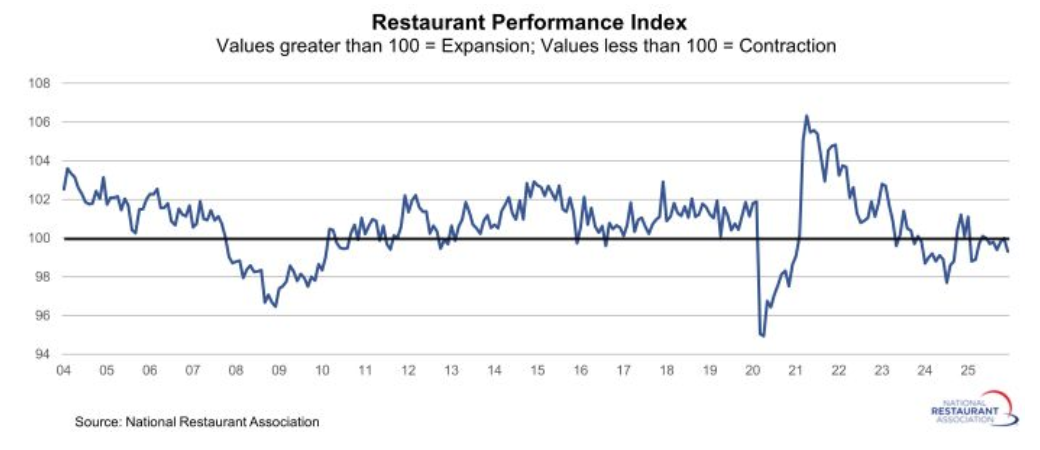

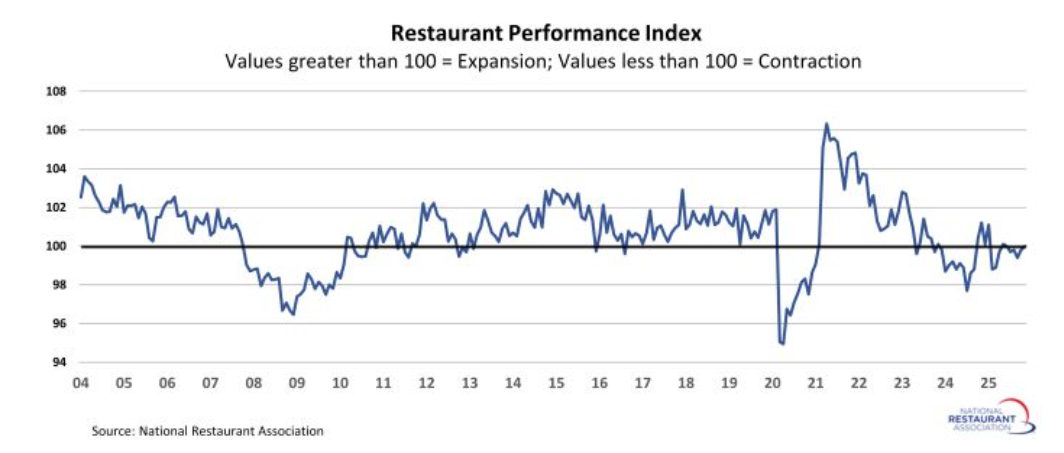

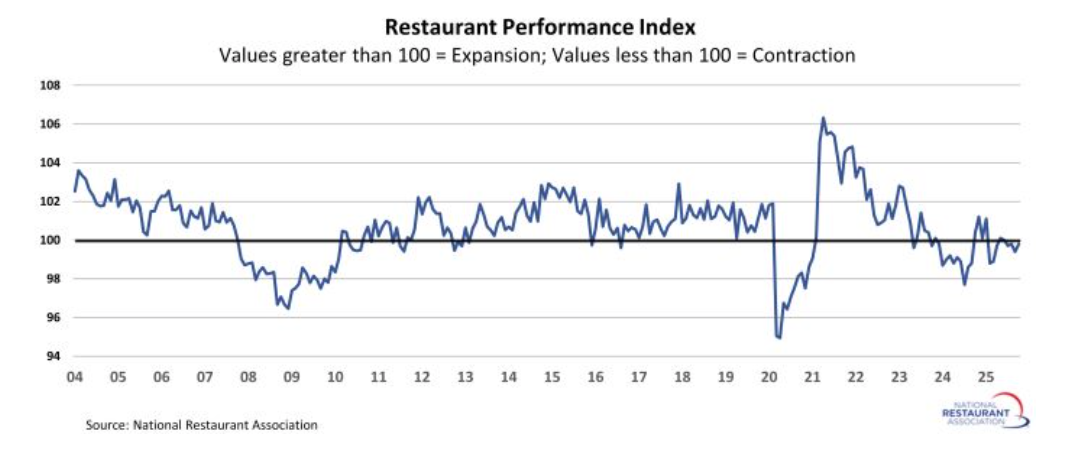

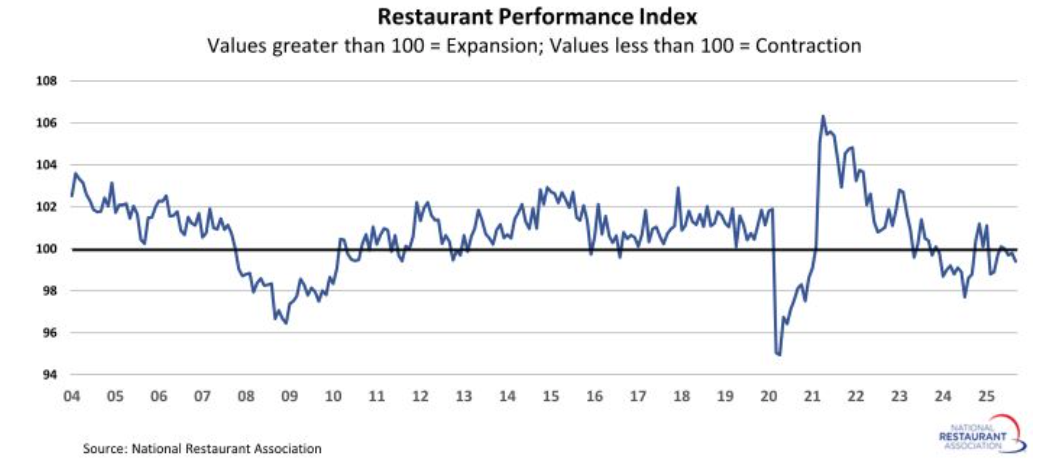

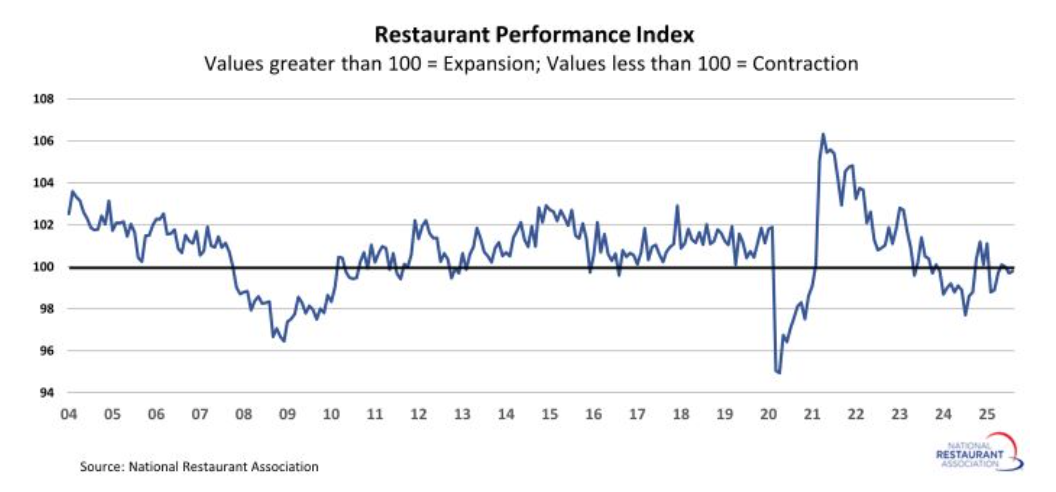

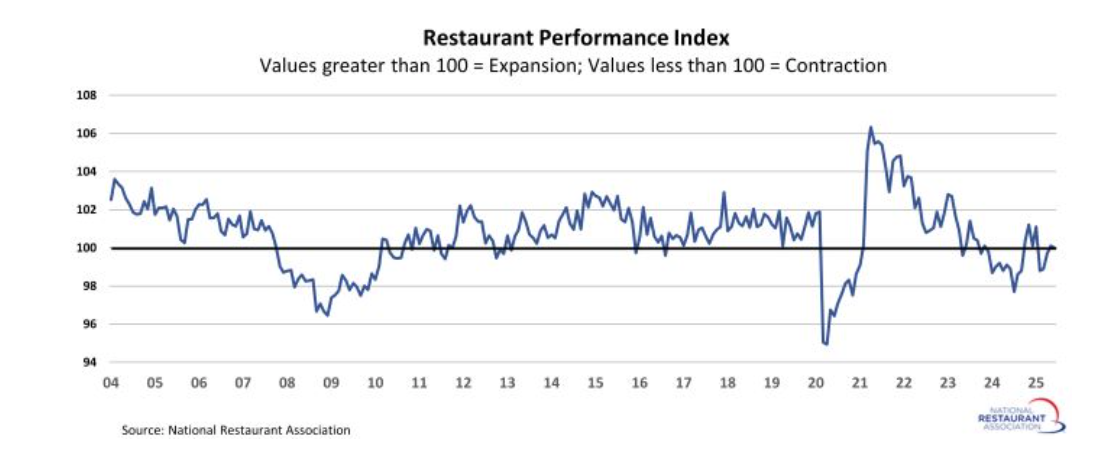

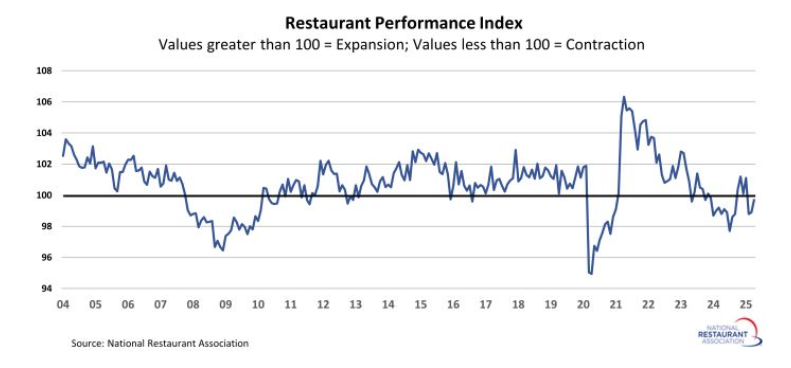

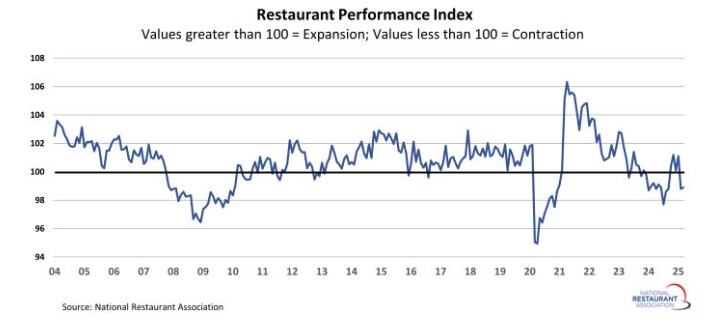

The Restaurant Performance Index rose +0.6% MoM to 99.9 in January 2026, remaining slightly below expansion threshold.

-

The Current Situation Index increased +0.8% MoM to 99.1 but stayed below 100 for a seventh consecutive month, indicating ongoing contraction in operating conditions.

-

Same store sales improved to 99.8 (Dec: 98.3) and 43% of operators reported higher YoY sales (Dec: 37%), though 45% still reported declines.

-

Customer traffic rose to 98.1 (Dec: 96.8), yet 55% of operators continued to report YoY traffic declines, marking a twelfth straight month of net decreases.

-

The Expectations Index rose +0.4% MoM to 100.6, moving into expansion territory driven by improved outlook for future sales.

-

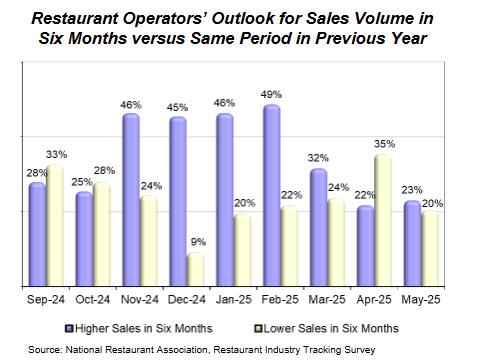

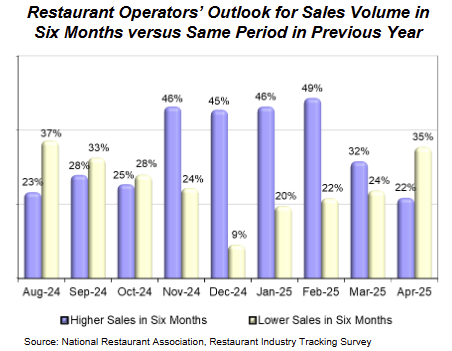

Thirty two percent of operators expect higher sales in six months while only 12% expect declines, indicating moderately improved sentiment.

-

Capital spending remained steady with 50% reporting recent expenditures and 53% planning spending in the next six months, showing continued investment activity.

-

Operators remained cautious on the broader economy as only 20% expect improvement while 25% expect worsening conditions and 55% expect no change.

-

-

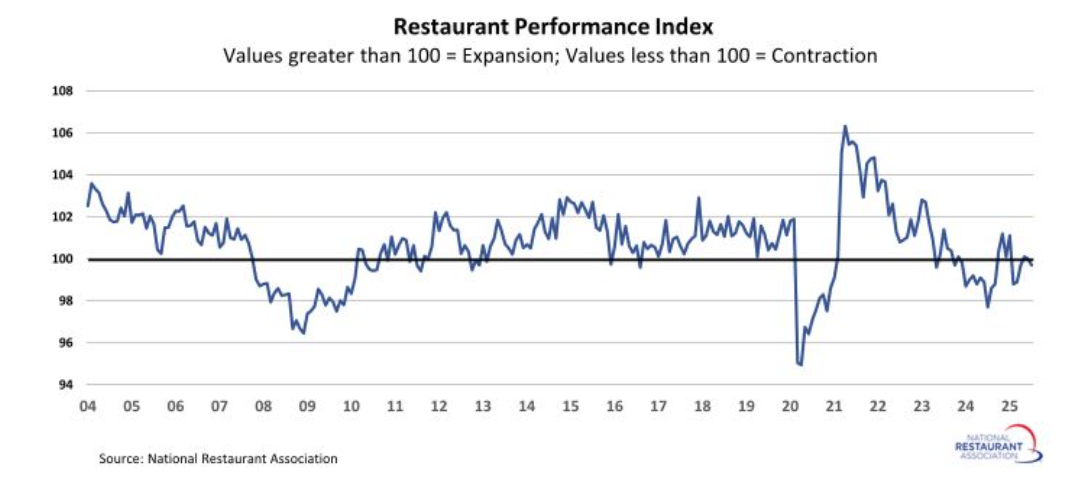

The Restaurant Performance Index fell -0.8% MoM to 99.3 in December 2025, marking weaker industry conditions after briefly reaching expansion territory in November.

-

The RPI declined from 100.0 in November to 99.3 in December, the lowest reading since March and a return to contraction below the 100 threshold.

-

The Current Situation Index dropped -1.0% MoM to 98.3, its lowest level since February and the sixth straight month below 100, reflecting softer operating conditions.

-

Within current conditions, same-store sales slipped to 98.3 (-2.0% MoM) and customer traffic fell to 96.8 (-1.2% MoM), representing the sharpest monthly declines among components.

-

Labor edged down to 97.8 (-0.5% MoM) while capital expenditures remained relatively firm at 100.2 (-0.2% MoM), showing softer activity alongside steady investment.

-

The Expectations Index decreased -0.6% MoM to 100.2, staying just above expansion territory but signaling reduced optimism.

-

Expectations for same-store sales declined to 100.9 (-1.8% MoM) and staffing to 100.1 (-0.7% MoM), while business conditions improved modestly to 99.5 (+0.5% MoM).

-

-

The Restaurant Performance Index (RPI) increased to 100.0 from 99.8 in October (+0.2% MoM), reaching its highest level since June and signaling overall industry conditions at the expansion threshold.

-

The Current Situation Index declined -0.4% MoM to 99.2, remaining below 100 for a fifth consecutive month and indicating ongoing contraction in current operating conditions.

-

Within current conditions, same-store sales eased to 100.3 (-0.9% MoM), customer traffic fell to 98.0 (-0.6% MoM), and labor slipped to 98.3 (-0.2% MoM), while capital expenditures edged up to 100.4 (+0.1% MoM).

-

The Expectations Index rose +0.8% MoM to 100.8, the highest reading in 10 months, reflecting improved six-month outlooks among operators.

-

Sales expectations strengthened notably, with the expectations same-store sales index jumping to 102.7 (+2.0% MoM), the strongest component gain within the expectations category.

-

Expectations for business conditions increased to 99.0 (+1.4% MoM), while staffing expectations dipped slightly to 100.7 (-0.3% MoM), showing mixed forward-looking signals.

-

On the activity side, 47% of operators reported YoY same-store sales gains in November, while 44% reported declines, and 51% reported lower customer traffic YoY, marking the 10th consecutive month of net traffic declines.

-

Capital spending remained active, with 52% of operators reporting investment over the past three months and 55% planning capital expenditures over the next six months, extending a multi-month trend above the 50% threshold.

-

-

The National Restaurant Association’s Restaurant Performance Index rose +0.4% MoM to 99.8 in October 2025, marking a modest improvement but still signaling industry contraction for a fourth straight month.

-

The Current Situation Index increased +0.5% MoM to 99.6, supported by better same-store sales even as customer traffic declined for the ninth consecutive month.

-

Same-store sales strengthened, with 48% of operators reporting YoY gains (Sep: 45%), while 35% reported declines (Sep: 44%), indicating a firmer sales backdrop.

-

Customer traffic remained weak, with 33% of operators citing YoY increases and 48% citing declines, reflecting continued softness in guest counts.

-

The Expectations Index rose +0.3% MoM to 100.0, showing operators’ slightly improved six-month outlook for sales, staffing, and capital spending.

-

Sales expectations softened: 30% expect higher sales in six months (Sep: 34%), while 24% expect declines, showing mixed sentiment.

-

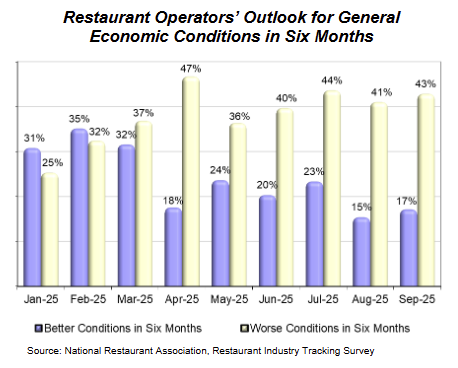

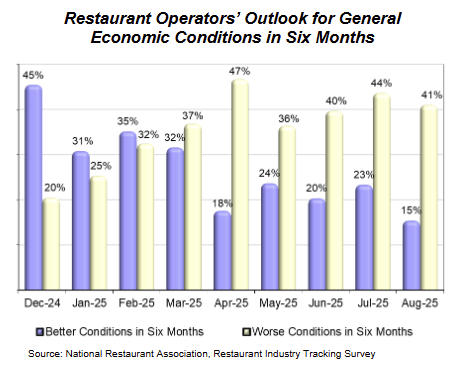

Economic expectations improved modestly: 22% foresee better conditions in six months (Sep: 11%), though 46% still expect worsening conditions.

-

Capital spending remained solid, with 51% of operators investing over the past three months and 54% planning spending in the next six months, marking the seventh straight month above the 50% threshold.

-

-

The National Restaurant Association’s Restaurant Performance Index (RPI) fell -0.4% MoM to 99.4 in September 2025, marking its lowest level since March and signaling continued contraction in restaurant industry activity.

-

The Current Situation Index declined -0.7% to 99.2, its third consecutive month below 100, reflecting weaker same-store sales and ongoing declines in customer traffic.

-

The Expectations Index edged down -0.1% to 99.7, its third straight month in contraction territory, as operators remained cautious about future sales and pessimistic about economic conditions.

-

Same-store sales were mixed: 45% of operators reported YoY gains while 44% saw declines, little changed from August.

-

Customer traffic weakened further, with 34% of operators reporting increases (down from 38%) and 52% reporting declines (up from 42%), marking the eighth consecutive month of net negative traffic.

-

Capital spending remained resilient, with 52% of operators making investments over the past three months—the fourth straight month above the 50% threshold.

-

Looking ahead, only 34% of operators expect higher sales in six months (down from 40% in August), while just 11% foresee an improving economy—the lowest optimism reading in 17 months.

-

Despite softer sentiment, 51% of operators still plan capital expenditures in the next six months, underscoring continued long-term investment amid near-term weakness.

-

-

The National Restaurant Association’s Restaurant Performance Index (RPI) edged up +0.1% MoM to 99.8 in August 2025, but remained below the 100 expansion threshold, reflecting ongoing contraction despite modest sales gains.

-

The Current Situation Index rose +0.1 pts to 99.8, with operators reporting higher same-store sales but continued weakness in customer traffic.

-

The Expectations Index also increased slightly to 99.8, with optimism about sales at its highest since February 2025, though the index stayed in contraction territory.

-

Same-store sales rose for the fifth consecutive month, with 46% of operators reporting gains YoY in August, though this was down from 48% in July.

-

Customer traffic remained a drag, as 42% of operators reported declines in August, marking the seventh straight month of net negative traffic readings.

-

Capital expenditures strengthened, with 54% of operators making investments in the past three months, the highest level in 20 months.

-

Looking ahead, 40% of operators expect higher sales in six months (vs 29% in July), while only 17% anticipate an improving economy and 43% expect conditions to worsen.

-

Despite economic pessimism, 54% of operators plan capital spending in the next six months, the fifth straight month of majority investment intentions.

-

-

The National Restaurant Association’s Restaurant Performance Index (RPI) fell -0.3% MoM to 99.7 in July 2025, slipping below the expansion threshold as weak traffic offset steady sales and cautious operator sentiment.

-

The Current Situation Index dipped -0.2% MoM to 99.7, with same-store sales rising for a fourth month but customer traffic down for the sixth straight month.

-

The Expectations Index declined -0.3% MoM to 99.7, as operators reported mixed sales outlooks and remained broadly pessimistic on the economy.

-

48% of operators reported higher same-store sales YoY in July, while 42% saw declines; traffic trends stayed negative despite a slight uptick.

-

Capital expenditures rose, with 53% of operators investing in the past three months—the highest in 13 months—and 55% planning spending in the next six months.

-

Only 15% of operators expect the economy to improve in six months, the weakest reading since September 2024, while 41% anticipate worsening conditions.

-

-

The National Restaurant Association’s Restaurant Performance Index (RPI) edged down -0.1% MoM to 100.0 in June 2025, holding just at the expansion threshold as mixed sales and traffic trends continued.

- The Current Situation Index declined -0.4% MoM to 100.0, as customer traffic (-0.9%) and labor (-0.7%) slipped, partially offset by a 0.7% increase in capital expenditures.

- The Expectations Index rose 0.2% MoM to 100.1, led by a modest 0.5% gain in future same-store sales expectations and a 0.3% rise in capex plans.

- 49% of operators reported higher same-store sales YoY in June (down from 52% in May), while 36% saw increased customer traffic (down from 40%).

- Just 23% of operators expect the economy to improve over the next six months, while 44% expect conditions to worsen.

- Despite macro pessimism, 54% of operators plan capital expenditures in the next six months, the highest reading in a year.

-

The National Restaurant Association’s Restaurant Performance Index rose 0.4% MoM to 100.1 in May 2025, returning to expansion territory for the first time since January as same-store sales and customer traffic improved.

- The Current Situation Index rose 0.9% MoM to 100.4, led by gains in sales (+1.0%), traffic (+1.6%), and labor (+1.3%), though capex slipped slightly (-0.2%).

- The Expectations Index edged down -0.2% to 99.9, with a drop in business conditions sentiment (-0.7%) outweighing modest gains in sales and capex outlooks.

- 52% of operators reported higher YoY same-store sales in May, the highest share since January; 40% saw an increase in customer traffic.

- Only 20% of operators expect economic conditions to improve over the next six months, down sharply from late 2024 optimism.

- Despite macro concerns, 53% of operators plan capital expenditures in the next six months, up from 52% in April.

-

The National Restaurant Association’s Restaurant Performance Index rose 0.9% MoM to 99.7 in April, but remained below the neutral level of 100, signaling continued contraction in overall industry conditions.

- The Current Situation Index increased 0.5% MoM to 99.4, its second straight monthly rise, supported by modest gains in same-store sales and labor indicators.

- The Expectations Index rose 1.2% MoM to 100.0, reaching the neutral expansion threshold, with slight improvement in sales and staffing outlooks.

- 45% of operators reported YoY same-store sales increases, while 48% continued to see lower customer traffic.

- Only 23% of operators expect higher sales in six months, and just 24% anticipate economic improvement, both notably weaker than late 2024 sentiment.

- Capital spending plans remained firm, with 52% of operators expecting to invest in equipment or remodeling in the next six months.

-

The National Restaurant Association’s Restaurant Performance Index was essentially unchanged in March, rising just 0.1% MoM to 98.9, remaining below the neutral level of 100.

- The Current Situation Index rose 2.0% MoM to 98.9, with modest improvements in same-store sales and customer traffic.

- The Expectations Index fell -1.8% MoM to 98.8, its second consecutive sharp decline.

- The indexes tracking expectations for same-store sales and business conditions were both down by more than -2% on a monthly basis.

- Despite gains in the present indicators, both components remained in contraction territory.

- The overall outlook among restaurant operators grew more pessimistic, particularly regarding future sales and broader economic conditions.