NFIB Small Business Optimism Survey

NFIB Small Business Optimism Survey

- Source

- NFIB

- Source Link

- https://www.nfib.com/

- Frequency

-

Monthly

2nd Tuesday of the month

- Next Release(s)

- April 14th, 2026 6:00 AM

Latest Updates

-

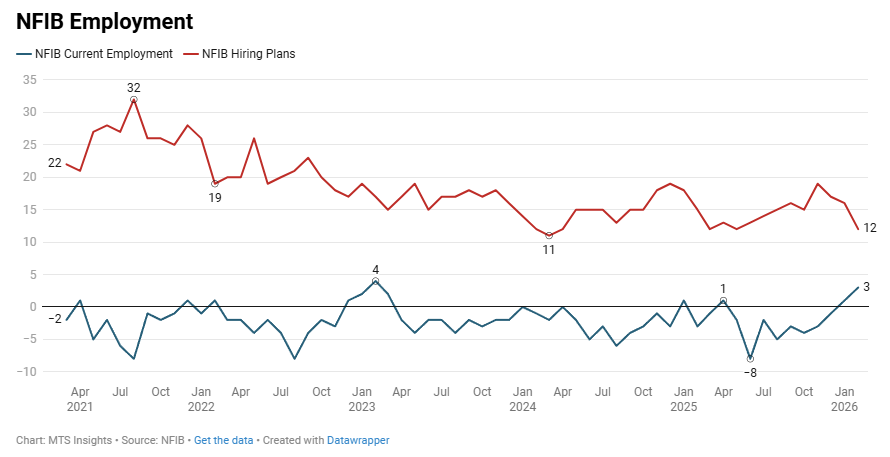

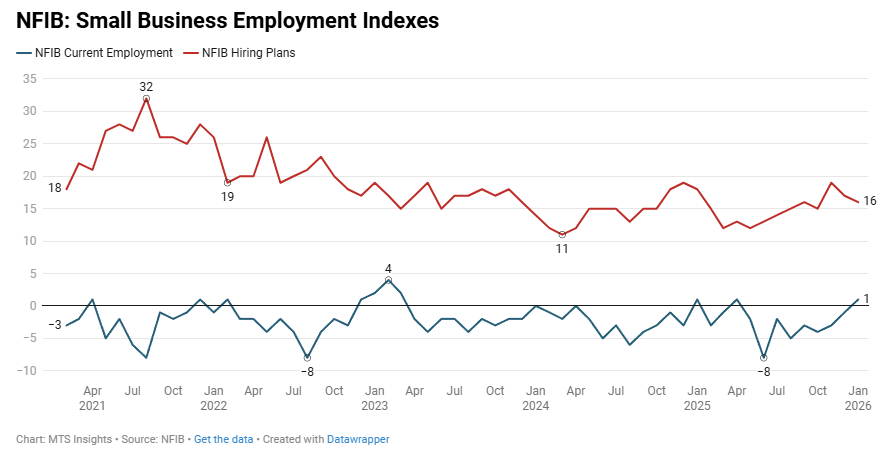

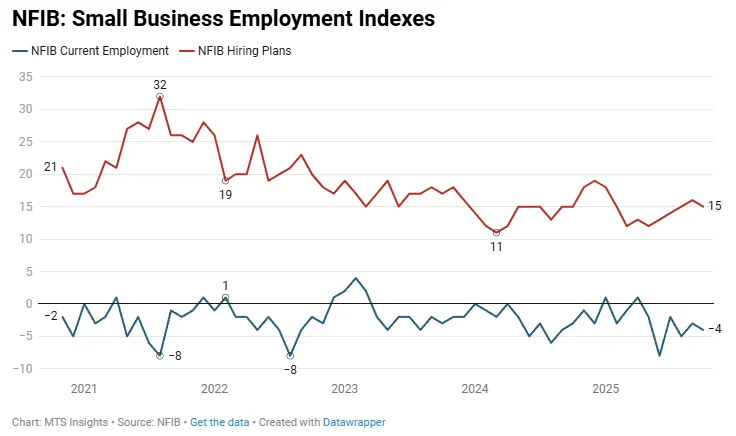

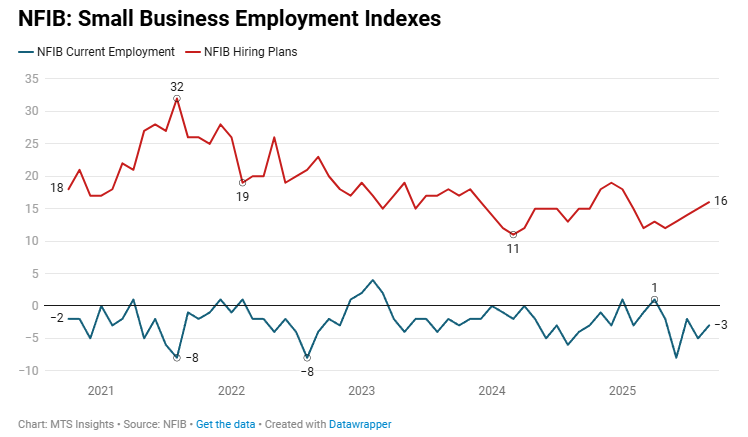

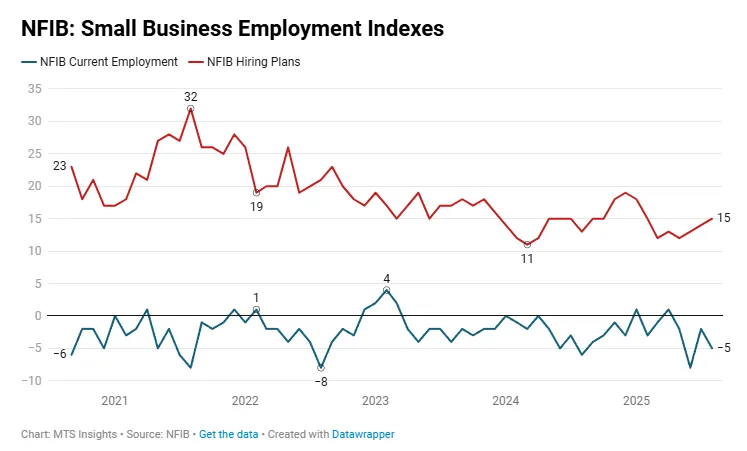

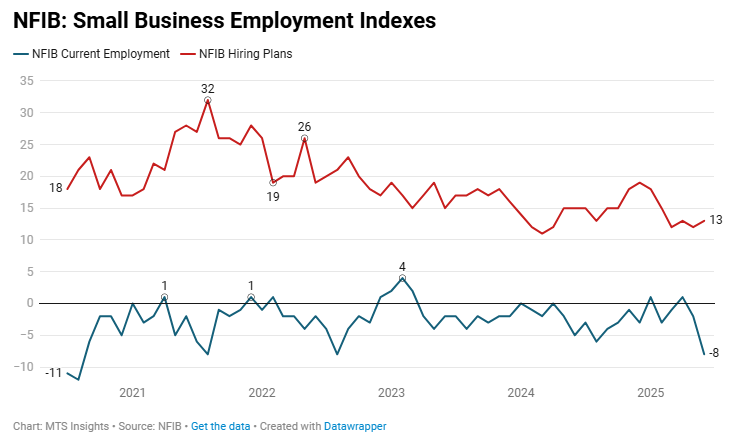

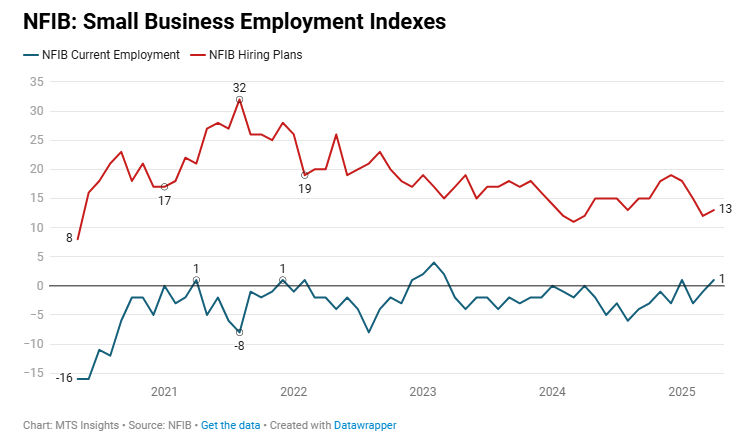

The NFIB Small Business Employment Index rose to 103.5 in February (+~1 pt MoM), standing 3.5 pts above its historical average and indicating continued tightness in the small business labor market.

-

The Employment Index increased to 103.5 (+~1 pt MoM), placing it 2.3 pts above the 2025 average and 3.5 pts above the historical average of 100, indicating that labor demand among small businesses remains elevated relative to long-term norms.

-

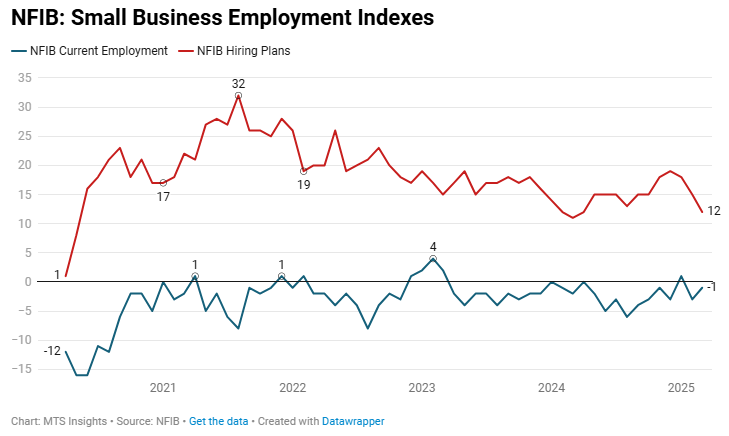

A total of 33% of small business owners reported job openings they could not fill (+2 pts MoM), including 28% with openings for skilled workers (+3 pts) and 10% with openings for unskilled labor (unchanged), highlighting persistent hiring challenges.

-

Hiring activity remained elevated, with 54% of owners reporting they hired or tried to hire in February (+4 pts MoM), though 46% of firms attempting to hire reported few or no qualified applicants, suggesting continued labor supply constraints.

-

A net 12% of owners plan to create new jobs in the next three months (-4 pts MoM), the lowest since May 2025 but still near the historical average of 11%, indicating softer but still positive hiring intentions.

-

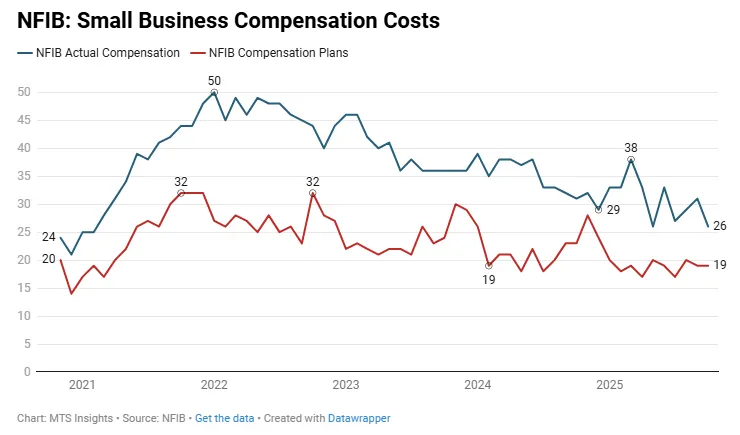

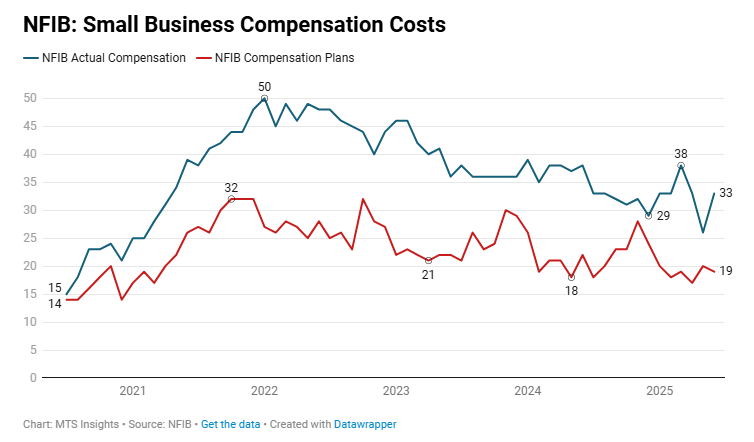

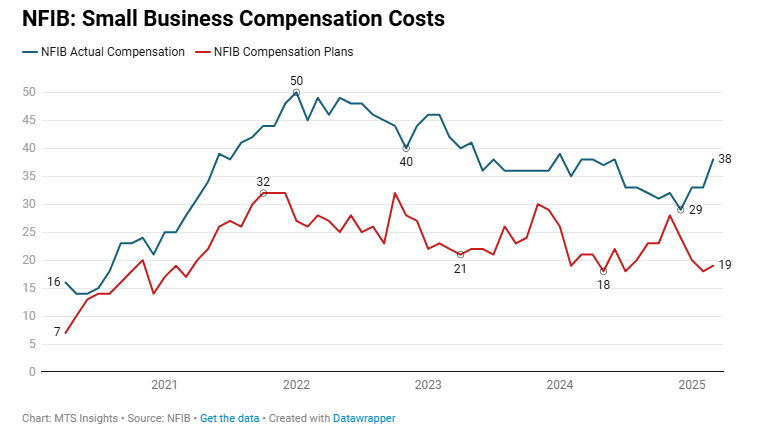

Compensation pressures remained firm as a net 34% of owners reported raising compensation (+2 pts MoM), the highest reading since March 2025, while a net 22% plan to raise compensation in the next three months (unchanged).

-

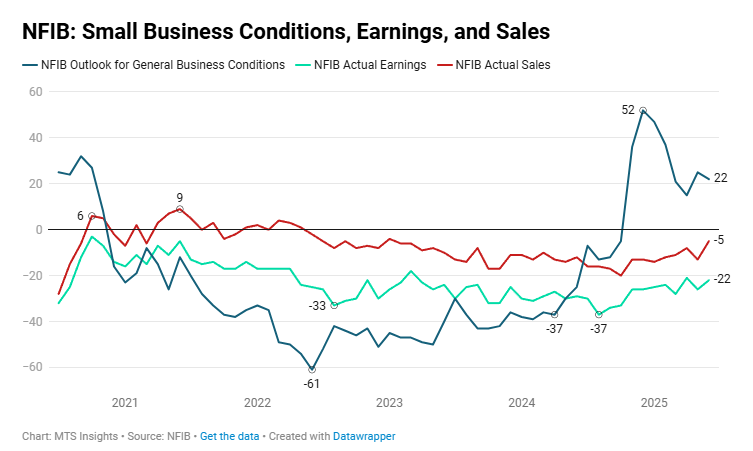

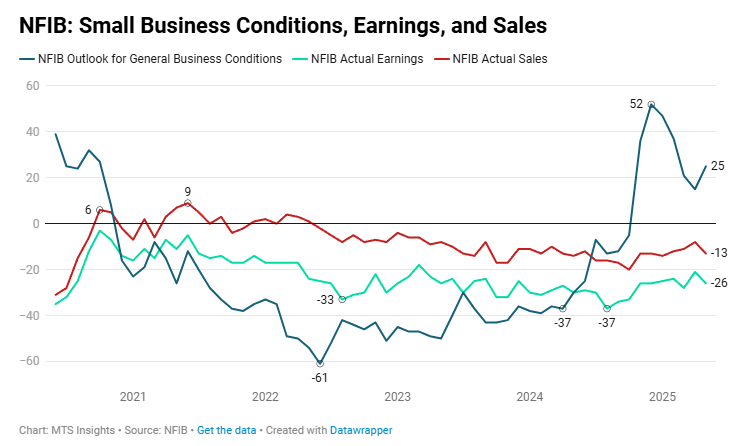

Sales conditions improved modestly, with a net 1% reporting higher nominal sales over the past three months (+7 pts MoM), bringing the reading close to the historical average of 0% and the strongest since May 2022.

-

However, forward-looking demand expectations weakened as the net share expecting higher real sales volumes fell to 8% (-8 pts MoM), reversing the gain seen in January.

-

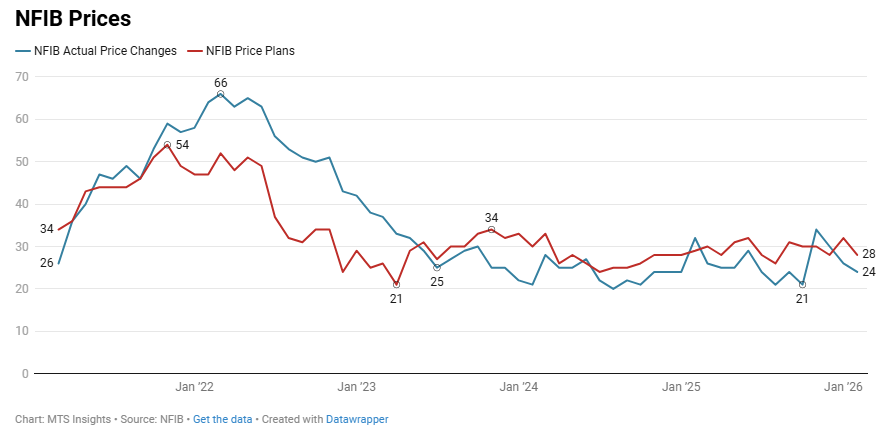

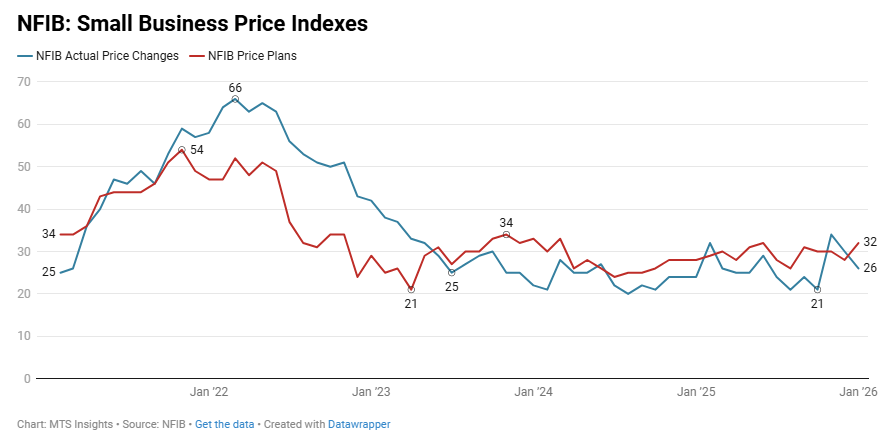

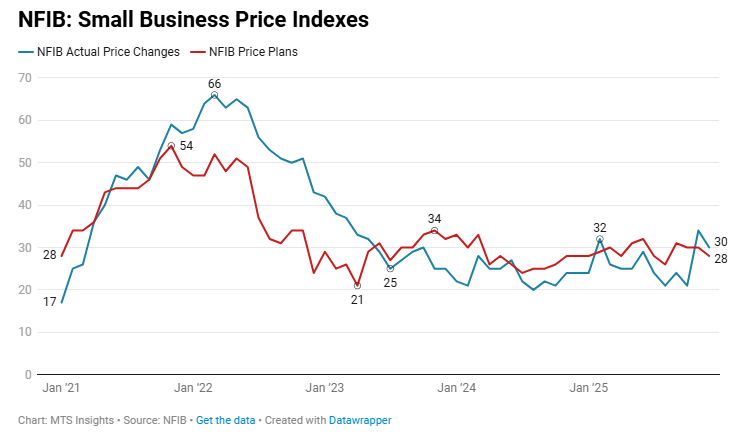

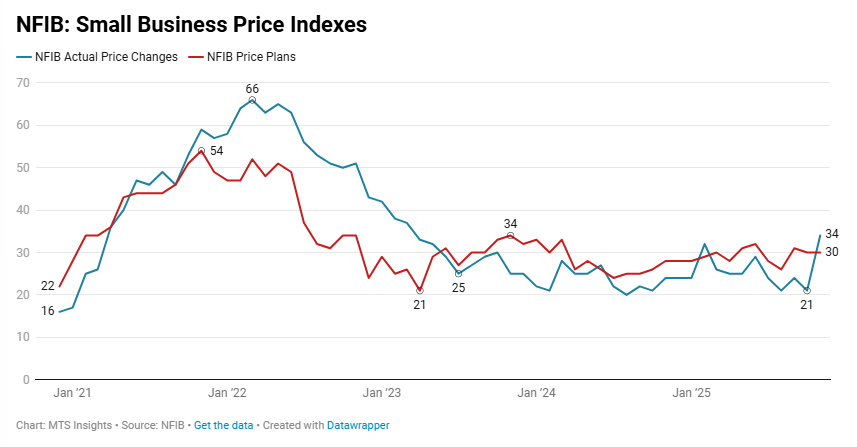

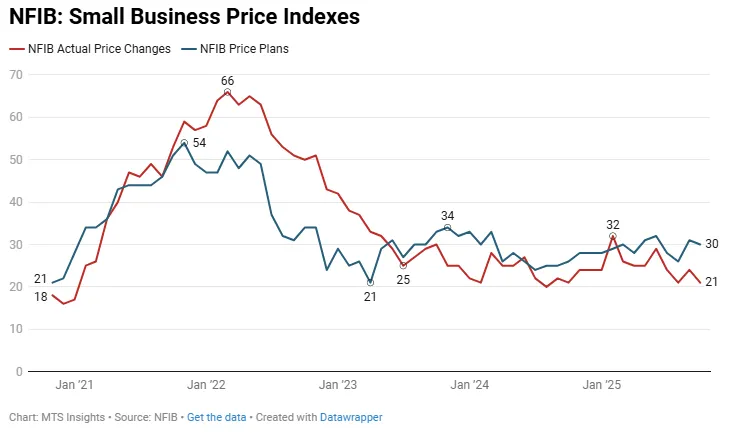

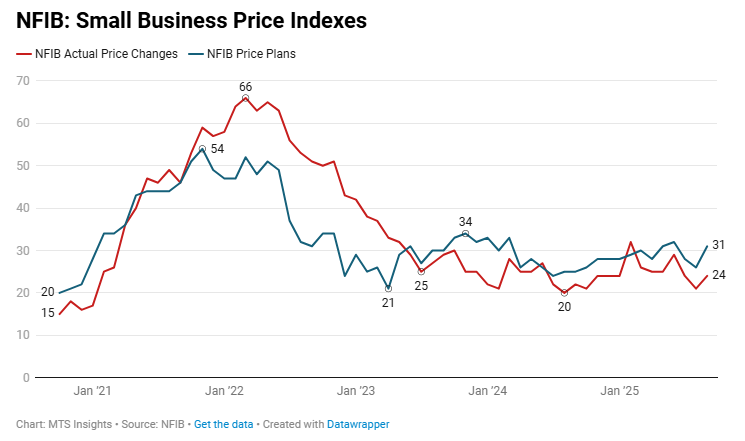

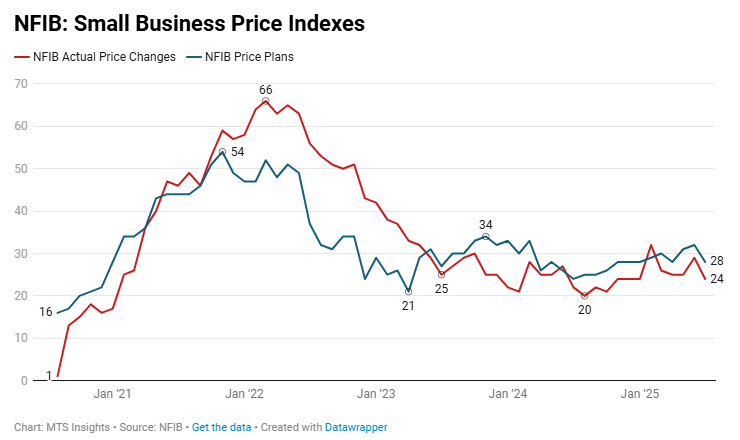

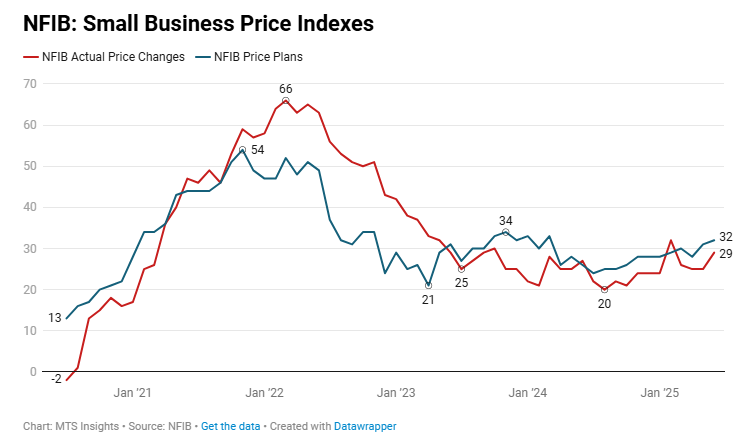

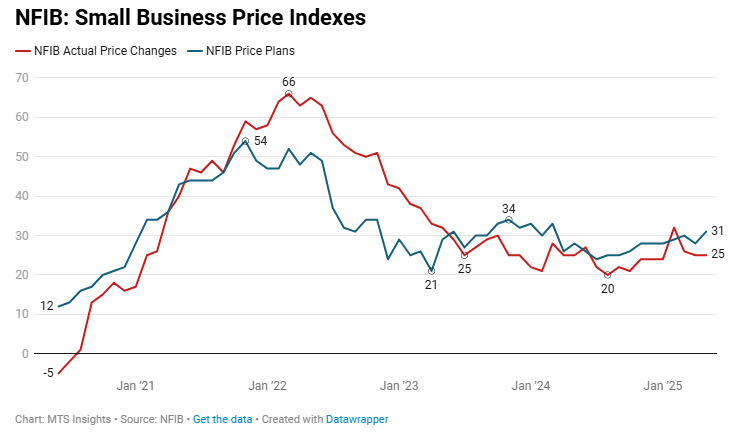

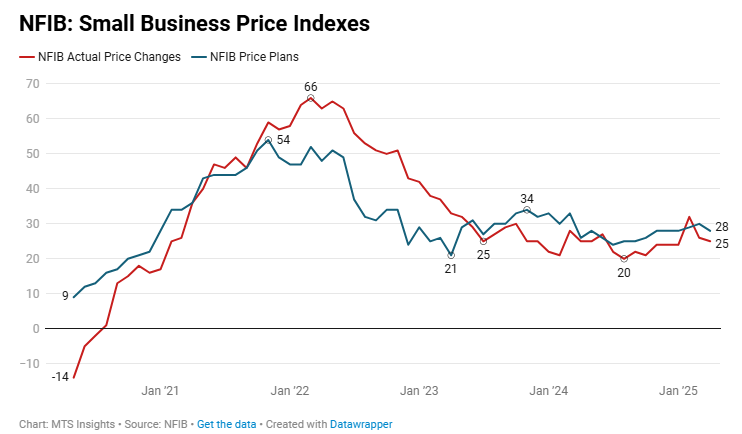

Price pressures eased slightly as a net 24% of owners raised average selling prices (-2 pts MoM) and a net 28% plan price increases in the coming months (-4 pts MoM), though both measures remain above historical averages.

-

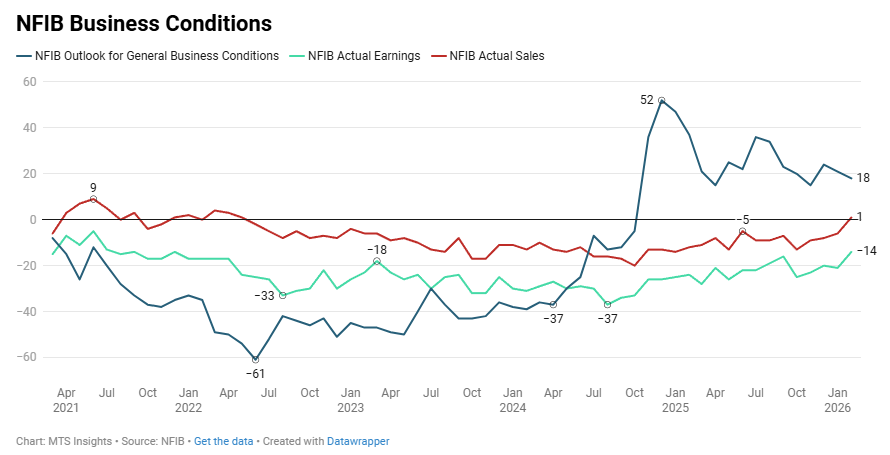

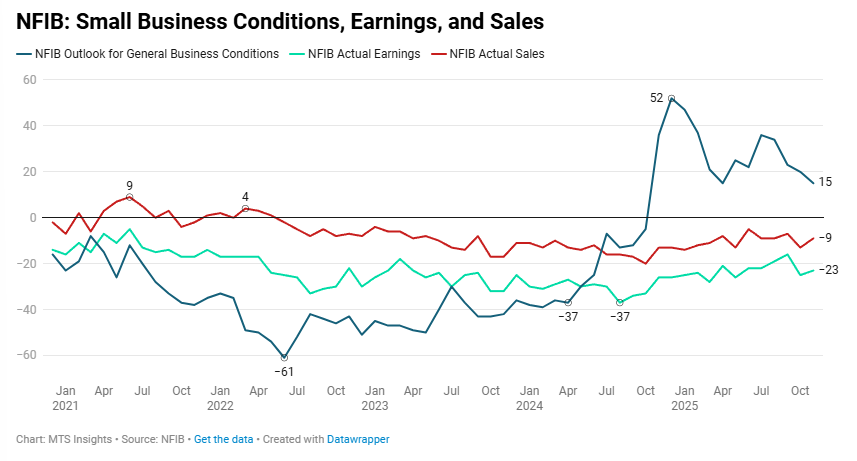

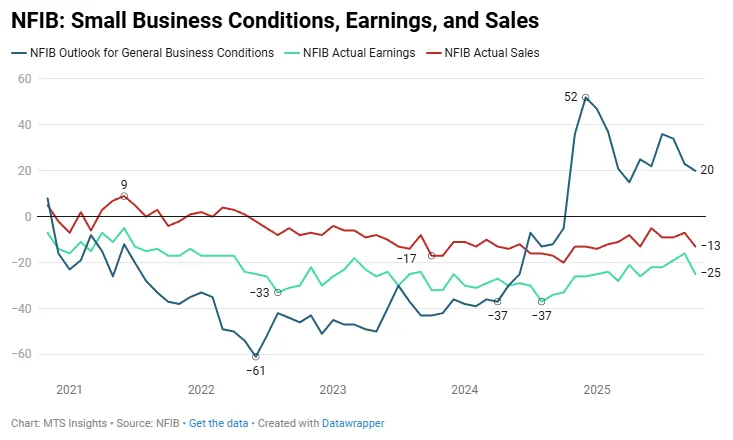

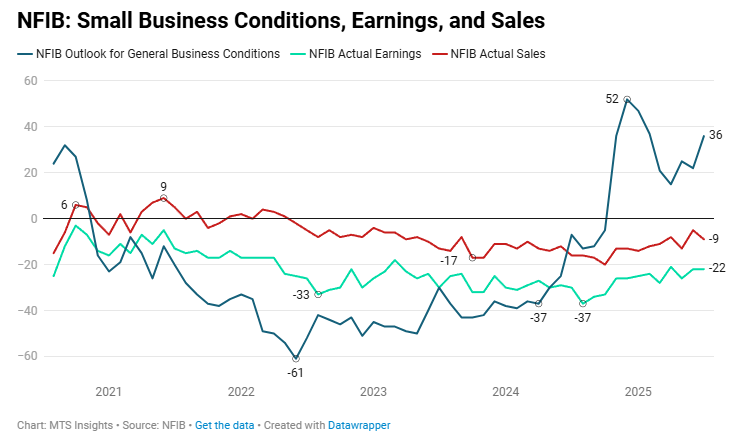

Profit trends improved as the net share reporting positive earnings trends rose 7 pts to -14%, the strongest reading since December 2021, while business condition expectations declined to a net 18% (-3 pts MoM) but remained well above the historical average of 4%.

-

-

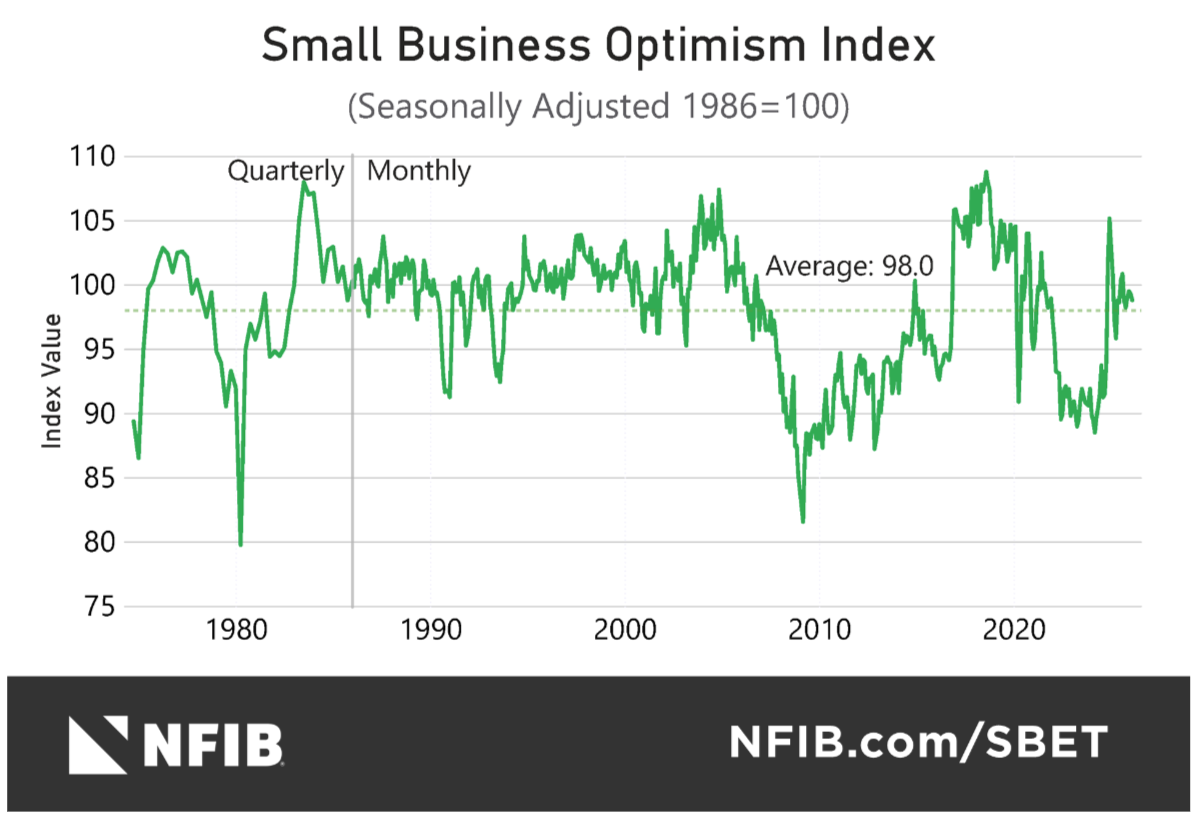

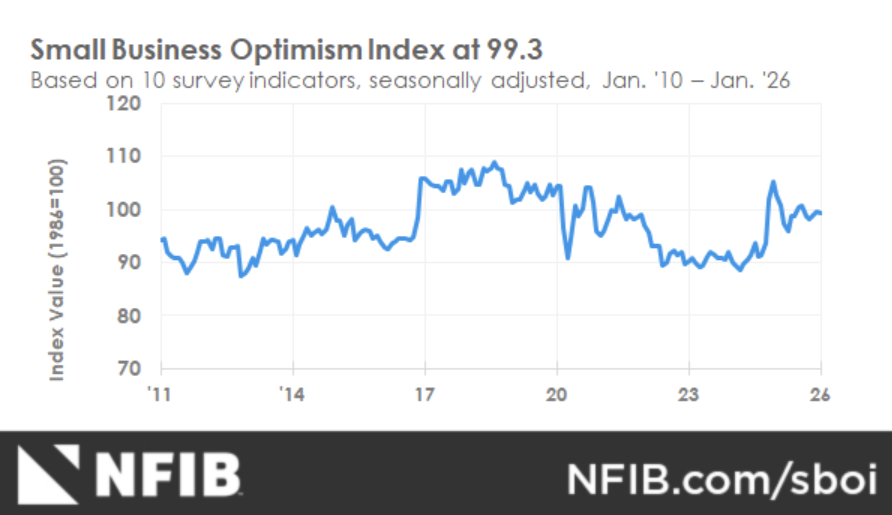

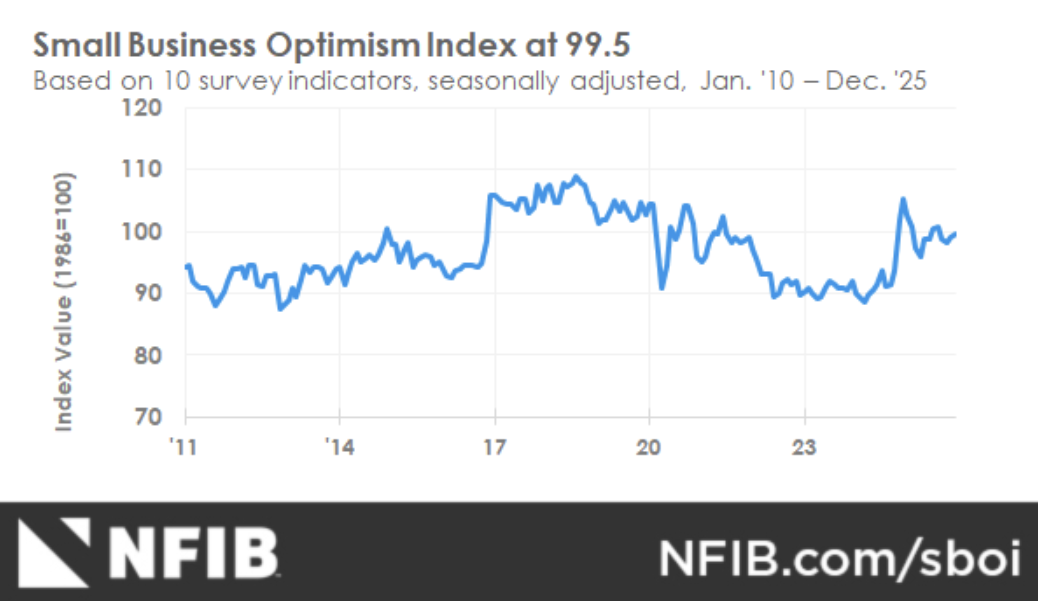

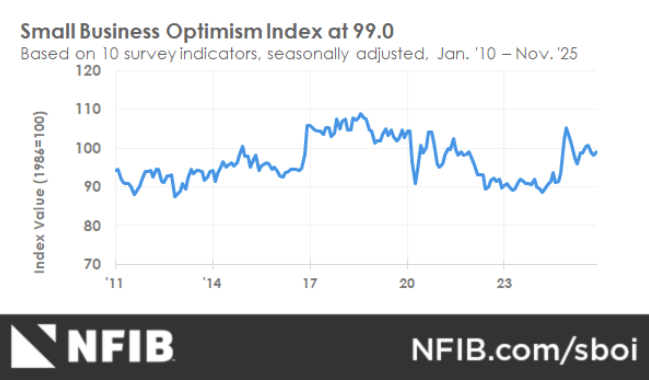

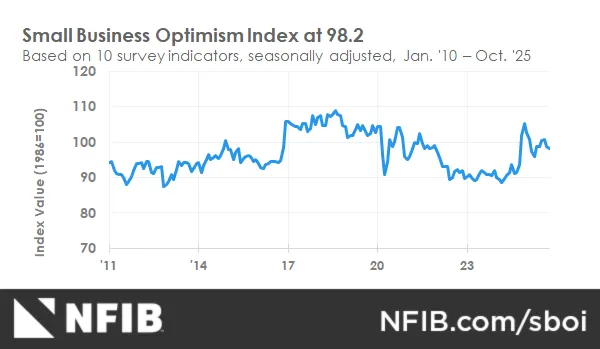

The NFIB Small Business Optimism Index edged down -0.2 pts to 99.3 in January 2026, staying above its 52-year average of 98 amid rising uncertainty.

-

Expected real sales volume rose +6 pts to a net 16% (SA), the only component with a substantial change, pointing to a firmer near-term demand outlook versus December.

-

The Uncertainty Index jumped +7 pts to 91, driven mainly by more owners unsure whether it is a good time to expand, indicating heightened hesitation despite optimism staying elevated.

-

Thirteen percent cited the cost or availability of insurance as their single most important problem (+4 pts), the highest share since December 2018, showing a notable rise in this constraint.

-

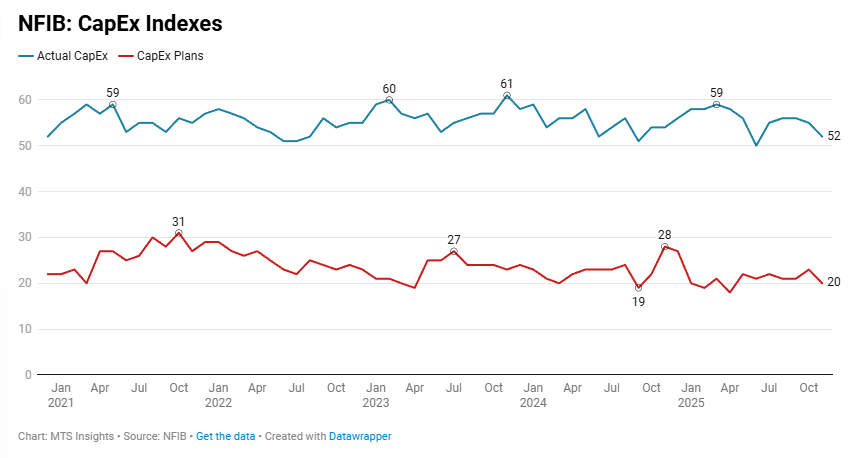

Sixty percent reported capital outlays in the past six months (+4 pts, highest since Nov 2023), while planned capital outlays slipped to 18% (SA, -1 pt), a level described as historically weak.

-

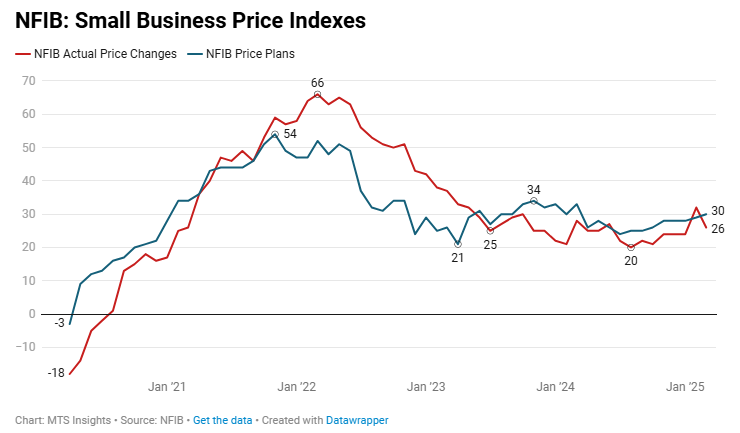

The net share raising average selling prices fell -4 pts to 26% (SA), still well above the historical average of 13%, while planned price increases rose to a net 32% (+4 pts), suggesting near-term pricing intentions firmed despite easing recent increases.

-

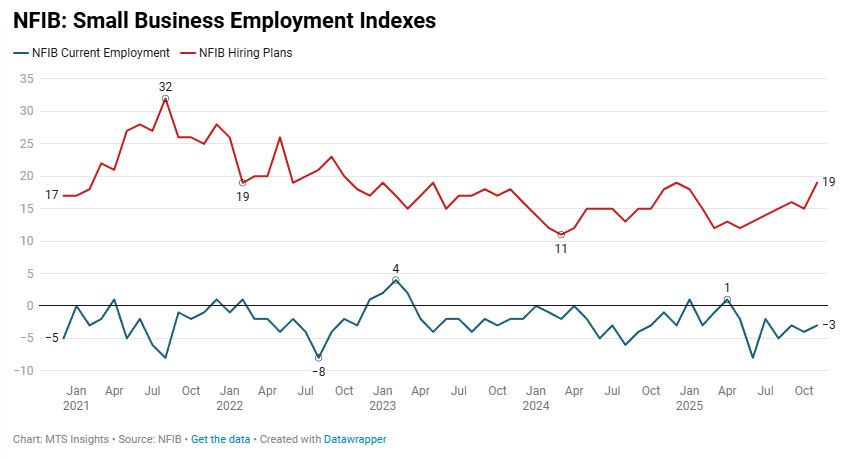

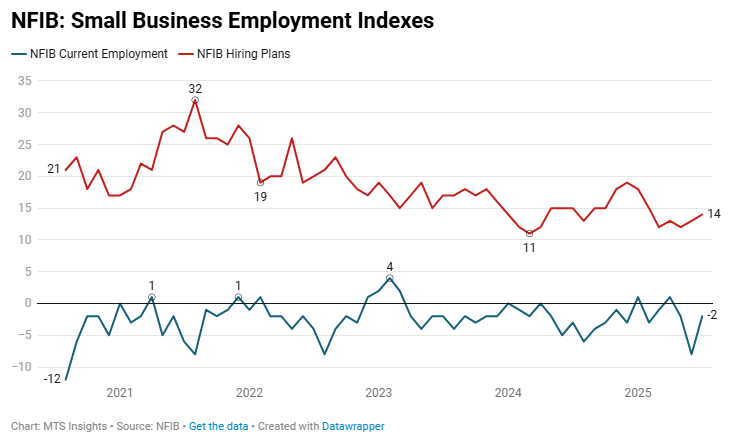

The Current Employment index improved to a net 1% (SA, +2 pts), the highest reading since April 2025 after dipping to cycle lows in Q2 and Q3 2025.

-

Unfilled job openings eased to 31% (SA, -2 pts) but remained above the 24% historical average, with 88% of hiring firms reporting few or no qualified applicants, while job creation plans dipped to a net 16% (SA, -1 pt).

-

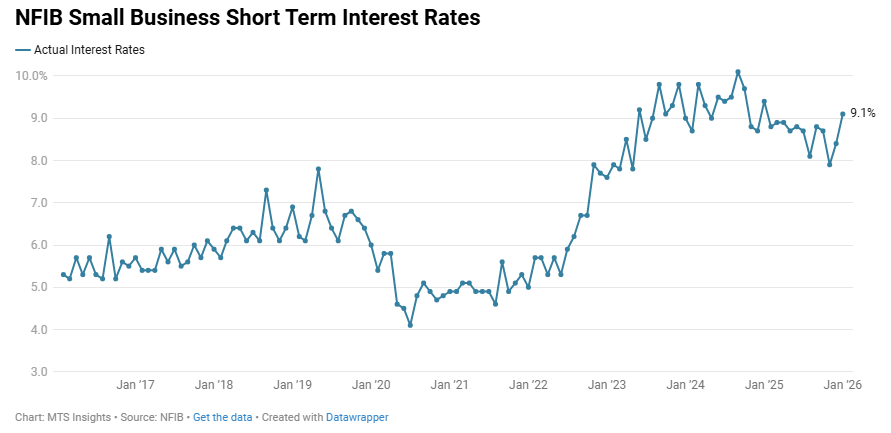

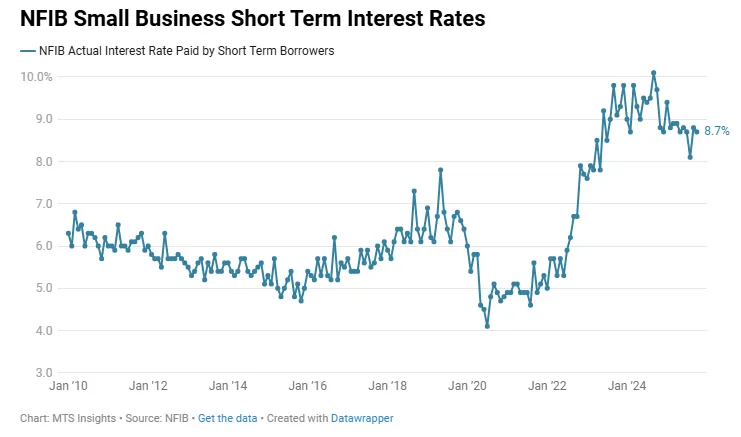

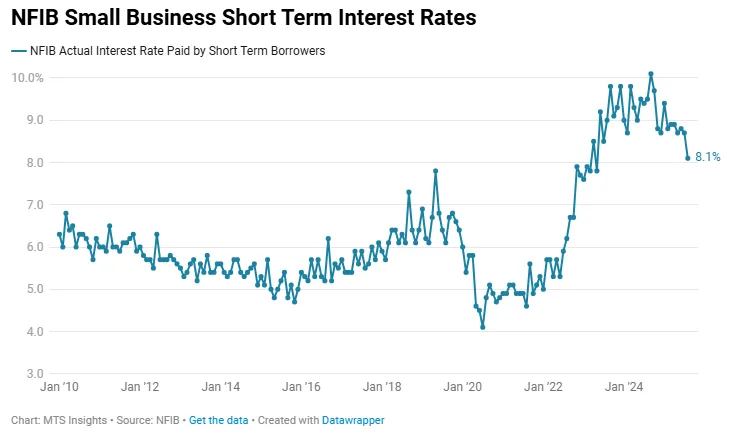

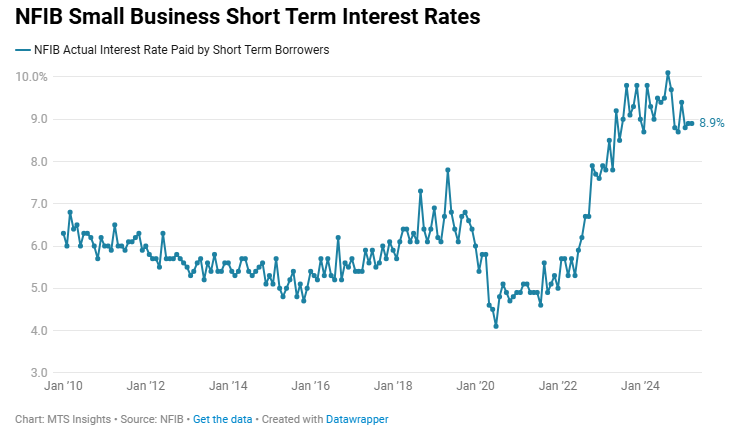

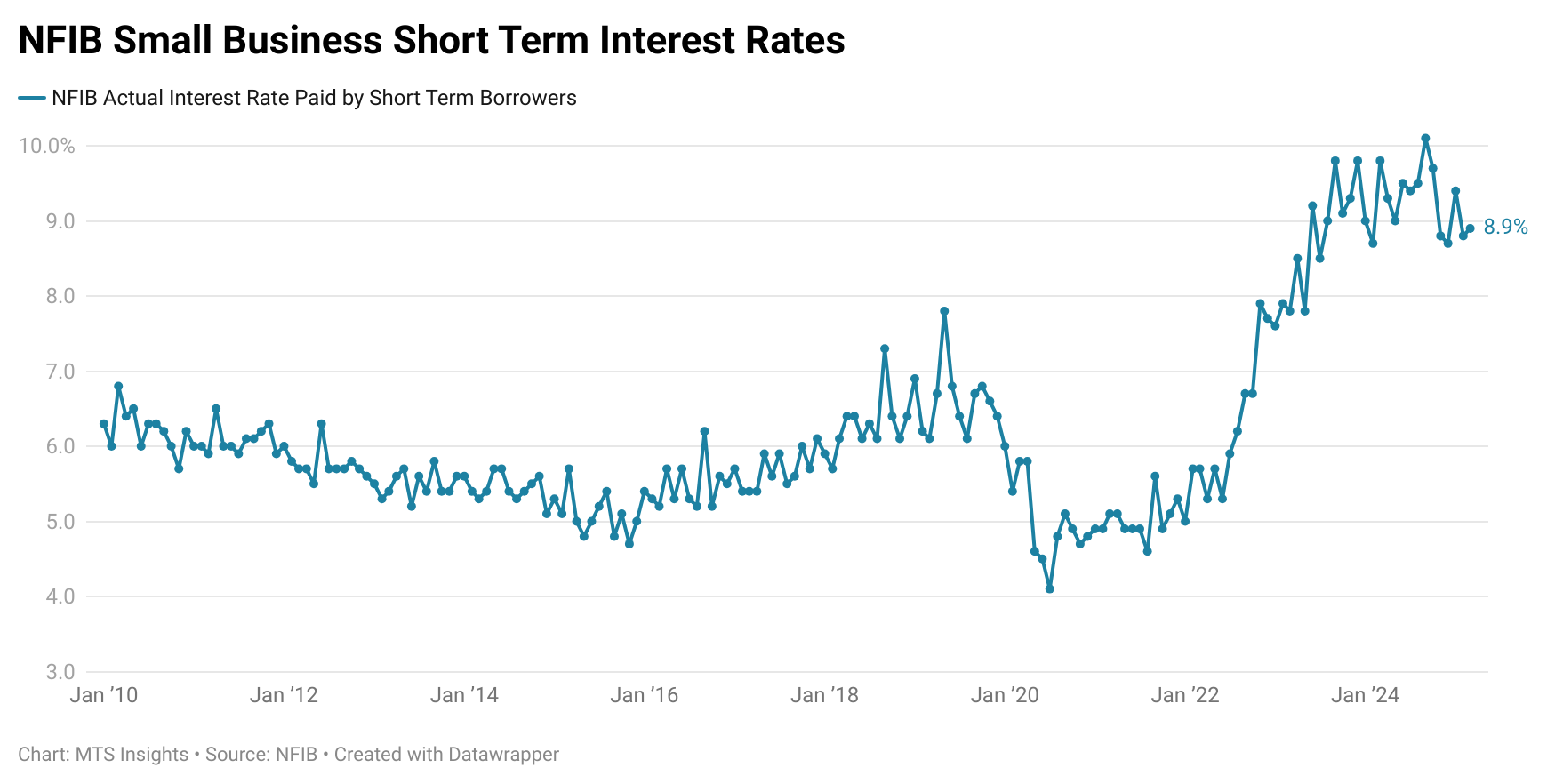

A net -6% reported paying a higher interest rate on their most recent loan (-3 pts), indicating some easing in credit conditions, even as the average short-maturity loan rate rose to 9.1% (+0.7 pts).

-

Business health improved, with 14% rating conditions as excellent (+5 pts) and 27% as fair (-7 pts), while expectations for better business conditions slipped to a net 21% (SA, -3 pts), pointing to stronger current assessments but slightly softer forward-looking views.

-

-

The NFIB Small Business Optimism Index rose +0.5 pts to 99.5 in December, remaining above its 52-year average of 98, driven primarily by strengthened expectations for business conditions while the Uncertainty Index fell to its lowest level since June 2024.

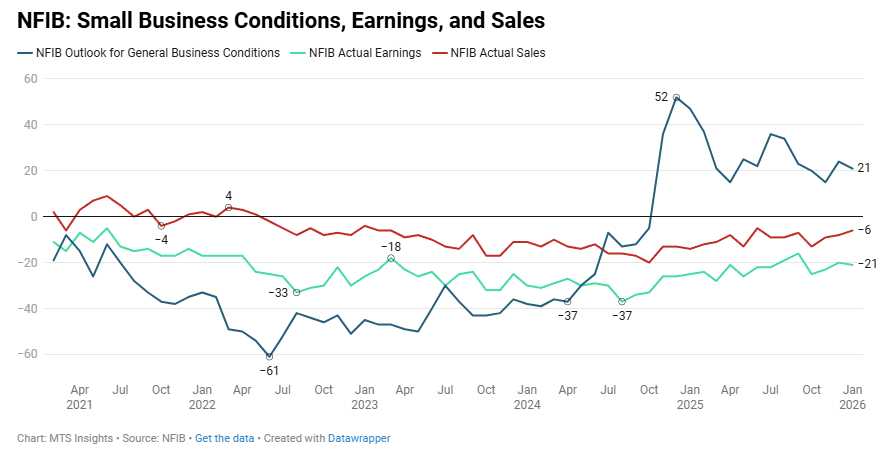

- Business condition expectations surged, with the net share expecting better conditions rising +9 pts to 24 percent (seasonally adjusted), marking the first increase since July and contributing the most to the headline gain, suggesting improved near-term confidence.

- Tax concerns intensified sharply, with 20 percent of owners citing taxes as their top problem (+6 pts from November), the highest reading since May 2021 and now ranking as the single most important issue facing small businesses.

- Price pressures moderated, as the net share raising average selling prices fell -4 pts to 30 percent (seasonally adjusted) and planned price increases declined -2 pts to 28 percent, though both remain well above the historical average of 13 percent, indicating persistent inflationary pressures despite recent easing.

- Credit conditions improved notably, with a net -3 percent reporting higher interest rates on their most recent loan (-5 pts from November), the lowest reading since January 2021, though the average short-term loan rate edged up +0.5 pts to 8.4 percent.

- Compensation pressures increased, with a net 31 percent raising pay (+5 pts from November, seasonally adjusted), while planned compensation increases held steady at 24 percent, reflecting continued upward wage pressure despite moderating labor market tightness.

- Capital spending activity strengthened, with 56 percent reporting outlays in the past six months (+4 pts), driven by vehicle acquisitions at 27 percent (+8 pts) and facility improvements at 19 percent (+5 pts), though forward-looking capital plans at 19 percent (-1 pt) remain historically weak.

- Labor market conditions remained tight, with 33 percent reporting unfilled job openings (unchanged), well above the 24 percent historical average, and 91 percent of hiring firms reporting few or no qualified applicants, while hiring plans declined to a net 17 percent (-2 pts).

- Sales trends weakened slightly, with actual nominal sales at a net -8 percent (+1 pt from November, seasonally adjusted) remaining below the historical average of 0 percent, while real sales expectations fell -5 pts to a net 10 percent, suggesting more cautious near-term demand outlooks.

- Inventory positions improved to their strongest level of the year, with the net share reporting inventory gains rising +6 pts to -1 percent (seasonally adjusted), while views on current stocks (-1 percent) and investment plans (-1 percent) were both unchanged, indicating more balanced inventory management.

- Supply chain disruptions affected 64 percent of businesses (unchanged from November), but the composition improved as significant impacts fell -4 pts to 3 percent while moderate and mild impacts rose, suggesting gradually easing supply pressures despite continued widespread effects.

- Profit trends improved modestly, with the net share reporting positive profit trends rising +3 pts to -20 percent (seasonally adjusted), with 41 percent of those reporting lower profits citing weaker sales and 64 percent of those with higher profits attributing gains to sales volume.

-

The NFIB Small Business Optimism Index rose +0.8 pts to 99.0 in November, remaining above its long run average, with stronger real sales expectations driving most of the gain despite a rise in uncertainty among owners.

-

Sales expectations strengthened notably, with the net share expecting higher real sales up +9 pts to 15 percent, the largest contributor to the headline increase and a sign of more positive demand expectations.

-

Actual nominal sales improved, as the net share reporting higher sales over the past three months rose +4 pts to -9 percent, marking a modest recovery from October’s weaker reading.

-

Hiring indicators firmed, with job openings that firms could not fill rising to 33 percent (+1 pt) and hiring plans climbing +4 pts to a net 19 percent, the highest level of the year, indicating continued labor demand even amid difficulty finding qualified workers.

-

Labor quality concerns eased, with 21 percent citing it as their top problem (-6 pts), though unfilled openings remain well above the historical average and 50 percent of hiring firms still report few or no qualified applicants.

-

Capital spending softened, as 52 percent reported recent outlays (-3 pts) and only 20 percent plan future investment (-3 pts), a historically weak reading consistent with elevated uncertainty about near term capital expenditure decisions.

-

Compensation pressures held steady, with a net 26 percent raising pay (unchanged), while compensation plans rose +5 pts to a net 24 percent, suggesting firms still expect upward wage pressure in coming months.

-

Price pressures increased materially, with the net share raising selling prices jumping +13 pts to 34 percent, the largest monthly gain on record and the highest level since March 2023, pointing to renewed inflation concerns linked partly to supply chain disruptions.

-

Credit conditions showed mild improvement, as the average short term loan rate declined to 7.9 percent (-0.8 pts), while only a net 4 percent reported their last loan was harder to obtain (-1 pt), indicating no major deterioration in access to financing.

-

Business condition expectations weakened, with the net share expecting better conditions falling -5 pts to 15 percent, extending a broader decline that has persisted throughout the year despite solid overall economic performance.

-

-

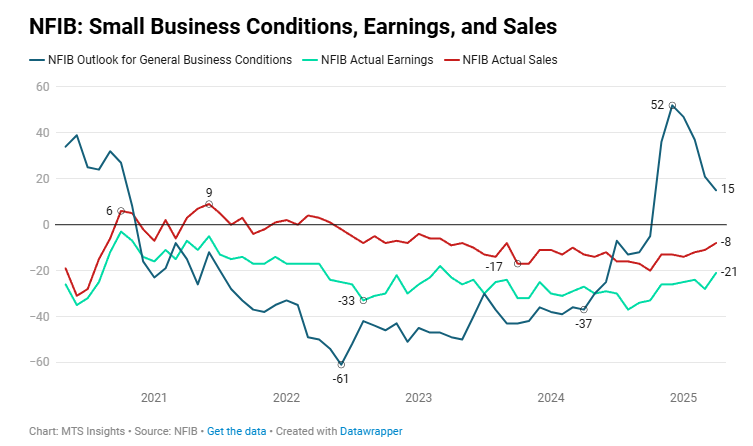

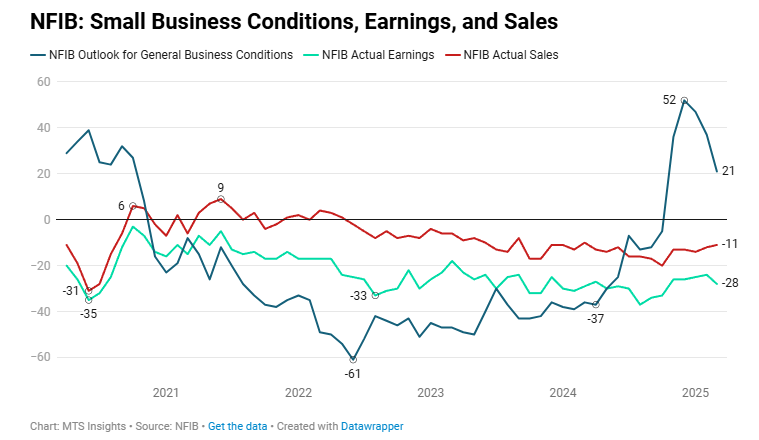

The NFIB Small Business Optimism Index dropped -0.6 pts to 98.2 in October, reaching its lowest level since April (when the “Liberation Day” tariffs were announced). Small business saw a bounce in the months that followed the introduction of broad tariffs, but since then, increases in optimism have been dampened. In the long-term, however, October 2025’s reading is the best for an October since October 2021 when the index was also at 98.2.

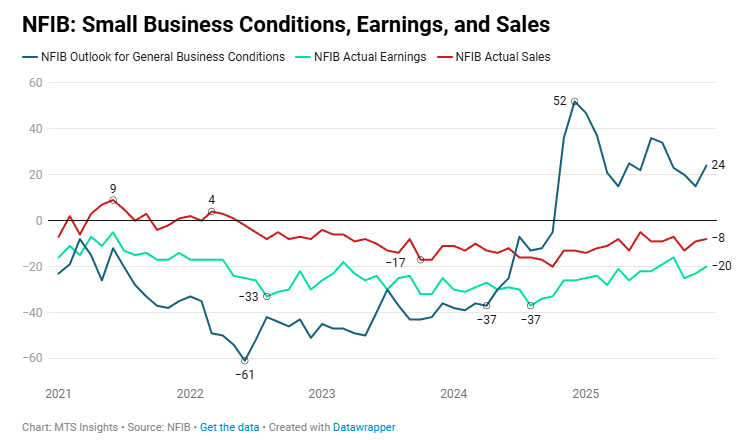

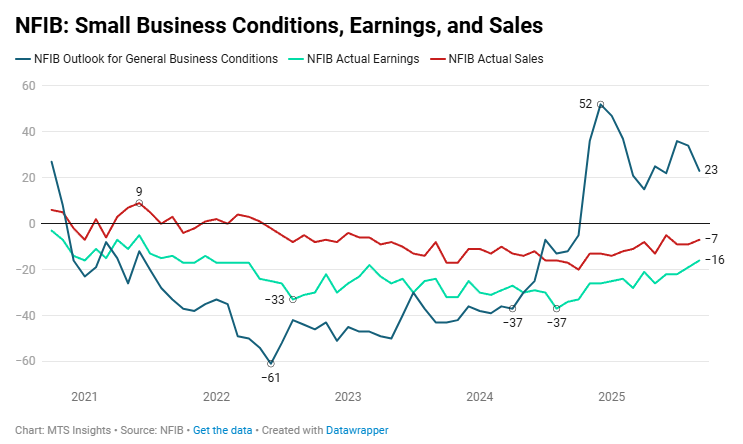

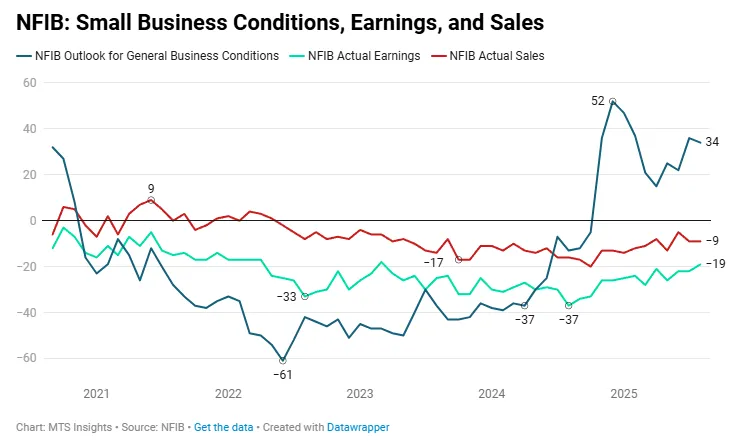

One component stuck out as the main reason for the weaker sentiment in October, the subindex tracking trends in earnings. NFIB noted that the Actual Earnings Changes index dropped -9 pts to -25, the lowest since May of this year, but still above the 2023-2024 averages. The decline in profitability also coincided with a drop in observed sales, down -6 pts to -13 (also the lowest since May), and an easing in the outlook for business conditions, down -3 pts to 20 (lowest since April). Overall, we are seeing a deterioration in both the soft. sentiment and hard, operating data points to a pretty significant degree. A plurality of the businesses that were more negative or uncertain pointed to “economic conditions” as the reason for the expansion outlook.

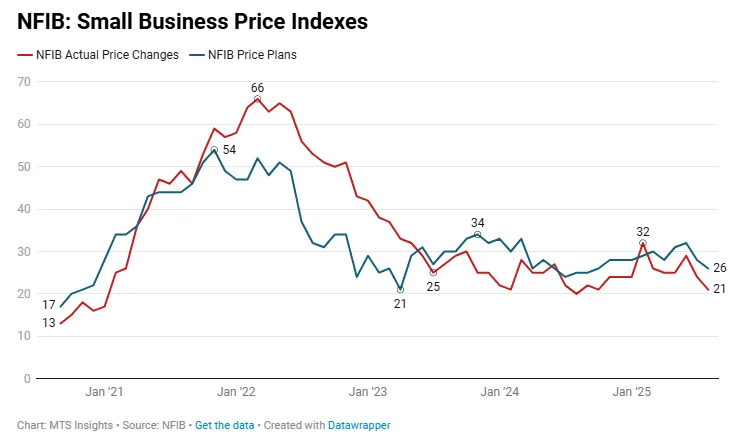

The price indexes moved a bit more favorably in October as both the current and future readings on price changes dropped. The Actual Price Changes index saw the larger decline, dropping -3 pts to 21 which is the joint lowest since August 2024 (tied with August 2025 and October 2024). The Price Plans index was a bit stickier, only dropping -1 pt to 30, as it stayed towards the higher end of the readings of the last three years (2023-2025 average is 28.6). These readings suggest there is still some moderate inflationary pressure on small businesses, but there was a slight decline in the share of respondents pointing to it as the “single most important problem,” from 14% in September to 12% in October.

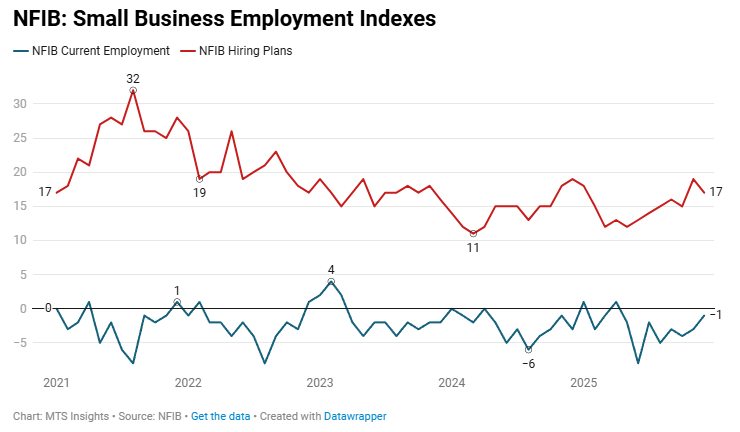

The NFIB’s employment indexes broadly point to a gradual slowdown in hiring by small businesses, but lower supply continues to keep the labor market tighter than it would be otherwise:

- On the demand side, we see that the Actual Employment and Hiring Plans both dropped -1 pt to 15 and -4, respectively. The trend in current employment has been mostly stable this year, while hiring plans have trended down when general optimism declined. The positive gap between actual and expected hiring is likely linked to the supply issue.

- On the supply side, the Job Openings index was unchanged at 32, and the Qualified Applicants index edged down to 49. In fact, 27% of small business owners cited labor quality as their single most important problem, up 9 ppts from September and the highest level since the record high of 29% in November 2021. Construction firms were especially concerned about the labor quality as 49% reported it as the “single most important problem,” 22 ppts higher than for all firms.

The interplay between weaker labor demand and continued supply constraints has kept compensation growth steady. While the overall trend has been one of moderation since the 2022 peak, the deceleration has occurred only gradually. In October 2025, the Actual Compensation index slipped -5 pts to 26, matching its lowest level since February 2021 but still hovering near its 2018–2019 average. Meanwhile, the Compensation Plans index has shown little change this year, remaining in a relatively narrow 17–20% range, suggesting that small businesses continue to face enough hiring challenges to maintain upward pressure on wages.

In terms of financial conditions, small businesses are not finding things too much easier after the September rate cut. The reported interest rate on short-term loans only fell slightly in October, down -0.1 ppts to 8.7%, but on a slightly more positive note, the index tracking rates paid by regular borrowers dropped to the lowest so far this year, indicating that only a net 1% of firms saw increases in rates vs 3 months ago. In general, small businesses haven’t seen a significant improvement due to the September rate cut, but we might see more of a response in the data to the second rate cut in late October.

-

The NFIB Small Business Optimism Index fell -2.0 pts to 98.8 in September 2025, the first decline in three months, reflecting rising inflation concerns, weaker sales expectations, and persistent labor challenges, even as optimism stayed above the long-run average.

-

The Uncertainty Index rose +7 pts to 100, its fourth-highest level in more than 51 years, as owners grew less confident about expansion plans.

-

A net 24% of firms raised prices in September (+3 pts MoM), and 31% plan further price hikes (+5 pts MoM), suggesting sustained inflation pressures.

-

Inflation was cited as the single most important problem by 14% of owners (+3 pts MoM), while 64% reported supply chain disruptions (+10 pts MoM).

-

The share of owners viewing current inventories as “too low” fell sharply to -7% (-7 pts MoM), the largest monthly drop in the survey’s history.

-

Profit trends improved modestly, with the net share reporting higher earnings up +3 pts to -16%, the strongest reading since December 2021.

-

Labor markets remained tight: 32% of firms had unfilled job openings (unchanged), while 16% plan new hires (+1 pt MoM) and 31% raised compensation (+2 pts MoM).

-

The share of firms citing labor quality as their top problem fell -3 pts to 18%, now tied with taxes (18%) as the leading concern.

-

Borrowing conditions tightened, with 7% reporting loans harder to obtain (+4 pts MoM) and the average short-term rate rising to 8.8% (+0.7 ppts MoM).

-

Only 11% of owners said it was a good time to expand (-3 pts MoM), underscoring elevated uncertainty and cautious sentiment heading into Q4.

-

-

The NFIB Small Business Optimism Index this morning presented a slightly more optimistic view of small business conditions, with the headline index edging up 0.5 pts to 100.8 in August, the highest since January, and mostly in line with expectations of a reading of 101. Over the last year, small business sentiment has been volatile, but the broad trend in the data suggests that small business owners are feeling better than they did when supply chain issues and inflation were at their peak in 2021-2022. That is, in large part driven by an improvement in soft data, which was only temporarily shaken by the tariff volatility earlier this year.

NOTE: It is worth noting that the NFIB is an advocacy group that often reflects the concerns of small business owners who tend to lean more conservative, and its survey is sometimes viewed through that lens. That said, the index is widely followed across the political spectrum as a gauge of small business sentiment.

Just as we have seen in the previous months, the improvement in the survey’s soft data points since the 2024 election has been the basis for the improvement in the headline index. While the subindexes tracking the outlooks for expansion and general business conditions eased in August, they remain at their highest levels since the beginning of the year, with the former at 14 and the latter at 34. The hard data points remain negative but are slowly improving. The subindex tracking actual earnings trends has been one key indicator rising over the last two years, and in August, it improved 3 pts to -19, the highest since March 2023. The actual sales index trend has been similar, but in August, it maintained a reading of -9.

The improvement in earnings might be linked to an easing in price pressures in August. Both of NFIB’s price indexes indicated that this might be the case. The subindex tracking current price changes dropped -3 pts to 21 in August, the lowest reading since October 2024, and the indicator tracking expected price increases eased -2 pts to 26, the lowest since January. The moves this past month suggest that the near-term upward pressure on prices from new tariffs has receded, though it’s worth noting that these indexes are still above their long-run averages.

Small business employment trends broadly point to some weakness in hiring within that segment of the economy. The subindex tracking actual employment changes fell -3 pts to -5, and has been negative for the last four months. The last time this index trended this way was in the summer of 2024 when the Fed cut by 50 bps. The index tracking hiring plans was a bit rosier, rising 1 pt to 15, the highest since February. One index that saw a larger move was the measure tracking qualified applicants. It fell -5 pts to 43, the lowest it has been since June 2020. This index's decline is a signal that labor markets are easing since any shift in the quality of the labor supply would be a gradual one that wouldn’t show up in survey data like this.

Amid the challenges seen in employment and inflation, the August NFIB survey pointed to a brighter spot in financing costs, where businesses reported some relief. The average interest rate paid (as reported by small business owners) dropped -0.6 ppts to 8.1% last month, the lowest average reported since March 2023. The easing in financial conditions is likely one of the key drivers of optimism and is likely to continue in September as bond markets see yields drop early this month in response to an increase in Fed rate cut expectations. The 10-year yield is down almost -20 bps so far in September.

Markets have been especially tuned into the trend in interest rates when it comes to investing in smaller-sized firms. The Russell 2000 ETF (IWM) saw its best month since November 2024 (when the results of the election sparked a broad market rally) in August, rising 7.2%. Small caps have started off the month well, but are facing a bit of a drop today in the morning trading session (around -0.9%) since Treasury yields are slightly higher. The big picture for investors in the NFIB survey is the following: it seems that most of the weaker indicators in employment and sales/earnings can be dismissed for the positives in a gradual decline in price pressures and better financial conditions.

-

The NFIB Small Business Optimism Index rose 1.7 pts to 100.3 in July 2025, above the 52-year average of 98, driven by improved expectations for business conditions and expansion plans.

- A net 36% expect the economy to improve (+14 pts MoM), while 16% say it’s a good time to expand (+5 pts).

- Hiring plans rose to a net 14% (+1 pt), though current job openings fell to 33% (-3 pts), the lowest since Dec 2020 but still above average.

- Capital spending plans increased to 22% (+1 pt), and inventory plans rose to 1% (+2 pts).

- Expected real sales slipped to 6% (-1 pt), and earnings trends remained weak at -22% (unchanged).

- The Actual Price Changes index fell -5 pts to 24, the lowest since January, and the Price Plans index fell -4 pts to 28, the lowest in three months.

- Inflation as the top concern stayed at 11%, while labor quality rose as the top issue at 21% (+5 pts).

-

The NFIB Small Business Optimism Index edged down -0.2 pts to 98.6 (vs 98.7 expected) in June 2025, remaining slightly above the 51-year average, as rising inventories and muted sales expectations weighed on sentiment.

- Expected business conditions fell -3 pts to 22, while expected real sales volumes dropped -3 pts to 7. The actual earnings and actual sales indexes both improved but were still negative.

- The Actual Price Changes index increased 4 pts to 29, the highest since February, and the Price Plans index ticked up 1 pt to 32, the highest since March 2024.

- Inflation as the top problem fell to 11%, the lowest since Sep 2021, while taxes rose to 19%, ranking as the top concern for small businesses.

- The Actual Employment index dropped -6 pts to -8, the lowest reading since August 2020. Despite that, hiring plans held steady, and the Job Openings index actually increased 2 pts to 36.

- Labor quality remained the top non-tax concern (16%), though fewer firms saw it as the most important issue than in prior years; labor cost concerns ticked up to 10%.

- The share of owners reporting current inventories as “too high” rose to 12%, while those saying “too low” fell to 7%, contributing the most to the index decline.

- Compensation plans saw a sharp rise, with a net 33% reporting pay increases (+7 pts MoM), the biggest monthly jump since Jan 2020. This may reflect the increasing costs associated with replacing foreign-born workers.

-

The NFIB Small Business Optimism Index rose 3.0 pts to 98.8 in May 2025, just above its 51-year average, driven by improved outlooks for sales and economic conditions.

- The net percent expecting better business conditions jumped 10 pts to 25, while expected real sales rose 11 pts to 10.

- Earnings trends worsened, falling -5 pts to -26, with weaker sales cited as the top reason.

- Hiring plans edged down 1 pt to 12, and job openings remained unchanged at 34%.

- Price hikes remained steady at a net 25%, while compensation plans rose 3 pts to 20 despite a sharp drop in actual wage hikes.

- The Price Plans index increased 3 pts to 31, the highest since March 2024.

- Inventory sentiment rose sharply, with 1% of firms saying current inventories are “too low” — the highest since August 2022.

-

The NFIB Small Business Optimism Index dropped -1.6 pts to 95.8 in April as the small business economic outlook continues to slide.

- The net percent of respondents expecting better business conditions fell -6 pts to 15, the lowest since the 2024 election and down from a peak of 52 in December 2024.

- Readings of hard data did improve even though optimism soured. The Actual Earnings and Actual Sales indexes both increased, up 7 pts to -21 and up 3 pts to -8, respectively.

- The price indexes both eased slightly but remain elevated historically. The Actual Price Changes index fell -1 pt to 25, and the Price Plans index fell -2 pts to 28. Neither readings are 2025 lows.

- The Actual Employment index improved back to positive, up 2 pts to 1, but there is still very little strength in small business hiring. The Job Openings index signaled weaker hiring demand as the index fell -6 pts to 34, the lowest since September 2024.

- Indicators of wage growth weakened, especially in the Compensation Plans index which fell -2 pts to 17, the weakest since March 2021.

- Short-term interest rates remained elevated for small businesses as the NFIB found no change in rates in April compared to March with another 8.9% reading.

-

The Small Business Optimism Index fell for the third month in a row, dropping -3.3 pts to 97.4 in March, below expectations of a smaller decline to 98.9. The rise since the election, driven by a sudden improvement in soft data in response to Trump’s victory, has been cut by over 7 pts in the first three months of 2025. The pain is unlikely to end there. This survey was completed before the announcement of US reciprocal tariffs which has been incredibly bearish for small caps. The fundamentals for smaller firms in the face of tariffs are bleak and should prevent a “buy the dip” moment.

As I highlighted in my analysis of the February NFIB report, the Trump administration’s pursuit of protectionism has caused small business owners to temper the optimistic attitudes they reported in December when sentiment was boosted by lower taxes and deregulation in the coming year. The General Business Conditions Outlook index is the main index that saw a post-election surge, and that has fallen another -16 pts to 21 in March. In total, the index has fallen -31 pts through the first quarter of 2025. The outlook is coming more in line with the measures of actual sales and actual earnings which both remain negative. In fact, the Actual Earnings index fell -4 pts in March to -28, the lowest since October 2024.

The movement in the price indexes suggests that there wasn’t yet a broad concern that tariffs would force small business owners to increase prices. The Actual Price Changes index backed off -6 pts to 32, an important reversal from what looked like a spike in pricing pressures coming from small firms in February. However, the reading is still the 2nd-highest since June 2024 and indicative of a gradual upward trend. Price expectations have seen a smoother increase over the course of Q1 2025, up 1 pt to 30 in March, and are now at the highest since March 2024. I expect these indexes to see larger moves up in the April survey as the reciprocal tariffs (if put in place) would be a broad-based increase in costs at a time when earnings for small businesses are consistently trending lower.

The employment indexes showed a similar trend as the price indexes. The Current Employment index improved 2 pts to -1, partly reversing a -4 pt decline in February. While a flat trend in actual hiring isn’t good, what is more concerning is that small businesses have reversed the increase in their hiring plans that was reported after Trump’s win. The Hiring Plans index peaked at 19 in December and is now down to 12 in March, the lowest since April 2024. For now the reading is positive, but the reaction to a sudden increase in nonlabor costs is likely to lead to a downturn in hiring expectations.

Indeed, employment will have to decline if those labor costs continue to trend the way they have been. The Actual Compensation Costs Index increased 5 pts to 38 in March, the highest since June 2024 and outpacing the Compensation Plans index by the widest margin since early last year. Small businesses consistently find themselves with a shortfall of qualified applicants, and this has pushed labor costs up in response. Paired with the rise in input costs that will come from tariffs, small businesses are looking at further margin compression if they don’t raise prices.

One avenue that small businesses could find some relief is in financing costs. President Trump has signaled several times that he wants Powell and the Fed to cut rates, and a sharp increase in market volatility could provide some relief is there is a flight to safety that causes bond yields to decline. In March, there was no relief as the NFIB measure of small business rates remained elevated at 8.9%, and early April trends suggest that relief this month could be minimal. Volatility caused a short-term decline in rates, but that has been completely reversed and the market continues to respect the inflationary pressures that are likely to come out of the tariffs that would keep the Fed on the sidelines. Additionally, as growth prospects sour, banks are likely to increase the risk premium on financing smaller firms which were already struggling pre-reciprocal tariff announcement.