NADA US Light Vehicle Sales

NADA US Light Vehicle Sales

- Source

- National Automobile Dealers Association

- Source Link

- https://www.nada.org/

- Frequency

- Monthly

- Next Release(s)

- April 30th, 2026 11:00 AM

Latest Updates

-

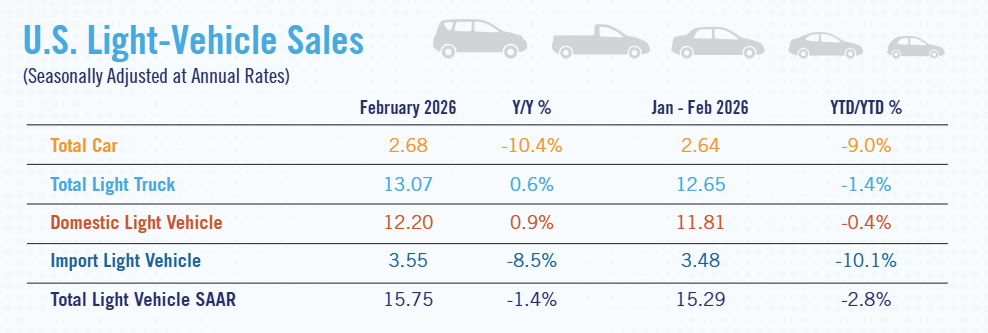

New light-vehicle sales in February reached a SAAR of 15.8 million units, down 1.4% year-over-year. While the sales pace improved compared to January 2026, significant winter storms continued into February and affected sales somewhat in the mid-Atlantic and Northeast regions. The sales pace is expected to accelerate in March as competition between OEMs heats up in the last month of the quarter.

- Battery electric vehicle (BEV) market share totaled 6.3% year-to-date through February, down 1.5 percentage points compared to the same period last year. BEV market share has yet to return to levels seen in 2025, before the expiration of federal BEV tax credits. And this is despite OEMs allocating significantly more incentive spending to their BEV products. According to JD Power, the average discount on BEVs should total $10,356 in February, while discounts on non-EVs should total $3,085. Meanwhile, sales of conventional hybrids have performed well, with market share totaling 13.6% year-to-date in February, an increase of 1.5 percentage points year-over-year.

- Discussions about vehicle affordability have permeated the auto industry as consumers cope with rising payments. According to JD Power, the average monthly payment in February should total $811, up $32 year-over-year. One strategy some consumers have been using to manage higher payments is extending their loan terms. JD Power notes that more consumers are choosing 84-month loans, which should represent 12.7% of financed sales in February, up from 7.7% in February 2025.

- While the Iran conflict is unlikely to have significant impacts on the auto industry in the short term, there certainly are risks depending on the duration of fighting in the region. The conflict could result in higher energy prices, which can lead to increased prices for production inputs and potential supply disruptions.

- So far this year average tax refunds are up roughly 10%, according to the Tax Foundation. Because of higher refunds, we expect a bigger-than-usual boost this spring to used-vehicle demand, as well as potentially a small boost to new-vehicle sales. Looking ahead to the end of the year, we expect new light-vehicle sales will total 16.0 million units in 2026.

-

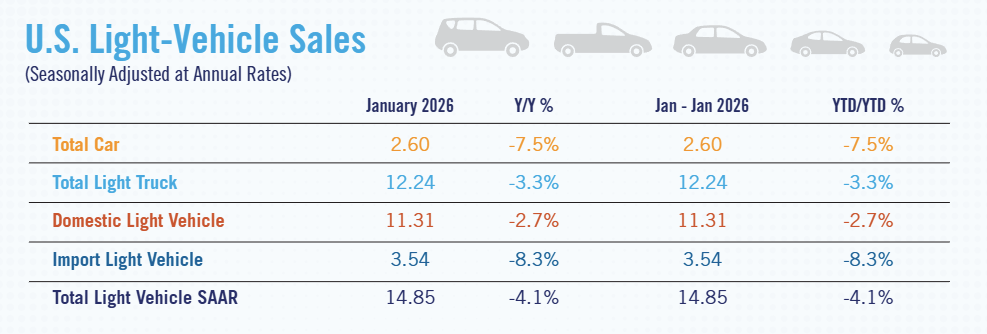

New light-vehicle sales started off 2026 by reaching a January SAAR of 14.9 million units, a 4.1% decline year-over-year and the lowest monthly SAAR since January 2024. Sales in the final two weeks of the month were impacted by severe winter storms, which left many pockets of the country stuck under major snow and ice that dampened store traffic.

- J.D. Power estimates that new-vehicle discounts fell in January. Average incentive spending per unit totaled $3,335, a 5.6% increase compared to January 2025, but down 5.5% compared to December 2025. As a share of MSRP, average incentive spending per unit reached 6.6%. Prior to the pandemic, average OEM discounts were closer to 10% of MSRP, so OEMs likely have room to raise discounts to juice demand if they choose.

- Battery electric vehicle (BEV) market share in January reached 6.6%, a decline of 1.9 percentage points compared to January 2025. With no federal EV tax credits in 2026, we will be paying close attention to any shifts in BEV sales and market share. Conventional hybrids continued to sell well in January, with market share at 12.6%, an increase of 0.5 percentage points year-over-year.

- At the end of January, new light-vehicle inventory on the ground and in transit totaled 2.53 million units, down 9.2% year-over-year and down 2.0% compared to December 2025. We expect new light-vehicle inventory to hover between 2.5 million and 2.6 million units in the first half of the year before rising the rest of the year. Our outlook for new-vehicle sales in 2026 is 16.0 million units.

-

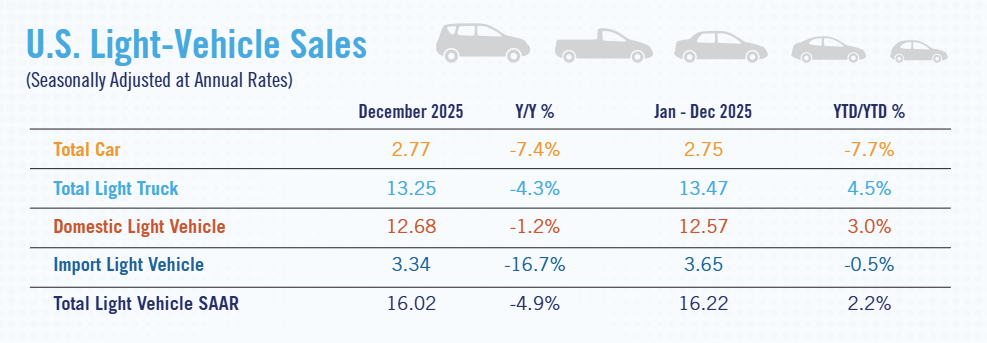

New light-vehicle sales totaled 16.2 million units in 2025, an increase of 2.4% compared to 2024. The US auto industry experienced several shocks last year, including tariffs on imported vehicles and parts as well as the end of the EV tax credits. But tariff announcements induced some consumers to pull ahead purchases in Q2 and buy a vehicle before the tariffs took effect. And the expiration of EV tax credits on September 30 spurred buying activity in Q3, leading to a record-high monthly market share for battery electric vehicles (BEV) of 11.8%.

- While BEV market share reached an all-time high in September, sales cooled significantly once tax credits were no longer available. By December, BEV market share fell to 5.9%, a decline of 5.9 percentage points compared to the record set in September. For all of 2025, BEV sales total 1.26 million units, an increase of 1.2% compared to 2024. Despite the increase in BEV sales, BEV market share declined year over year by 0.1 percentage points to 7.7% in 2025.

- Meanwhile, sales of conventional hybrid vehicles increased significantly in 2025. Conventional hybrid sales reached 2.05 million units, up 27.6% year over year. Given the changes in the regulatory landscape, we expect BEV sales growth to continue to cool and hybrid sales to increase as OEMs build vehicles with powertrains more in line with current consumer demand.

- Despite concerns of significant price increases due to tariffs, average transaction prices increased modestly as most OEMs absorbed much of the additional costs. According to J.D. Power, the average transaction price for a new light vehicle in December 2025 should total $47,104, up 1.5% compared to December 2024. The average monthly payment on a new-vehicle finance contract in December 2025 will likely reach $776, an increase of $22 compared to December 2024. Payment increases were somewhat muted as average interest rates declined slightly during the year. J.D. Power estimates the average interest rate on a new-vehicle finance contract will be 5.84% in December 2025, a decrease of 32 basis points year over year.

- Looking ahead to 2026 we are optimistic about new-vehicle sales, though there will certainly be challenges as the industry adjusts to evolving regulatory and trade environments. With the passage of the One Big Beautiful Bill last year, we expect tax season will provide a solid boost to consumer spending and be a tailwind for new-vehicle sales. However, a lackluster labor market may cause some consumers to wait before buying a new vehicle. Still, we expect a solid year for new light-vehicle sales, with a forecast of 16.0 million units in 2026.

-

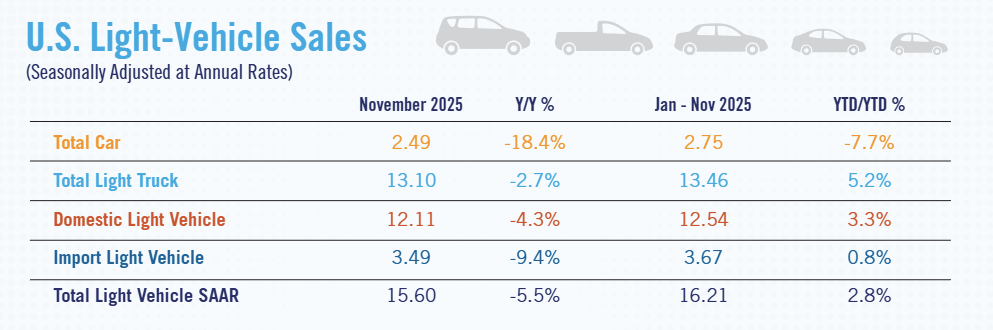

New light-vehicle sales in November 2025 were down year-over-year for the second month in a row. The November 2025 SAAR of 15.6 million units represents a decline of 5.5% compared to November 2024 but was a slight improvement over the October 2025 SAAR of 15.3 million units. The industry is still dealing with the aftermath of significant pull-ahead sales volume that occurred as consumers bought vehicles earlier this year before the expiration of the EV tax credits and before tariff-related price increases took effect.

- November was the second month without the EV tax credit, and BEV market share continued to fall—reaching 5.1% of all new vehicles sold, which was less than half the all-time high of 11.3% in September. Discounts remain high on EVs, with J.D. Power estimating that the average EV incentive per unit will total $11,869 in November. Overall average incentive spending per unit is expected to show an increase of $375 from October, reaching a total of $3,211 for November.

- J.D. Power estimates that the average new-vehicle retail-transaction price will total $46,029 in November, up $722 year over year. The average new-vehicle monthly payment in November is set to reach $760, a record for the month of November in any previous year. Those with trade-ins will be helped as used-vehicle values have been increasing recently. The industry leased significantly fewer cars three years ago due to the semiconductor microchip shortage, leading to tight supplies of late-model used inventory available today. Rising used-vehicle values should help those consumers with a trade-in vehicle.

- Despite the slowdown in sales so far in Q4, we expect new light-vehicle sales to finish the year at 16 million-plus units, given the strong sales performance earlier this year.

-

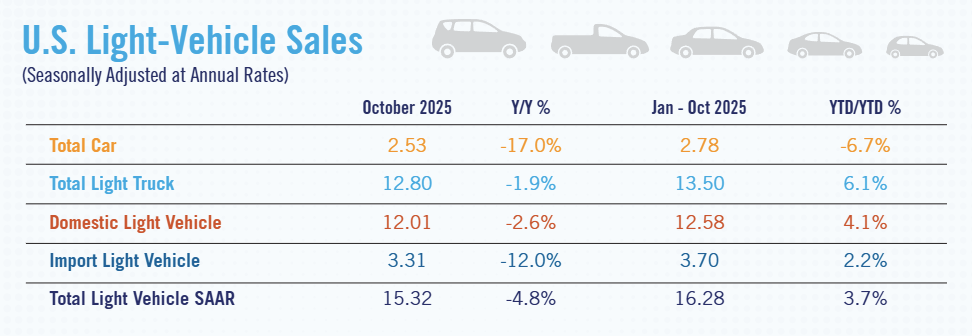

New light-vehicle sales in October 2025 recorded the lowest SAAR in 15 months. The October 2025 SAAR of 15.3 million units represents a decline of 4.8% year over year and 5.9% compared to September 2025. The SAAR decrease was primarily driven by the decline in battery electric vehicle (BEV) sales, which fell significantly in October 2025 following the end of the EV tax credits on September 30.

- BEV sales represented just 5.9% of new-vehicle sales in October 2025, down from the all-time high of 11.3% in September 2025. BEV sales in October 2025 totaled just under 75,000 units, a decline of 46.7% compared to September 2025 and down 23.8% year over year. The expiration of the EV tax credits in September pulled ahead many EV sales that likely would have occurred later. The decline in BEV sales could have been more severe without several OEMs increasing their own incentives in October to help make up for the loss of the federal credit. According to J.D. Power, average incentive spending per unit on BEVs totaled $13,161, up $2,047 compared to September 2025. It remains to be seen what the natural demand for BEVs will be in the absence of the credit, but we do expect it will take quite some time for BEV sales to reach the rate they were in the final months of the EV tax credits.

- Our outlook for the rest of the year is for a slower sales pace relative to Q3 2025. Given the pull-ahead sales that occurred earlier this year, a slower Q4 won’t necessarily impact full-year sales totals too much. We expect sales will be flat or up slightly compared to full-year 2024.

-

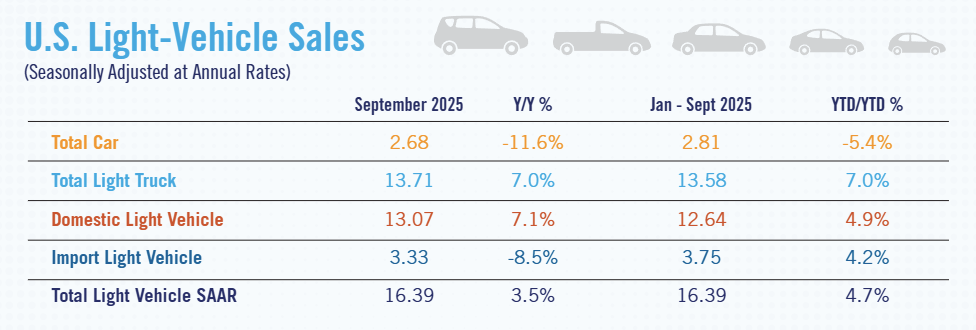

New light-vehicle sales in September 2025 reached a SAAR of 16.4 million units, up 3.5% year over year. September was a solid sales month as many consumers headed to dealer lots before EV tax credits expired on September 30. Battery electric vehicle (BEV) sales hit an all-time high in market share and accounted for 11.8% of all new vehicles sold. This market share was up nearly two percentage points from August 2025, which was also a strong month for BEV sales. Year-to-date, BEV sales accounted for 8.4% of all new vehicles sold, an increase of 0.7 percentage points compared to the same period last year. And for third-quarter 2025, BEV sales increased 24.1% year over year. Plug-in hybrid (PHEV) vehicles, which were also eligible for the tax credits, didn't perform nearly as well as BEVs. PHEV sales in September 2025 accounted for just 1.7% of all new vehicles sold, which is right in line with their year-to-date market share of 1.8%.

- The average discount on a new vehicle increased slightly from August to September. According to J.D. Power, average incentive spending per unit should totaled $3,116, up just $24 compared to August 2025. J.D. Power notes that more incentive spending was targeted at EVs. Expressed as a share of the average MSRP, overall incentive spending is expected to be 6.1%, while incentive spending for non-EVs should reach just 4.8%. New light-vehicle inventory on the ground and in-transit totaled 2.65 million units at the end of September 2025, up by 6.2% compared to August 2025 but down 5.9% year-over-year. Looking ahead, we expect inventory levels to end the year slightly below their levels at the end of Q3.

- New light-vehicle sales have been solid so far through the third quarter, with a year-to-date SAAR of 16.4 million units—an increase of 4.7% year over year. We believe there has been some significant pull-ahead volume, as consumers rushed to dealer lots earlier in the year before tariffs took effect and in recent months as consumers purchased EVs before the end of tax credits. The big question now: Will volume hold in the final quarter of the year and into next year as 2026 models arrive on dealer lots? We have already seen several OEMs release price increases in the mid-single-digit percentage range for 2026 models, and we are watching closely to see how much—and when—OEMs will pass along tariff-related price increases. Given the strong sales performance so far, we have increased our 2025 sales forecast to 15.9 million units.

-

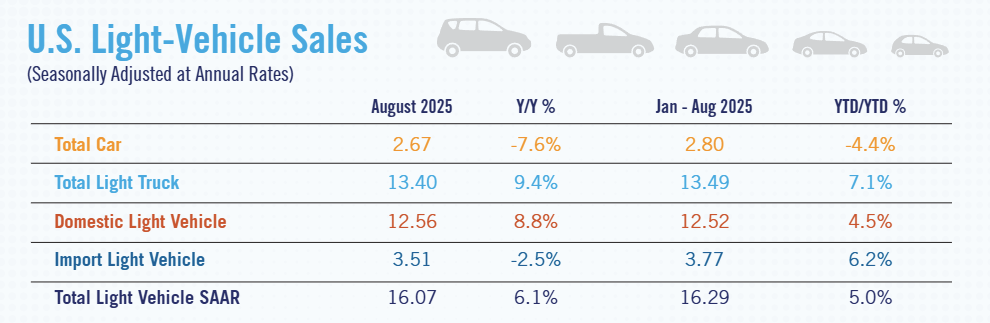

New light-vehicle sales in August 2025 totaled a SAAR of 16.1 million units, an increase of 6.1% year over year. Through the first eight months of the year, new light-vehicle sales are up 5.0% year over year on a SAAR basis. Tariff price increases are expected to appear in MSRP increases as OEMs transition from the 2025 to 2026 model year. August’s sales strength could indicate that some consumers want to secure their vehicle before the price increases kick in.

- BEV sales were very strong in August as consumers headed to dealerships to purchase these vehicles before the tax-credit phaseout at the end of September 2025. In August 2025, BEV market share reached 9.7%—up 1.2 percentage points from July 2025 and the highest on record. Year-to-date BEVs have accounted for 7.7% of all new-vehicle sales this year. Looking ahead to September, we expect strong BEV sales for the month but believe BEV sales will cool in the final quarter. Hybrid vehicles also continue to be hot sellers, accounting for 12.3% of all new-vehicle sales this year. Hybrid sales volume was a touch under 1.35 million units through August 2025, an increase of 34.8% year over year.

- The August 2025 sales total included the Labor Day weekend. Typically, this is one of the biggest sales weekends of the year, and OEMs respond by increasing incentive spending. According to J.D. Power, OEMs have kept incentive activity relatively restrained due to tariffs. J.D. Power estimates that average incentive spending per unit will total $3,105, down $7 from July 2025 and up by $38 year over year. It remains to be seen how incentive spending will change for the 2026 model year given that many OEMs are expected to increase prices to offset higher tariff costs.

-

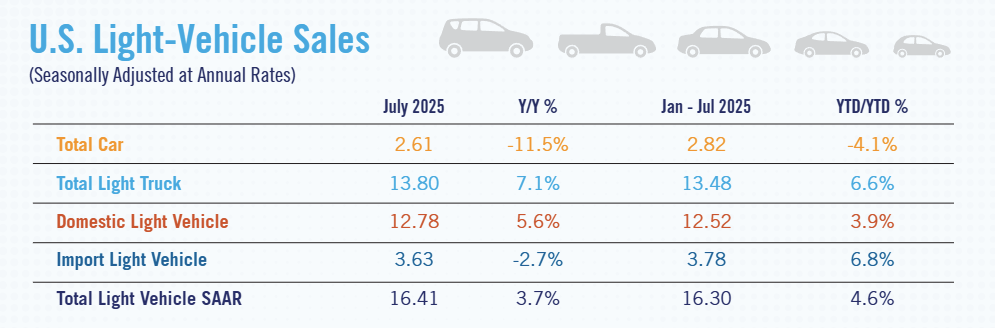

New light-vehicle sales in July 2025 were stronger than expected. July 2025’s SAAR totaled 16.4 million units, up 7.1% from June 2025’s SAAR and an increase of 3.7% year-over-year. July’s year-over-year comparison may have been larger, but July 2024’s results included sales that would have occurred in June 2024 were it not for the massive software outage that affected many dealerships across the country.

- With just a few months left before EV tax credits are set to expire, we expected to see increased activity in the EV space. While BEV sales in July 2025 increased by 22.7% compared to June 2025, sales were flat when compared to July 2024. The same is true for market share year-to-date for BEVs, which totaled 7.4%—also flat year-over year. Meanwhile, plug-in hybrids—some of which are also eligible for the EV tax credit—saw sales and market share decline slightly year-over-year. The most popular alternative-fuel segment continues to be hybrids, which posted a 37.7% year-over-year sales gain in July 2025. Year-to-date, hybrids have also picked up 3 percentage points of market share.

- According to J.D. Power, average incentive spending per unit should total $3,051 in July 2025, an increase of $273 compared to June 2025 and up $52 compared to a year ago. As vehicle prices have continued to rise, so too have monthly payments. According to J.D. Power, the average monthly payment on a new-vehicle finance contract is expected to reach $742, up $12 year-over-year. The average new-vehicle finance rate in July 2025 is also expected to be up year-over-year by 30 basis points to 6.54%.

- July’s sales results exceeded expectations. Despite this strong performance, one month is not enough to adjust our full-year sales forecast of 15.3 million units. J.D. Power estimates that tariffs are adding $4,275 in cost per vehicle on average. Many OEMs reported significant impacts to their bottom line due to tariffs. It remains to be seen how long OEMs can absorb the price hikes before passing the costs along to consumers. We expect to have more clarity on changing OEM pricing strategies in the fall as 2025 models transition to 2026 models.

-

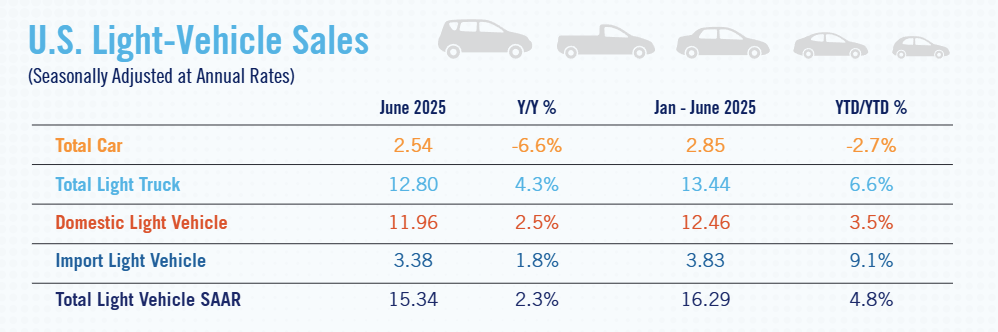

New light-vehicle sales in June 2025 totaled a SAAR of 15.3 million units. The June 2025 SAAR represents an increase of 2.3% compared to June 2024. Sales in June 2024 were impacted by a major dealership-software outage that limited sales a year ago, so the year-over-year increase appears stronger than it was. According to J.D. Power, roughly 173,000 sales were pulled ahead into March and April 2025 as consumers flocked to dealerships to purchase new vehicles before auto tariffs took effect. June 2025 sales results and sales in the coming months will likely be lower due to that pull-ahead volume. Without these tariff-induced pre-buy purchases, June 2025 sales results likely would have been closer to a 16.0 million-unit SAAR.

- Auto tariffs have caused vehicle-production shifts and disruptions. Because of these disruptions and the strong sales performance in March and April 2025, new light-vehicle inventory has fallen month-over-month recently. New light-vehicle inventory on the ground and in transit totaled 2.57 million units at the start of June, and total inventory levels are likely to be flat or down slightly once final data are available. Inventory hit a high this year in February at 2.78 million units, but it is unlikely we will see inventory that high again this year. According to Omdia (formerly Wards Intelligence), new light-vehicle inventory is forecast to decline to 2.3 million units by the end of August before rising back to roughly 2.5 million units by year-end.

- According to J.D. Power, average incentive spending per unit should total $2,727 in June 2025. As inventory becomes scarcer, we expect to see OEMs pull back on their incentive spending in coming months. J.D. Power also notes that the average monthly payment on a new-vehicle finance contract should total $747 in June 2025, up $22 year over year and the highest on record for the month of June.

- Looking ahead to the second half of the year, we will be closely watching the resilience of the American car buyer. Our outlook is for sales to decline in the second half of the year after the strong performance in the first half. We expect consumers may wait on the sidelines until there is more certainty with trade policy and its effects on new light-vehicle prices and vehicle availability. Overall, we expect lower North American new light-vehicle production, lower new-vehicle inventory levels and a slower sales pace compared to the first half of the year and compared to our pre-tariff expectations. Our forecast for new light-vehicle sales for all of 2025 is 15.3 million units.

-

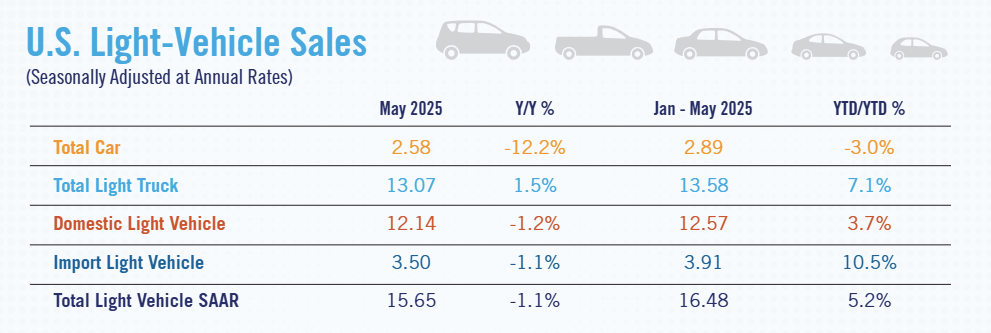

New light-vehicle sales slowed to a 15.7-million-unit SAAR in May 2025, following back-to-back months where the SAAR clocked in above 17 million units.

- The May sales results fell back in line with pre-tariff expectations. J.D. Power estimates an additional 149,000 vehicles were purchased in March and April 2025, as consumers pulled ahead purchases to avoid tariff-related price impacts. While it is likely there were still some pull-ahead sales in May 2025, it appears the pre-tariff surge in new-vehicle sales has ended. We expect such pull-ahead purchases will result in lower monthly sales later in the year.

- New-vehicle production has fallen slightly in the months following the vehicle tariff announcements. Those production declines—coupled with the strong sales pace in March and April 2025—represented the first year-over-year decline in new-vehicle inventory since June 2022. At the start of May 2025, the number of new light-duty vehicles on the ground and in transit to dealer lots was 2.62 million units, a decline of 4.1% year over year. New-vehicle inventory likely will cool even more once final May 2025 data are available. With solid vehicle demand and a tighter supply of new vehicles in May, OEMs have been under less pressure to incentivize sales with discounts. According to J.D. Power, average incentive spending per unit is expected to total $2,563 in May 2025, a decline of $200 compared to April 2025 and down $143 year-over-year.

- In the coming months, we expect all OEMs to be affected by the tariffs on imported vehicles and parts, although the cost impacts will be much greater for some OEMs than others. So far, each OEM has been taking its own strategy when dealing with the cost increases, but the burden of these increases will be borne by OEMs, dealers and consumers alike. Exactly how much each OEM will be affected remains to be seen as the higher costs work their way through the vehicle-supply chain. Our outlook for new light-vehicle sales in 2025 has been lowered to 15.3 million units.

-

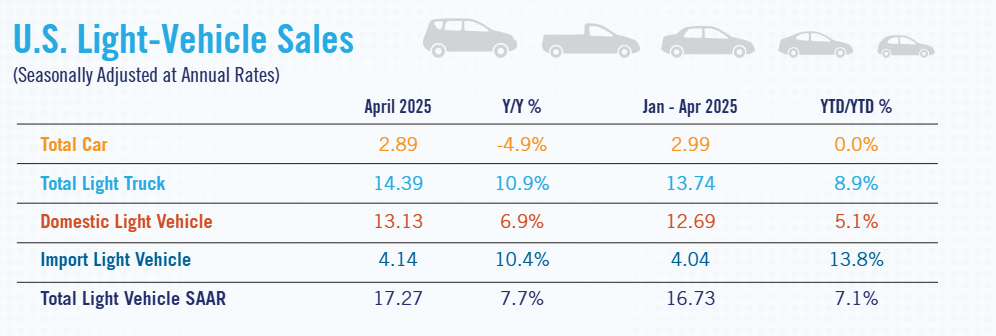

New light-vehicle sales in April 2025 topped a 17-million-unit SAAR for the second straight month as consumers pulled forward purchases to beat tariffs. April 2025’s SAAR of 17.3 million units represents an increase of 7.7% year over year.

- The SAAR for the first four months of the year totaled 16.7 million units at the end of April, up 7.1% compared to the same period last year.

- Wards Intelligence estimates that the March and April 2025 SAARs would have been closer to 16 million units were it not for the tariff-induced buying spree.

- New light-vehicle inventory on the ground and in transit declined year-over-year in April 2025 for the first time in three years. At the end of April 2025 new light-vehicle inventory totaled 2.62 million units, down 4.1% year-over-year.