Money and Credit

Money and Credit

- Source

- Bank of England

- Source Link

- https://www.bankofengland.co.uk/

- Frequency

- Monthly

- Next Release(s)

- May 1st, 2026 4:30 AM

-

June 2nd, 2026 4:30 AM

-

June 29th, 2026 4:30 AM

-

September 1st, 2026 4:30 AM

-

September 29th, 2026 4:30 AM

-

October 29th, 2026 4:30 AM

-

November 30th, 2026 4:30 AM

-

January 5th, 2027 4:30 AM

-

February 1st, 2027 4:30 AM

Latest Updates

-

Money and Credit: February 2026

-

Total lending to individuals in the UK increased 0.3% MoM, or £5.9 billion, in January, with the annual growth of lending at 4.0% YoY, matching the December pace.

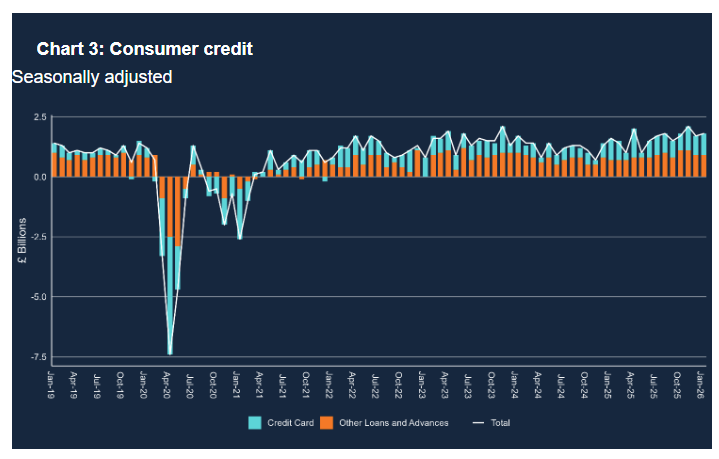

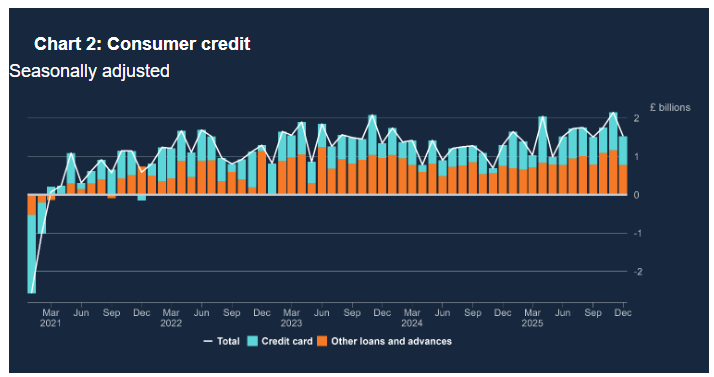

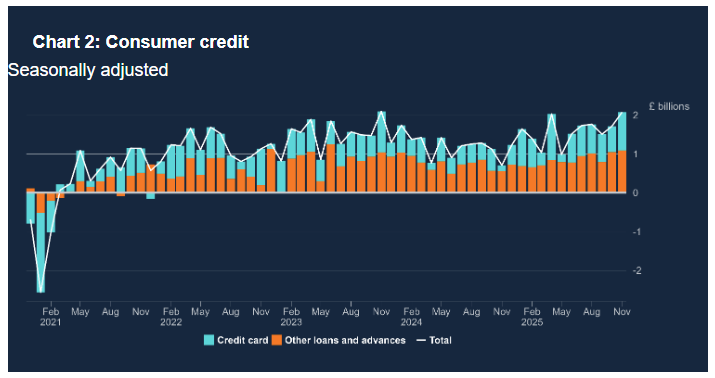

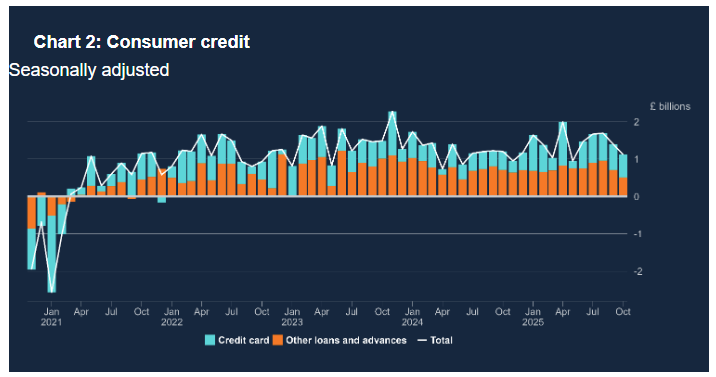

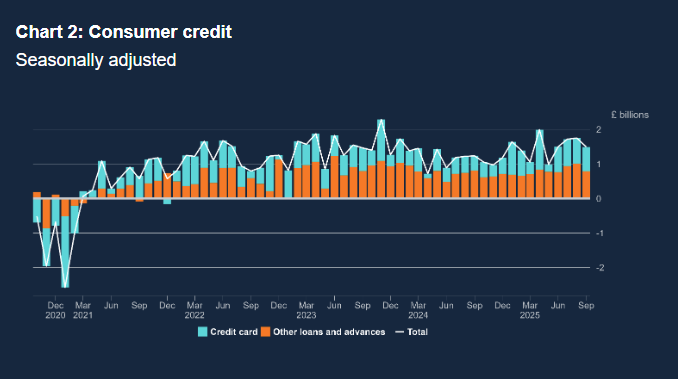

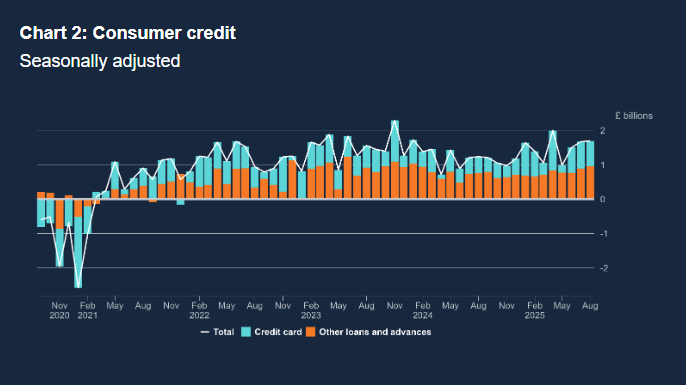

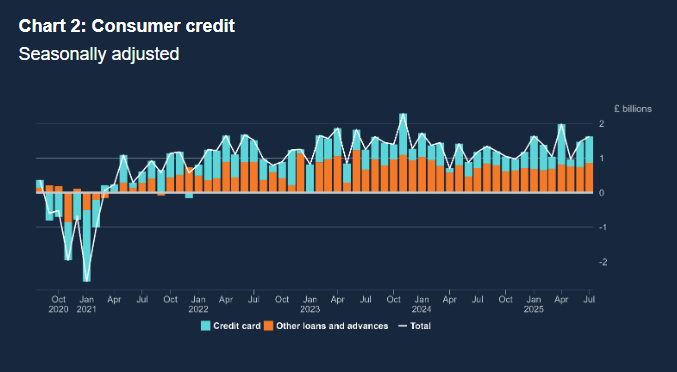

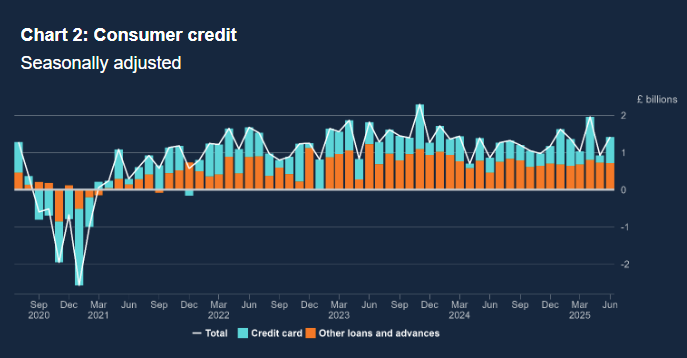

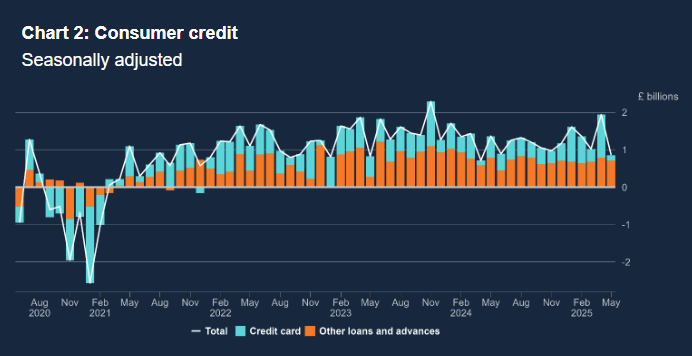

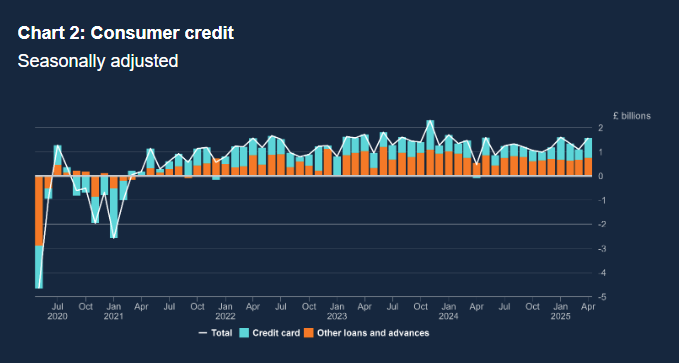

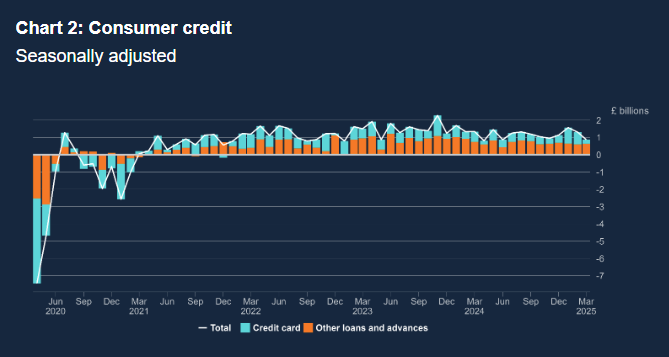

- Net consumer credit growth was 0.7% MoM, or £1.8 billion, in January, similar to the pace in December. YoY growth was 8.3% YoY, also matching the December pace.

- Net borrowing of mortgage debt by individuals decreased to £4.1 billion in January, from £4.5 billion in December, below the previous 6-month average of £4.5 billion.

- Net mortgage approvals for house purchases decreased to 60,000 in January, below an average of around 64,100 over the previous 6-months. Approvals for remortgaging decreased slightly to 38,100 in January from 38,400 in December.

- Net borrowing of consumer credit by individuals increased to £1.8 billion in January, from £1.7 billion in December, in line with the previous 6-month average of £1.8 billion. Within this, net borrowing through credit cards was £0.9 billion in January, up from £0.8 billion in December. Net borrowing through other forms of consumer credit (such as car dealership finance and personal loans) remained unchanged at £0.9 billion in January

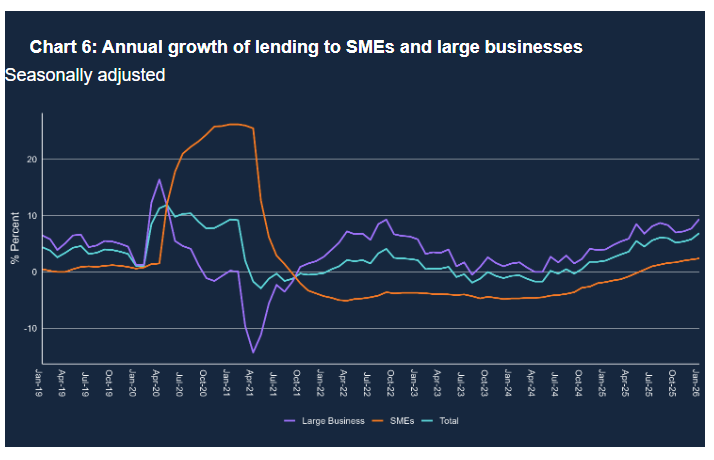

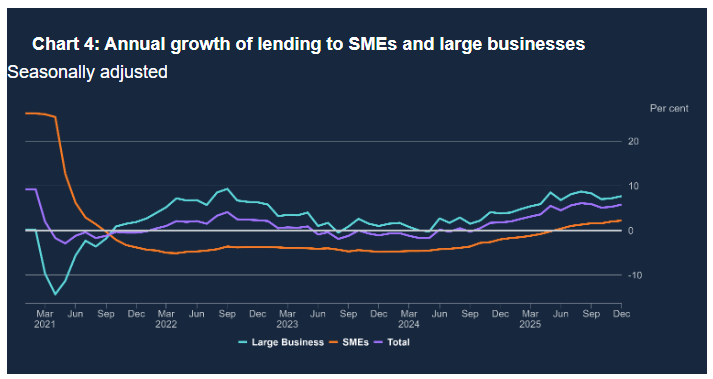

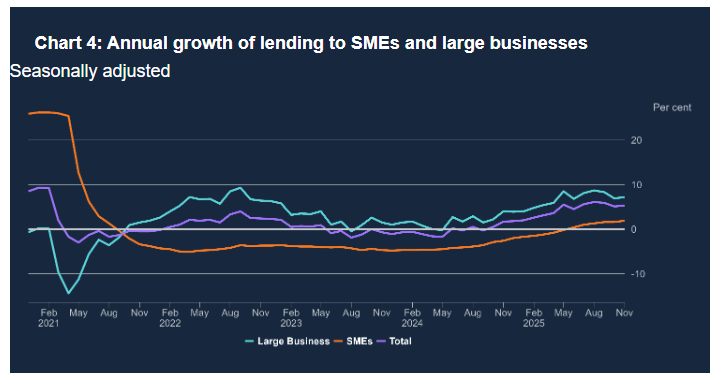

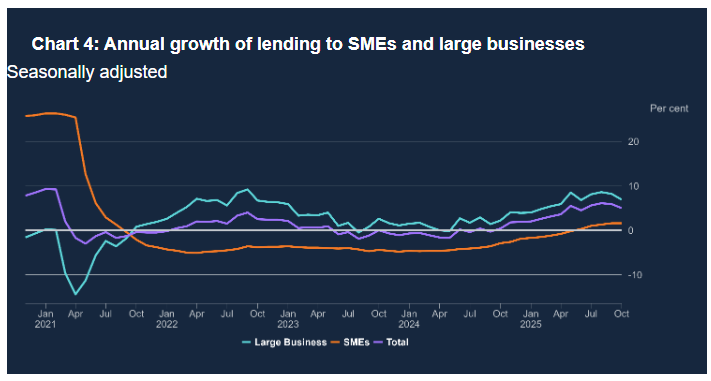

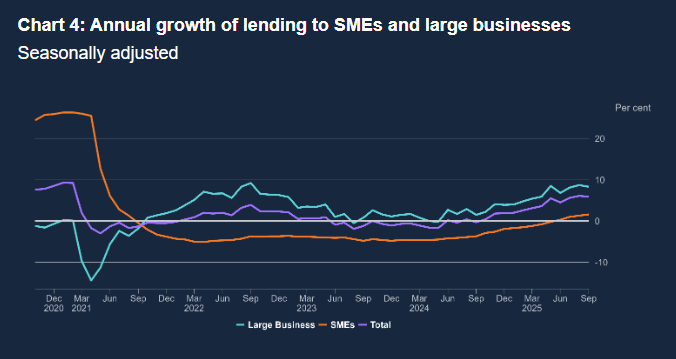

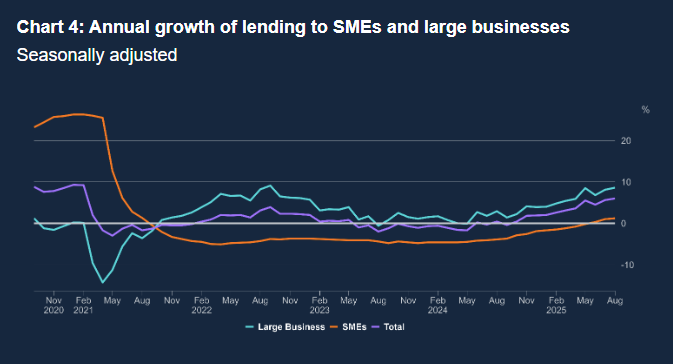

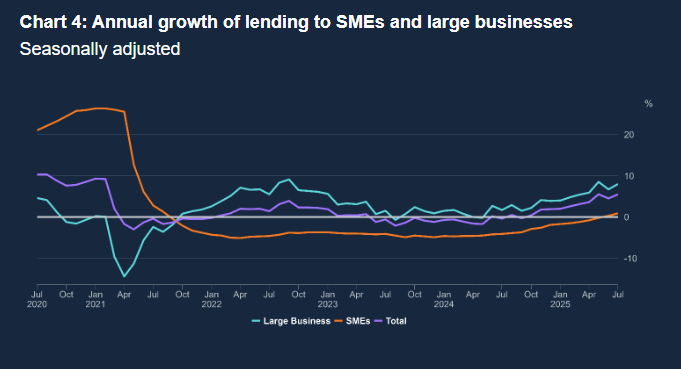

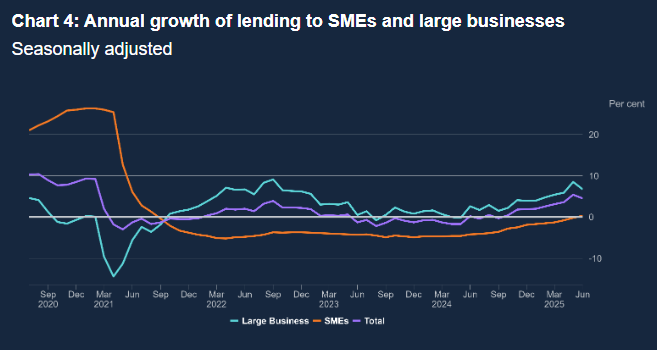

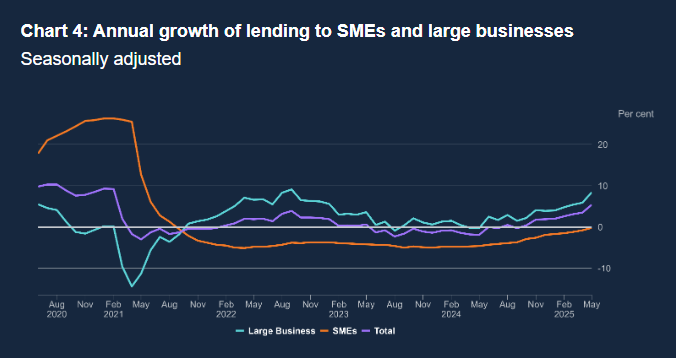

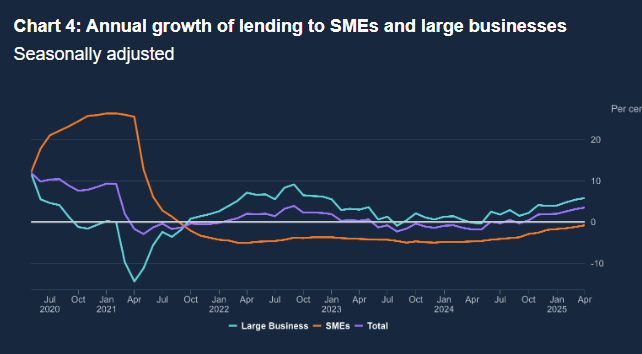

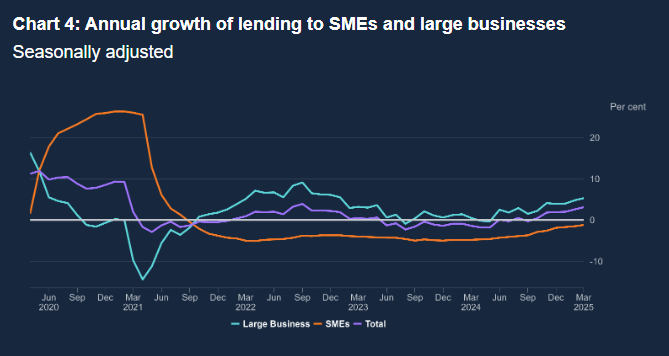

- Non-financial firm loan growth was 6.9% YoY in January, up from 5.8% YoY in December and the highest since February 2021. Large firms saw loan growth of 9.4% YoY (highest since May 2020), and small firms saw loan growth of 2.4% YoY (highest since July 2021).

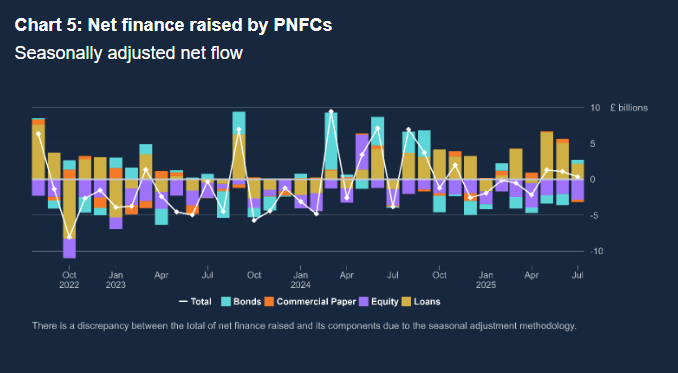

- Private non-financial corporations (PNFCs) borrowed, on net, £5.1 billion of finance in January, following net repayments of £1.2 billion in December. Within total net finance raised, bank loans amounted to £2.8 billion of borrowing in January, following £6.2 billion of net borrowing in December.

- The UK M4 money supply edged down -0.1% MoM, or -£3.9 billion, with annual growth slowing to 3.0% YoY in January, down significantly from 4.7% YoY in December.

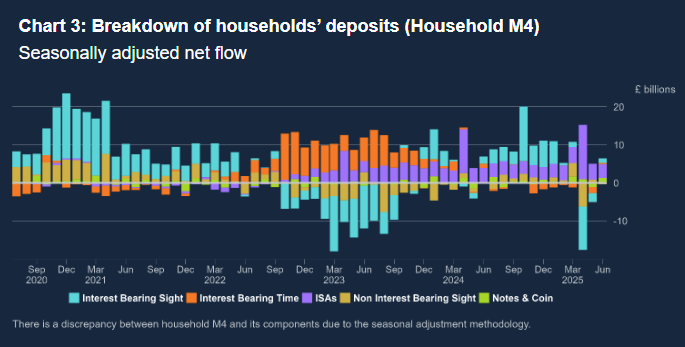

- The net flow of sterling money (M4ex) was -£7.1 billion in January, compared to £13.9 billion in December. This was largely driven by NIOFCs and PNFCs decreasing their holdings of money by £6.3 billion and £5.0 billion respectively. These decreases were partially offset by households increasing their holdings of money by £4.2 billion, within this households deposited £5.2 billion into ISAs, £3.1 billion into non-interest-bearing deposit accounts and £2.5 billion into interest-bearing sight deposit accounts.

- The flow of sterling net lending to private sector companies and households (M4Lex) was £10.5 billion in January, compared to £13.1 billion in December. January’s lending was driven by households, PNFCs, and NIOFCs borrowing £4.8 billion, £2.9 billion and £2.8 billion respectively, compared to borrowings of £5.5 billion, £5.1 billion and £2.5 billion respectively in December.

-

Total lending to individuals increased 0.3% MoM, or £6.1 billion, in December, with annual growth slowing slightly to 4.0% YoY (down from 4.1% YoY in November).

- Net consumer credit increased 0.6% MoM, or £1.5 billion, moderating from the strong increase in November. YoY growth was unchanged at 8.2% YoY.

- Net borrowing of mortgage debt by individuals remained unchanged when compared to November at £4.6 billion in December.

- In December, net mortgage approvals for house purchase fell by 3,100 to 61,000. By contrast, approvals for remortgaging rose by 1,600 to 38,400 in December.

- Net borrowing of consumer credit by individuals decreased to £1.5 billion in December from £2.1 billion in November. Within this, net borrowing through credit cards was £0.7 billion in December, down from £1.0 billion in November. Net borrowing through other forms of consumer credit (such as car dealership finance and personal loans) decreased in December, to £0.8 billion from £1.2 billion.

- Private non-financial corporations (PNFCs) repaid, on net, £1.4 billion to capital markets and banks and building societies in December, following net borrowing of £6.0 billion in November.

- The net flow of sterling money (known as M4ex) was £13.2 billion in December, compared to £16.7 billion in November. This was driven by households, non-intermediate other financial corporations (NIOFCs) and PNFCs increasing their holdings of money by £4.8 billion, £4.5 billion, and £3.8 billion respectively.

- The flow of sterling net lending to private sector companies and households (M4Lex) was £12.6 billion in December, compared to £16.1 billion in the previous month. December’s lending was driven by households, PNFCs and NIOFCs borrowing £5.5 billion, £4.7 billion, and £2.3 billion respectively.

-

Total net lending to individuals increased 0.3% MoM, or £6.6 billion, in November, with the annual growth increasing slightly to 4.1% YoY (up from 4.0% YoY in October).

- Net consumer credit increased 0.8% MoM, or £2.1 billion (vs £1.1 billion expected), which is the strongest monthly growth rate since April.

- Within this, net borrowing through credit cards was £1.0 billion in November, up from £0.7 billion in October. Net borrowing through other forms of consumer credit (such as car dealership finance and personal loans) slightly increased in November, to £1.1 billion from £1.0 billion.

- Net borrowing of mortgage debt by individuals increased to £4.5 billion in November, following a decrease of £1.0 billion to £4.2 billion in October.

- In November, net mortgage approvals for house purchase fell by 500 to 64,500. By contrast, approvals for remortgaging rose by 3,200 to 36,600 in November.

- Private non-financial corporations (PNFCs) borrowed, on net, £5.8 billion from capital markets and banks and building societies in November, following net repayments of £4.8 billion in October.

- PNFC loan growth accelerated from 5.1% YoY in October to 5.3% YoY in November. Large firm loan growth was 7.2% YoY (up from 6.9% YoY), and small firm loan growth was 1.9% YoY (up from 1.6% YoY), the strongest since July 2021.

- The broadest level of the M4 money supply increased 0.8% MoM (vs -0.1% MoM expected), or £24.4 billion, pushing the annual growth to 4.3% YoY in November, up from 3.5% YoY in October and the strongest since October 2022.

- The net flow of sterling money (known as M4ex) was £15.3 billion in November, compared to £8.8 billion in October, and the highest since January 2025 (£25.4 billion). This was largely driven by households and non-intermediate other financial corporations (NIOFCs) increasing their holdings of money by £8.1 billion and £6.1 billion respectively.

- The flow of sterling net lending to private sector companies and households (M4Lex) was £15.5bn in November, compared to £13.3 billion in the previous month. November’s lending was driven by NIOFCs, households, and PNFCs borrowing £5.9 billion, £5.5 billion, and £4.1 billion respectively.

-

Total net lending to individuals increased 0.3% MoM, or £5.4 billion, in October. The annual increase was unchanged from September, remaining at 3.7% YoY.

- Net consumer credit increased 0.5% MoM, or £1.1 billion (vs £1.35 billion expected), the lowest monthly increase since May. The annual growth of credit was unchanged at 7.2% YoY.

- Within consumer credit growth, net borrowing through credit cards slightly decreased, to £0.6 billion from £0.7 billion. Net borrowing through other forms of consumer credit was £0.5 billion in October, down from £0.7 billion in September.

- Net borrowing of mortgage debt by individuals fell back to £4.3 billion in October, after a rise to £5.2 billion in September.

- In October, net mortgage approvals for house purchase decreased by 600 to 65,000, while approvals for remortgaging fell by 3,600 to 33,100, the lowest since February 2025 (32,900).

- Private non-financial corporations (PNFCs) repaid, on net, £4.8 billion of finance in October, the highest level of net repayments since October 2023 (£5.5 billion).

- PNFC loan growth was 5.0% YoY in October, down from 5.9% YoY in September and the lowest since June. Large firm loan growth was 6.9% YoY (down from 8.2% YoY in September), and small firm loan growth was 1.6% YoY (unchanged from September).

- The broadest level of M4 money supply fell -£7.3 billion, or -0.2% MoM (vs +0.4% MoM expected) in October, the largest decline since September 2023. The annual rate of growth slowed from 3.7% YoY in September to 3.5% YoY.

- The net flow of sterling money (known as M4ex) was £8.5 billion in October, compared to £14.2 billion in September. This was largely driven by households increasing their holdings of money by £6.8 billion in October, with households depositing an additional £5.5 billion into interest-bearing sight deposit accounts, £4.2 billion into ISAs, and £0.3 billion into interest-bearing time deposit accounts.

- The flow of sterling net lending to private sector companies and households (M4Lex) was £13.0 billion in October, compared to £19.6 billion in September. October’s lending was driven by NIOFCs and households borrowing £8.2 billion and £4.7 billion respectively, while net borrowing by PNFCs was zero.

-

Total lending to individuals increased 0.4% MoM or £7.0 billion in September. The annual growth in lending to individuals accelerated to 3.7% YoY, the highest since January 2023.

- Net borrowing of mortgage debt by individuals rose by £1.2 billion to £5.5 billion in September, the highest since March 2025 (£13.2 billion).

- Net mortgage approvals for house purchase increased by 1,000, to 65,900 in September. By contrast, approvals for remortgaging decreased by 600 over the same period, to 37,200.

- Net borrowing of consumer credit by individuals was £1.5 billion (+0.6% MoM) in September, down from £1.7 billion in August. Within this, net borrowing through credit cards was little changed at £0.7 billion in September. Net borrowing through other forms of consumer credit decreased to £0.8 billion, from £1.0 billion over the same period.

- Private non-financial corporations (PNFCs) raised, on net, £0.2 billion of finance in September, following net borrowing of £6.2 billion in the previous month.

- The annual growth rate of borrowing by large businesses was 8.3% in September, down from 8.7% in August. The annual growth rate of borrowing by SMEs increased to 1.6% from 1.3% over the same period.

- The net flow of sterling money (known as M4ex) was £13.7 billion in September, compared to £11.2 billion in August. This was largely driven by households increasing their holdings of money by £7.9 billion in September, with households depositing an additional £5.8 billion into interest-bearing sight deposit accounts, £2.4 billion into ISAs, and £0.7 billion into non-interest-bearing accounts.

- The flow of sterling net lending to private sector companies and households (M4Lex) was £19.5 billion in September, compared to £10.2 billion in August. September’s lending was driven by increases of £11.1 billion, £5.3 billion, and £3.1 billion in the flow of net lending to NIOFCs, households, and PNFCs respectively.

-

Consumer credit borrowing was £1.69 billion (+0.7% MoM) in August, roughly the same as £1.67 billion in July and in line with expectations of borrowing of £1.6 billion. The annual increase was 7.1% YoY, the strongest since October 2024.

- Total lending to individuals was £6.0 billion, or an increase of 0.3% MoM. On an annual basis, total lending was up 3.5%, the highest since February 2023.

- Net borrowing of mortgage debt was up slightly to £4.3 billion, up 0.3% MoM and 3.5% YoY. Net mortgage approvals for house purchases decreased by 500 in August, to 64,700. Approvals for remortgaging decreased by 900, to 37,900.

- Total loans to non-financial firms in August was £3.2 billion, up 6.0% YoY (strongest since February 2021), with loans to large businesses up 8.6% YoY (prev 8.1% YoY) and loans to small businesses up 1.2% YoY (up from 1.0% YoY).

- The M4 money supply increased £12.8 billion, or 0.4% MoM (vs 0.2% MoM expected), in August, and the annual rate was 3.4% YoY (the highest since May 2025).

- The net flow of sterling money (M4ex) was £10.9 billion (+0.4% MoM) in August, compared to £6.7 billion in July. Within this, households increased their holdings of money by £5.4 billion and NIOFCs increased theirs by £5.0 billion. Additionally, PNFCs also increased their holdings of money by £0.6 billion.

- The flow of sterling net lending to private sector companies and households (M4Lex) was £10.0 billion (+0.4% MoM) in August, compared to £7.8 billion in July. This was driven by increases of £4.7 billion, £3.5 billion, and £1.8 billion in net lending to households, PNFCs, and NIOFCs, respectively.

-

Consumer credit borrowing increased £1.6 billion, or 0.7% MoM, in July (up from £1.5 billion in June), with the annual rate accelerating from 6.8% YoY in June to 7.0% YoY in July, the strongest since October 2024.

- Total lending to individuals in July was £6.1 billion, or an increase of 0.3% MoM. On an annual basis, total lending is up 3.4% YoY, the highest since February 2023.

- UK net mortgage borrowing fell to £4.5 billion in July 2025 (from £5.4 billion in June), with an annual increase of 2.9% YoY, the strongest since February 2023.

-

Mortgage approvals for house purchases rose slightly to 65.4k (+800 MoM), while remortgaging approvals fell to 38.9k (-2.7k MoM).

-

Total loans to non-financial firms in July was £5.0 billion, and loan growth jumped to 5.5% YoY, the highest since February 2021.

-

Large businesses’ borrowing growth rose to 8.0% YoY (up from 6.7% YoY), while SME borrowing growth picked up to 0.9% YoY (up from 0.3% YoY), the strongest since August 2021.

-

PNFCs raised £0.3 billion net finance, as loan and bond inflows were offset by equity buybacks and commercial paper redemptions.

-

The M4 money supply increased £3.6 billion in July (or 0.1% MoM) with the annual increase slowly accelerating to 2.9% YoY (from 2.7% YoY).

-

The net flow of sterling money (M4ex) slowed to £7.1 billion (vs £11.4 billion in June), while net private sector lending (M4Lex) dropped to £7.7 billion (vs £19.9 billion).

-

UK consumer credit rose £1.4 billion, or 0.6% MoM, in June, up from £0.9 billion in May, with annual growth accelerating to 6.7% YoY from 6.5% YoY (strongest since October 2024).

- Credit card borrowing surged to £0.7 billion (from £0.2 billion), while other forms of credit held steady at £0.7 billion.

- The effective rate on new personal loans fell -30 bps to 8.42%, and credit card rates dipped 5 bps to 21.49%.

- Net mortgage borrowing by individuals rose to £5.3 billion in June (vs £2.2 billion in May), pushing the annual mortgage lending growth rate up to 2.8% from 2.6% (strongest since February 2023).

- Mortgage approvals for house purchases rose to 64,200, and remortgaging approvals hit 41,800, the highest since Oct 2022.

- The effective interest rate on new mortgages fell for the fourth straight month to 4.34%.

- PNFCs raised £0.98 billion in net finance, with loan inflows offset by £3.5 billion in bond/equity redemptions.

- Overall, net lending to non-financial firms was -£2.47 billion after over £8.62 billion in net lending in May.

- Large businesses repaid £2.84 billion in loans (vs £8.3 billion borrowed in May); SME borrowing was flat MoM but returned to positive YoY growth for the first time since 2021.

- PNFC deposit growth slowed to £2.3 billion (vs £4.8 billion in May); effective deposit rates ticked lower.

- The overall level of M4 money supply increased 0.3% MoM, or £8.25 billion, the strongest monthly rate since January 2025.

- The M4 money supply (M4ex) rose £11.3 billion in June (vs £5.6 billion in May), while M4Lex lending surged to £18.9 billion, the highest since Sept 2022.

- Household M4 rose £7.8 billion, driven by £3.6 billion in ISAs and £1.2 billion in sight deposits.

- Net lending gains were led by NIOFCs (£10.3 billion), followed by households (£5.0 billion) and PNFCs (£3.5 billion).

-

UK consumer credit growth slowed to £0.86 billion, or 0.4% MoM, in May, down from £1.94 billion in April. The annual increase slowed to 6.5% YoY, from 6.7% YoY.

- Net borrowing of mortgage debt by individuals rose to £2.1 billion in May (vs £2.5 billion expected), reversing the sharp contraction in April. The annual growth rate for net mortgage lending increased slightly from 2.5% to 2.6% in May.

- The ‘effective’ interest rate – the actual interest paid – on newly drawn mortgages decreased to 4.47% in May from 4.49% in April.

- PNFCs borrowed £1.0 billion net, with £6.1 billion in loan inflows offset by equity buybacks and bond redemptions.

- Loans to non-financial firms were up 5.4% YoY, the highest since February 2021, with loans to large firms up 8.4% YoY (highest since September 2022) and loans to small firms down -0.2% YoY (weakest contraction since August 2021).

- The M4 money supply increased 0.2% MoM (vs 0.2% MoM expected) and 3.5% YoY in May, up from 3.2% YoY in April.

- M4ex rose £5.2 billion and 0.2% MoM, led by increases in household and NIOFC holdings; PNFC money holdings fell by -£3.8 billion, or -0.7% MoM.

-

Consumer credit rose £1.6 billion (vs £1.1 billion expected), or 0.7% MoM, in April, driven by credit card borrowing doubling to £0.8 billion. On an annual basis, consumer credit growth accelerated to 6.7% YoY, the highest since October 2024.

- UK mortgage lending fell sharply by -£13.7 billion to -£0.76 billion in April, the first net repayment since November 2023, following a surge in March.

- Mortgage approvals for house purchases declined by -3,100 to 60,500, the fourth consecutive monthly drop, while remortgaging approvals rose to 35,300.

- Total lending to individuals was flat on a monthly basis, the weakest since a -0.1% MoM decline in July 2021, as a decline in mortgage lending offset a rise in consumer credit.

- Total lending to non-financial businesses was £1.2 billion in April, up 3.5% YoY or the strongest annual increase since September 2022.

- Lending to large PNFCs was up 5.8% YoY, the highest since December 2022, and lending to smaller PNFCs was only down -0.8% YoY, the smallest decline since September 2021.

- PNFCs repaid -£2.4 billion in finance, led by equity buybacks and bond redemptions, while their deposits fell by -£7.0 billion.

- Households deposited +£3.0 billion in April, with £14.0 billion flowing into ISAs—an all-time high—offset by large outflows from sight accounts.

- The M4 money supply was flat MoM in April, below expectations of an 0.2% MoM increase, and was up 3.2% YoY, a slight deceleration from 3.4% YoY in March.

- M4ex money supply increased +£6.2 billion MoM, slowing from March’s +£12.7 billion, while the flow of sterling net lending (M4Lex) dropped to just +£1.2 billion from +£17.0 billion.

- The M4Lex to private sector companies and households was up 0.4% MoM and flat MoM, respectively. On an annual basis, M4Lex to PNFCs was up 4.2% YoY, the highest since February 2021.

-

UK consumer credit increased just £0.88 billion, or 0.4% MoM, in March, down from £1.31 billion in January and below expectations of a £1.2 billion increase. On an annual basis, consumer credit is up 6.1% YoY (prev 6.4% YoY).

- Within this, net borrowing through credit cards decreased to £0.2 billion in March, the lowest since April 2024.

- Net borrowing of mortgage debt by individuals increased sharply by £9.7 billion to £13.0 billion in March, the highest since June 2021.

- Total lending to individuals was £13.8 billion, or an increase of 0.7% MoM, well above expectations of lending totaling £4.4 billion and the highest since June 2021.

- Net lending to private, non-financial businesses (PNFCs) declined by -£1.5 billion. However, total YoY loan growth accelerated to 3.9% YoY, the highest since September 2022.

- The M4 money supply increased 0.3% MoM (vs 0.2% MoM expected) and was up 3.4% YoY in March, down from 3.9% YoY in February.

- The M4 money supply for households was up 0.4% MoM and 5.3% YoY, and the M4 money supply for PNFCs increased 1.0% MoM and 2.6% YoY, the strongest annual increase since September 2022.