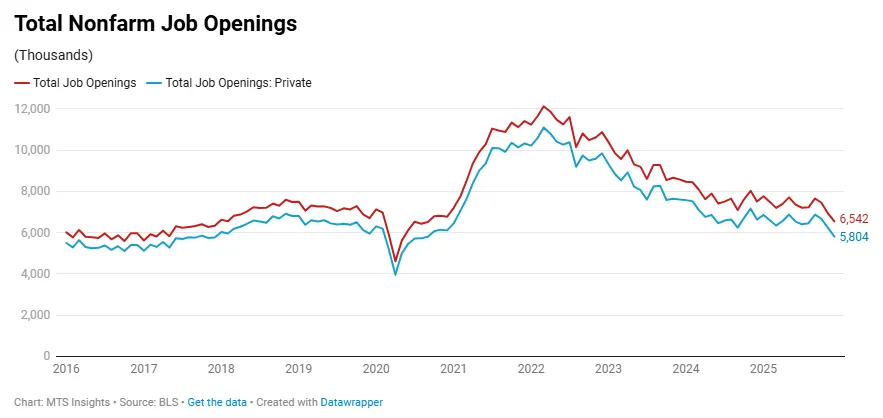

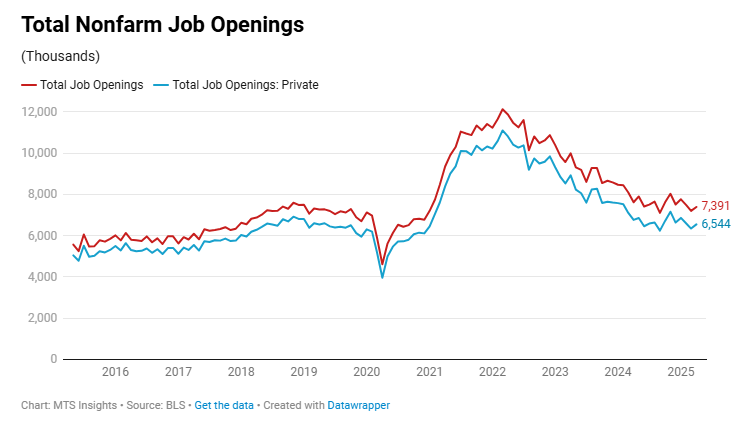

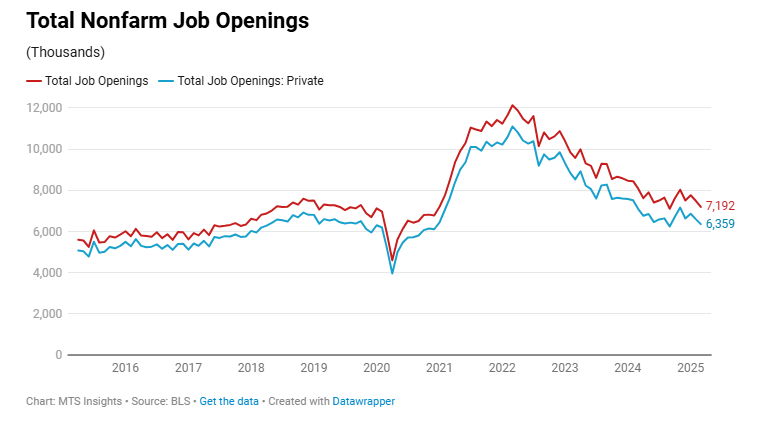

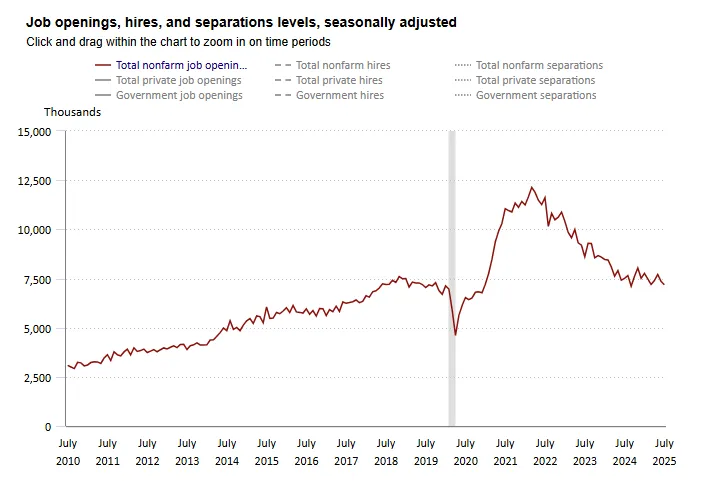

Job Openings

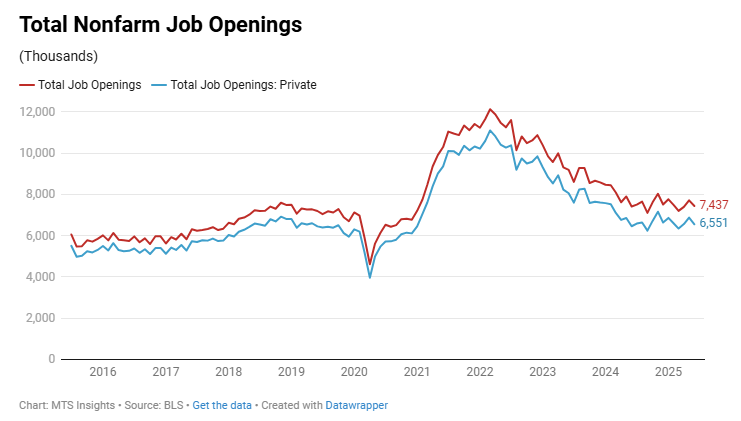

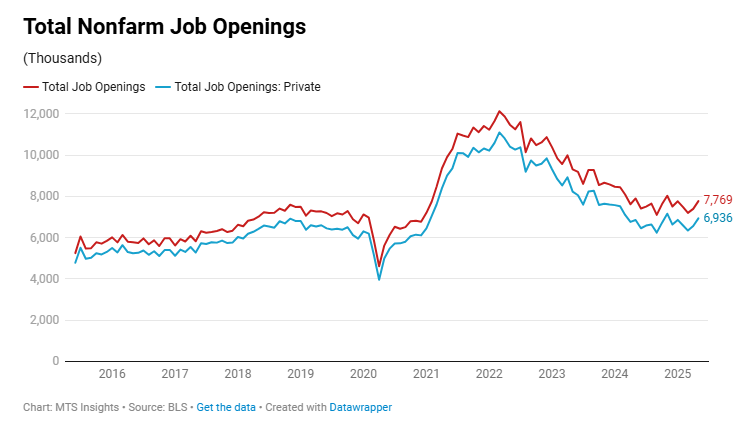

The data released this morning in the BLS’s JOLTS survey pointed to a continuation of the gradual decline in hiring demand in the labor market. In July, the total number of job openings fell -176k to 7.18 million, well below the expectations of a slight increase to 7.40 million. The job openings rate also declined, dropping from 4.4% in June to 4.3% in July. This decline in openings at the beginning of Q2 brings the overall level down to its lowest point since September 2024 and the 2nd lowest since December 2020. In these headline data points, we see clear evidence of weaker labor demand.

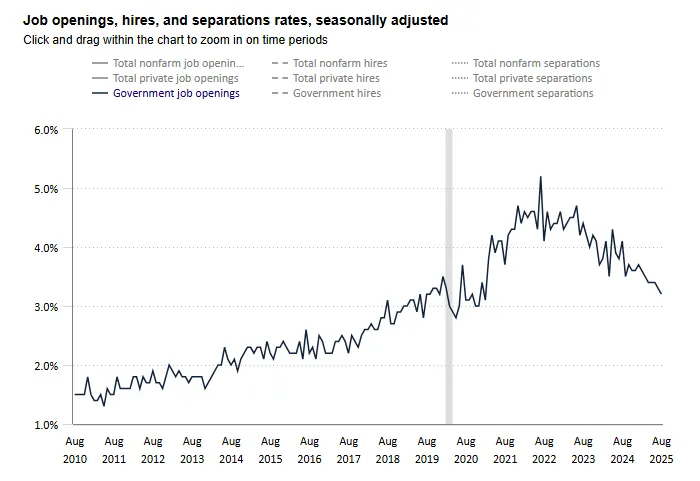

The data for private sector openings saw a similar trend. Total private openings were down -138k to 6.40 million, and the openings rate was down -0.1 ppts to 4.5%. These data points were consistent with lows seen in March of this year and September 2025. The largest declines in the industry details for job openings rates were in retail trade (-0.7 ppts to 3.2%) and health care & social assistance (-0.7 ppts to 5.1%), and the smaller arts & recreation industry saw a sharp -2.1 ppts decline to a rate of just 3.8%. Government job openings also declined, down -38k to 783k, with the rate falling to just 3.2% in July, down from 3.7% in January 2025 and the lowest since February 2021.

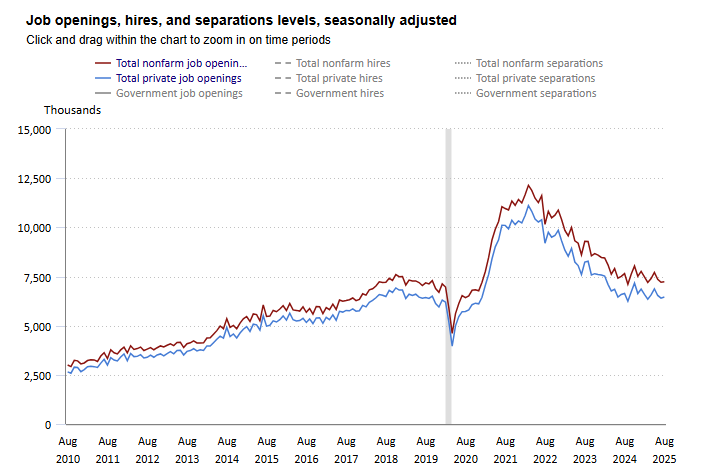

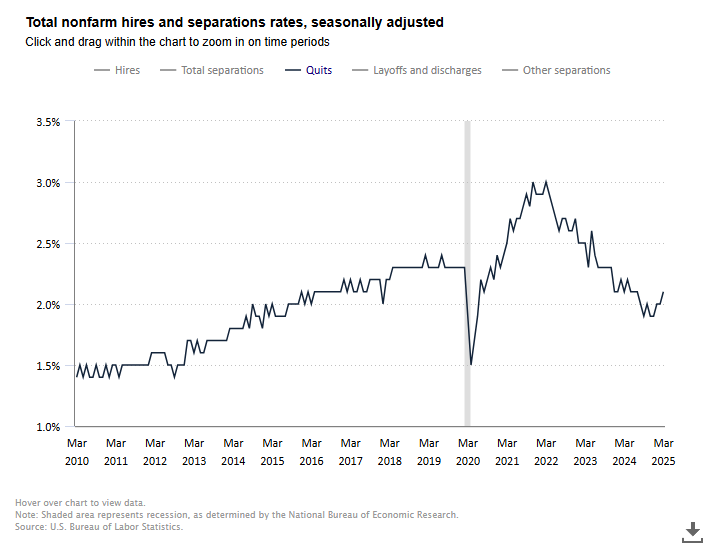

Hires and Separations

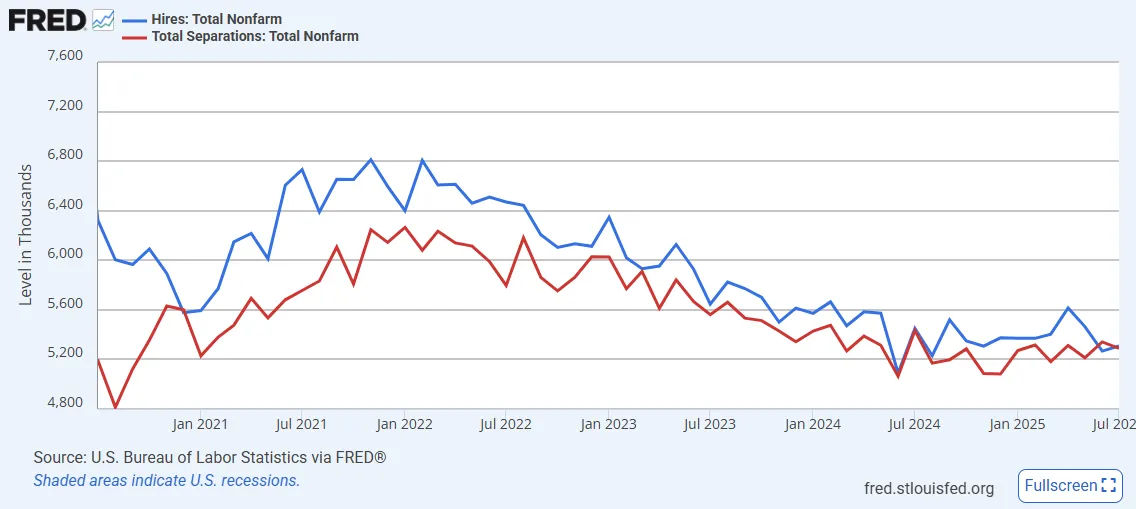

A feature of the recent cooling in the labor market is that both hires and separations have slowed together. This has created what Fed Chair Powell in his Jackson Hole speech called “a curious kind of balance” in the labor market where there is a “slowing in both the supply of and demand for workers.” Indeed, in July, both hires and separations saw little movement with the former up 41k and the latter down -52k. The rates for both hires and separations remained unchanged at 3.3%, and the levels of both are down around -140k from a year ago. The private sector data is very similar with both private hires and separations down around -80k to -90k over the last year.

Within separations, there wasn’t a significant change in the number of quits or layoffs. Total quits fell just -1k to 3.21 million, and the quits rate remained unchanged at 2.0% for the fourth straight month. The most significant move in quits is in the private sector over the last year where the quits rate has fallen slowly from 2.4% in July 2024 to 2.2% in July 2025. The total number of layoffs & discharges increased just 12k to 1.81 million, with private layoffs & discharges up just 14k. Over the last year, the increase in the private layoffs & discharges rate has only increased 0.1 ppts to 1.3%.

Overall, the data describes a labor market where firms are reluctant to expand hiring but at the same time aren’t increasingly laying off employees. The trend of stagnation in private sector hiring paired with the Trump administration’s efforts to shrink the government through hiring freezes, contract cancellations, and workforce reductions has caused the softening in the labor market to be a little harsher than if the public sector were more expansionary.

Revisions

Revisions to the July jobs report were the focus when that data was released early last month. Are there any revisions worth looking at in the July JOLTS report? Here’s what the BLS reported:

- The job openings total for June was revised down by -80k. The June revision is an adjustment of -1.1% which is just under one standard deviation away from the average revision of 0.4%. Notably, private sector job openings in June were only revised down by -15k.

- The total for hires in June was revised up by 63k, an adjustment of +1.2%. This is slightly above the average revision of +0.6%. Private hires in June were revised up 72k.

- The total for separations in June saw a sharp upward revision of 281k. This adjustment of +5.6% is more than two standard deviations above the mean revision of +0.7%. Private separations saw a similar, unusual upward revision.

- The upward revision in separations came from record upward revisions to layoffs & discharges in June. Specifically, total layoffs & discharges were revised up 192k (or +12.0%), and private layoffs & discharges were revised up 174 (or 11.3%). These adjustments were both record highs based on data going back to 2016.

- Looking specifically at government data, revisions to June data suggested much weaker hiring trends at the end of Q2 2025. Job openings were revised down -65k (or -7.3%), hires were revised down -11k (or -3.2%), and layoffs/discharges were revised up 18k (or +29.5%).

Overall, taken together with the July data, the revisions reframe the June data as weaker, but not nearly to the degree of the revisions to the July employment data. The record revisions to the layoffs & discharges numbers are particularly significant and will likely be a factor in the Fed’s deliberations later this month.

JOLTS Survey

JOLTS Survey