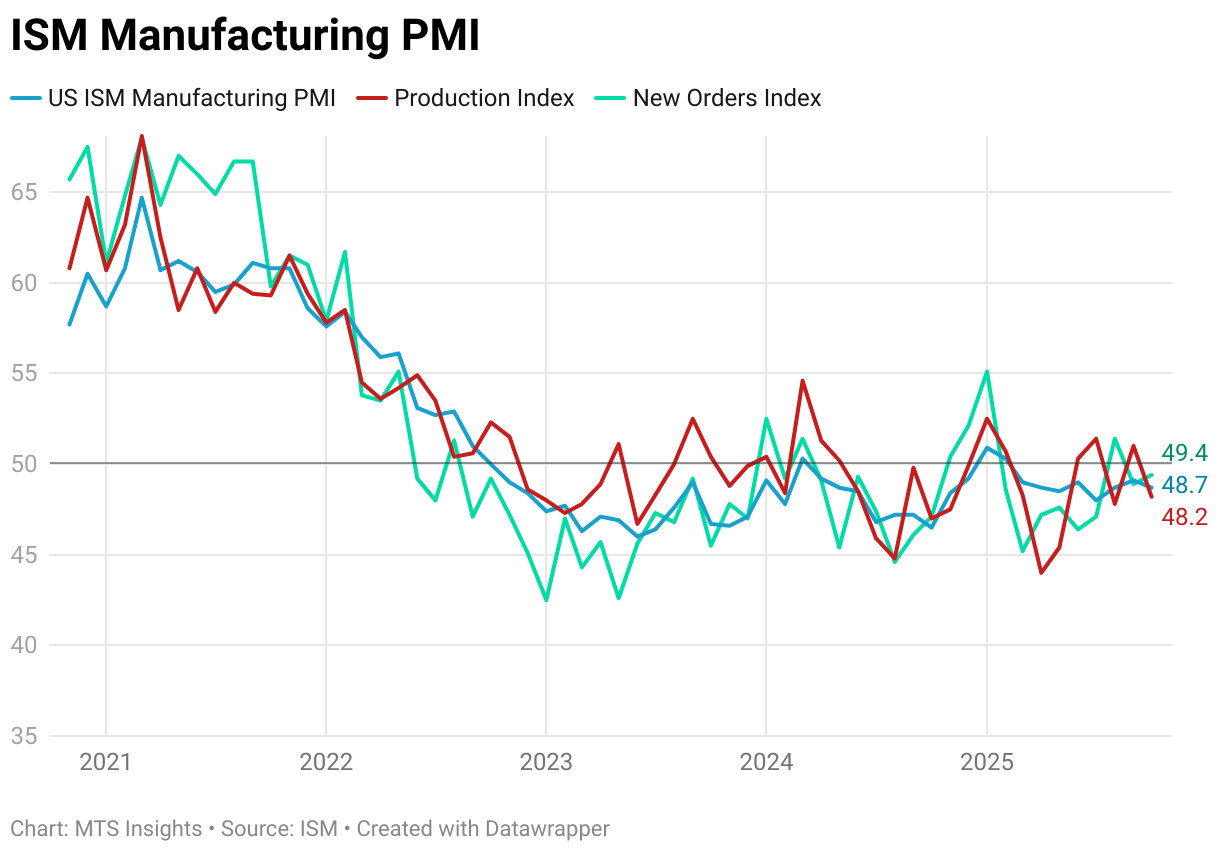

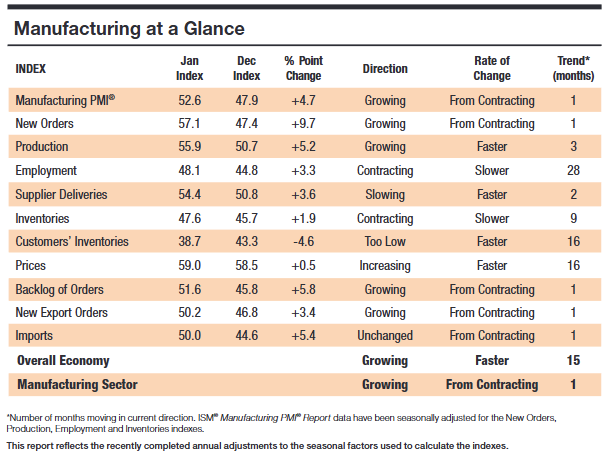

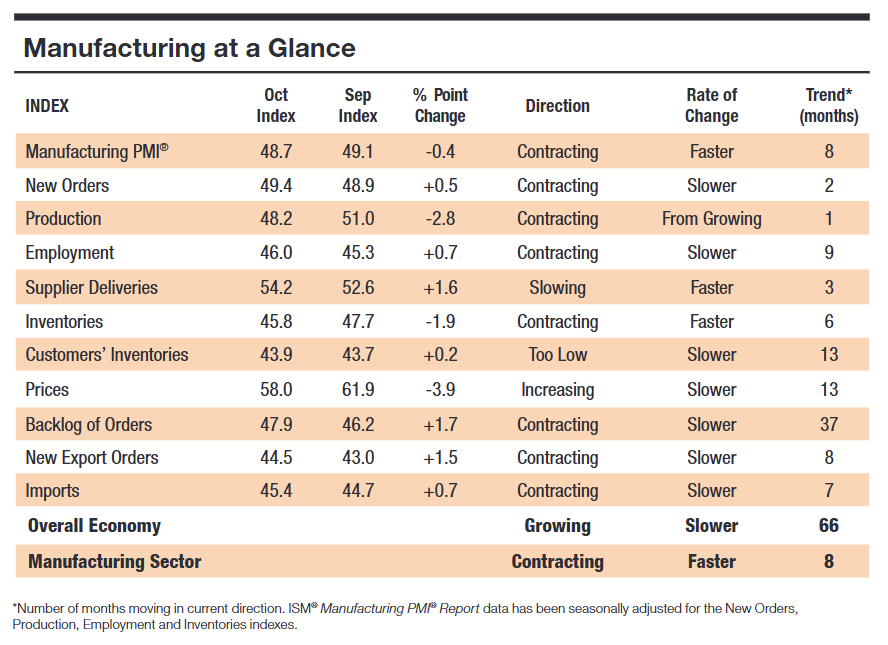

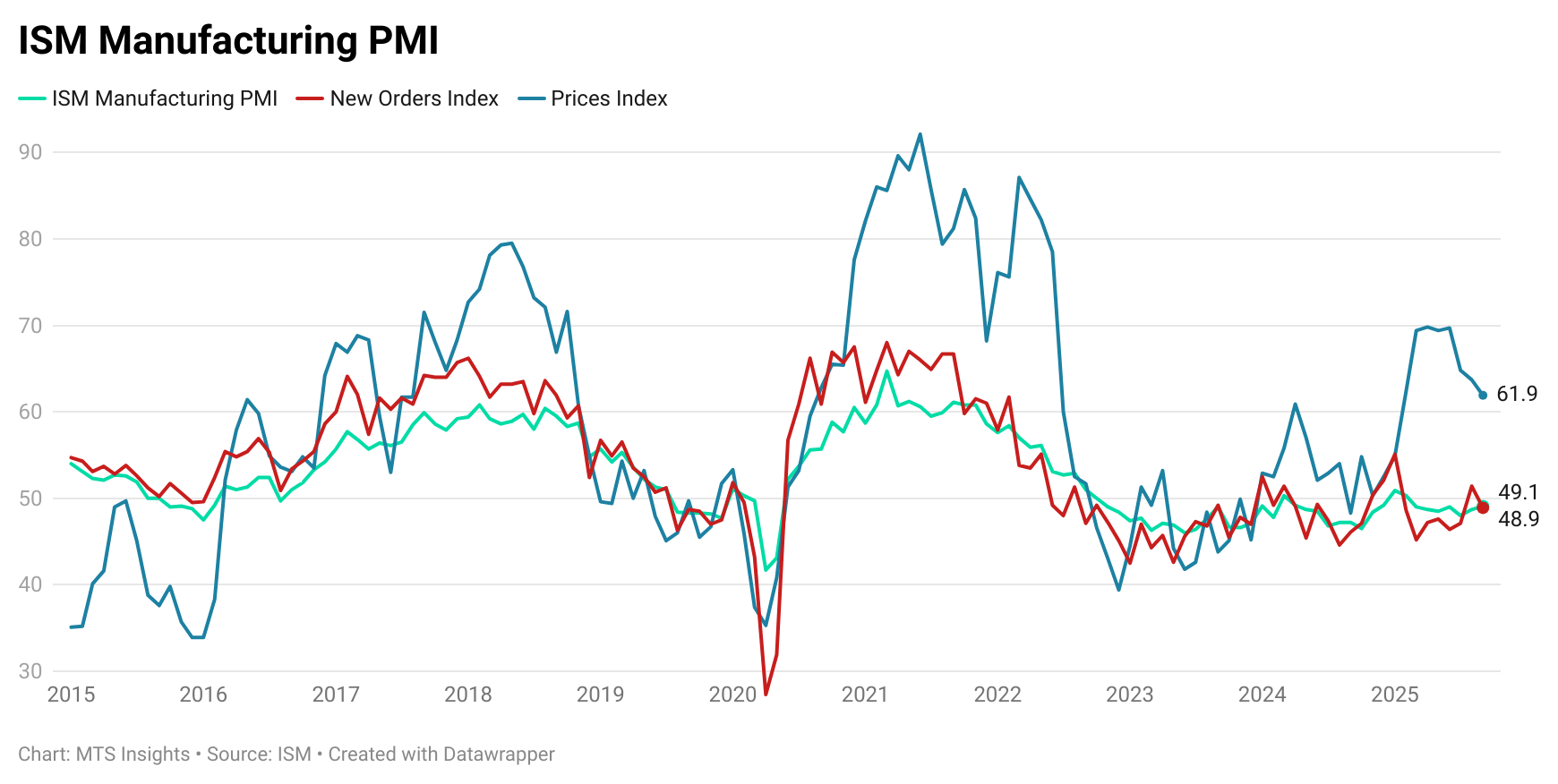

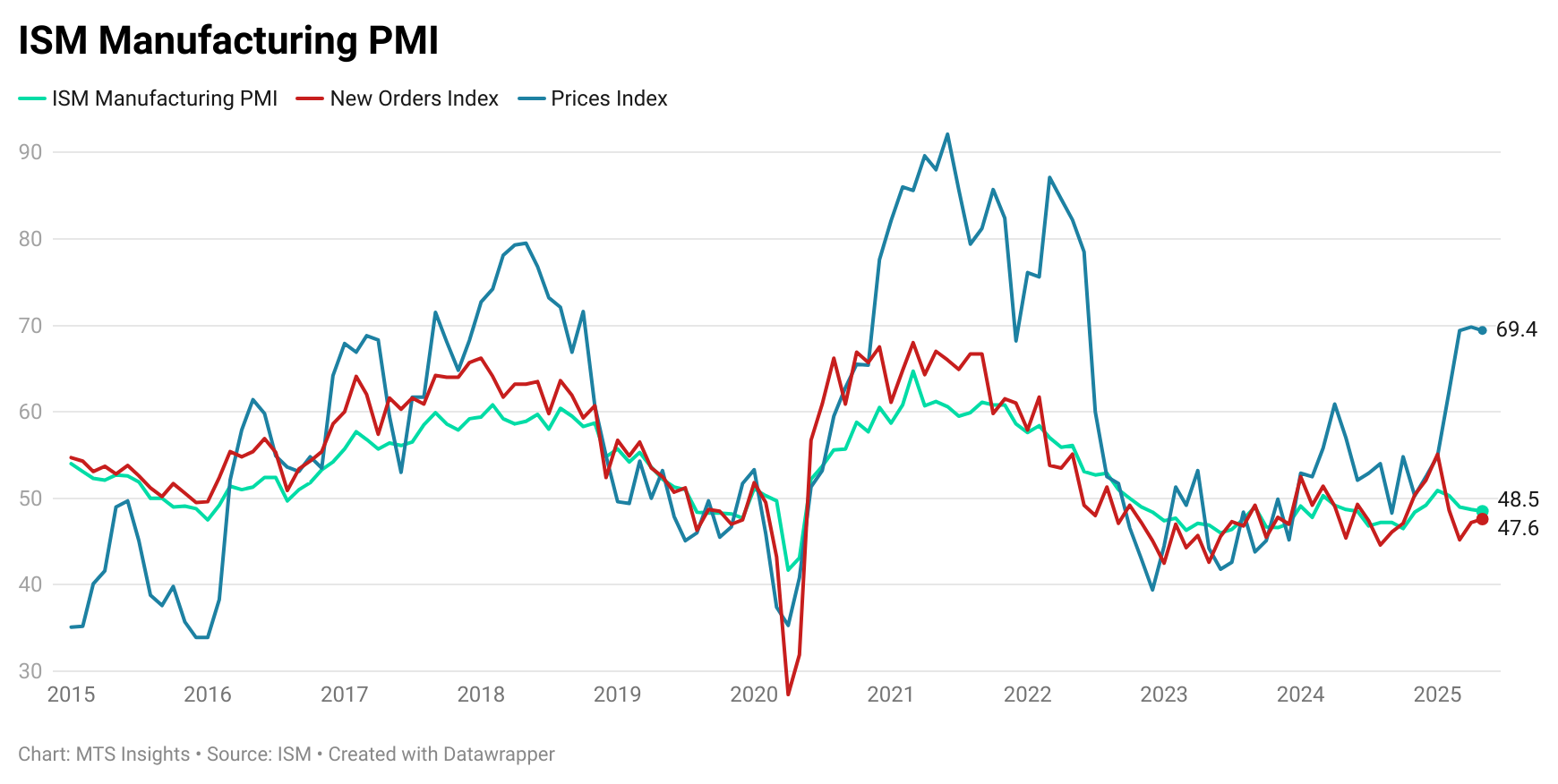

The ISM Manufacturing PMI presented a more negative view of the US manufacturing sector in August. The headline index increased 0.7 pts but remained in contraction territory for the 6th straight month at 48.7. This was slightly below consensus expectations of 49.0. Like the S&P data, the ISM data pointed to a sector heavily impacted by tariffs, with diverging performance between local and foreign markets.

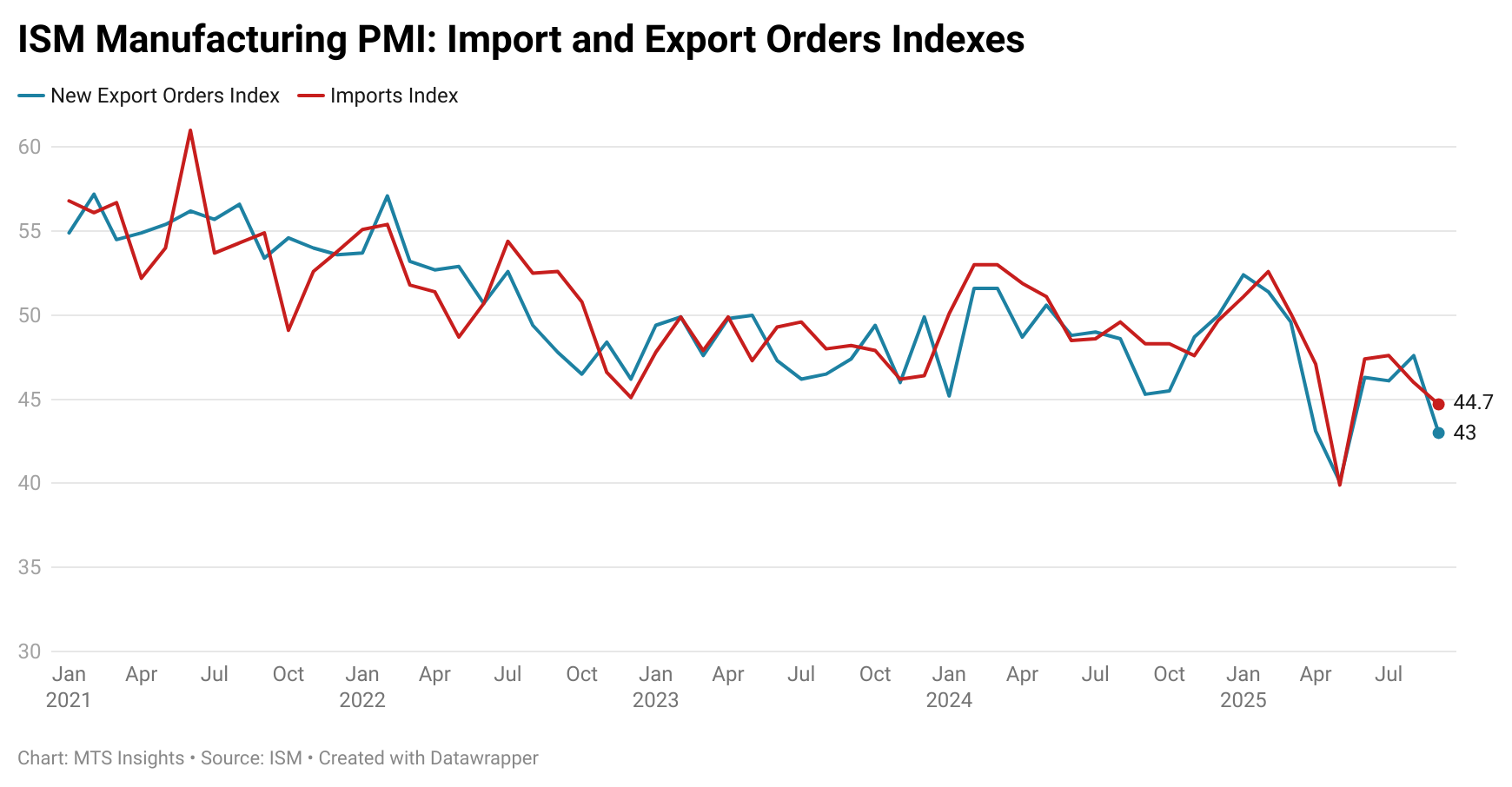

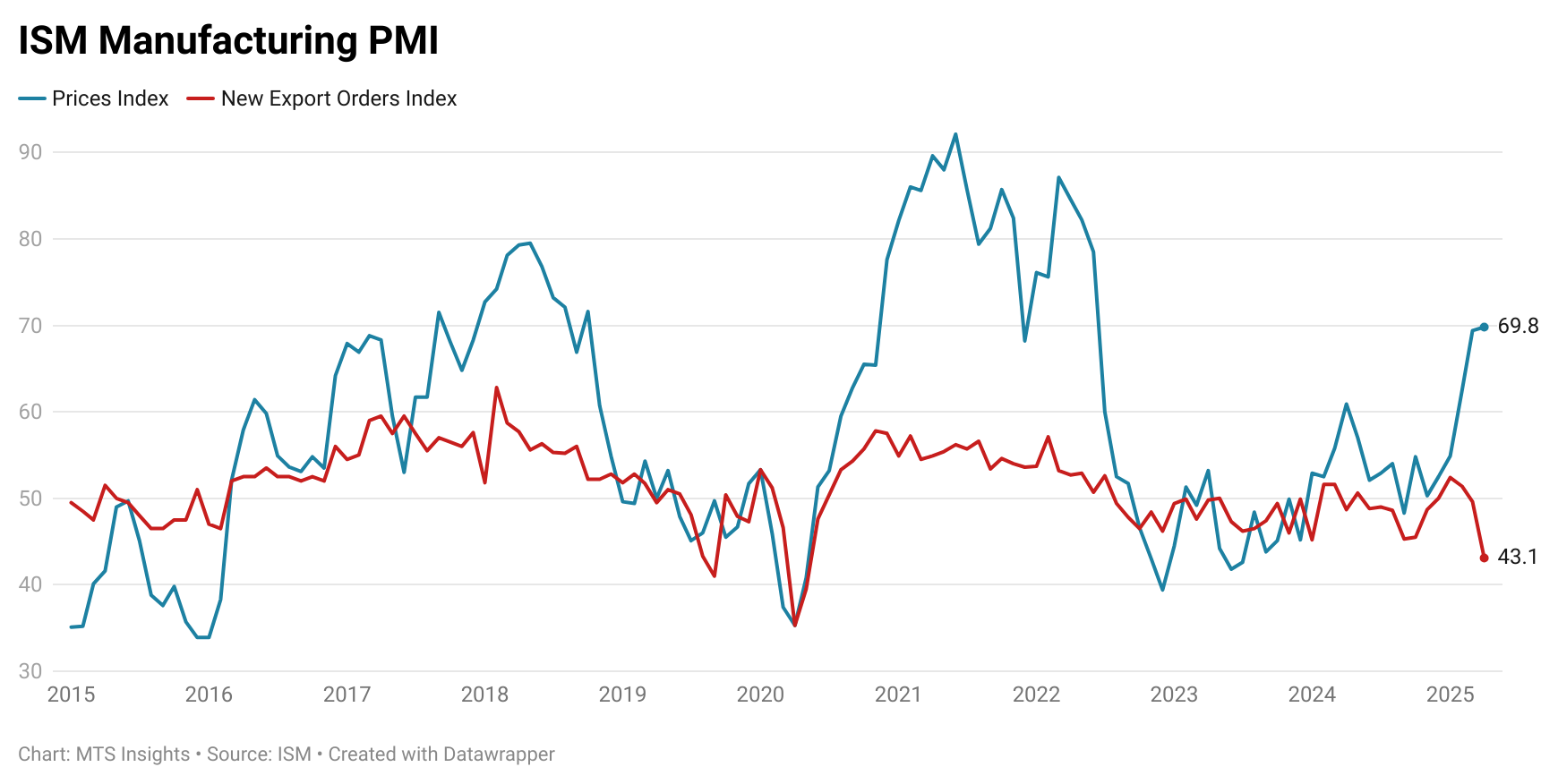

The two biggest movers in August were the New Orders index, up 4.3 pts to 51.4, and the Production index, down -3.6 pts to 47.8. Interestingly, the indexes appeared to have flipped such that demand went from a moderate contraction to a slight gain, and supply flipped from a marginal gain to a decline. The New Export Orders index increased 1.5 pts in August, but remained in a moderate decline, suggesting that the noted improvement in demand is primarily related to domestic markets.

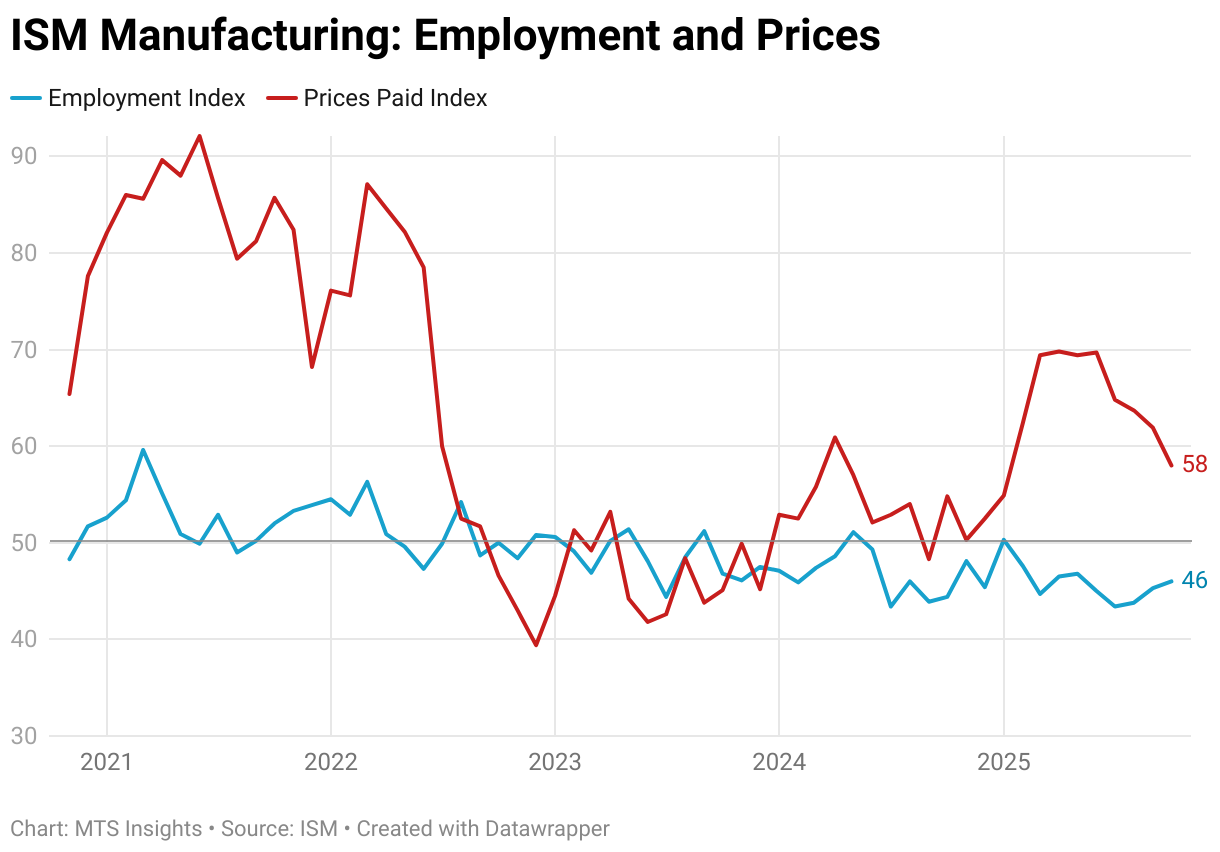

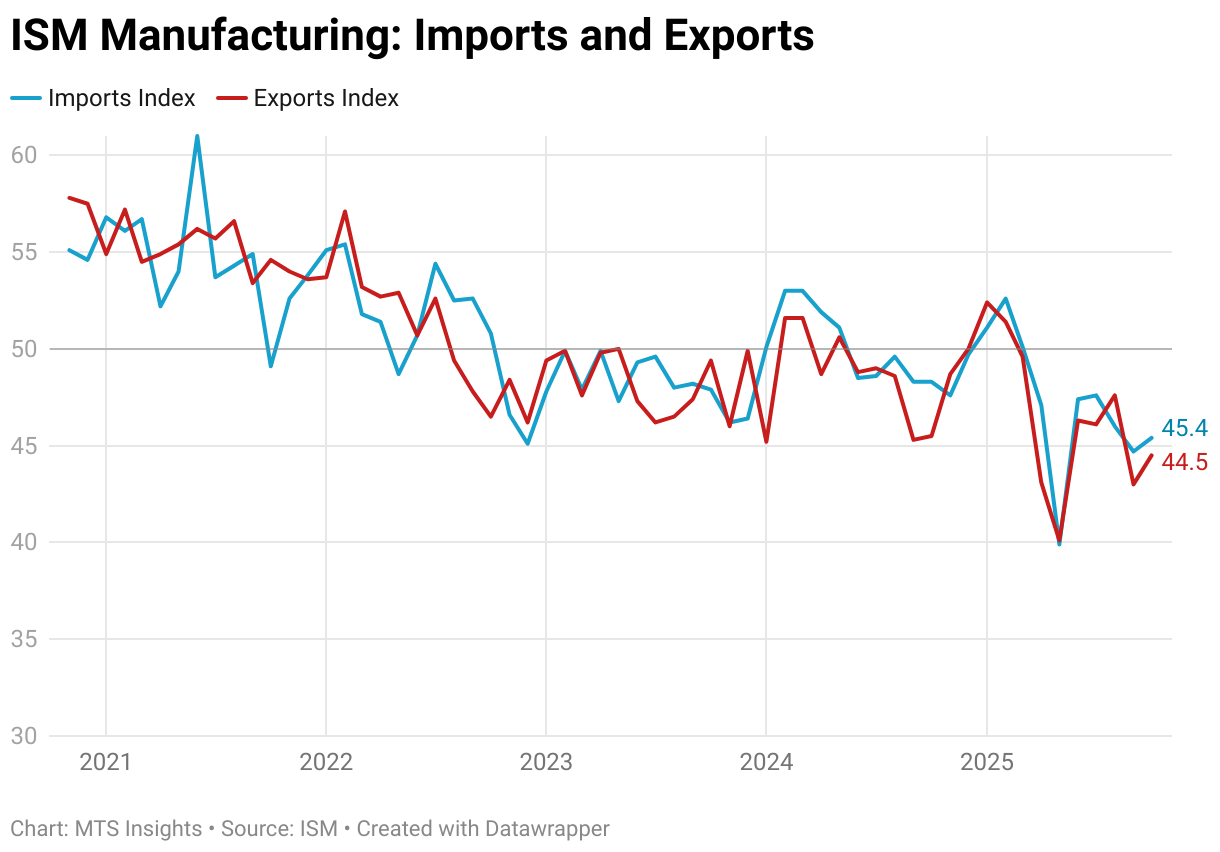

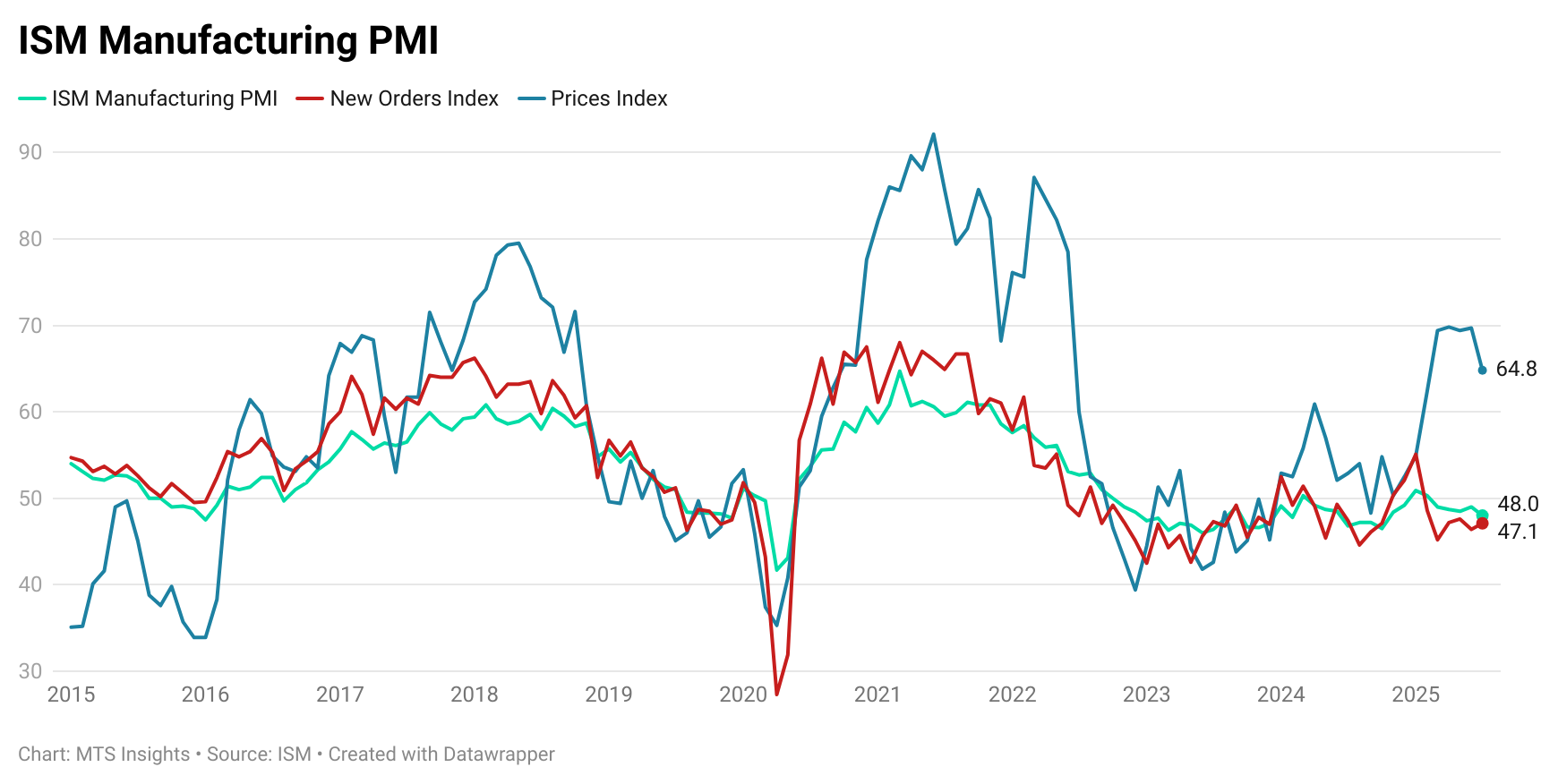

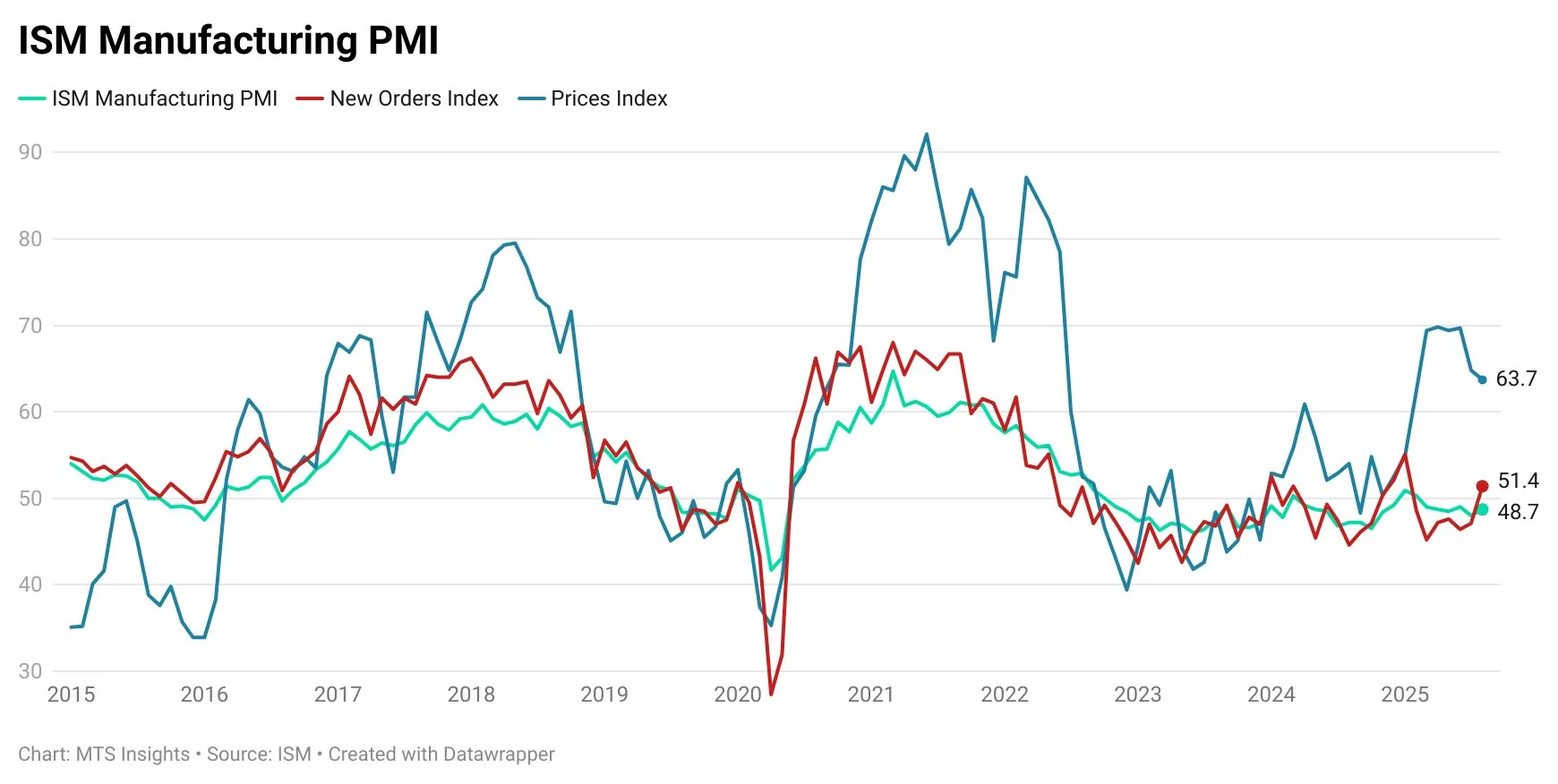

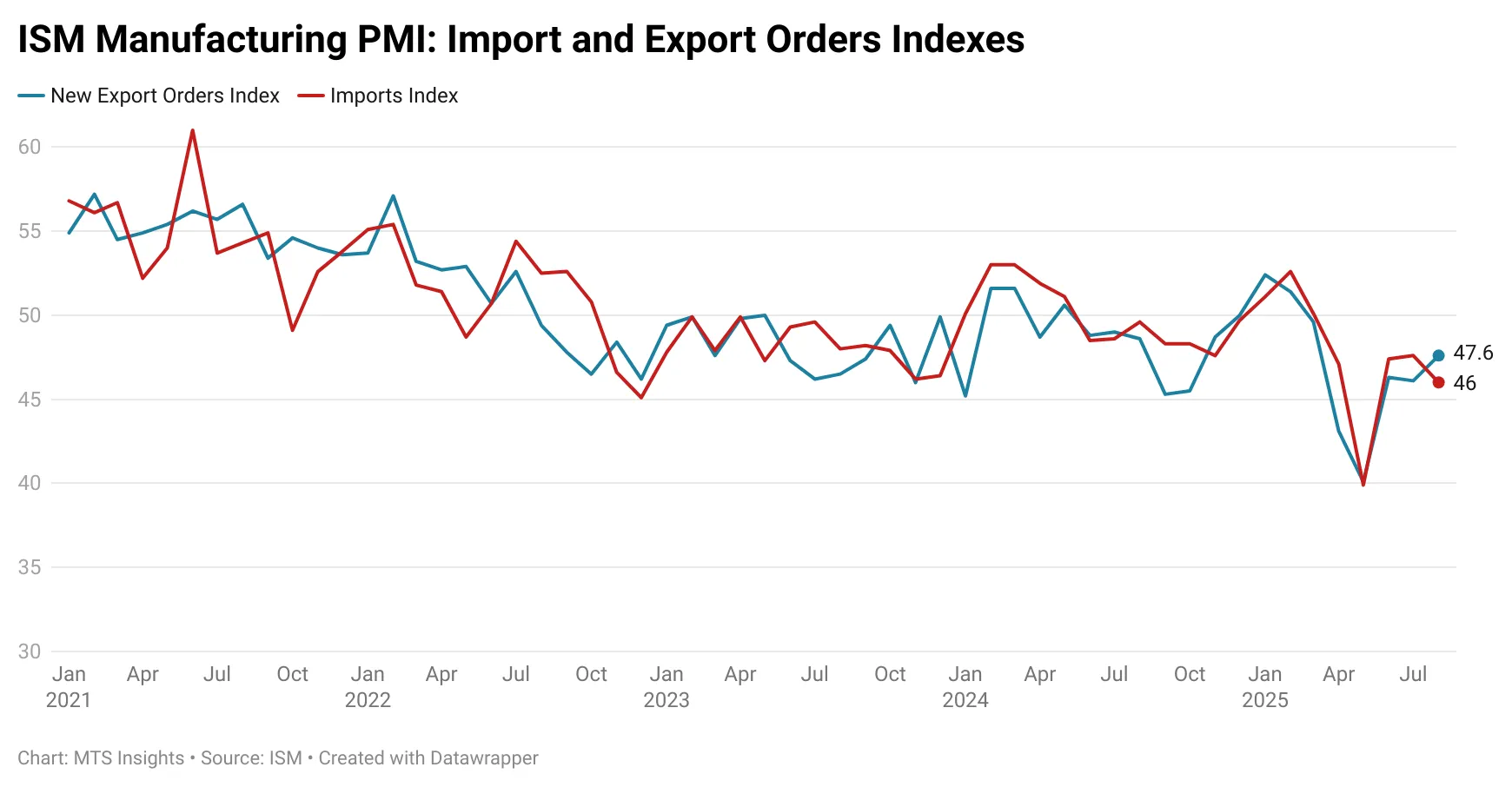

The tariff impacts show in the indexes tracking imports and prices. The Import index declined -1.6 pts to 46.0 as the subindex gave back some of the post “Liberation Day” rebound gains. In fact, with the exception of the May reading of 39.9, the August import indicator is the lowest since December 2022. It is very possible that the Import index will continue to decline as tariff policy becomes more entrenched and firms move past the inventory-building phase. The Price index has also reacted sharply to tariffs. While it did drop -1.1 pts in August, it remains elevated at 63.7, reflecting price pressures seen during the supply chain crunch of 2022-2023. In this subindex measuring inflationary pressures, the ISM survey is very similar to the S&P survey, such that both are pointing to a highly inflationary environment.

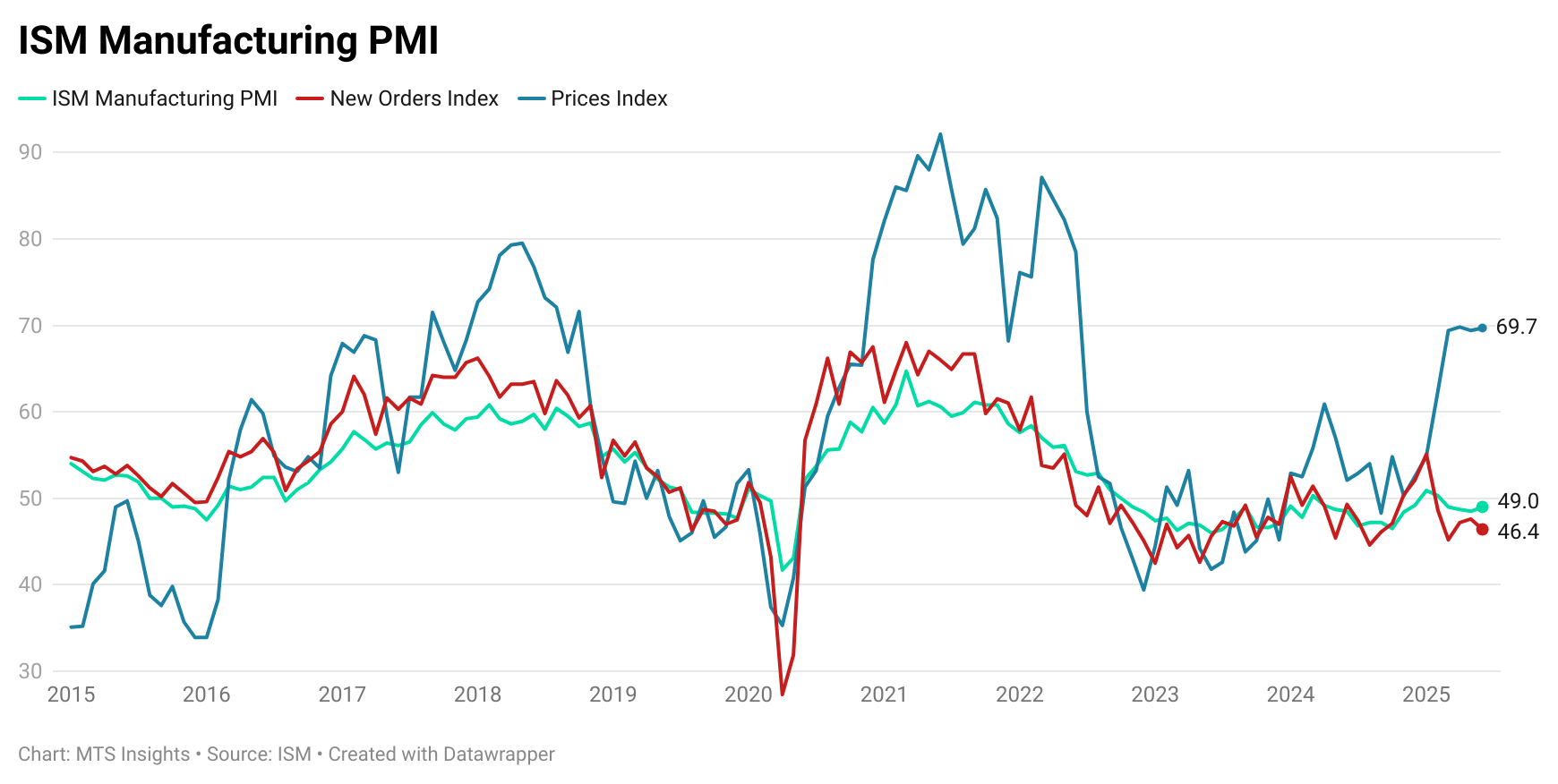

While there are similarities between the two surveys, there are some notable differences. The S&P survey showed evidence of inventory building by manufacturing firms in August, such that it was a major component of the strength in operating conditions. The ISM survey pointed to the opposite trend: the Inventories index was at 49.4, a slight contraction, and the Customers’ Inventories index eased to 44.6, an even deeper deterioration. Another key difference was in the employment measures. While the S&P PMI pointed to strong hiring trends, the ISM Employment index remained at a low 43.8, demonstrating a solid contraction in the manufacturing workforce not seen since Q3 2024 (when the Fed cut by 50 bps).

Overall, the ISM data is a more pessimistic view of the US manufacturing sector, even though the primary indicator of demand flipped from contraction to expansion. Besides that, the subindexes pointed to a continued weakening in trade, both imports and exports, shrinking inventories, and a significant decline in the manufacturing workforce. While this is all developing, tariffs are keeping price pressures high to make for a complicated environment for manufacturers.

ISM Manufacturing PMI

ISM Manufacturing PMI