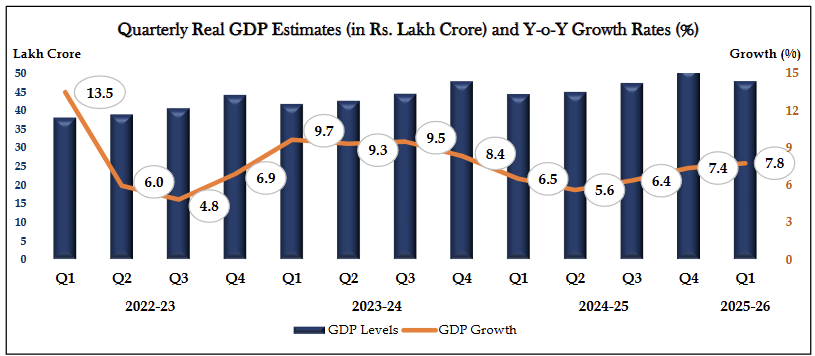

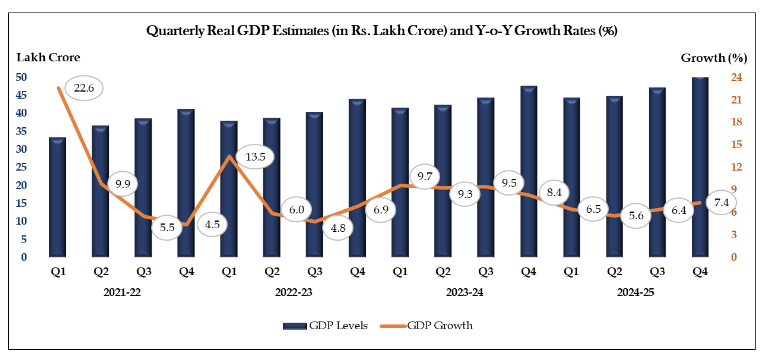

India GDP

India GDP

Data

GDP

- Source

- MOSPI

- Source Link

- https://mospi.gov.in/

- Frequency

- Quarterly

Latest Updates

-

India GDP: Q3 2025