IATA Air Cargo Market Analysis

IATA Air Cargo Market Analysis

- Source

- IATA

- Source Link

- https://www.iata.org/

- Frequency

- Monthly

- Next Release(s)

- April 30th, 2026 9:30 AM

Latest Updates

-

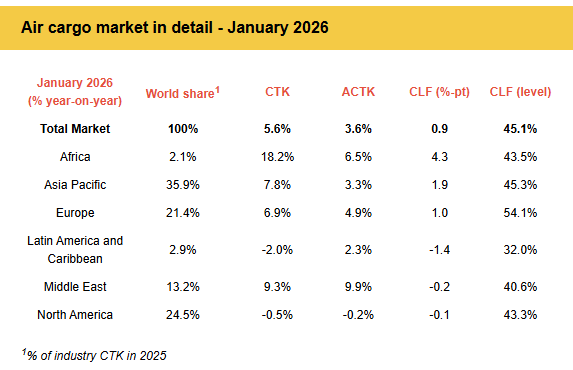

The International Air Transport Association (IATA) released data for January 2026 global air cargo markets showing:

- Total demand, measured in cargo tonne-kilometers (CTK), rose by 5.6% compared to January 2025 levels (+7.2% for international operations).

- Capacity, measured in available cargo tonne-kilometers (ACTK), increased by 3.6% compared to January 2025 (+5.7% for international operations).

“The demand for air cargo had a robust start to 2026, recording 5.6% year-on-year growth in January. At the regional level, the story is more polarized. Carriers in Africa, Middle East, Asia-Pacific, and Europe all reported faster growth than the global average. In contrast, carriers in the Americas reported aggregate contractions.

The resilience of air cargo will continue to be tested in the coming months. In addition to the long-running uncertainties of evolving US trade policies, the outbreak of hostilities in the Middle East will both weigh heavy on global supply chains. Addressing these topics will add extra importance to discussions at the upcoming World Cargo Symposium in Lima, Peru (10-12 March 2026) where strengthening air cargo’s adaptability and efficiency through digitalization and other measures will be a key focus,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:

- The global goods trade grew by 4.9% year-on-year in December 2025.

- Jet fuel prices decreased by 6.5% year-on-year in January.

- Global manufacturing sentiment strengthened in January, with the global Purchasing Managers’ Index (PMI) rising above the 50-point expansion threshold to 51.8, its highest level in over a year and a half. The PMI for new export orders climbed to 49.9, slightly below the growth threshold but the highest in 10 months, reflecting mixed but cautiously optimistic industrial growth.

-

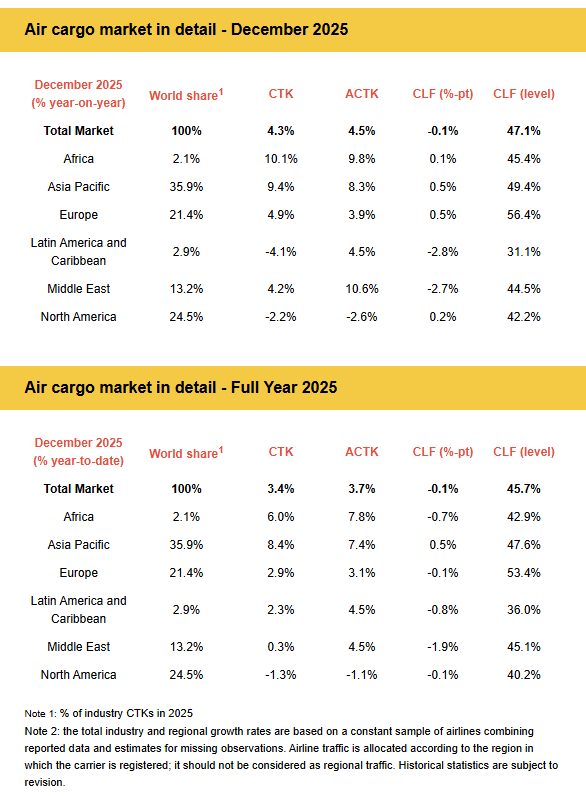

The International Air Transport Association (IATA) released data for full year 2025 and December 2025 global air cargo market performance showing:

- Full-year demand for 2025, measured in cargo tonne-kilometers (CTK), increased 3.4% compared to 2024 (4.2% for international operations).

- Full-year capacity in 2025, measured in available cargo tonne-kilometers (ACTK), increased by 3.7% compared to 2024 (5.1% for international operations).

- December 2025 brought the year to a close with continued strong performance. Global demand was 4.3% above December 2024 levels (5.5% for international operations). Global capacity was 4.5% above December 2024 levels (6.4% for international operations).

Additionally, IATA noted that full-year yields fell 1.5% year-on-year. This is the smallest decline in three years as a more normal supply-demand balance is achieved and the exceptionally strong yields of COVID and post-COVID continue to taper. Despite competitive pressure capping air cargo’s pricing power, yields remain 37.2% above 2019 levels.

“Air cargo delivered a strong performance in 2025, with demand up 3.4% year-on-year. Global e-commerce strength drove volumes, even as trading relationships with the US faced rising tariffs, the removal of de minimis tariff exemptions, and continuing policy uncertainty. Air cargo rose to the occasion. It adapted quickly to support global businesses and supply chains as they front-loaded product deliveries ahead of tariff impositions and adjusted to rising demand within Asia and between Asia and Europe as US-Asia trade stagnated,” said Willie Walsh, IATA’s Director General.“Growth in 2026 is expected to moderate slightly to 2.4%, in line with historical trends. We can expect that demand will continue to be shaped by trade and geopolitical developments. Whatever trading patterns emerge, we can be confident that reliance on air cargo to keep global supply chains running will remain, with carriers responding to the challenge by deploying capacity and designing their networks for optimum flexibility,” said Walsh.

Several factors in the operating environment should be noted:

- Global trade in goods grew by 2.5% annually in 2024. Year-to-date, January to November, for 2025, the index grew 4.4% (versus 2.4% of same period in 2024).

- Jet fuel prices fell 3.1% in December and averaged 9.1% lower in 2025 than in 2024. However, higher crack spreads meant refiners captured more margin, offsetting part of the benefit for airlines.

- Global manufacturing sentiment strengthened in December to reach 50.9. New export orders fell slightly to 49.1, but remained below the 50-point expansion threshold, reflecting ongoing caution amid tariff uncertainty.

-

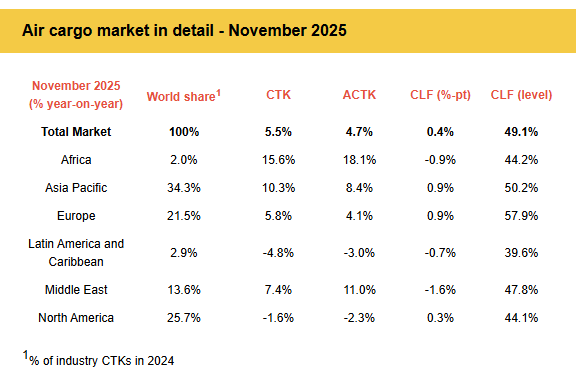

The International Air Transport Association (IATA) released data for November 2025 global air cargo markets showing:

- Total demand, measured in cargo tonne-kilometers (CTK), rose by 5.5% compared to November 2024 levels (+6.9% for international operations).

- Capacity, measured in available cargo tonne-kilometers (ACTK), increased by 4.7% compared to November 2024 (+6.5% for international operations).

“Air cargo demand grew 5.5% year-on-year in November 2025, boosted by shippers prioritizing timely delivery in the lead-up to the year-end holiday season. Strong emerging market demand and selective Middle Eastern growth more than made-up for softness in the Americas amid ongoing adjustment to the new US tariff regime. Globally, the fourth quarter for air cargo was resilient as strategic re-routing of trade shaped performance across key markets. The strong end for 2025 bodes well for the air cargo industry as it enters the new year,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:

- The global goods trade grew by 3.2% year-on-year in October.

- Jet fuel prices rose 5.9% in November despite falling crude prices, driven by refinery disruptions, EU restrictions on Russian-derived products, and limited spare refining capacity, pushing crack spreads close to double last year’s levels.

- Global manufacturing sentiment strengthened in November, with the PMI rising for the fourth consecutive month to reach 51.17. New export orders improved slightly to 49.87, but remained below the 50-point expansion threshold, reflecting ongoing caution amid tariff uncertainty.

-

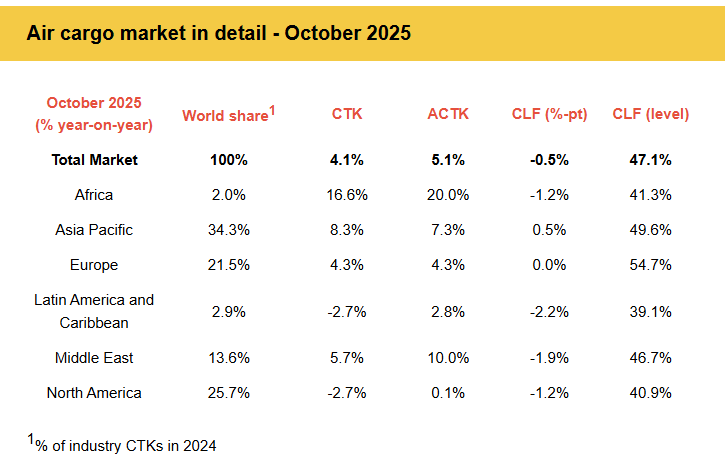

The International Air Transport Association (IATA) released data for October 2025 global air cargo markets showing:

- Total demand, measured in cargo tonne-kilometers (CTK), rose by 4.1% compared to October 2024 levels (+4.8% for international operations).

- Capacity, measured in available cargo tonne-kilometers (ACTK), increased by 5.1% compared to October 2024 (+6.4% for international operations).

“Air cargo demand grew 4.1% year-on-year in October, marking the eighth consecutive month of expansion and setting a new monthly record for volumes. While the Asia-North America trade lane extended its contraction to six months, October saw double-digit or near double-digit growth within Asia, between the Middle East and Europe, and between Europe and Asia. This shifting growth pattern shows that air cargo is enabling global supply chains to adapt to the impact of US tariffs. This positive news is especially significant as the air cargo sector enters the peak fourth quarter shipping season,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:

- The global goods trade grew by 5.3% year-on-year in September.

- Global industrial production rose 3.7% year-on-year in September, the fastest pace since March 2025 and the strongest monthly reading since late 2022.

- Jet fuel prices increased 2.5% in October even as crude fell, with a tightening diesel market driving the jet crack spread to nearly double last year’s level.

- Global manufacturing sentiment strengthened slightly in October, with the PMI rising for the third consecutive month to reach 51.45. New export orders deteriorated slightly to 48.31, remaining below the 50-point expansion threshold, reflecting ongoing caution amid tariff uncertainty.

-

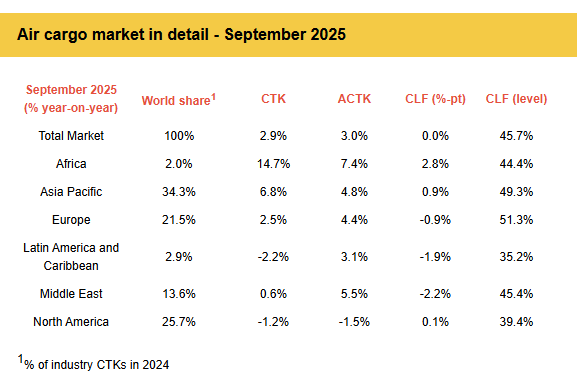

- Total demand, measured in cargo tonne-kilometers (CTK), rose by 2.9% compared to September 2024 levels (+3.2% for international operations).

- Capacity, measured in available cargo tonne-kilometers (ACTK), increased by 3.0% compared to September 2024 (+4.4% for international operations).

“Air cargo demand grew 2.9% year-on-year in September, marking the seventh consecutive month of overall growth. Buried in that growth is a significant alteration of trade patterns as US tariff policies, including the ending of de minimis exemptions, kick in. On one side of the equation, a decline in North America-Asia demand has set in over the last five months. But this has been more than compensated for with strong growth within Asia and on routes linking Asia to Europe, Africa and the Middle East. While many had feared an unwinding of global trade, we are instead seeing air cargo adapting successfully to serve shifting market demands,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:

- The global goods trade grew by 3.7% year-on-year in August.

- Jet fuel prices rose 5.4% in September despite lower oil prices, driven by a tighter diesel market, which doubled the crack spread year-on-year.

- Global manufacturing sentiment strengthened in September, with the PMI rising for the second straight month to reach 51.3. New export orders improved slightly to 49.6 but remained below the 50-point expansion threshold, reflecting ongoing caution amid tariff uncertainty.

-

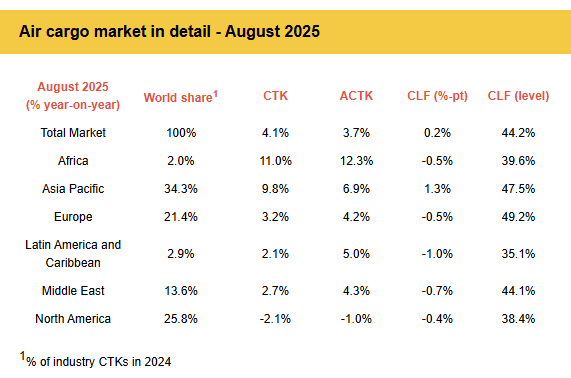

- Total demand, measured in cargo tonne-kilometers (CTK), rose by 4.1% compared to August 2024 levels (+5.1% for international operations).

- Capacity, measured in available cargo tonne-kilometers (ACTK), increased by 3.7% compared to August 2024 (+5.5% for international operations).

“Air cargo demand grew 4.1% in August, marking the sixth consecutive month of year-on-year growth. Volumes continue to grow even as global trade patterns change. Air cargo has benefitted from a shift from sea for some high value goods as shippers try to minimize the risk of tariff changes. And growth patterns indicate some being diverted away from North America, fueling stronger growth for the Europe–Asia, Within Asia, Africa–Asia, and Middle East–Asia trade lanes. This adaptability is vital as shippers navigate the evolving landscape of US tariff policy,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:- The global goods trade grew by 5.4% year-on-year in July.

- Jet fuel prices in August were 6.4% lower year-on-year, marking the fourteenth consecutive month of year-on-year declines.

- Global manufacturing in August showed rising optimism in manufacturing PMI, with a rebound to 51.75, the strongest reading since June 2024. Sentiment on new export orders, however, remains below 50 at 48.73, reflecting persistent caution amid tariff uncertainty.