Analysis

Israel and Iran’s brief exchange of military strikes – a first since early April – that concluded by Monday did not materially change the status quo in terms of the Iran war impact for the broader ocean freight and logistics markets: higher oil prices putting some upward pressure on freight rates via elevated fuel costs.

Likewise, the IRGC threat to close the Bab el-Mandeb Strait via renewed Houthi attacks would not change much for freight if implemented, as the vast majority of container traffic continues to divert away from the Red Sea. The added tension may push back the timeline for a Hormuz reopening, though the White House continues to assert that negotiations are making progress.

The USTR has released the results of a Section 301 investigation of forced labor imports to 60 countries and found all had either not legislated or not sufficiently enforced laws meant to bar the entry of goods manufactured using forced labor. The study argues that these imports harm the US and recommends 12.5% tariffs on countries without sufficient prohibitions, and 10% on countries not sufficiently enforcing their laws.

This move can be seen as an effort to replace invalidated IEEPA tariffs by the late July expiration date of the current 10% Section 122 global duty, with the next step – a required hearing – slated for July 7th.

Despite the fact that this 301 would maintain the same long list of exemptions compiled over the past year, and that tariffs at these levels would be lower than those set under IEEPA for many countries, some are pushing back against the accusation – either on principle or in anticipation of additional tariffs from 301 investigations set to conclude before the end of July as well.

Transpacific ocean peak season is well underway, with some observers pointing to frontloading ahead of the approaching tariff deadline as one driver of the early start.

And though the Hormuz closure hadn’t caused broad operational changes beyond the Gulf states in the first three months of the war, the rising price of oil may be another factor to the early peak season surge. Many contracted shippers – set to face an 80% jump in fuel surcharges starting in July when the quarterly BAF is updated – may be pulling forward peak season shipments to get ahead of that cost increase. And indications that manufacturers in the Far East are set to increase prices due to higher input costs may also be driving some of the observed early demand bump.

Whatever the drivers, the National Retail Federation’s latest US ocean import volume report confirms the peak season pull forward and moves this year’s peak month up to June from its estimate of a July high a month ago. The report projects June volumes will climb 5% compared to May arrivals before imports ease 3% in July and continue to cool through September – suggesting that the early start is indeed driven by frontloading that will come at the expense of volume strength later in the summer.

Transpacific container spot rates that were starting from an already elevated fuel cost baseline are now spiking to year highs as demand surges. June 1st GRIs and PSSs pushed last week’s prices up to $4,800/FEU – a $1,600/FEU and more than 50% climb – to the West Coast, with a $1,300/FEU and 25% climb for East Coast rates that hit $6,300/FEU. These spikes are the sharpest one-week increases since sudden tariff changes spurred a June demand surge last year, though rates climbed more than $2k/FEU in that instance.

Last year, prices started to fall by mid-June, while indications are that additional rate increases set for next week could push prices up further this time. But NRF projections that demand will peak in June, make additional rate increases in July less likely.

Peak season started early for Asia - Europe lanes as well due to some of the same drivers at play on the transpacific – looming BAF increases and producer price hikes – but also because of longer lead times from Red Sea diversions and persistent congestion at some of the major European hubs, with building congestion at some Chinese ports also a factor.

Rates increased about $1k/FEU to both N. Europe and the Mediterranean last week, pushing prices up to $4,000/FEU to N. Europe and $5,500/FEU to the Mediterranean. These rate levels have already surpassed peak season highs last year with strong year on year volume growth through April likely persisting into peak season too. Mediterranean prices are approaching a level last seen in late 2024 in the lead up to Lunar New Year. Some experts expect mid-month GRIs to push rates up further, but like on the transpacific, June could be the peak in terms of demand and rate levels.

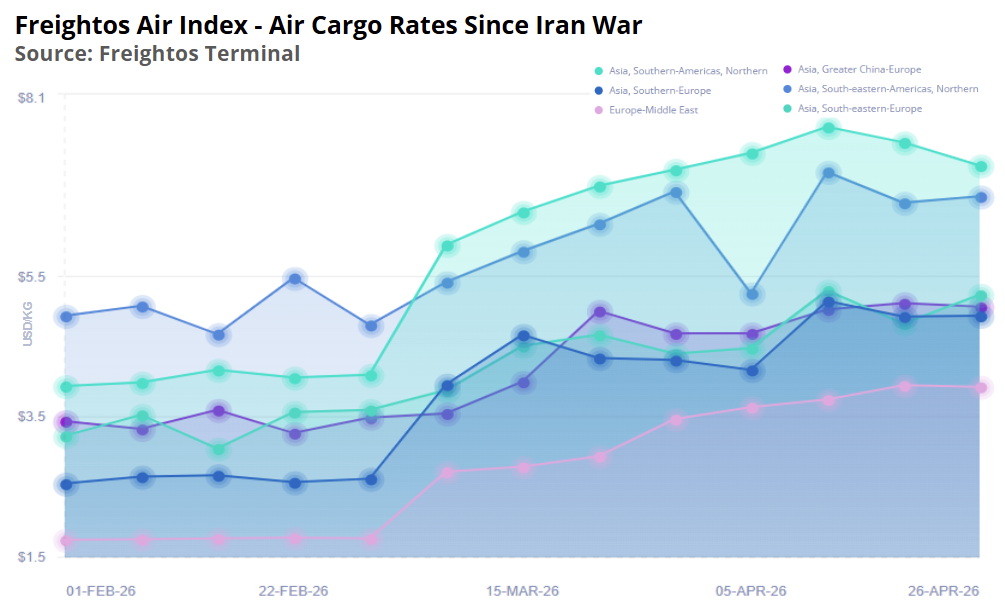

In air cargo, the recent missile strikes in the Middle East did not result in significant air space closures, and the region’s recovery continues. In May, monthly Middle East inbound air cargo volumes climbed even with last year for the first time since the start of the war.

Low value, e-commerce air cargo imports to the US fell sharply in the first few months following the Trump Administration’s de minimis suspension last May. But e-commerce air volumes have not disappeared. Demand rebounded to some extent toward the end of 2025 as platforms adjusted to the new rules. And even if e-commerce imports haven’t fully recovered – Q1 volumes were 11% lower than in 2025 – they still accounted for 13% of all Q1 air imports to the US this year compared to 16% in Q1 last year.

Likewise, e-comm volumes moving by air are expected to contract when the EU eliminates its de minimis threshold on July 1st. But while the rule change will increase visibility and scrutiny of low value imports, lessons learned by the e-commerce platforms from the US de minimis changes may mean EU e-commerce volumes entering by air won’t drop dramatically.

Meanwhile, for both lanes, a new vertical is increasingly driving demand even as e-commerce cools. Q1 US air cargo import volumes from hardware related to the explosion in demand for AI computing – such as semiconductors, servers and racks – contributed to a 70% year on year increase in high-tech air cargo imports in Q1, driving an 11% increase in overall US air volume imports even as e-commerce demand contracted.