Freightos Weekly Update

Freightos Weekly Update

- Source

- Freightos

- Source Link

- https://www.freightos.com/

- Frequency

-

Weekly

Tuesday

- Next Release(s)

- March 17th, 2026 12:00 PM

-

March 24th, 2026 12:00 PM

-

March 31st, 2026 12:00 PM

-

April 7th, 2026 12:00 PM

-

April 14th, 2026 12:00 PM

-

April 21st, 2026 12:00 PM

-

April 28th, 2026 12:00 PM

-

May 5th, 2026 12:00 PM

-

May 12th, 2026 12:00 PM

-

May 19th, 2026 12:00 PM

-

May 26th, 2026 12:00 PM

-

June 2nd, 2026 12:00 PM

Latest Updates

-

Analysis

Very few vessels have passed through the Strait of Hormuz since the start of the war in Iran a week and a half ago. The closure is of global concern due to its stifling of oil tanker movements which is already slowing production and pushing oil prices up.

The US International Development Finance Corporation announced a plan to insure vessel transits despite the security risk, though few carriers will likely take up the offer without naval protection as well. And the government is much more likely to devote these resources to oil tankers than to container flows.

For the container market, disruptions from the strait’s closure are so far limited to containers already en route to (or stuck in) the Gulf ports, with some knock-on congestion elsewhere. Ports in countries like India and Bangladesh – significant exporters to the Gulf states – are reporting backlogs. And yard utilization levels are increasing at transhipment hubs in the Far East where some Gulf-bound containers are now being diverted. Yard density at those ports could increase somewhat in the coming days as shippers who so far decided to wait and see may choose to divert Gulf-bound containers there as the Strait remains closed.

Carriers are rolling out contingency plans for Gulf volumes via alternative ports in the region, with shipments then moving on to their destinations by road. Carriers are applying significant surcharges for those containers already in transit on these lanes, and offering alternatives like storage, return to origin and change of destination, which will also incur additional costs.

For the broader container market though, Iran’s closure of the Strait of Hormuz has not caused disruptions or price increases yet. And while congestion at Far East tranship hubs could cause delays for non-Gulf volumes in the near term, these backlogs should be much less significant than those seen at the outset of the Red Sea crisis, since the volumes involved are much lower and since carriers have already suspended new bookings to those destinations.

But one way global container shipping could be impacted is by rising fuel costs. The climbing price of oil has already led some carriers like CMA CGM and Hapag-Lloyd to announce emergency fuel surcharges for all lanes at $70-75/TEU for regional transits and $150/TEU for long haul voyages starting March 23rd, with others announcing fuel increases only on certain lanes for now. If oil prices remain elevated, more carriers are likely to introduce emergency surcharges, though standard fuel rates – adjusted on a quarterly basis and already set for Q2 – could only increase to start Q3.

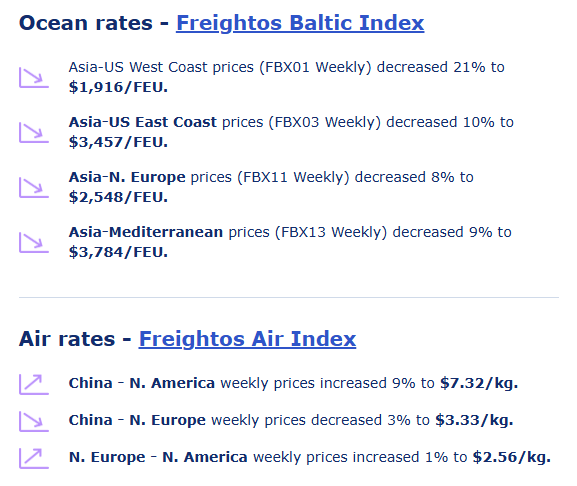

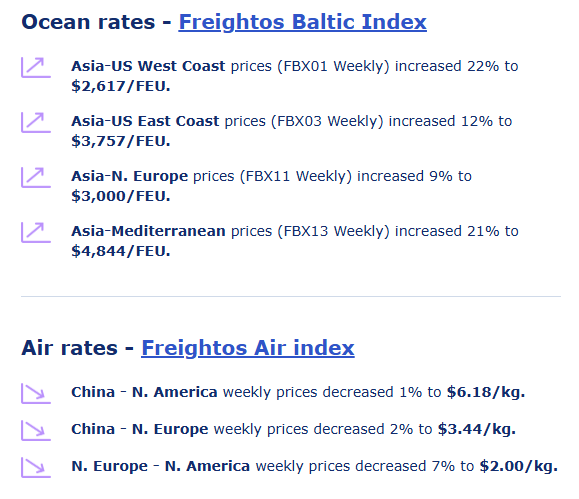

Freightos Baltic Index transpacific container rates increased about $200 or 10% to $2,022/FEU last week, with daily rates to the East Coast showing a similar climb to about $3,000/FEU so far this week. Asia-Europe rates increased 6% last week to about $2,600/FEU and 2% to $3,700/FEU to the Mediterranean, with prices continuing to climb so far this week.

These rate increases are not likely related to the war in Iran, and instead reflect attempts by carriers to bump prices up now that we’re in the post-Chinese New Year period when it is not uncommon for demand to increase for a couple weeks. Emergency fuel surcharges, though, could start showing up as a component of rate levels once implemented.

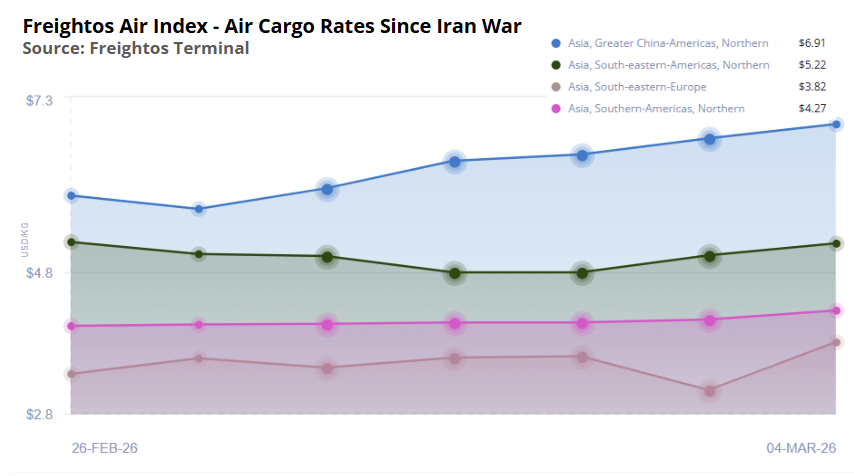

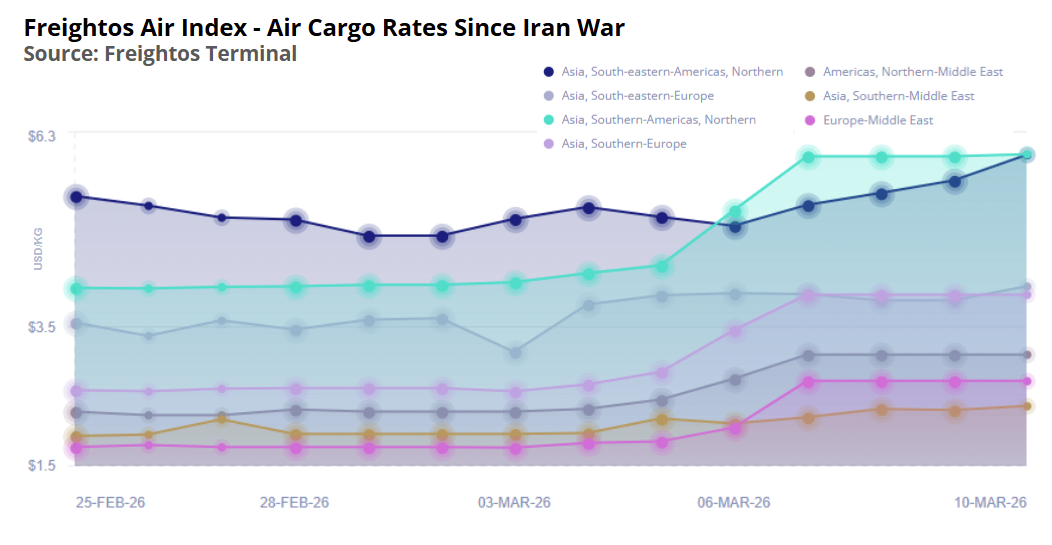

In air cargo, a more broad range of lanes have been impacted by airspace closures in the Gulf, with rates climbing significantly on a list of lanes.

Gulf carriers Qatar Airways and Emirates Skycargo are two of the top three largest cargo carriers by capacity, and together with Etihad make up about 13% of global capacity. Their hubs serve as a major east-west connection point, including providing a significant share of South Asia and South East Asia capacity to Europe and N. America.

As a result, Freightos Air Index data show air cargo rates have increased by about 50% since the start of the war from South Asia to N. America and Europe, with rates now at about $6.00/kg and $4.00/kg respectively. SEA - Europe prices are up 20% to more than $4.00/kg. China - US rates have climbed 20% to more than $7.00/kg too, though this increase may be mostly due to post-LNY demand. That these disruptions are coinciding with the post-LNY rush could be adding some upward pressure to ex-China rates as volumes that normally would go via the Gulf compete for long haul space.

Most Gulf airports closed completely for several days at the start of the war, but over the last few days some started to reopen partially. The UAE has reportedly opened safe air corridors enabling 48 flights per hour to depart. Emirates Airways reports it is now operating a reduced but stable flight schedule, and are now estimated to be flying more than 50% of their scheduled flights. Etihad has also resumed some flights, though Qatar Airways Cargo operations through Doha remain suspended. With these flights and capacity returning to the cargo market, we may see pressure on rates ease somewhat in the coming days. Like in ocean, some forwarders are working to fly cargo with final destinations in the Gulf to alternate airports in the region, especially Saudi Arabia, and move goods on by road.

In trade war developments, following the Supreme Court’s decision invalidating President Trump’s IEEPA-based tariffs, the US Court of International Trade ordered the government to start refunding the billions of dollars in IEEPA tariffs paid over the past year.

Some experts were surprised by the speed at which this ruling was issued, and that it relies on a single case to resolve refunds for everyone even as more than 2,000 individual suits had been filed. Customs and Border Protection responded that these hundreds of thousands of payments can’t be made immediately and asked for 45 days to set up an automated system. There are still a lot of questions as to when refunds will actually start going out and who will receive them, but these developments are a big step forward.

In the meantime, the administration has put 10% global tariffs into place relying on Section 122 – even as two dozen states are challenging the administration’s use of this law – and the USTR says Section 301 investigations that will be used as the basis for country-specific tariffs replacing EEPA duties are underway and will be concluded before the Section 122 tariffs expire in late July. The president has said that an additional executive order will introduce Section 122 tariffs at 15% for some countries, though so far no such order has been issued.

The current Section 122 tariffs mean lower-than-IEEPA duty levels for some companies, leading to reports of some companies starting to frontload before the July deadline, while others are not taking action just yet. The latest National Retail Federation US ocean import volume projections through June are about even with those from just before the SCOTUS decision, suggesting that most companies are remaining cautious, and not pulling volumes forward. The report expects H1 volumes to be 2.5% lower than in 2025.