FAO Cereal Supply and Demand Brief

FAO Cereal Supply and Demand Brief

- Source

- United Nations

- Source Link

- https://www.fao.org/

- Frequency

- Monthly

- Next Release(s)

- December 5th, 2025 4:00 AM

Latest Updates

-

Favourable short-term prospects for cereal markets

Release date: 07/11/2025

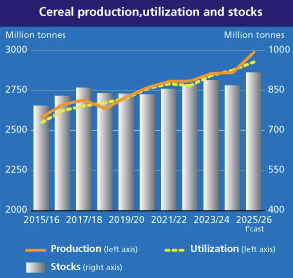

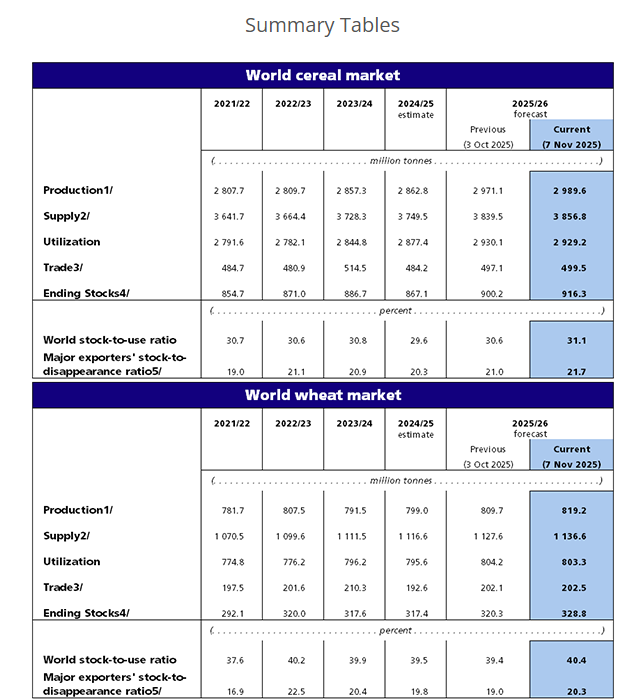

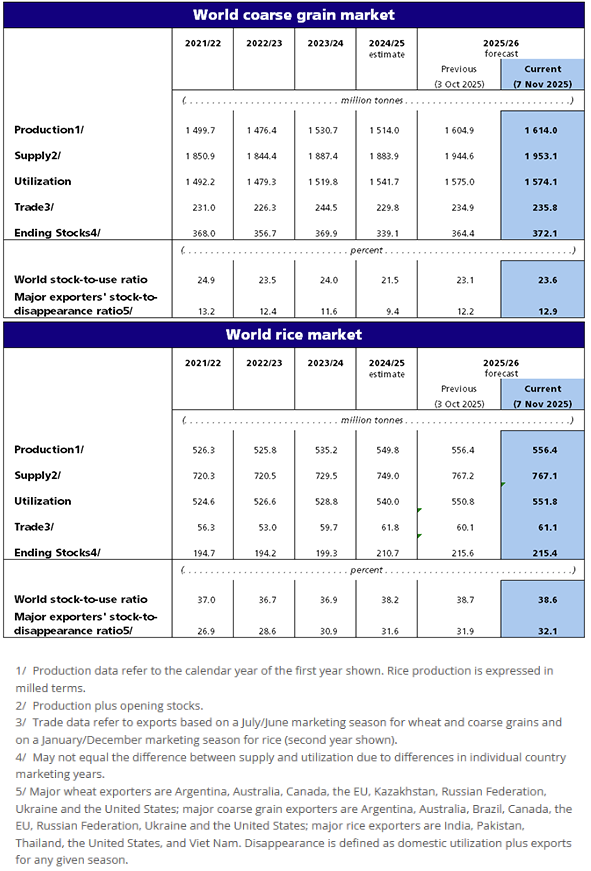

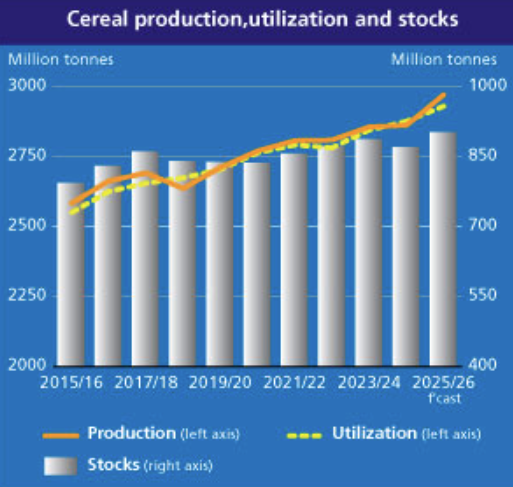

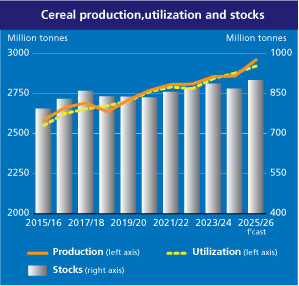

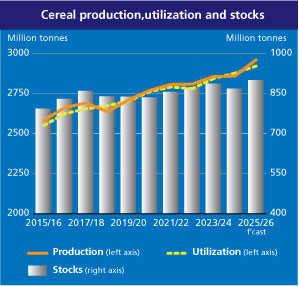

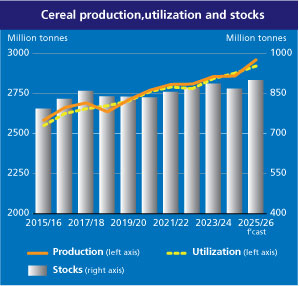

Forecast at 2 990 million tonnes, world cereal production (including rice in milled equivalent) is expected to reach a record level in 2025, up 4.4 percent from 2024. Outputs of all major cereals are anticipated to rise, with the largest year-on-year increase forecast for maize and the smallest for rice. Both maize and rice outputs are predicted to hit new record highs.

World cereal utilization in 2025/26 is forecast at 2 929 million tonnes, up 51.9 million tonnes or 1.8 percent from 2024/25. The growth is expected to result mainly from ample supplies and lower prices. Feed use of cereals is expected to rise by 2.1 percent, with major producers such as Brazil and the United States of America directing more maize to animal rations, while in Asia, strong demand from aquaculture is expected to be met though imports of feed-quality wheat. Other uses of cereals, particularly maize, are also set to increase. Human consumption of cereals is forecast to rise marginally, reflecting population growth and gradual dietary shifts.

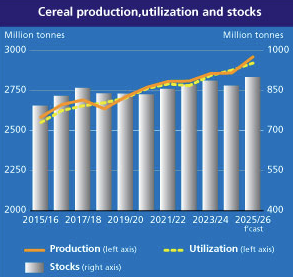

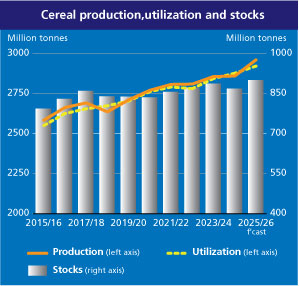

Based on the current forecasts for global cereal production in 2025, stocks could rise by 5.7 percent from their opening levels to a record high of 916.3 million tonnes. Global maize inventories are expected to expand the most, especially in Northern America, followed by wheat and barley, while global sorghum stocks may decrease slightly. World rice stocks at the close of the 2025/26 marketing years are forecast to rise by 2.2 percent to a new peak of 215.4 million tonnes. Overall, the global cereal stocks-to-use ratio in 2025/26 is predicted to rise to 31.1 percent, the highest level since 2017/18. .

World trade in cereals in the 2025/26 season is anticipated to expand by 3.2 percent to 499.5 million tonnes. Wheat trade (July/June) is expected to rise by 9.9 million tonnes, or 5.1 percent from the previous season, driven largely by Asian imports, which are forecast to increase by 15.6 million tonnes. Global trade in coarse grains is anticipated to expand amid relatively low export prices and stronger demand for animal protein, though traded volumes will likely remain below the 2023/24 peak. By contrast, global rice trade is forecast to decline by 1.2 percent to 61.1 million tonnes in 2026.

-

Cereal markets remain well supplied, with a positive outlook for the short term

Release date: 03/10/2025

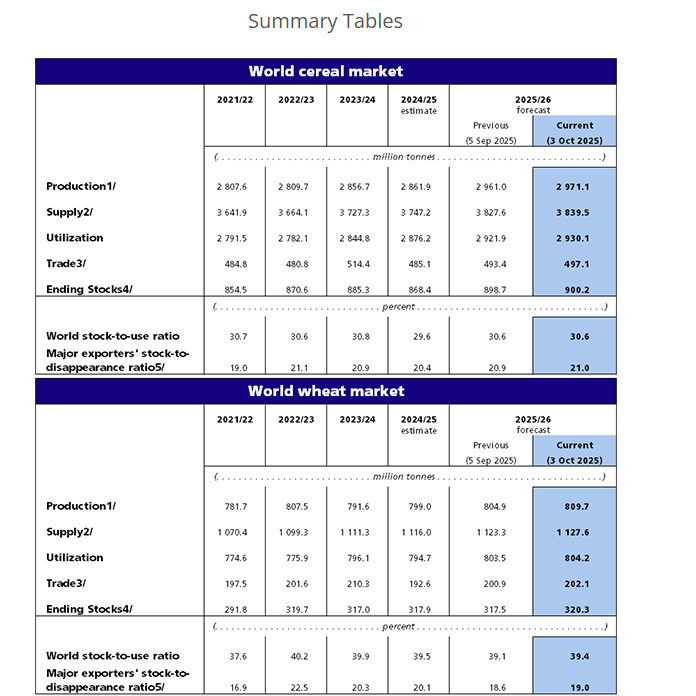

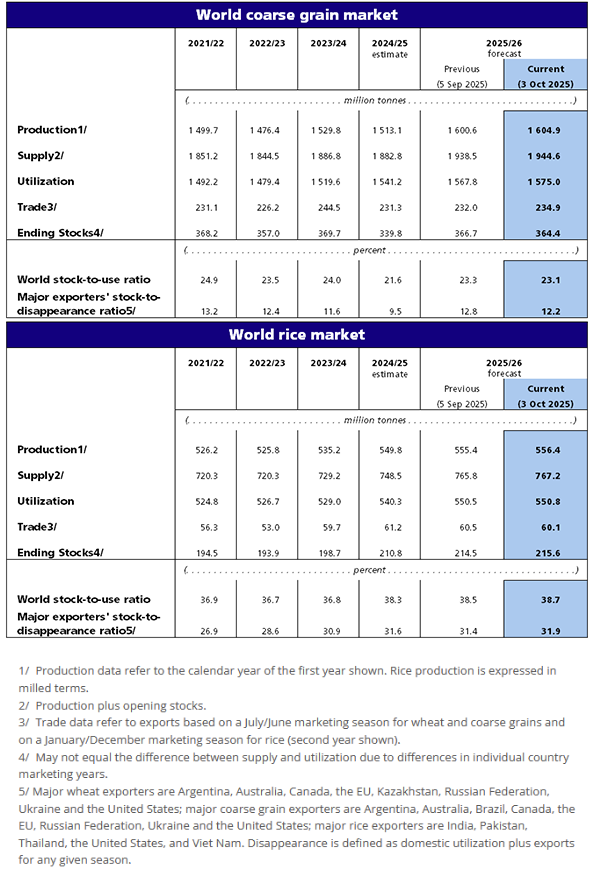

FAO’s latest forecast for global cereal production in 2025 has been raised by 10.1 million tonnes (0.3 percent) this month, putting the total at 2 971 million tonnes. The increase reflects upward revisions to production forecasts across all crops, led by wheat, maize and rice (in order of magnitude). At this level, world cereal production is 3.8 percent higher year on year, marking the largest annual growth since 2013.

World wheat production is forecast at 809.7 million tonnes in 2025, up 0.6 percent compared to the previous month and now 1.3 percent above the 2024 output. Most of this month’s increase is linked to Australia, where favourable July-August rains, following a dry start of the season in parts, boosted yield expectations and lifted the 2025 production forecast to a level now on par with the five-year average. Forecasts for the European Union and the Russian Federation are also raised on stronger yields. Global coarse grains production in 2025 is forecast at 1 605 million tonnes, up 0.3 percent from last month’s figure and now 91.7 million tonnes higher than the 2024 outturn. The latest upward revision is principally driven by a higher forecast in Brazil, linked to better-than-expected yields. Maize production has also been raised for China (mainland), on newly released official data, and for the United States of America, tied to a larger area that outweighed a concurrent small cut to yields. At 427.1 million tonnes, the United States of America’s maize output would reach an all-time high and account for one-third of the global output, the highest share of global maize production since 2016. These increases offset cuts to production forecasts in the European Union, where dry and hot weather curtailed yield expectations, and in Mexico, where recent official figures point to a smaller-than-expected area. The forecasts for global barley and sorghum production in 2025 have also been raised marginally this month, largely reflecting improved prospects in Australia. As for rice, FAO has provisionally lowered its production forecast for Pakistan by 0.6 million tonnes (milled basis), owing to severe floods in Punjab, the country’s leading rice producing province. However, this downgrade is outweighed by 1.6 million tonne increase in production expectations for India, where a strong pace of Kharif crop plantings is reported, despite some challenges posed by deficient rains in some eastern and northeastern states and by floods in northwestern areas. As a result of these changes and various other smaller amendments, world rice production is now forecast to reach a record high of 556.4 million tonnes (milled basis) in 2025/26, up 1.0 million tonnes from September expectations and implying a 1.2 percent annual expansion.

FAO’s forecast for world cereal utilization in the 2025/26 season is now expected to reach a record level of 2 930 million tonnes following an upward revision of 8.1 million tonnes since September. At 1 575 million tonnes, the forecast for total utilization of coarse grains in 2025/26 is up 7.2 million tonnes since the previous report and 33.8 million tonnes (2.2 percent) higher than the 2024/25 level. This month’s upward revision mostly reflects higher use of maize and barley in feed rations and for industrial purposes. Plentiful supplies of maize are forecast be directed to animal feed in the leading producers Brazil and the United States of America, and in importing countries such as Egypt and Mexico. Wheat use in 2025/26 is also seen at a record level of 804.2 million tonnes with both feed use and human consumption expected to rise, the latter in line with population growth with per-capita food consumption broadly unchanged year on year. World rice utilization is forecast at a historical peak of 550.8 million tonnes in 2025/26, little changed from September expectations and up 2.0 percent from 2024/25.

The forecast for world cereal stocks by the close of seasons in 2026 has been revised upwards by 1.6 million tonnes since the previous month to 900.2 million tonnes, with upward revisions made to wheat and rice, while forecasts for coarse grains are scaled back slightly. Stocks of wheat are expected to grow by 2.4 million tonnes from their opening levels with some build-up in major producers such as Canada and the Russian Federation after large harvests. Stocks of maize are expected to rebound largely due to accumulations in major producers Brazil and the United States of America while stocks in the European Union could decline as production forecasts are scaled back, while feed use is expected to grow. Among other coarse grains, stocks of barley, sorghum and rye are expected to remain stable. The global cereal stocks-to-use ratio in 2025/26 is expected to remain nearly unchanged from last season at 30.6 percent, continuing to indicate comfortable supply prospects in the new season. Following a 1.1 million tonne upgrade to 215.6 million tonnes, FAO’s forecast of world rice stocks at the close of 2025/26 marketing years continues to suggest that world rice reserves could strike a record high, sustained by accumulations in rice exporting and importing countries.

FAO’s latest forecast for world trade in cereals in 2025/26 has been raised by 3.7 million tonnes to 497.1 million tonnes this month, pointing to an increase of 2.5 percent (12.0 million tonnes) from the 2024/25 level. World trade in wheat (July/June) is forecast to grow by 4.9 percent (9.5 million tonnes) in 2025/26 to 202.1 million tonnes, up 1.2 million tonnes from last month’s forecast. Lower export prospects in the European Union reflecting slow pace observed in the first quarter are outweighed by upward revisions to exports from Australia, on abundant supplies following a bumper harvest, and the United States of America on competitive prices and continuing strong demand from Iraq and Türkiye. Trade in coarse grains is also lifted by 2.9 million tonnes on upward revisions to barley and sorghum while global maize trade, at 189.9 million tonnes, is now expected to be near to the level of the 2024/25 season as importing countries take advantage of abundant supplies and low prices. The start of the 2025/26 season has seen strong demand for coarse grains from the European Union, Mexico and Türkiye while purchases by China remain subdued. International rice trade is forecast at 60.1 million tonnes in 2026 (January-December), down from a revised forecast of 61.2 million tonnes for 2025. The 1.8 percent annual reduction is expected to be demand driven, as ample availabilities from good local harvests and large purchases in 2025, could drive a second annual cut in Asian imports, while also easing purchases by African countries somewhat.

-

Improved prospects for coarse grains put global cereal production in 2025 forecast at all-time high

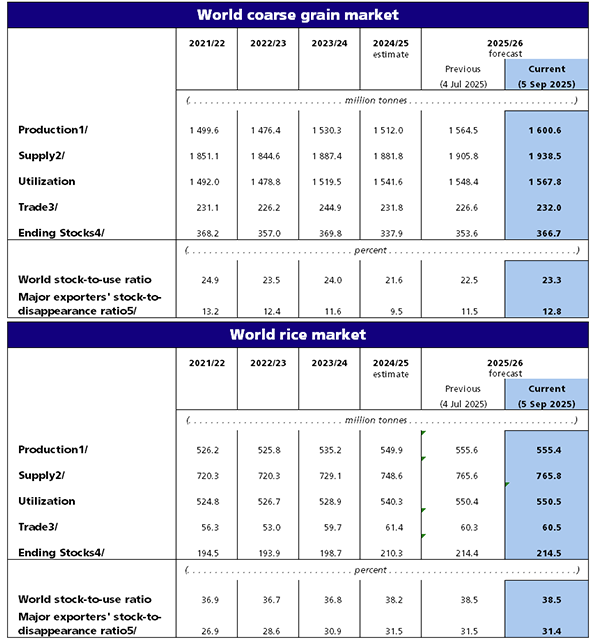

Release date: 05/09/2025

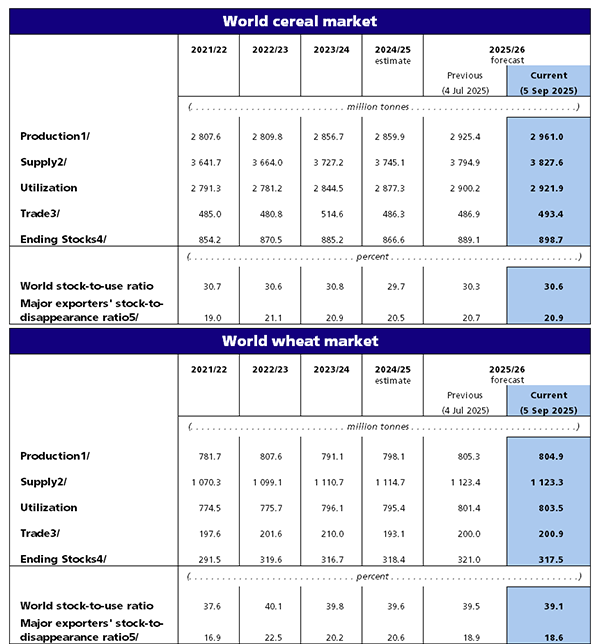

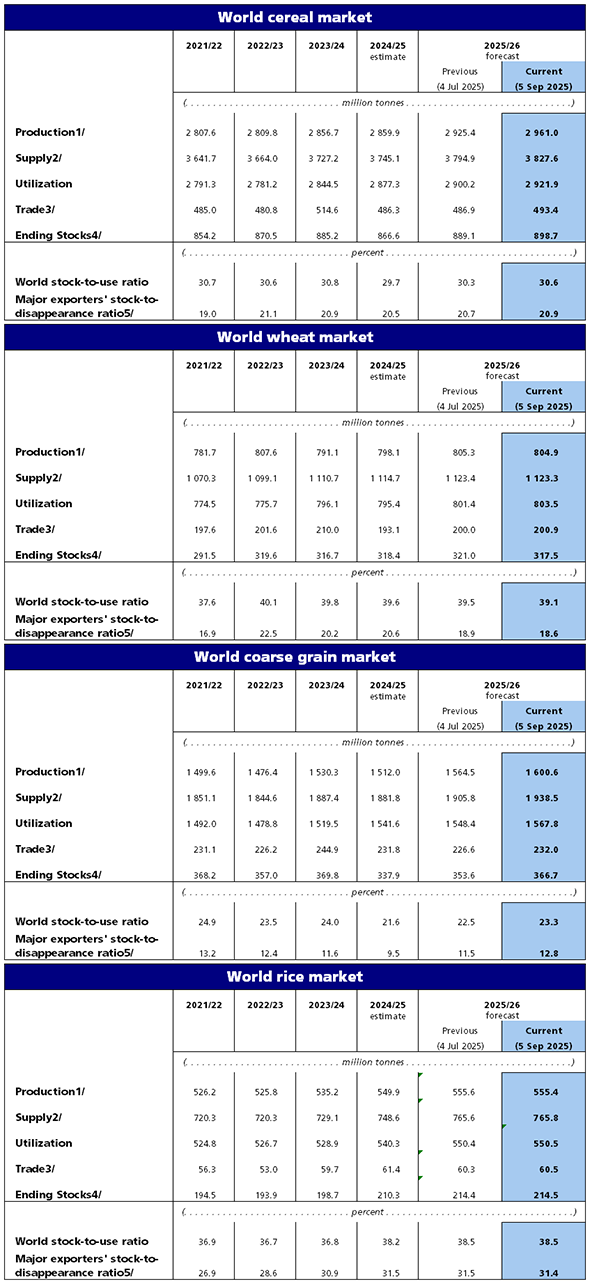

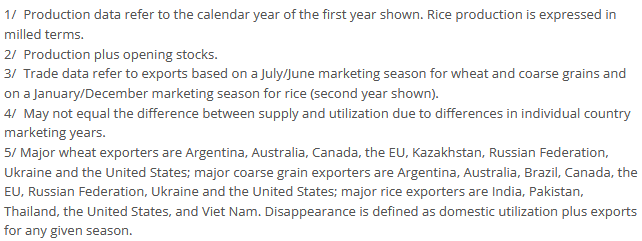

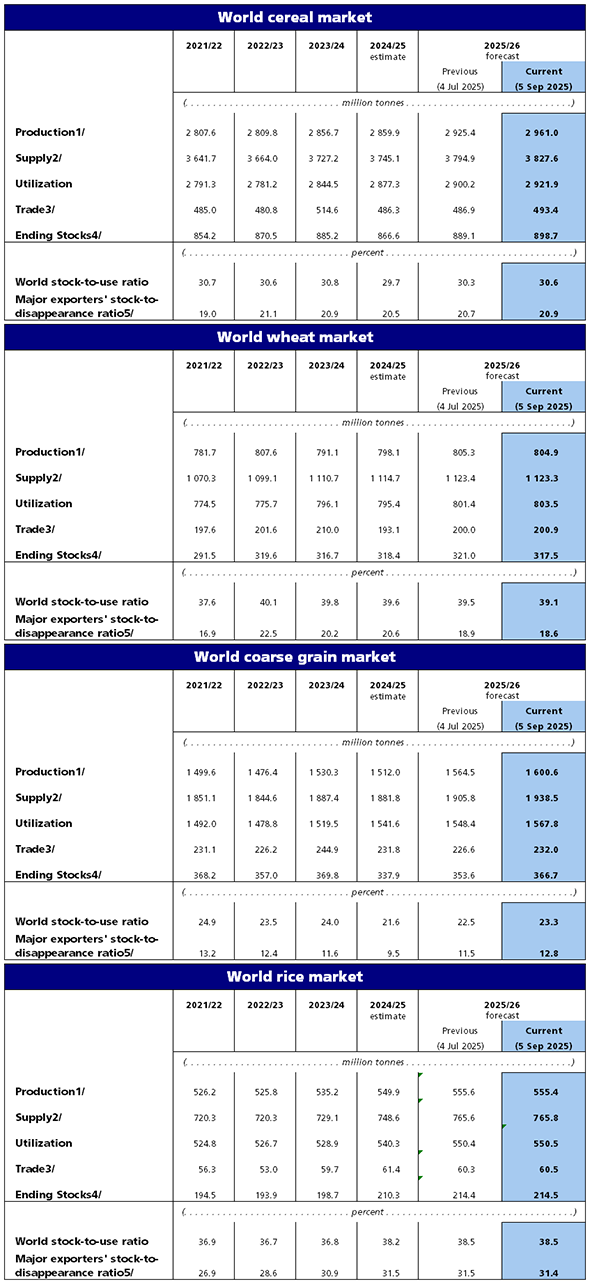

FAO’s latest forecast for world cereal production in 2025 has been revised up by 35.6 million tonnes (1.2 percent) compared to the projection from July, driven by improved prospects for coarse grain crops. This latest revision reinforces the expectation of a record-high global cereal output in 2025, which is now anticipated at 2 961 million tonnes, 3.5 percent above the previous year’s level.

The global production forecast for coarse grains in 2025 has been lifted to 1 601 million tonnes, a sharp increase of 36.1 million tonnes compared to July, and now at 88.6 million tonnes (5.9 percent) above 2024’s level. The marked upward revision is primarily due to a sizable increase in the maize output forecast in the United States of America, reflecting record-high yields and updated area estimates. Positive revisions to maize production outlooks are also made for Brazil and Mexico, driven by, respectively, higher yields and larger planted area to the main crop. Contrastingly, maize production forecasts have been trimmed in the European Union, as dry weather and higher-than-average temperatures are expected to reduce both harvested area and yields. Global sorghum production is also revised higher this month, by 2.2 million tonnes, to 66.6 million tonnes, 5.6 percent above the previous year’s level. The revision largely stems from better yield prospects in Brazil, which put the 2025 sorghum outturn at a record level. FAO’s forecast for the world wheat output stands at 804.9 million tonnes, marginally down from the previous projection in July, but 6.9 million tonnes higher year-on-year. The downward revision is mostly due to lower yield prospects in China (mainland) on account of adverse weather conditions and a smaller-than-expected acreage in Argentina. Partly offsetting these declines, upward adjustments have been made to the wheat production forecast in the European Union, driven by weather-improved prospects for yields. As for rice, FAO has downgraded its production forecast for Nepal, reflecting lower area and yield expectations owing to unconducive rains over parts of the country. Official forecasts have also been downscaled in the United States of America, where spring floods in southern producing areas compounded on prospects of reduced producer margins. However, these revisions are largely compensated by output upgrades for various other countries, most notably Indonesia, where favourable price prospects are now seen lifting plantings to seven-year highs. As a result, world rice production remains forecast to expand by 1.0 percent in 2025/26 to a record high of 555.5 million tonnes (milled basis). Production expansions in Bangladesh, Brazil, China, India, and Indonesia are anticipated to sustain the annual growth, more than compensating for contractions namely in Madagascar, Nepal, the United States of America, and Thailand.

The forecast for world cereal utilization in 2025/26 has been increased by 21.7 million tonnes since July, reaching 2 922 million tonnes, up 44.6 million tonnes (1.6 percent) from the 2024/25 level. Total utilization of coarse grains is forecast to rise by 1.7 percent to 1 568 million tonnes in the 2025/26 season due to increased use of maize and, to a lesser extent, sorghum. Amid plentiful supplies, use of maize for animal feed is seen rising in major producers Brazil and the United States of America while falling in Argentina. Feed use of barley in Saudi Arabia is revised upward, albeit to a level still below that of previous season. Feed use of wheat is also revised upwards this month, specifically in the European Union and in Thailand, where demand is increasing from the aquaculture sector. Global wheat utilization in 2025/26 is now forecast at a record level of 803.5 million tonnes, up 8.1 million tonnes from the 2024/25 level, with wheat expected to be increasingly incorporated into animal feed rations in China. FAO’s forecast of world rice utilization has changed little, pointing to 550.6 million tonnes being used in 2025/26, up 1.9 percent year-on-year and a record high.

The forecast for world cereal stocks by the close of seasons in 2026 has been raised by 9.6 million tonnes since July, with global reserves now seen reaching 898.7 million tonnes, 3.7 percent above their opening levels and a record. This month’s upward revision is attributed to an upgrade to stocks of coarse grains, outweighing a downgrade to stocks of wheat. Among coarse grains, the bumper output in the United States of America is expected to result in significantly larger reserves of maize than previously anticipated with stocks in that country at the end of the 2025/26 season foreseen to reach a record level of over 50.0 million tonnes. Conversely, global wheat stocks are forecast lower than in July and are now expected to remain near to their opening levels after downward revisions to the Islamic Republic of Iran, where the production outlook is reduced and to the European Union, where a historical revision made to human consumption over previous seasons results in a lowering of 2025/26 ending stocks by 1.8 MMT. The global cereal stocks-to-use ratio in 2025/26 is expected to reach 30.6 percent, an increase of almost one percent on the previous season, confirming the comfortable supply outlook. World rice stocks at the close of 2025/26 marketing years remain forecast to expand by 2.0 percent to a record high of 214.5 million tonnes, sustained by buildups namely in Brazil, China, India, and Thailand, which could overshadow drawdowns namely in Indonesia, Madagascar, and the United States of America.

FAO’s forecast for world trade in cereals in 2025/26 is pegged at 493.4 million tonnes, up 6.5 million tonnes from the July forecast and pointing to a 1.4 percent increase from the 2024/25 level. This month’s upward revision is due mainly to an increase in trade of coarse grains, predominantly maize. Abundant exportable supplies of maize from bumper crops in Brazil and the United States of America are expected to attract importing countries and are behind a 5.1-million-tonne upward revision to maize trade, even though China is expected to continue its reduced purchases of maize in 2025/26. Barley trade is raised only slightly since July, despite lower prices and stronger demand expected from livestock farmers in Saudi Arabia. Trade in wheat in the new season is seen rising by 4.0 percent, or 7.8 million tonnes with continued strong demand from China, the Islamic Republic of Iran, Pakistan, Syrian Arab Republic and Türkiye. Among exporting countries, the major players will continue to supply markets with the European Union expected to regain market share after a reduced harvest in 2024. International trade in rice is anticipated to reach a fresh peak of 61.4 million tonnes in 2025 (January-December), up 2.9 percent year-on-year and 0.6 million tonnes more than previously reported. Bangladesh accounts for much of the import revision introduced this month, although imports were also raised namely for Ghana and Guinea-Bissau, more compensating for downward corrections for various other countries.

-

Global cereal production projected at all-time high, but uncertainties persist Release date: 04/07/2025

FAO’s latest forecast for global cereal production in 2025 has been lifted by almost 14 million tonnes (0.5 percent) in July compared to the previous month, and is now pegged at 2 925 million tonnes. The revised outlook is driven by improved prospects for wheat, maize and rice (in decreasing order of magnitude) and puts the forecast of the global output 2.3 percent above the previous year’s level, marking an all-time high. Global wheat production has been raised by 0.7 percent in July over the previous month’s level, now standing at 805.3 million tonnes in 2025, up 0.9 percent year on year. The monthly increase primarily reflects recent official data from India and Pakistan pointing to better-than-expected yields, with a record output forecast in the former country. Global coarse grain production is also revised marginally higher this month to 1 262 million tonnes, now standing 3.5 percent above the previous year’s level, and remaining the main driver behind global production growth this year. Most of the coarse grains quantity is comprised of maize and the improved prospects this month are driven by stronger maize yields in Brazil and an upgrade to the maize production outlook for India, where robust domestic demand for feed and industrial use is seen encouraging a larger area in 2025 compared to preliminary expectations. These positive revisions more than offset cuts to production forecasts in Ukraine where, in addition to the effects of the conflict, dry-weather conditions are weakening yield prospects, and in the European Union, owing to a minor revision to the area. Expectations of hotter and drier-than-average conditions in the coming months in parts of the northern hemisphere could impact yield potential, particularly for maize with plantings almost complete. As for rice, since June, FAO has raised its forecast of global rice production in 2025/26 by 4.1 million tonnes. The revision largely stems from upward adjustments to 2024/25 and 2025/26 production expectations for India, although crop prospects also improved for Bangladesh, Pakistan, and Viet Nam, in most cases owing to higher area expectations. By contrast, forecasts were downgraded for Iraq and the United States of America. Taking these adjustments into account, FAO now anticipates global rice production in 2025/26 to reach 555.6 million tonnes (milled basis), up 1.0 percent year-on-year and a record high.

The forecast for world cereal utilization in 2025/26 stands at 2 900 million tonnes, up 2.0 million tonnes since June and 0.8 percent higher than in 2024/25. Global coarse grain utilization in 2025/26 has been raised by 4.7 million tonnes, stemming from higher utilization of each major coarse grain (barley, maize and sorghum) than initially expected, bringing the forecast to 1 548 million tonnes, a marginal increase of 0.3 percent above the 2024/25 level. By contrast, world wheat utilization in 2025/26 has been lowered this month, by 4.0 million tonnes, underpinned by downward revisions to the forecast for China (mainland), Morocco, and the United States of America. Despite the downward adjustment, global wheat utilization is still projected to rise by 0.8 percent in 2025/26 from its 2024/25 level. FAO forecasts world rice utilization to reach 550.4 million tonnes in 2025/26, up 1.8 percent from the 2024/25 high, thanks to an expansion in food intake and, to a lesser extent, continued growth in use of rice for ethanol production in India.

FAO’s forecast for world cereal stocks by the close of seasons in 2026 has been raised by 15.5 million tonnes since the previous month to 889.1 million tonnes, pointing to a 2.2 percent rise compared to opening levels. Based on the latest forecasts, the global cereal stocks-to-use ratio would rise from 29.8 percent in 2024/25 to 30.3 percent in 2025/26, indicating sufficient supply prospects in the new season. The increase is linked to wheat, with the forecast for global stocks lifted by 11.0 million tonnes this month. Most of the upward revision is concentrated in Australia, China (mainland), Pakistan, the Russian Federation, and the United States of America. Following this upward revision, global wheat stocks are now expected to rise above their opening levels by 0.9 percent, reaching 321.0 million tonnes. Pegged at 353.6 million tonnes, global coarse grain stocks are lowered marginally (by 0.5 million tonnes) this month, stemming from a downward revision to barley stocks (mostly in Australia, China (mainland), and the Russian Federation), but are still set to increase by 3.6 percent above their opening levels in 2025/26. FAO has raised its forecast of world rice stocks at the close of the 2025/26 marketing seasons by 5.0 million tonnes to a fresh peak of 214.4 million tonnes. Much of this revision reflects prospects of higher reserves in India, consistent with the improved production outlook for the country and despite expectations of record-breaking Indian exports over the season. Carry-over forecasts are also raised for Bangladesh, Ecuador, and Pakistan.

International cereal

trade

in 2025/26 is expected to increase by 1.2 percent from the 2024/25 level, reaching 486.9 million tonnes, unchanged from the previous forecast. Standing at 226.6 million tonnes, global trade in coarse grains in 2025/26 (July/June) is forecast to decline by 0.6 percent from the 2024/25 level. Accounting for that decline, global maize trade is anticipated to decrease by 1.9 percent in 2025/26. The global maize trade forecast remains nearly unchanged this month at 182.8 million tonnes as a downgrade to exports from Ukraine is offset by an increase in Uganda’s exports, reflecting changes in production prospects in both countries. By contrast, international trade in barley and sorghum is projected to rise in 2025/26 (July/June) by 2.8 percent and 15.3 percent, respectively. The forecast for global wheat trade in 2025/26 (July/June) still indicates an increase of 4.0 percent from last season’s reduced level but has been trimmed by 0.6 million tonnes since the previous forecast to 200.0 million tonnes, reflecting a downward revision in the export forecast for the Russian Federation, which outweighs higher export prospects for Australia and Ukraine. On the import side, the decline is attributed to slightly lower imports anticipated for China (mainland), Morocco, and the United Arab Emirates. Following slight upward adjustments to export prospects for Cambodia and Viet Nam, FAO now anticipates international trade in rice to amount to 60.8 million tonnes in 2025 (January-December), up 2.0 percent from 2024 and an all-time high.

-

World cereal trade and stocks declined in 2024/25 with recovery expected in 2025/26 Release date: 06/06/2025

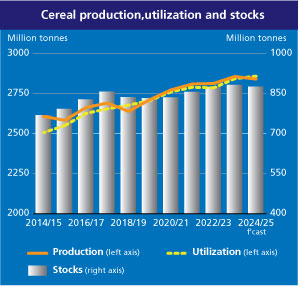

As the 2024/25 (July/June) marketing season concludes, global cereal production for 2024 is estimated at 2 853 million tonnes, representing a slight decrease of 0.1 percent compared to the 2023 output. This decline is attributed to a reduction in coarse grain production, particularly maize, which offset the increases in wheat and rice outturns. At 2 875 million tonnes, world cereal utilization in 2024/25 is estimated 1.2 percent above its 2023/24 level, reflecting growth in utilization of coarse grains (mostly maize and sorghum) and rice. As a result of the growth in utilization amidst stagnant production, cereal stocks at the end of seasons in 2025 are estimated 2.0 percent below their opening levels, at 865 million tonnes. The decline in cereal stocks stems entirely from a drawdown of barley and maize, which is partially offset by stock buildups of rice and, to a lesser extent, wheat. Pegged at 478 million tonnes, FAO’s estimate for global cereal trade in 2024/25 points to a 6.9 percent decrease below the 2023/24 level. The decline is driven by a sharp fall in global trade of wheat and all major coarse grains. By contrast, global trade of rice in 2024/25 is estimated above its 2023/24 level.

Looking forward to the 2025/26 season, world cereal production (including rice in milled equivalent) is expected to reach a record 2 911 million tonnes in 2025, surpassing the 2024 output by 2.1 percent. Production of all major cereals is anticipated to rise, with the largest year-on-year increase (in percentage terms) forecast for maize and the smallest for wheat. Maize, rice and sorghum outputs are all predicted to reach new record highs.

World cereal utilization is forecast to increase by 0.8 percent in 2025/26, reaching 2 898 million tonnes. Global food consumption of cereals is predicted to grow by 0.9 percent from 2024/25, while feed use is forecast to expand by 0.5 percent, with increases expected for all major cereals. Other uses of cereals are projected to rise by 1.0 percent, led by increased uses of wheat and rice.

With world cereal production expected to exceed utilization in 2025/26, world cereal stocks are predicted to expand by 1.0 percent (8.3 million tonnes) above their opening levels to 873.6 million tonnes. This would mark a partial recovery from the contraction recorded in 2024/25. The bulk of the anticipated increase is due to higher inventories expected for coarse grains, while a smaller rise is expected for rice. By contrast, wheat stocks are forecast to decline. Based on the current forecasts, the global cereal stock-to-use ratio should remain close to the 2024/25 level, at 29.8 percent.

After contracting by nearly 7.0 percent in 2024/25, global cereal trade is predicted to partially recover in 2025/26, rising by 1.9 percent to 487.1 million tonnes. The rebound is expected to be led by a 3.8 percent growth in global wheat trade, supported by a modest 0.9 percent increase in coarse grain trade. By contrast, international trade in rice is predicted to contract by 0.7 percent.

For a more detailed analysis of global cereal markets, see the forthcoming issue of Food Outlook, which will be released on 12 June 2025.

Summary Tables

-

Supply tightens slightly as 2024/25 marketing season wraps up; production outlook for 2025 wheat crop remains favorable

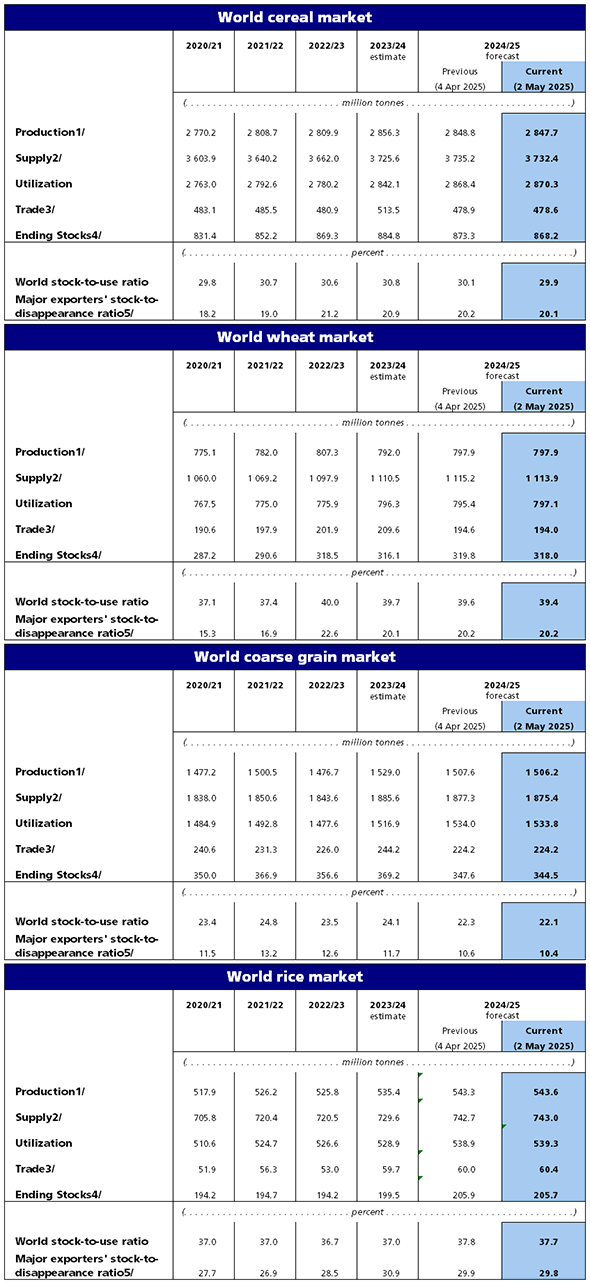

Release date: 02/05/2025

FAO has slightly lowered its estimate for global cereal production in 2024 by 1.1 million tonnes compared to the April figure. The global cereal output is now pegged at 2 848 million tonnes, remaining marginally lower year on year, largely due to a reduced world maize outturn. FAO’s forecasts of rice production in 2024/25 have changed only marginally since April. As a result, and largely due to a robust expansion in area planted, global rice output is forecast to expand by 1.5 percent year-on-year in 2024/25 to reach an all-time high of 543.6 million tonnes (milled basis).

The world cereal utilization for 2024/25 is forecast at 2 870 million tonnes, an increase of 1.9 million tonnes from last month and 28.2 million tonnes (1.0 percent) above the 2023/24 level. Global wheat utilization for 2024/25 is raised by 1.8 million tonnes, primarily reflecting higher expected use in Argentina and the European Union, bringing the forecast to 797 million tonnes, up fractionally (0.1 percent) from previous season. FAO’s projection for global coarse grain utilization in 2024/25 remains nearly unchanged at 1 534 million tonnes, indicating to a 1.1 percent growth from the 2023/24 level. The anticipated increase is mostly driven by higher feed use of maize, especially in China and the Russian Federation. Largely reflecting more buoyant use expectations for various countries located in Africa, FAO’s forecast of world rice utilization has been raised by 0.4 million tonnes since April to 539.4 million tonnes. At that level, world rice uses would stand at a fresh peak and exceed the previous season’s estimate by 2.0 percent.

The forecast for world cereal stocks by the close of season in 2025 is lowered further this month, by 5.1 million tonnes, bringing the forecast to 868.2 million tonnes, indicating a decline of 16.6 million tonnes (1.9 percent) below opening levels. The latest forecasts indicate that the world cereal stocks-to-use ratio in 2024/25 would stand at 29.9 percent, down from 30.8 percent in 2023/24, but still at a relatively comfortable level. Global wheat stocks are revised down by 1.9 million tonnes this month, mostly reflecting lower stock estimates in the European Union and Türkiye. Despite the downward revision, global wheat stocks are still forecast to increase marginally above opening levels, by 0.6 percent, to 318 million tonnes in 2024/25. Global coarse grain stocks are also lowered this month, by 3.1 million tonnes, on account of lower maize stocks, especially in the United States of America due to largest exports. The downward revision this month further lowers the forecast of global coarse grain stocks at the end of seasons in 2024/25 to 344.5 million tonnes, representing a 6.7 percent fall from opening levels with most of the decline attributed to a drawdown of global maize stocks. FAO’s forecast of world rice stocks at the close of 2024/25 marketing seasons has changed little since April, continuing to point to global reserves rising 3.1 percent above their already ample opening level to reach an all-time high of 205.7 million tonnes. At a country level, China, India, Indonesia, and the Philippines are seen spearheading the forecast stock expansion, which alongside build-ups in other countries could overshadow expected drawdowns in reserves namely in Japan, the Republic of Korea and Myanmar.

Nearly unchanged this month, world trade in cereals in 2024/25 is still forecast at 478.6 million tonnes and is expected to decline by 6.8 percent from the 2023/24 level. Global wheat trade in 2024/25 (July/June) is lowered marginally this month, by almost 1.0 million tonnes, mostly reflecting another downgrade in the Russian Federation’s export volumes and smaller purchases by Türkiye. With this further downward revision, global wheat trade in 2024/25 (July/June) is forecast to contract by 7.4 percent from the 2023/24 level to 194.0 million tonnes. The forecast for global trade in coarse grains in 2024/25 (July/June) still stands at 224.2 million tonnes, pointing to an 8.2 percent decline from the 2023/24 level. The steep decline stems from anticipated contractions in trade volumes of all major coarse grains (barley, maize and sorghum). These declines are largely driven by lower demand from China, the worlds largest coarse grain importer, as well as smaller exportable supplies in some of the major exporters, including maize in Brazil and barley in the Russian Federation. International trade in rice is now seen reaching 60.4 million tonnes in 2025 (January-December), up 1.2 percent from the 2024 all-time high and little changed from April expectations.

Looking ahead to 2025

Global prospects for wheat production remain mostly unchanged from the previous month, with only minor adjustments made due to weather-related developments. FAO’s latest forecast for 2025 wheat production stands at 795 million tonnes, on par with the previous year’s output.

In Europe, the wheat production forecast for the European Union has been revised slightly higher this month, as improved weather conditions in southern countries bolstered overall yield expectations, reinforcing the outlook of a strong production rebound in 2025 following the low of 2024. However, developing dryness in northern areas, marked by rainfall deficits and warmer-than-usual temperatures, poses a slight downside risk. In the United Kingdom of Great Britain and Northern Ireland, a higher-than-expected wheat area has edged the production forecast upward and closer to the five-year average, but as in some other northern European Union countries, unusually warm temperatures in April have raised some concerns for yield potentials. The forecast for the Russian Federation remains unchanged, with adverse weather and a reduced area expected to result in a lower year-on-year output. In Ukraine, April rainfall helped improve crop conditions in parts after earlier dryness, but the wheat outlook still points to a below-average output largely reflecting the impact of the conflict. In Northern America, Canada’s main spring season wheat planting is underway, with production prospects still pointing to an output on par with last year’s level. In the United States of America, drought concerns persist, likely keeping total wheat production slightly below 2024 levels. In Asia, hot and dry weather conditions in India prompted a trimming to the national production forecast. However, the widespread use of irrigation has limited the impact, and a record wheat harvest is still predicted in 2025. Pakistan’s production forecast is raised slightly this month, reflecting a larger-than-anticipated area; the wheat output is forecast to slightly exceed the five-year average. In the Near East, higher precipitation volumes in April were insufficient to offset earlier rainfall deficits and warmer-than-usual temperatures, consequently wheat production expectations in Iran (Islamic Republic of) and Türkiye remain below average. In Northern Africa, the outlook is mixed: Morocco faces a below-average harvest, Algeria is forecast to harvest a near-average wheat crop, and Egypt and Tunisia (where irrigation is extensively used) are expected to see average to above-average outputs. In the southern hemisphere, where wheat plantings are underway, Argentina’s production prospects have been bolstered by predictions of better-than-expected rainfall, underpinning a small upward revision to the production forecast, which remains above the five-year average. In Australia, wheat production is forecast to fall year-on-year but remain above 30 million tonnes.

Harvesting of the 2025 coarse grain crops is beginning in southern hemisphere countries. In Brazil, good price prospects have underpinned an estimated increase in the area, while overall conducive weather conditions are likely to result in a small upturn in yields. Overall, total maize production in 2025 is pegged above last year’s outturn and the five-year average. The maize production forecast for Argentina remains unchanged this month, and below the five-year average, mostly owing to a cutback in the sown area largely on the back of fears of maize stunt disease, spread by leafhopper insects. In South Africa, total maize production is revised slightly higher in May, reflecting continued beneficial weather since the turn of the year, and the 2025 harvest is forecast to recover after the dry-weather-reduced output in 2024. Planting of coarse grains crops is underway in the northern hemisphere countries, and early expectations in the United States of America, the world’s leading producer, point to a 5 percent increase in plantings, supporting expectations of a sizeable production increase in 2025.

-

Global cereal trade in 2024/25 expected to contract to lowest level since 2019/20

Release date: 04/04/2025

FAO has revised upward the estimate for global cereal production in 2024 by 7.1 million tonnes compared to the figure of March. Standing at 2 849 million tonnes, the world cereal outturn, however, remains 0.3 percent lower year on year. This month’s positive adjustment is primarily driven by larger-than-previously anticipated wheat outturns in Australia and Kazakhstan. The world output for barley is also raised, albeit by a lesser margin compared to wheat, and is mostly linked to a more abundant harvest in Australia. World rice production in 2024/25 is forecast at a record high of 543.3 million tonnes (milled basis), little changed from March expectations and implying a 1.6 percent area-driven expansion. India is expected to account for much of the season’s anticipated growth. Good harvests in Cambodia, China and the United Republic of Tanzania, among others, could however also contribute, more than compensating for weather-driven contractions, namely in Bangladesh, Indonesia and Myanmar.

The forecast for world cereal utilization in 2024/25 stands at 2 868 million tonnes, up 1.3 million tonnes since last month and 0.9 percent above the 2023/24 level. This month’s revision is due to an upward revision of 2.7 million tonnes in the global coarse grains’ utilization forecast with higher anticipated usage of all major coarse grains (maize, barley and sorghum) than previously anticipated. This adjustment raises the coarse grains utilization forecast to 1 534 million tonnes, indicating a 1.1 percent growth from last season. Conversely, the global wheat utilization forecast, now pegged at 795.4 million tonnes, is expected to decline fractionally below previous season’s level following a downward revision of 1.4 million tonnes, primarily reflecting an adjustment in India. The forecast for global rice utilization in 2024/25 remains at 539.0 million tonnes, up 2.1 percent from 2023/24 and a fresh peak. Food intake is seen driving this expansion, on a per capita basis, growing to 53.3 kg per year. Nevertheless, and although still accounting for a limited share of world rice uses, non-food industrial uses could also stage a notable (17 percent) annual expansion, largely due to greater use of rice for ethanol production in India.

World cereal stocks by the close of the 2025 seasons are still projected to decline below opening levels by 1.5 percent, reaching 873.3 million tonnes, despite a 4.0 million tonne upward revision this month. The latest forecasts indicate that the world cereal stocks-to-use ratio in 2024/25 would stand at 30.1 percent, slightly down from 30.9 percent in 2023/24, but still at a comfortable level. The projected decline in cereal stocks rests on an anticipated 6.0 percent decline in global coarse grain stocks. A reduction in maize inventories in China, driven by lower imports, leads to a further 3.3 million tonne decrease in global coarse grain stocks, bringing the forecast to 347.6 million tonnes. By contrast, the global wheat stocks forecast is raised this month, by 7.1 million tonnes, indicating an increase of 0.8 percent above their opening levels, reaching 320 million tonnes. The bulk of this upward revision is attributed to stock increases in India, Kazakhstan, and the Russian Federation. World rice stocks at the close of 2024/25 marketing years are forecast to expand by 3.2 percent year-to-year to reach a record high of 205.9 million tonnes, reflecting expectations of stock rebuilding among importing countries, as well as another accumulation among exporting countries.

FAO’s forecast for world trade in cereals in 2024/25 has been further reduced by 5.3 million tonnes to 478.9 million tonnes, marking a 6.7 percent decrease from the 2023/24 level and the lowest since 2019/20. The global coarse grain trade forecast for 2024/25 is lowered by 3.7 million tonnes this month, with both maize and sorghum trade revised downwards due to smaller expected purchases by China. Among the exporters, maize exports from Brazil are revised downwards in line with the export pace to date, and sorghum exports from the United States of America are reduced on account of anticipated lower flows to China, its main destination. These revisions bring the global coarse grain trade forecast to 224.2 million tonnes, a steep 8.2 percent decline from the 2023/24 level. Lower expected purchases by China also lead to a 1.7 million tonne downward revision in the 2024/25 global wheat trade forecast. Smaller wheat exports from Kazakhstan and the Russian Federation further contribute to the diminished global trade outlook. Now forecasted at 195 million tonnes, global wheat trade is expected to contract in 2024/25 by 7.2 percent from previous season. International rice trade is forecast to expand by 1.0 percent in 2025 (January-December) to reach a high of 60.0 million tonnes. On the demand side, although Indonesia, the Philippines and Viet Nam look set to diminish their purchases this year, import cutbacks from these counties could be more than compensated by higher purchases, most notably, by Bangladesh, Madagascar and Nepal.

Looking ahead to 2025

FAO’s forecast for global wheat production in 2025 remains broadly unchanged since the first outlook of March. Forecast at 795 million tonnes, the 2025 world wheat output is on par with the previous year’s level following the upward revisions made this month to the 2024 estimate.

Winter wheat crop conditions in the key producing countries of the northern hemisphere have remained broadly unchanged in the last month. In the European Union, official figures place the wheat output at 135.5 million tonnes, up 12 percent year on year, based on higher plantings and yields, following the weather-induced lows of 2024. However, continued rainfall deficits in eastern areas present a moderate downside risk to yield potentials. In the Russian Federation, low soil moisture levels and a reduction in plantings are set to result in a lower output in 2025. In Ukraine, production of wheat in 2025 is pegged at a level below the five-year average, underpinned by the effects of the ongoing war, while dry weather conditions are driving expectations of a likely modest year-on-year decline. In the United States of America, total wheat production is forecast to dip in 2025, on account of lower yields, with a larger area of the winter wheat crop affected by drought conditions relative to the previous year. In Canada, with the main planting period to start in May, preliminary projections indicate a price-driven expansion in the wheat area. However, this is likely to be offset by a decline in yields, keeping production largely unchanged year on year, albeit still above the five-year average. In India, driven by a record wheat area, on the back of strong price incentives and government subsidies for agricultural inputs, production is seen increasing in 2025, with wheat production forecast at an all-time high of 115.4 million tones. In Near East Asia, widespread rainfall shortages have impacted production expectations in both Iran (Islamic Republic of) and Türkiye, increasing the likelihood of a decline in wheat harvests in 2025; access to irrigation is, however, likely to limit the downturn. In North Africa, total wheat production in 2025 is anticipated to remain below the five-year average, reflecting the effects of poor early-season rainfall, notably in Algeria and Morocco, whilst in Egypt, wheat production – primarily irrigated – is expected to increase year-on-year, amid an expansion policy by the government. In the key wheat-producing countries south of the equator, the outlook for Argentina is generally favourable, with a reduction in export tariffs and prospects of remunerative prices underlying expectations of an increase in plantings. This is likely to push up production, despite an anticipated modest drop in yields. In Australia, the early outlook points to a moderate decline in wheat production, but the harvest is still expected to exceed 30 million tonnes.

For coarse grain production in 2025, planting in the northern hemisphere will start soon, while the bulk of the crops in southern hemisphere countries will be harvested during the second quarter of the year. Maize production in Brazil is set to increase in 2025, reflecting both a modest increase in plantings, stimulated by an uptick in prices during late 2024 prior to the main season sowing period, and likely improvements in yield levels. In Argentina, a steep decrease in plantings and rainfall deficits are weighing on production prospects, and consequently the maize outturn in 2025 is expected to fall. In South Africa, a sizeable upturn in white maize plantings, driven by record prices, and good weather conditions since the start of the year are underpinning expectations of a recovery in maize production following the low of 2024.

-

Early wheat production prospects for 2025 point to potential increase

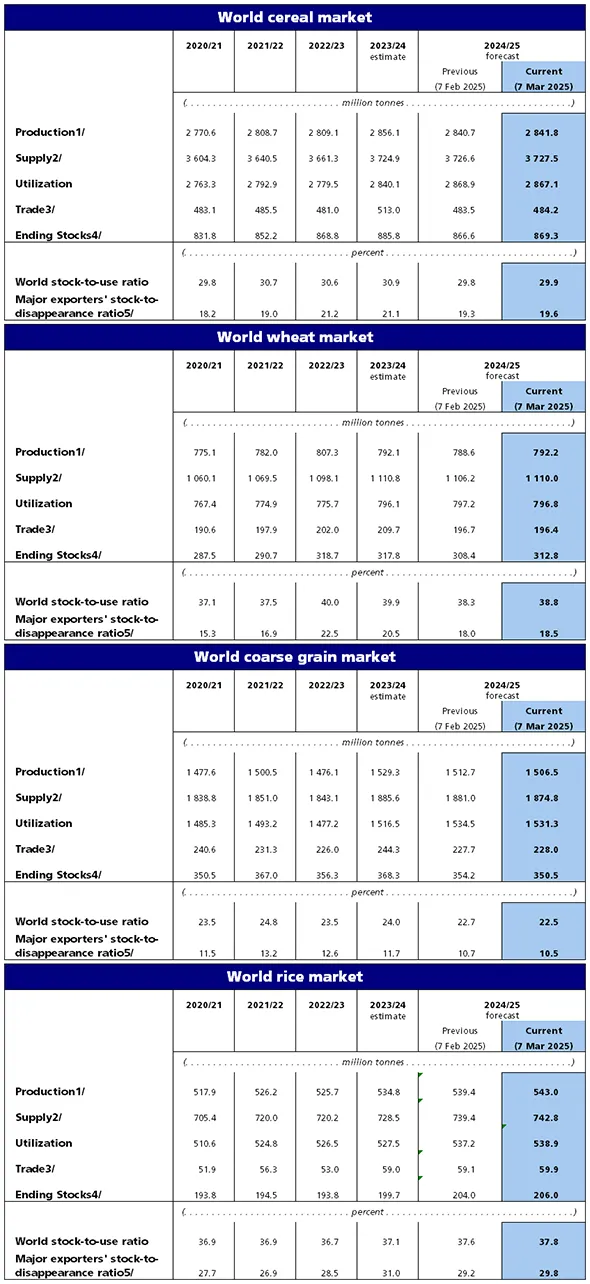

Release date: 07/03/2025

Global cereal production for 2024 has been modestly revised upward this month to 2 842 million tonnes, narrowing the gap to 2023 output, which still exceeds the 2024 level by over 14.4 million tonnes. The adjustments to the 2024 output relate mainly to wheat, mostly reflecting recent official data pointing to a larger harvest in the Islamic Republic of Iran, and for rice. Since February, FAO has upgraded its forecast of world rice production in 2024/25 by 3.6 million tonnes to a fresh peak of 543.0 million tonnes (milled basis). The revision largely reflects more buoyant crop prospects for India, where, following a record-breaking Kharif harvest, secondary crop plantings have progressed at a robust pace to date. Nevertheless, higher-than-previously-anticipated plantings of offseason crops have also boosted the production outlook for Cambodia and Myanmar. These increases in wheat and rice offset reductions made to the global coarse grain production forecast, primarily driven by a smaller-than-previously-expected barley harvest in the Russian Federation.

The global cereal utilization forecast for 2024/25 has been reduced by 1.9 million tonnes this month, but still indicates a 1.0 percent increase over the 2023/24 level, reaching 2 867 million tonnes. The world wheat utilization forecast for 2024/25 remains nearly unchanged as a decrease in food consumption is offset by an increase in other use, mostly in China (mainland). The forecast for 2024/25 global coarse grain utilization has been lowered by 3.2 million tonnes to 1 531 million tonnes, reflecting a 1.0 percent decrease from 2023/24. This reduction is due to a cut in maize feed use (primarily Indonesia) as well as other use of barley (in South Africa, Thailand, and the United Kingdom of Great Britain and Northern Ireland). On the other hand, ample supplies are expected to facilitate world rice utilization to expand at an accelerated rate of 2.2 percent in 2024/25 to reach 539.0 million tonnes. This level would represent an all-time high and stands 1.7 million tonnes above February expectations.

Despite an upward revision of 2.7 million tonnes this month, global cereal stocks ending in 2025 are still expected to decline by 1.9 percent compared to opening levels to 869.3 million tonnes. The global cereal stocks-to-use ratio is expected to decrease from 30.9 percent in 2023/24 to 29.9 percent in 2024/25, still indicating a comfortable global supply situation. World wheat stocks are anticipated to decline by 1.6 percent to 312.8 million tonnes, despite an upward revision of 4.4 million tonnes this month, mostly due to higher imports in Egypt, increased production in the Islamic Republic of Iran and reduced exports from the Russian Federation. By contrast, global coarse grain inventories are further reduced by 3.7 million tonnes, and are now forecast to be 4.8 percent below their opening levels. The downgrade is primarily due to lower imports in China (mainland) and reduced domestic production in Indonesia and the Russian Federation. World rice stocks at the close of 2024/25 marketing seasons are forecast to expand by 3.1 percent year-on-year to a record high of 206.0 million tonnes. This level stands 2.0 million tonnes above February expectations, as upgrades to stock forecasts for Cambodia and, especially India, outweighed cutbacks to expected reserves namely in Myanmar.

The global cereal trade forecast for 2024/25 is pegged at 484.2 million tonnes, a slight increase of 0.7 million tonnes from last month, but still indicating a 5.6 percent decline from previous season. World wheat trade in 2024/25 (July/June) has been revised down marginally by 0.4 million tonnes since the last report, now expected to be 6.4 percent below its level in 2023/24. This month’s revision mostly reflects a cut to the export forecast for the Russian Federation and a downgrade in Türkiye’s imports. The forecast for global trade in coarse grains edges upwards fractionally (0.3 million tonnes), driven by higher maize trade prospects due to greater exports from Brazil and larger imports by Türkiye, but it is still projected to contract by 6.7 percent from 2023/24. Upgrades to import prospects for Bangladesh, Madagascar and various other countries have raised FAO’s forecast of international trade in rice in 2025 (January-December) by 800 000 tonnes to 59.9 million tonnes, implying a 1.5 percent increase from 2024 and a fresh trade peak.

Early outlook for 2025 crops

FAO’s preliminary forecast for global wheat production in 2025 indicates a modest increase, with world output projected at 796 million tonnes, a near 1 percent rise year-on-year. This growth is largely driven by expected production gains in the European Union, following a decline in 2024. Estimates suggest an increase in sowings, primarily for soft wheat, with most of the expansion centered in France and Germany. The average wheat yield among European Union countries is also expected to rise year on year; however, developing dry conditions in the east and excessive rainfall in the west, particularly in France, may limit these gains. In the United Kingdom of Great Britain and Northern Ireland, the winter wheat area is forecast to rebound after a 2024 reduction caused by overly wet conditions during the autumn planting period, leading to a modest production increase in 2025. In the United States of America, the total wheat area is expected to expand in 2025, driven by an increase in winter sowings and a likely rise in spring wheat acreage, potentially replacing some soybean plantings. Yields are projected to decline moderately year-on-year due to a greater portion of the winter wheat crop facing mild drought conditions compared to 2024. As a result, total wheat production is expected to decrease slightly, reaching 52.5 million tonnes. In Canada, early projections indicate an expansion in wheat plantings, supported by better soil moisture conditions and expectations of strong prices later in the year. Assuming a return to average yields, wheat production is forecast at 35 million tonnes, in line with 2024’s output. In the Russian Federation, winter wheat acreage has declined for a third consecutive year. Combined with low soil moisture levels and thin snow cover, which raises the risk of frost damage, production is forecast to fall by 2 percent year-on-year to 80 million tonnes. Ukraine’s 2025 wheat area remains below average due to the ongoing war, which continues to restrict field access, strain finances, and damage infrastructure, reducing profitability of the sector. Rainfall deficits have further weakened yield prospects, and production is projected to decline moderately year-on-year. In India, wheat plantings have reached a record level in 2025, supported by strong price incentives and government subsidies for agricultural inputs. Yields, however, are forecast to decline slightly, keeping production unchanged year-on-year at 113 million tonnes. In China, mid-February field assessments indicate favourable wheat crop conditions. The crop has recently broken dormancy in northern regions, while in eastern and central parts, it is progressing through the tillering and jointing stages. Production is expected to remain stable year-on-year and above the five-year average at 140 million tonnes. In Pakistan, wheat production is projected to decline to a near-average level in 2025, primarily due to lower yields. This reflects dry conditions that affected rainfed wheat crops and caused irrigation water shortages in northern regions. In Near East Asia, primarily Iran (Islamic Republic of) and Türkiye, rainfall deficits since late 2024 have curbed plantings and lowered yield expectations. Consequently, in both countries, wheat production is projected to fall in 2025, possibly slipping below the five-year average. In North Africa, total cereal production is anticipated to remain below average in 2025, as poor early-season rainfall delayed plantings and lowered yield potential, particularly in rainfed areas.

South of the equator, a surge in domestic maize prices in Brazil during late 2024 encouraged increased maize plantings for the main season, following below-average sowings of the minor maize crop, which is currently being harvested. Assuming normal weather patterns until the harvest period that starts in June, production expectations remain positive for 2025. In Argentina, dry conditions during sowing and early growth stages have limited yield potential. Coupled with reduced plantings due to concerns over stunt disease (spiroplasma) outbreaks, maize production is projected to be below average in 2025. In South Africa, overall maize production is forecast to increase in 2025, supported by expanded white maize acreage — driven by record prices — and a likely rebound in yields following drought-induced declines in 2024.

-

Cereal stocks set to decline in 2024/25 due to anticipated reductions in wheat and maize inventories

The latest forecast for global cereal production in 2024 has been marginally scaled back from the previous month and remains at just under 2 841 million tonnes, 0.6 percent lower year on year. The latest downward revision is primarily due to a significant reduction in the United States of America maize estimate, where late-season moisture stress curbed yields below earlier expectations. Partially offsetting this decline, production estimates for China (mainland) and the European Union were revised upward. Global barley and wheat forecasts were also trimmed marginally, based on latest data from Australia and the European Union showing smaller harvests than previously foreseen. As for rice, official production assessments released since December reported somewhat higher rice production outcomes in China, Mali, Nepal, and Viet Nam compared to previous FAO expectations, which offset slight output downgrades namely for the Philippines and Senegal. As a result, global rice production is now seen reaching an all-time high of 539.4 million tonnes (milled basis) in 2024/25, up 0.6 million tonnes from December expectations and 0.9 percent more than in 2023/24.

Turning to the 2025 crops, the main planting period for winter wheat in northern hemisphere countries came to an end in January. In the European Union, early indications point to an increase in sowings, largely for soft wheat, with most of the expansion originating in France and Germany. Weather conditions have generally been favorable in preceding months, and although drier-than-average conditions are expected in February, wheat yields are anticipated to improve in 2025 following last year’s lows, further strengthening prospects for a production recovery. In the United Kingdom of Great Britain and Northern Ireland, the winter wheat area is expected to rebound after difficult planting conditions limited the cultivated area last year. In the Russian Federation, less-than-favorable weather has contributed to a reduction in plantings, and combined with unseasonably warm temperatures in early 2025, which have thinned snow cover and increased the risk of winterkill, production may decline slightly. In India, remunerative prices and continued favorable weather conditions are supporting an overall positive production outlook for the 2025 wheat crop.

In the main coarse grain-producing southern hemisphere countries, the 2025 crop is expected to be harvested from the second quarter of the year. In Argentina, maize area is projected to decline year-on-year, reflecting farmers' concerns about the impact of stunt disease transmitted by leafhoppers, which affected production in 2024. However, with expectations of beneficial weather over the next two months, yield prospects remain generally favorable. In Brazil, firmer maize prices could encourage a slight increase in total plantings compared to preliminary expectations, while yields are expected to improve year on year. However, some concerns remain over the delayed sowing of the soybean crop, which could, in turn, delay the planting of the main safrinha maize crop. In South Africa, record-high maize prices triggered an increase in maize plantings. Weather conditions have improved following uneven rainfall in the last quarter of 2024, and yield prospects remain at average to above-average levels.

World cereal utilization in 2024/25 is forecast to rise by 0.9 percent (24.5 million tonnes) above the 2023/24 level, reaching 2 869 million tonnes, up 9.8 million tonnes since the December report. Accounting for the bulk of the increase, an 8.4 million tonne upward revision in the 2024/25 coarse grain utilization, mostly due to higher foreseen use of maize, especially for feed, brings the forecast to 1 535 million tonnes, 1.0 percent (14.7 million tonnes) above its 2023/24 level. By contrast, at 797.2 million tonnes, the global wheat utilization forecast for 2024/25 is up only marginally (0.8 million tonnes) since the December report and remains near last season’s level with an anticipated increase in food consumption offsetting a decline in feed use of wheat this season. World rice utilization is forecast to expand by 1.9 percent in 2024/25 to reach a fresh peak of 537.2 million tonnes. This forecast stands some 500 000 tonnes above December expectations, reflecting upward revisions to use expectations for a host of African countries, which more than compensated for a less buoyant domestic use outlook namely for India.

FAO’s latest forecast for world cereal stocks by the close of seasons in 2025 has been revised downwards by 7.8 million tonnes, now pointing to a 2.2 percent decline (19.3 million tonnes) below opening levels to 866.6 million tonnes. Despite the expected decline in stocks, the global cereal stocks-to-use ratio in 2024/25 is anticipated to remain at a comfortable level of 29.8 percent, albeit down from the 2023/24 level of 30.9 percent. Total coarse grain stocks have been lowered by 6.1 million tonnes since the previous forecast to 354.2 million tonnes, pointing to a 3.8 percent (14.1 million tonnes) decline from opening levels. The revision largely rests on a sharp cut (10.1 million tonnes, 20.5 percent) in the United States of America’s maize stocks as a result of lower production and higher export prospects since the previous report. Global wheat inventories were also lowered this month, by 1.3 million tonnes, to 308.4 million tonnes, representing a decline of 2.9 percent below opening levels. The revision is underpinned by a 3-million-tonne reduction in China’s wheat stocks on account of their lower anticipated wheat imports. FAO’s forecast of world rice stocks at the close of 2024/25 marketing years has been trimmed by 500 000 tonnes since December. Nevertheless, it continues to point to world rice stockpiles expanding by 2.0 percent to a historical high of 204.0 million tonnes, on the back of expected stock rebuilding among rice importing countries, as a group, and a still ample aggregate level of reserves in rice exporting countries.

Remaining nearly unchanged since the previous forecast at 483.5 million tonnes, world

trade

in cereals in 2024/25 is headed for a contraction of 5.6 percent (28.7 million tonnes) from the 2023/24 level. Global coarse grains trade in 2024/25 (July/June) stands at 227.7 million tonnes, down 6.8 percent (16.5 million tonnes) from its 2023/24 level. Weaker demand from China for barley and maize drove downward revisions in both global trade of barley (down 2.1 million tonnes m/m) and maize (down 0.7 million tonnes m/m). Lower forecasts of barley exports from Australia and the European Union, and of maize exports from Brazil, India and the Russian Federation also contributed to the weaker trade prospects. FAO’s wheat trade forecast for 2024/25 (July/June) has also been revised downwards since December, by 1.5 million tonnes, to 196.7 million tonnes. China’s import forecast has been lowered to its lowest level of wheat imports since 2019/20, reflecting slower-than-previously anticipated import pace to date and expectations of reduced domestic demand for feed use of wheat. Export sales were lowered for the European Union, on account of tighter supplies, and the Russian Federation due to slowing export pace as well as an export quota (of 10.6 million tonnes) for the period from mid-February to the end of June, the country’s lowest wheat export quota in five years. International trade in rice in 2025 (January-December) is now seen reaching 59.1 million tonnes, up from a revised estimate of 58.4 million tonnes for 2024 and 3.5 million tonnes more than reported in December. India remains forecast to drive the export expansion of 2025, although Brazil, Myanmar and Uruguay are also expected to step-up shipments over the course of the year.

-

Cereal trade revised downwards amid weaker demand

The latest forecast for global cereal production in 2024 has been revised downward from the previous month and now stands at 2 841 million tonnes. At this level, the world cereal output is 0.6 percent lower year on year but remains the second largest on record. The reduction this month primarily reflects downward revisions to maize and wheat production forecasts. The global maize output, accounting for about 80 percent of the coarse grains total, is pegged at 1 217 million tonnes, slightly lower than the previous month's forecast and 1.9 percent below the 2023 level. The adjustment is driven by lower-than-expected yields in the European Union and the United States of America. Similarly, the global wheat production forecast for 2024 has been marginally reduced to 789 million tonnes, which is now on par with the 2023 outturn. The bulk of the month-on-month decrease is linked to a lower wheat estimate in the European Union, where overly wet conditions curbed yields in parts. As for rice, FAO’s forecast of world rice production in 2024/25 has changed little since November. Thus, it continues to point to area expansions resulting in a 0.8 percent annual increase in global rice output to a record high of 538.8 million tonnes (milled basis).

Turning to the 2025 crops, planting of the winter wheat crop is underway across the northern hemisphere, and softer prices in 2024 may dissuade area expansions. In the United States of America, sowing of the winter wheat crop is progressing at an average pace and, owing to recent beneficial rainfall, 55 percent of winter crops are rated as good to excellent at the end of November, 5 percentage points higher than last year. In the European Union, sowing operations were delayed due to a wet start of the autumn period in western areas, particularly in southern Spain. While dry conditions in November accelerated the sowing pace, continued water deficits in eastern countries hindered early crop development in some regions. Below-normal rainfall in key southern wheat-growing areas in the Russian Federation has led to low soil moisture levels, hampering planting operations. Less-than-favourable weather conditions also impeded sowings in Ukraine, where the war continues to be a major impediment to the agriculture sector. In Far East Asia, remunerative prices and government support policies, coupled with favourable soil moisture conditions, are likely to see similar-sized wheat plantings in China (mainland) and India for the 2025 crop, with potential for expansions.

In the southern hemisphere, the 2025 coarse grain crops are being planted. In South America, early signs point to a pullback in Argentinian maize sowings, as farmers have been discouraged by dry conditions and the risk of stunt disease transmitted by leafhoppers, which adversely affected production in 2024. In Brazil, early planting intentions point to an unchanged maize area for the 2025 crop, and a return of rainfall in central and southeastern regions has bolstered prospects of an increase in yields following a small downturn last year. In South Africa, preliminary expectations point to an unchanged maize area, as an anticipated increase in white maize sowings, buoyed by record prices, is expected to offset a likely contraction, albeit small, in the yellow maize area.

World cereal utilization in 2024/25 is forecast at 2 859 million tonnes, up 1.8 million tonnes from the previous month and 0.6 percent higher than in 2023/24. Global coarse grain utilization in 2024/25 is raised month on month by 1.2 million tonnes to 1 526 million tonnes, now 0.4 percent above levels in 2023/24. The upward revision stems from fractionally higher feed use, mostly of sorghum, and industrial use of maize. Nearly unchanged from last month, global wheat utilization in 2024/25 is forecast to remain near last season’s level at 796 million tonnes, with growth in food consumption seen balancing a decline in feed use of wheat. FAO has raised its forecast of world rice utilization in 2024/25 by 900 000 tonnes since November, largely reflecting prospects of more pronounced use expansions in Asia. As a result, global rice utilization is now forecast to reach 536.7 million tonnes, which would represent a 2.0 percent increase from 2023/24 and an all-time high.

FAO’s forecast for world cereal stocks by the close of seasons in 2025 has been cut by 14.2 million tonnes since the previous month to 874 million tonnes, now pointing to a decline in global stocks of 0.7 percent below the opening levels. Based on the latest forecast, the global cereal stock-to-use ratio would be 30.1 percent in 2024/25, down from 30.8 percent in 2023/24 but still indicating a comfortable supply level. Following this month’s 8.2-million-tonne downward revision, global coarse grain inventories are now forecast to fall below opening levels by 1.2 percent to 360 million tonnes in 2024/25. A cut in maize stocks makes up the bulk of the downward revision and mostly reflects lower inventories in China (mainland), the European Union, and the United States of America as a result of smaller imports foreseen for the former and lower production for the latter two. World wheat inventories have also been lowered by 5.1 million tonnes since November’s report, bringing the forecast for 2024/25 to 310 million tonnes. Most of the downward revision is made in the European Union reflecting the lower production estimate. FAO has trimmed its forecast of world rice stocks at the close 2024/25 marketing years by close to 900 000 tonnes since November, as less buoyant stock prospects for China, India and Thailand outweighed a slight upgrade for Indonesia. Despite the revision, world rice reserves remain forecast to expand by 2.6 percent to a peak of 204.5 million tonnes, reflecting expectations of carry-over increases in exporters (Thailand and Pakistan, in particular) and in importers (namely in China and the Philippines).

The world trade in cereals forecast for 2024/25 stands at 484 million tonnes, down 1.1 million tonnes from last month and 4.6 percent lower than the 2023/24 level. Global trade of coarse grains in 2024/25 (July/June) is revised downwards by 1.7 million tonnes since the previous forecast to 230 million tonnes, down 5.8 percent below the 2023/24 level. This month’s revision stems from a 2.0-million-tonne cut in the global maize trade forecast this month, supported by weaker maize import demand anticipated from China (mainland) and marginally smaller exports from Brazil, the European Union, and the United States of America, bringing the global forecast for 2024/25 to 186 million tonnes; this represents a year-on-year decline of 6.3 percent. Pegged at 198 million tonnes, the forecast for world wheat trade in 2024/25 (July/June) is nearly unchanged month on month and still points to a decline of 5.4 percent from last season, mostly driven by a fall in expected purchases by China (mainland) and the European Union, as well as smaller sales from the European Union, the Russian Federation, and Ukraine. International trade in rice in 2025 (January-December) is now forecast to reach 55.6 million tonnes, up from a revised forecast of 53.6 million tonnes for 2024. On the export side, given the September/October repeal of export restrictions on non-fully broken rice, India remains forecast to underpin the trade expansion envisaged for 2025, while export prospects are downcast most notably for Cambodia, Thailand and Viet Nam.