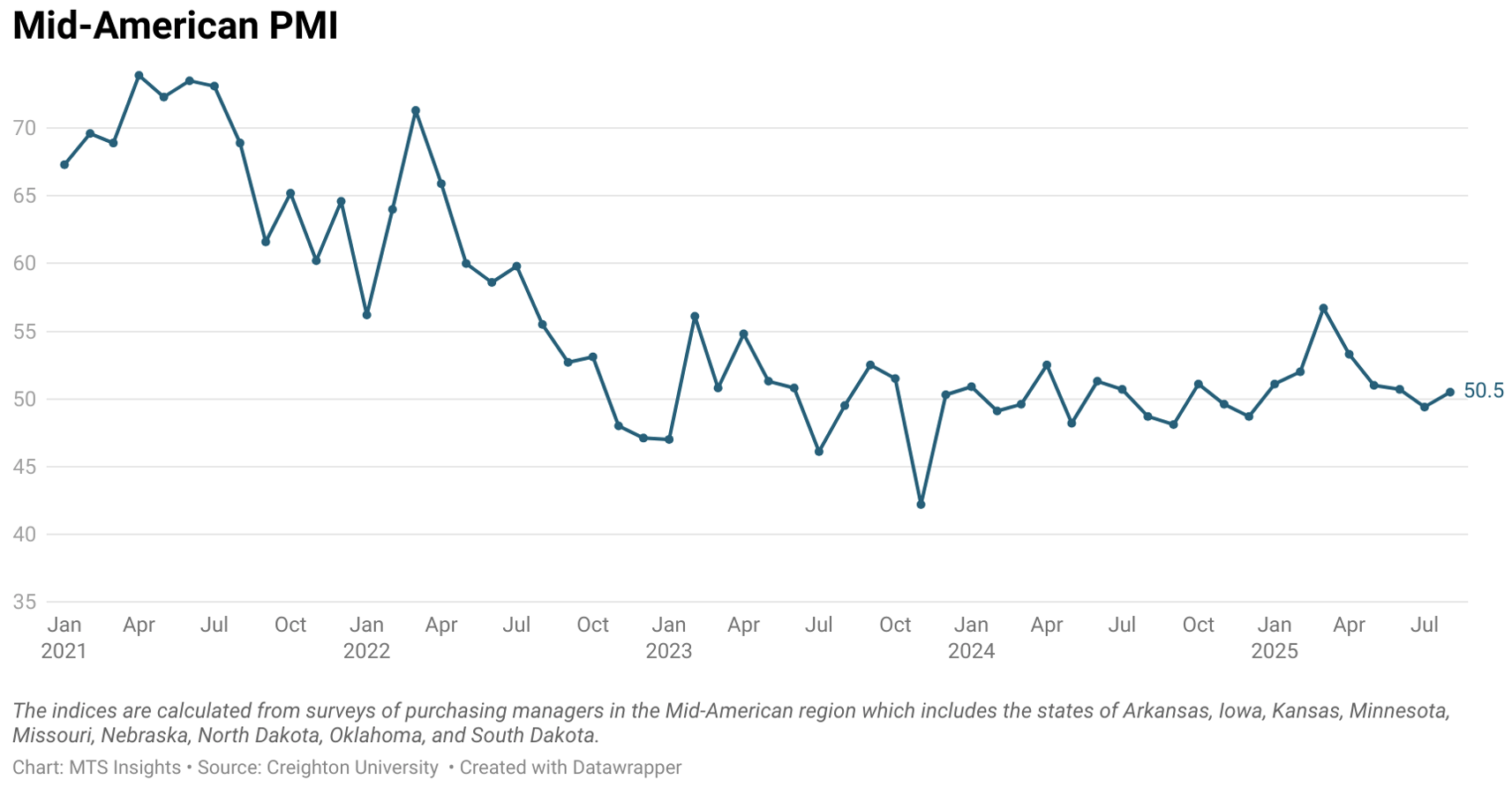

Creighton University Mid-American PMI

Creighton University Mid-American PMI

- Source

- Creighton University

- Source Link

- https://www.creighton.edu/

- Frequency

-

Monthly

1st business day

- Next Release(s)

- February 2nd, 2026 10:00 AM

Latest Updates

-

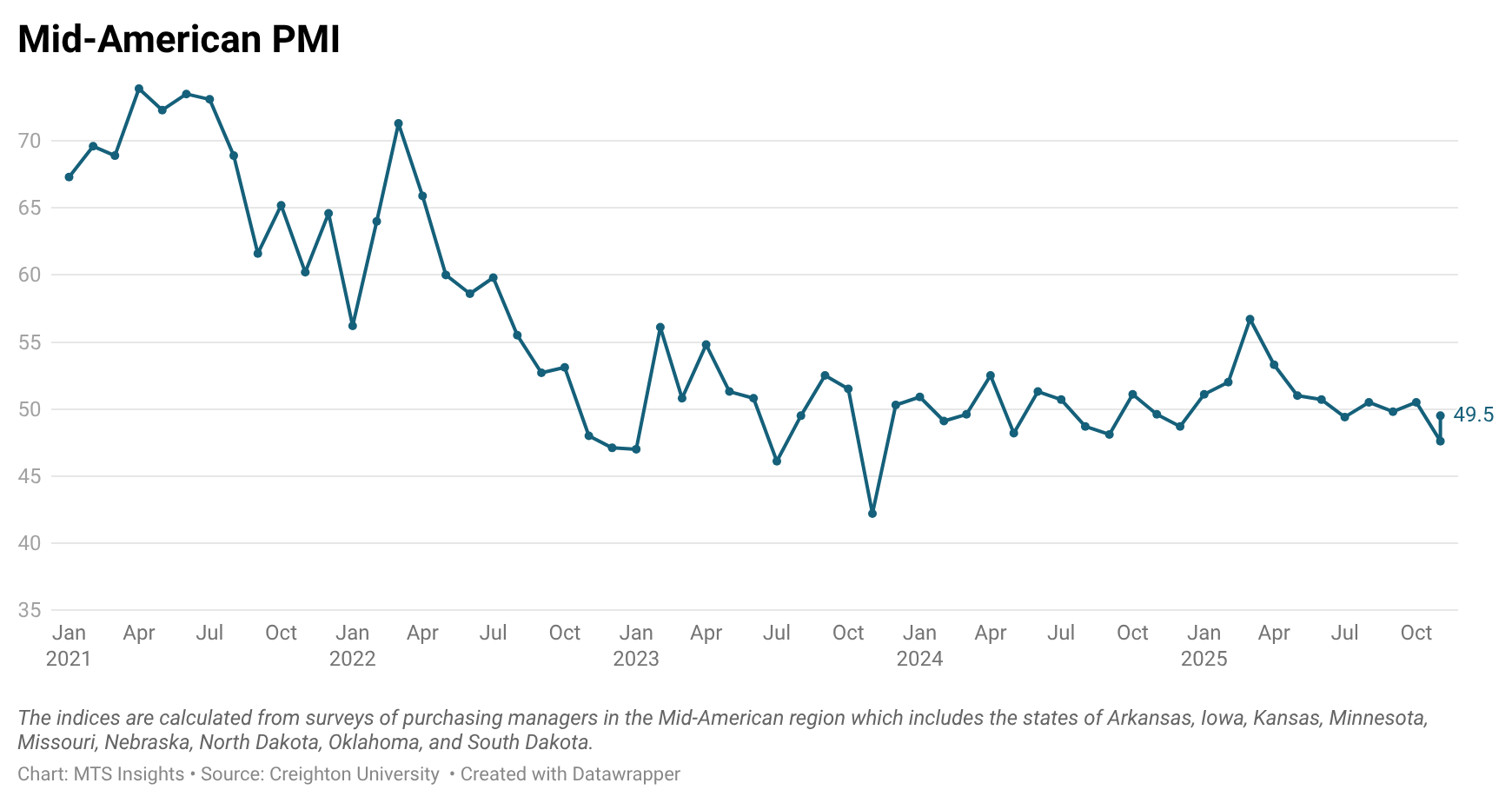

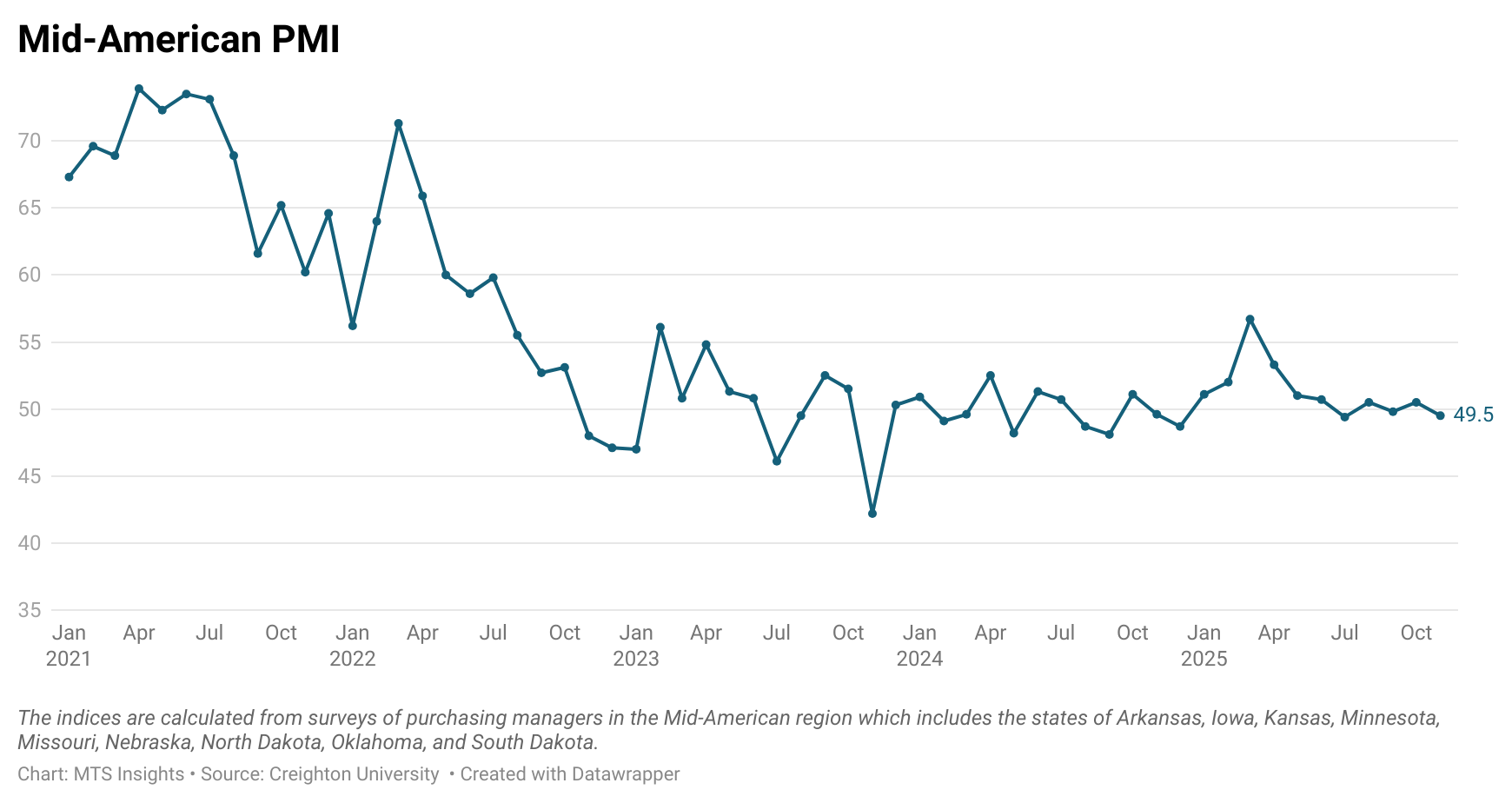

Mid-American Index November 2025 December 2025 Overall 49.5 47.6 New Orders 48.3 42.9 Production 46.2 47.4 Delivery Lead Time 55.1 53.2 Employment 47.6 44.0 Inventories 50.1 50.4 Prices 59.8 59.8 Confidence 47.4 50.0 -

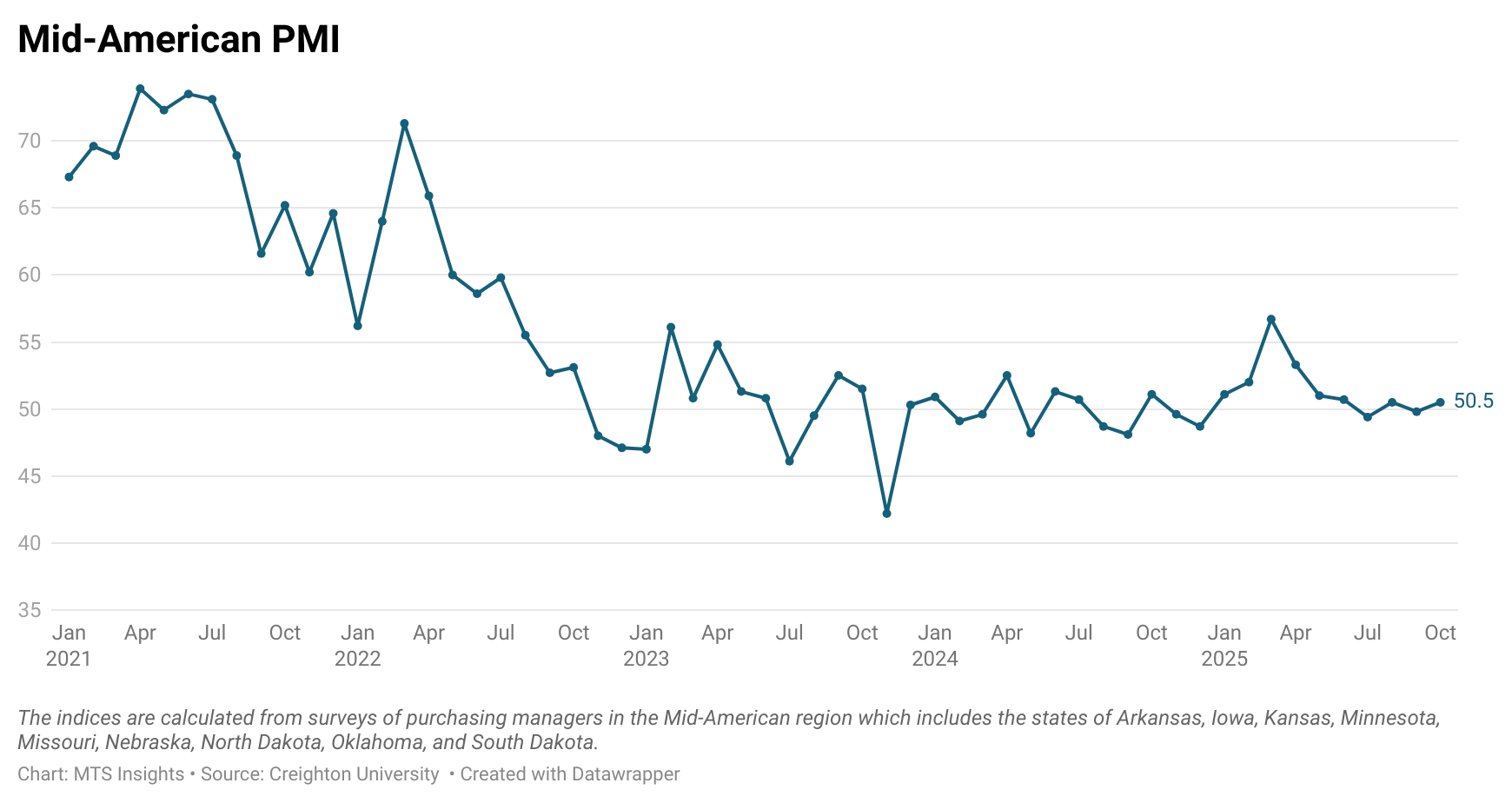

Mid-American Index October 2025 November 2025 Overall 50.5 49.5 New Orders 48.4 48.3 Production 49.8 46.2 Delivery Lead Time 57.9 55.1 Employment 46.9 47.6 Inventories 50.3 50.1 Prices 62.9 59.8 Confidence 42.2 47.4 -

The overall Mid-America Business Conditions Index rose +0.7 pts to 50.5 in October, moving back above the growth-neutral threshold and signaling a modest return to expansion in the regional manufacturing sector.

-

The employment index increased to 46.9 from 44.9 but remained below 50.0 for the seventh straight month, showing continued contraction in regional manufacturing jobs.

-

Approximately 16% of supply managers reported layoffs in October, while the insured unemployment rate edged up to 0.7% from 0.6% a year earlier.

-

The wholesale price index eased slightly to 62.9 from 64.1, yet still indicated elevated inflationary pressures, partly tied to higher import prices.

-

On average, firms said tariffs raised input costs by 7.9% in 2025, and 53% of firms sourcing internationally reported re-shoring some production.

-

The new export orders index fell to 40.8 from 43.4, marking six consecutive months of declines amid trade retaliation and weaker foreign demand.

-

Imports also weakened, with the index dropping to 34.0 from 34.8 as firms cut back on purchases from abroad following earlier record import volumes.

-

The business confidence index improved to 42.2 from 38.2 but remained subdued, as only 21.1% of respondents expected better conditions in the next six months.

-

Inventories rose to 50.3 from 48.6, reflecting precautionary stockpiling in anticipation of potential tariff increases.

-

Across the nine-state region, Missouri led with a robust reading of 62.7, while Kansas and North Dakota slipped below 50.0, highlighting divergent state-level trends.

-

-

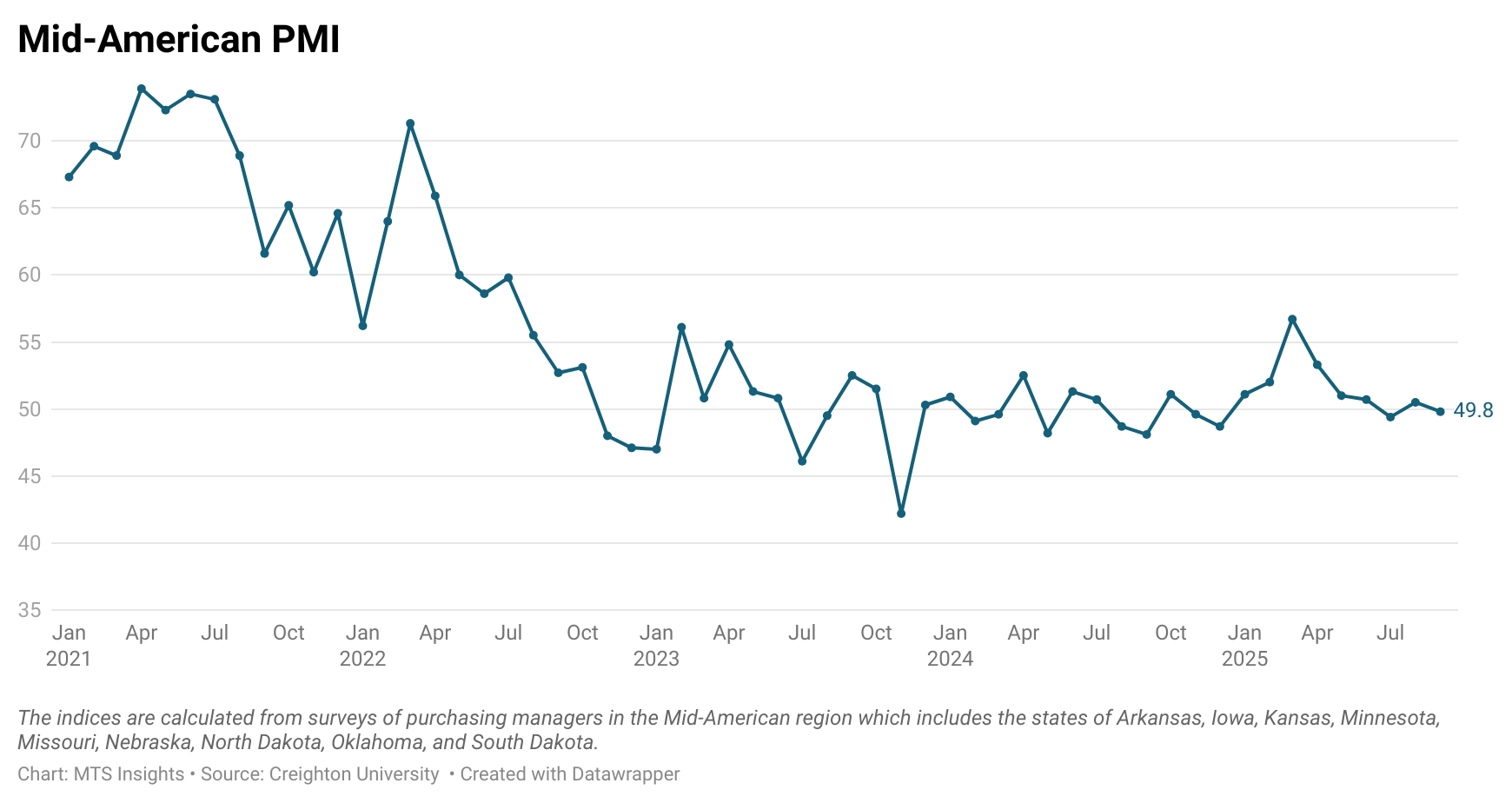

The overall Mid-America Business Conditions Index fell -0.7 pts to 49.8 in September, falling back below the neutral level after briefly returning to growth in August.

- The regional manufacturing sector shed jobs for the sixth straight month.

- Approximately 60% of supply managers reported that higher tariffs were having little or no impact on their purchasing decisions.

- Both imports and exports weakened for the month.

- According to the latest U.S. International Trade Administration (ITA) data, regional exports of manufactured goods sank by $3.1 billion, compared to the same period in 2024, for a 5.5% decline.

- Wholesale prices increased from the previous month and remained at elevated levels.

-

Mid-America Manufacturing Indicates Little to No Growth

Tariffs Are Impacting Imports and Exports

August 2025 Survey Highlights:

• The overall Mid-America Business Conditions Index continued to hover around growth neutral for the month.

• Employment losses occurred for the fifth straight month.

• Approximately 15% of firms reported that hiring had risen from July, compared to 10% of businesses that indicated that their firm had begun layoffs.

• The regional inflation yardstick moved into a range indicating that inflationary pressures are moving higher at the wholesale level.

• As reported by one supply manager, “We are starting to see the impact of tariffs on our bottom line.”

• Approximately four of five firms reported that tariffs were pushing import prices higher.• According to U.S. International Trade Administration (ITA) data, the regional economy exported $46.5 billion in manufactured goods for the first half of 2025, compared to $49.3 billion for the same period in 2024, for a 5.7% decline.

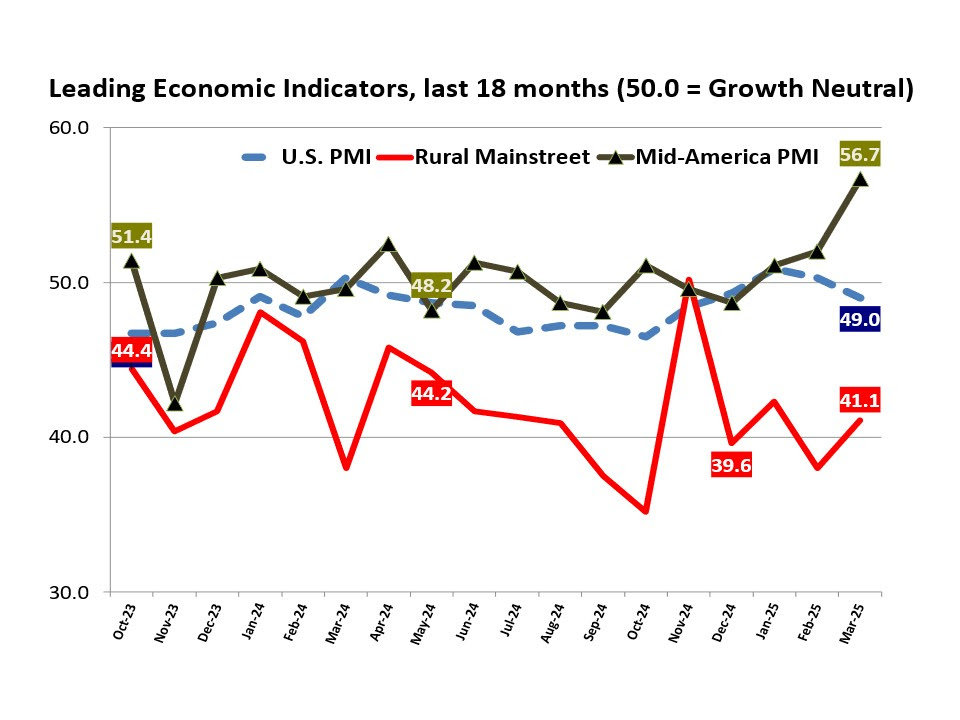

OMAHA, Neb. (Sept. 2, 2025) — For the seventh time in 2025, the Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, rose slightly above growth neutral in August.Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, climbed to 50.5 from 49.4 in July.

“Creighton’s latest survey continues to reflect job losses across the region, accompanied by elevated wholesale inflation,” said Ernie Goss, PhD, Director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business. “Supply managers reported weakness in both imports and exports along with higher prices for imported goods.”

As reported by one supply manager in August, “We are starting to see the impact of tariffs on our bottom line.”

The Mid-America report is produced independently of the national ISM.

Employment: The August employment index increased slightly to a weak 45.6 from 45.4 in July, marking the fifth consecutive month below the growth-neutral threshold of 50. “This sustained weakness reflects ongoing labor market challenges in the regional manufacturing sector,” said Goss.

On the other hand, approximately 15% of firms reported in August that hiring had risen from July, compared to 10% of businesses that indicated that their firm had begun layoffs.

As reported by an August survey participant, “We have trouble filling positions because of the low unemployment (less than 2%) in our area.”

Comments from Supply Managers in August:

• "Our layoffs have been self-inflicted due to a change in org structure.”

• “Grain prices have a direct impact on our market and are of concern as bumper crops will only push prices south and lower net farm income."

• “Quotes for products that would have been valid for 30 days now expired in seven.”

• “While I understand the economy is by no means on solid footing as of yet, if the Trump administration had done nothing, we would be in an all-out recession by now due to Biden's poor policy decisions and anti-American stance on several levels.”• “It will be touch and go for the next year for this economy to adjust to the new policies, both domestic and globally.”

• “The only real issues holding us back from rebounding faster are the continued obstructions from the liberals who are still reeling from TDS.”

Wholesale Prices: The August price gauge declined to 64.9 from 69.7 in July. “The regional inflation yardstick has moved into a range indicating that inflationary pressures are moving higher at the wholesale level. However, due to slowing regional and U.S. economies, I expect the Federal Reserve to cut interest rates at its September 16-17 meetings,” said Goss.

“When asked about the impact of tariffs on prices for inputs purchased abroad, approximately four of five firms reported that tariffs were pushing import prices higher,” said Goss.

Confidence: Looking ahead six months, economic optimism, as captured by the August Business Confidence Index, rose to a weak 47.4 from July’s 42.6. “Concerns regarding tariffs and slowing business activity pushed supply managers’ expectations lower. Only one in 10 supply managers expect rising economic conditions for their firm over the next six months,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, increased slightly to 49.3 from 49.1. “Rapid expansions in inventories in the first quarter are now being offset by monthly pullbacks in buildups,” said Goss.

Trade: Recent uncertainty regarding tariffs and trade restrictions pushed new export orders lower for the last four months. New export orders stood at 39.5, up slightly from 38.3 in July. As a result of record imports for the first two months of 2025, and higher import prices, supply managers pulled back on purchasing from abroad in the last six months. The August import index slumped to 35.9 from 36.3 in July.

U.S. tariffs appear to be negatively affecting exports as well as imports. According to U.S. International Trade Administration (ITA) data, the regional economy exported $46.5 billion in manufactured goods for the first half of 2025, compared to $49.3 billion for the same period in 2024, for a 5.7% decline.

In terms of export gainers for the first half of 2025, compared to 2024, North Dakota registered the top percentage gain with a 50.4% addition, and South Dakota recorded the largest percentage loss with a 19.1% reduction in the export of manufactured goods.

Other survey components of the August Business Conditions Index were: New orders increased to 49.8 from 45.5 in July; the production index climbed to 53.4 from 49.0 in July; and the speed of deliveries of raw materials and supplies declined to 54.2 from July’s 57.8. Lower readings indicate faster deliveries and/or falling supply chain disruptions or delays.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Arkansas: The state’s August Business Conditions Index increased to 48.4 from 43.0 in July. Components from the August survey of supply managers were: new orders at 49.1; production or sales at 51.8; delivery lead time at 54.1; inventories at 45.4; and employment at 41.7. According to ITA data, the Arkansas manufacturing sector exported $2.8 billion in goods for the first half of 2025, compared to $3.0 billion for the same period in 2024, for a 7.5% decline.

Iowa: The state’s Business Conditions Index for August increased to 45.8 from 43.7 in July. Components of the overall August index were: new orders at 50.3; production or sales at 48.6; delivery lead time at 51.9; employment at 38.4; and inventories at 39.7. According to ITA data, the Iowa manufacturing sector exported $7.2 billion in goods for the first half of 2025, compared to $8.1 billion for the same period in 2024, for a 10.8% decline.

Kansas: The Kansas Business Conditions Index for August fell to 50.7 from July’s 51.1. Components of the leading economic indicators from the monthly survey of supply managers for August were: new orders at 49.4; production or sales at 64.1; delivery lead time at 55.9; employment at 44.5; and inventories at 50.3. According to ITA data, the Kansas manufacturing sector exported $6.2 billion in goods for the first half of 2025, compared to $6.3 billion for the same period in 2024, for a 2.8% decline.

Minnesota: The August Business Conditions Index for Minnesota dropped to 48.3 from 49.3 in July. Components of the overall August index were: new orders at 49.0; production or sales at 51.8; delivery lead time at 54.0; inventories at 45.2; and employment at 41.6. According to ITA data, the Minnesota manufacturing sector exported $11.3 billion in goods for the first half of 2025, compared to $12.9 billion for the same period in 2024, for a 12.7% decline.

Missouri: The state’s August Business Conditions Index climbed to 54.4 from July’s 51.8. Components of the overall index from the survey of supply managers for August were: new orders at 50.2; production or sales at 49.2; delivery lead time at 60.1; inventories at 61.5; and employment at 51.1. According to ITA data, the Missouri manufacturing sector exported $8.3 billion in goods for the first half of 2025, compared to $8.8 billion for the same period in 2024, for a 5.3% decline.

Nebraska: The state’s August Business Conditions Index climbed to 53.1 from July’s 51.6. Components of the index from the monthly survey of supply managers for August were: new orders at 49.9; production or sales at 54.5; delivery lead time at 58.0; inventories at 55.7; and employment at 47.7. According to ITA data, the Nebraska manufacturing sector exported $3.2 billion in goods for the first half of 2025, compared to $3.7 billion for the same period in 2024, for a 12.3% decline.

North Dakota: The state’s Business Conditions Index advanced above growth neutral for a 14th consecutive month but declined to 51.7 from 52.2 in July. Components of the overall index for August were: new orders at 49.6; production or sales at 53.6; delivery lead time at 56.8; employment at 45.8; and inventories at 52.5. According to ITA data, the North Dakota manufacturing sector exported $3.1 billion in goods for the first half of 2025, compared to $2.1 billion for the same period in 2024, for a 50.4% gain.

Oklahoma: The state’s Business Conditions Index for August rose to 50.3 from 49.0 in July. Components of the overall August index were: new orders at 49.4; production or sales at 52.9; delivery lead time at 55.6; inventories at 49.5; and employment at 44.1. According to ITA data, the Oklahoma manufacturing sector exported $3.5 billion in goods for the first half of 2025, compared to $3.3 billion for the same period in 2024, for a 4.5% gain.

South Dakota: The August Business Conditions Index for South Dakota increased to 47.4 from 44.5 in July. Components of the overall August index were: new orders at 48.9; production or sales at 51.2; delivery lead time at 53.2; inventories at 43.2; and employment at 40.4. According to ITA data, the South Dakota manufacturing sector exported $821.8 million in goods for the first half of 2025, compared to $1.0 billion for the same period in 2024, for a 19.1% decline.

-

Mid-America Manufacturing Slumps for July

Higher Inflation with Job Losses

July 2025 Survey Highlights:

- The overall Mid-America Business Conditions Index declined below growth neutral for the month.

- Employment losses occurred for the fourth straight month.

- The regional inflation yardstick moved into a range indicating that inflationary pressures are moving higher at the wholesale level.

- Only 6.7% of supply managers reported that tariffs caused their firms to move input purchases from international providers to domestic suppliers.

- According to U.S. International Trade Administration (ITA) data, the regional economy exported $38.9 billion in manufactured goods for the first five months of 2025, compared toff $40.8 billion for the same period in 2024, for a 4.7% decline.

- In terms of 2025 export gainers, North Dakota registered the top percentage gain with a 42.6% addition, and South Dakota recorded the largest percentage loss with a 19.9% reduction in the export of manufactured goods.

OMAHA, Neb. (August 1, 2025) — After six straight months of above growth neutral readings, the Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, sank below 50.0 growth neutral threshold for July.

Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, declined to 49.4 for July from 50.7 in June.

“Creighton’s latest survey continues to reflect job losses across the region, accompanied by elevated wholesale inflation,” said Ernie Goss, PhD, Director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business. “Supply managers expressed growing concern that rising tariffs could further accelerate inflationary pressures. Despite these concerns, only 6.7% of surveyed supply managers reported shifting purchases from international to domestic suppliers in response to the tariffs.”

The Mid-America report is produced independently of the national ISM.

Employment: The July employment index fell to 45.4 from 49.4 in June, marking the fourth consecutive month below the growth-neutral threshold of 50. This sustained weakness reflects ongoing labor market challenges in the regional manufacturing sector.

“The Creighton survey has now recorded six straight months of job losses across the nine-state Mid-America region,” said Goss. “While employment rose in the first quarter—driven by increased production ahead of anticipated tariff impacts—the last four months have signaled a return to regional manufacturing job declines,” said Goss.

U.S. Bureau of Labor Statistics data show that the region shed 12,900 (-0.9%) manufacturing jobs over the past 12 months. The U.S. lost 89,000 (-0.7%) manufacturing jobs over the same time period.

Comments from Supply Managers in July:

- “Most of the suppliers I work with are dropping their production down to four-day work weeks. Nothing like a 20% cut in pay.”

- “I believe that the President's tariff changes are going to help our country to be better trading partners. It will take a bit of time for it all to shake out though.”

- “No changes to international purchases until a final tariff rate is in place. Certain products have been put on hold.”

- “We are not accepting pricing increases and have any tariffs added as a surcharge, so they are easy to remove.”

- “Long-term contracts have been key to holding pricing steady. Where there are extreme cost pressures with suppliers, collaboration on a resolution is the method of choice, while rare.”

- “While the Trump administration is doing everything possible to bring the economy back to its former glory, the democrats continue their seditious acts to block any attempts at dismantling their previous criminal maneuvers to destroy this great country! A reckoning is coming.”

Wholesale Prices: The July price gauge climbed to 69.7 from 67.9 in June. “The regional inflation yardstick has moved into a range indicating that inflationary pressures are moving higher at the wholesale level. However, due to a slowing regional and U.S. economies, I expect the Federal Reserve to cut interest rates at its September 16-17 meetings,” said Goss.

On average, supply managers expect tariffs to push input prices up by 7.8% over the next 12 months. This is up from 7.5% recorded in June.

Confidence: Looking ahead six months, economic optimism, as captured by the July Business Confidence Index, dropped to 42.6 from June’s 50.0. “Concerns regarding tariffs and slowing new orders pushed supply managers’ expectations lower. Only one in six supply managers expect rising economic conditions for their firm over the next six months,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, increased to 49.1 in July from June’s 46.9. “Rapid expansions in inventories in the first quarter are now being offset by monthly pullbacks in buildups,” said Goss.

Trade: Recent uncertainty regarding tariffs and trade restrictions pushed new export orders lower for the last four months. New export orders slumped to 38.3 from 43.4 in June. As a result of record imports for the first two months of 2025, supply managers pulled back on purchasing from abroad in the last five months. The July import index increased to a still weak reading of 36.3 from 30.0 in June.

Supply managers were asked about their firm’s reactions to tariffs and threats of tariffs. Only 6.7% of manufacturing supply managers reported switching from international suppliers to domestic suppliers. More than one-third, or 67.0%, reported making no changes of suppliers due to tariffs. The remaining 26.3% indicated that their firms had switched from one international supplier to another international input supplier.

According to U.S. International Trade Administration (ITA) data, the regional economy exported $38.9 billion in manufactured goods for the first five months of 2025, compared to $40.8 billion for the same period in 2024, for a 4.7% decline. In terms of export gainers, North Dakota registered the top percentage gain with a 42.6% addition, and South Dakota recorded the largest percentage loss with a 19.9% reduction in the export of manufactured goods.

Other survey components of the July Business Conditions Index were: New orders dropped to 45.5 from 52.4 in June; the production or sales index increased slightly to 49.0 from 48.5 in June; and the speed of deliveries of raw materials and supplies rose to 57.8 from June’s 56.5. Higher readings indicate slower deliveries and/or rising supply chain disruptions or delays.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Arkansas: The state’s July Business Conditions Index fell to 43.0 from 48.2 in June. Components from the July survey of supply managers were: new orders at 43.7, production or sales at 47.0; delivery lead time at 53.1; inventories at 39.5; and employment at 31.8. According to ITA data, the Arkansas manufacturing sector exported $2.3 billion in goods for the first five months of 2025, compared to $2.4 billion for the same period in 2024, for a 5.6% decline.

Iowa: The state’s Business Conditions Index for July declined to 43.7 from 48.0 in June. Components of the overall July index were: new orders at 43.9; production or sales at 47.3; delivery lead time at 53.6; employment at 33.2; and inventories at 40.6. According to ITA data, the Iowa manufacturing sector exported $6.2 billion in goods for the first five months of 2025, compared to $6.9 billion for the same period in 2024, for a 10.3% decline.

Kansas: The Kansas Business Conditions Index for July increased to 51.1 from 49.9 in June. Components of the leading economic indicators from the monthly survey of supply managers for July were: new orders at 45.5; production or sales at 50.3; delivery lead time at 58.6; employment at 47.7; and inventories at 58.6. According to ITA data, the Kansas manufacturing sector exported $5.0 billion in goods for the first five months of 2025, compared to $5.2 billion for the same period in 2024, for a 3.5% decline.

Minnesota: The July Business Conditions Index for Minnesota dropped to 49.3 from 52.8 in June. Components of the overall July index were: new orders at 45.1; production or sales at 49.8; delivery lead time at 57.5; inventories at 50.2; and employment at 44.3. According to ITA data, the Minnesota manufacturing sector exported $9.5 billion in goods for the first five months of 2025, compared to $10.7 billion for the same period in 2024, for an 11.4% decline.

Missouri: The state’s July Business Conditions Index rose to 51.8 from 50.8 in June. Components of the overall index from the survey of supply managers for July were: new orders at 45.6; production or sales at 50.6; delivery lead time at 59.1; inventories at 54.4; and employment at 49.2. According to ITA data, the Missouri manufacturing sector exported $7.0 billion in goods for the first five months of 2025, compared to $7.1 billion for the same period in 2024, for a 0.5% decline.

Nebraska: The state’s July Business Conditions Index climbed to 51.6 from June’s 51.3. Components of the index from the monthly survey of supply managers for July were: new orders at 45.5; production or sales at 50.4; delivery lead time at 58.8; inventories at 53.6; and employment at 48.3. According to ITA data, the Nebraska manufacturing sector exported $2.7 billion in goods for the first five months of 2025, compared to $3.1 billion for the same period in 2024, for a 10.8% decline.

North Dakota: The state’s Business Conditions Index advanced above growth neutral for a 13th consecutive month to 52.2 from 52.0 in June. Components of the overall index for July were: new orders at 45.7; production or sales at 50.8; delivery lead time at 59.4; employment at 50.0; and inventories at 55.0. According to ITA data, the North Dakota manufacturing sector exported $2.5 billion in goods for the first five months of 2025, compared to $1.8 billion for the same period in 2024, for a 42.6% gain.

Oklahoma: The state’s Business Conditions Index for July declined to 49.0 from 50.6 in June. Components of the overall July index were: new orders at 45.0; production or sales at 49.5; delivery lead time at 57.2; inventories at 49.7; and employment at 43.7. According to ITA data, the Oklahoma manufacturing sector exported $2.9 billion in goods for the first five months of 2025, compared to $2.6 billion for the same period in 2024, for a 3.5% gain.

South Dakota: The July Business Conditions Index for South Dakota slumped to 44.5 from 48.5 in June. Components of the overall July index were: new orders at 44.1; production or sales at 47.6; delivery lead time at 54.1; inventories at 42.1; and employment at 34.8. According to ITA data, the South Dakota manufacturing sector exported $0.7 billion in goods for the first five months of 2025, compared to $0.9 billion for the same period in 2024, for a 19.9% decline.

-

Slow Growth for Mid-America Manufacturing

Higher Inflation with Job Losses

June 2025 Survey Highlights:

- The overall Mid-America Business Conditions Index declined for the month but remained above growth neutral for the sixth straight month.

- The June regional manufacturing employment index remained below growth neutral.

- Inflation continues to trend higher.

- On average, supply managers expect tariffs to push input prices up by 7.5% in the second half of 2025.

- A high proportion of supply managers reported a balance between job openings and job applicants.

- According to U.S. International Trade Administration (ITA) data, the regional economy exported $32.1 billion in manufactured goods for the first four months of 2025, compared to $31.3 billion for the same period in 2024, for a 2.3% decline.

- In terms of export gainers for the first four months of 2025, North Dakota registered the top gain with a 29.7% addition, and South Dakota recorded the largest loss with a 20.4% reduction in exports of manufactured goods.

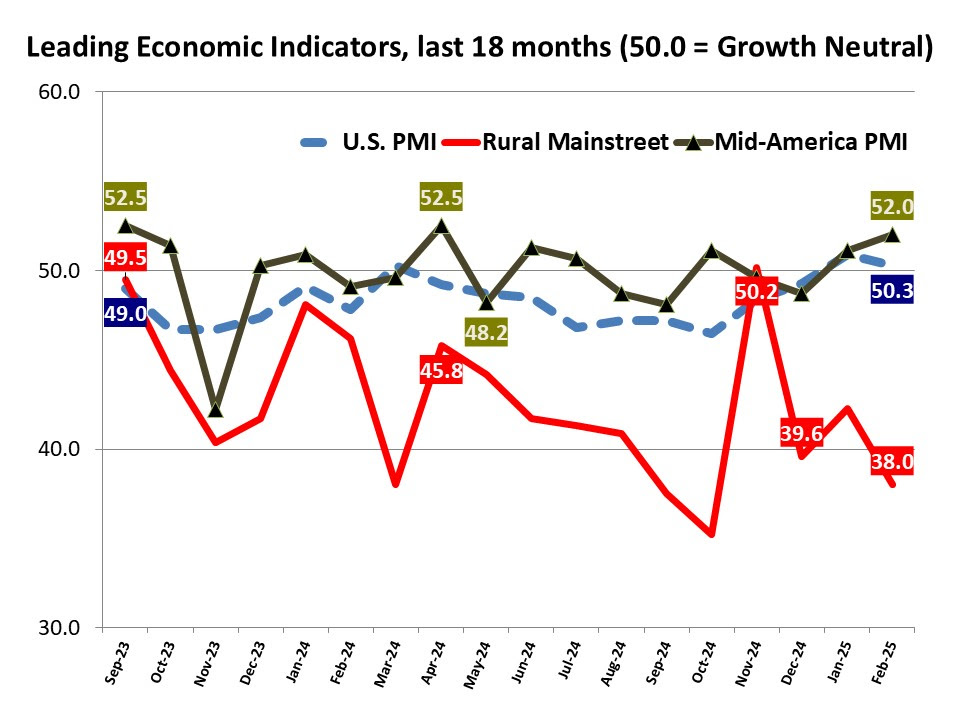

OMAHA, Neb. (July 1, 2025) — The Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, moved above the 50.0 growth neutral threshold for a sixth straight month.

Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, declined to 50.7 from 51.0 in May.

“The Creighton survey continues to record job losses with accompanying higher wholesale inflation. Supply managers remain concerned that rising tariffs will push inflation significantly higher. On average, supply managers expect input prices to climb by 7.5% in 2025,” said Ernie Goss, PhD, Director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business.

The Mid-America report is produced independently of the national ISM.

As indicated by a supply manager in the June survey, “We are starting to experience more notification on tariff increases and starting to see shortages of products.”

Employment: The June employment index was unchanged from May’s weak 49.4. “First quarter employment was pushed higher due to higher production in anticipation of the fallout from tariffs. However, readings from the last three months represented a return to manufacturing job losses in the region,” said Goss.

U.S. Bureau of Labor Statistics data show that the region shed 9,900 (-0.7%) manufacturing jobs over the past 12 months. The U.S. lost 88,000 (-0.7%) manufacturing jobs over the same period.

Comments from Supply Managers in June:

- “Bird flu is still impacting eggs, liquid eggs, pricing, etc. Freight continues to increase. Service levels are noticeably down and lowering expectations have been normalized from five years ago. Much more involved with managing vendors, service.”

- “The county we are located in has a very low unemployment rate, less than 2%, and we have several large employers that pay well. Our business is slow or we would have a serious shortage of workers.”

- “Tariffs drive up imported and domestic steel and aluminum prices.”

- “While we are getting applications for positions, about half of them are from applicants wishing to work remotely, which has taken on a different connotation as time goes on. For some positions, such as sales, remote work is fine. That won't work for our current supply chain team – it is too collaborative and responsive.”

- “Expect a significant increase in costs over the next two months.”

Wholesale Prices: The June price gauge climbed to 67.9 from 67.4 in May. “The regional inflation yardstick has moved into a range indicating that inflationary pressures are moving higher at the wholesale level. However, due to slowing regional and U.S. economies, I expect the Federal Reserve to cut interest rates at either its July meeting on July 29-30 or its September 16-17 meetings,” said Goss.

On average supply managers expect tariffs to push input prices up by 7.5% in 2025.

Confidence: Looking ahead six months, economic optimism, as captured by the June Business Confidence Index, increased to 50.0 from May’s 43.2. “Despite concerns regarding tariffs, supply managers continue to see improving economic conditions. One in four supply managers expect rising economic conditions for their firm over the next six months. This is up from one in five last month,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, fell to 46.9 from May’s 51.6. “Rapid expansions of inventories in the first quarter are now being offset by pullbacks in buildups,” said Goss.

Trade: Recent uncertainty regarding tariffs and trade restrictions pushed new export orders lower for the last three months. New export orders slumped to 43.4 from 44.8 in May and 46.2 in April. As result of record imports for the first two months of 2025, supply managers pulled back on purchasing from abroad in March, April, May and June. The June import index increased to a still very weak reading of 30.0 from 29.8 in May and April’s record low of 12.5.

According to U.S. International Trade Administration (ITA) data, the regional economy exported $32.1 billion in manufactured goods for the first four months of 2025, compared to $31.3 billion for the same period in 2024, for a 2.3% decline. In terms of export gainers, North Dakota registered the top gain with a 29.7% addition, and South Dakota recorded the largest loss with a 20.4% reduction in exports of manufactured goods.

Other survey components of the June Business Conditions Index were: new orders increased to 52.4 from 51.0 in May; the production or sales index sank to 48.5 from 49.4 in May; and the speed of deliveries of raw materials and supplies rose to 56.5 from May’s 53.7. Higher readings indicate slower deliveries and rising supply chain disruptions or delays.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Arkansas: The state’s June Business Conditions Index fell to 48.2 from 53.2 in May. Components from the June survey of supply managers were: new orders at 51.9, production or sales at 47.4; delivery lead time at 54.2; inventories at 44.8; and employment at 42.3. According to ITA data, the Arkansas manufacturing sector exported $1.8 billion in goods for the first four months of 2025, compared to $2.0 billion for the same period in 2024, for a 5.6% decline.

Iowa: The state’s Business Conditions Index for June declined to 48.0 from 49.9 in May. Components of the overall June index were: new orders at 51.9; production or sales at 47.4; delivery lead time at 54.2; employment at 41.9; and inventories at 44.8. According to ITA data, the Iowa manufacturing sector exported $5.0 billion in goods for the first four months of 2025, compared to $5.4 billion for the same period in 2024, for an 8.1% decline.

Kansas: The Kansas Business Conditions Index for June increased to 49.9 from 48.1 in May. Components of the leading economic indicators from the monthly survey of supply managers for June were: new orders at 52.3; production or sales at 48.5; delivery lead time at 56.0; employment at 47.3; and inventories at 45.6. According to ITA data, the Kansas manufacturing sector exported $4.0 billion in goods for the first four months of 2025, compared to $4.1 billion for the same period in 2024, for a 2.6% decline.

Minnesota: The June Business Conditions Index for Minnesota rose to 52.8 from May’s 52.3. Components of the overall June index were: new orders at 52.8; production or sales at 50.1; delivery lead time at 58.6; inventories at 46.9; and employment at 55.4. According to ITA data, the Minnesota manufacturing sector exported $7.8 billion in goods for the first four months of 2025, compared to $8.5 billion for the same period in 2024, for an 8.4% decline.

Missouri: The state’s June Business Conditions Index dropped to 50.8 from 53.4 in May. Components of the overall index from the survey of supply managers for June were: new orders at 52.4; production or sales at 48.9; delivery lead time at 56.8; inventories at 46.0; and employment at 49.7. According to ITA data, the Missouri manufacturing sector exported $5.7 billion in goods for the first four months of 2025, compared to $5.3 billion for the same period in 2024, for a 6.3% gain.

Nebraska: The state’s June Business Conditions Index climbed to 51.3 from May’s 48.6. Components of the index from the monthly survey of supply managers for June were: new orders at 52.5; production or sales at 49.2; delivery lead time at 57.3; inventories at 46.3; and employment at 46.3. According to ITA data, the Nebraska manufacturing sector exported $2.2 billion in goods for the first four months of 2025, compared to $2.4 billion for the same period in 2024, for a 6.4% decline.

North Dakota: The state’s Business Conditions Index advanced above growth neutral for a 12th consecutive month to 52.0 from 50.8 in May. Components of the overall index for June were: new orders at 52.7; production or sales at 49.6; delivery lead time at 57.9; employment at 53.2; and inventories at 46.6. According to ITA data, the North Dakota manufacturing sector exported $1.9 billion in goods for the first four months of 2025, compared to $1.5 billion for the same period in 2024, for a 29.7% gain.

Oklahoma: The state’s Business Conditions Index for June increased to 50.6, up slightly from May’s 50.5. Components of the overall June index were: new orders at 52.4; production or sales at 48.8; delivery lead time at 56.6; inventories at 45.9; and employment at 49.2. According to ITA data, the Oklahoma manufacturing sector exported $2.4 billion in goods for the first four months of 2025, compared to $2.2 billion for the same period in 2024, for a 6.6% gain.

South Dakota: The June Business Conditions Index for South Dakota slumped to 48.5 from 48.7 in May. Components of the overall June index were: new orders at 52.0; production or sales at 47.7; delivery lead time at 54.7; inventories at 45.0; and employment at 43.3. According to ITA data, the South Dakota manufacturing sector exported $0.5 billion in goods for the first four months of 2025, compared to $0.7 billion for the same period in 2024, for a 20.4% decline.

-

Mid-America Manufacturing Growth Slows with Higher Prices

Tariffs Pushing Input Prices Higher

May 2025 Survey Highlights:

- The overall Mid-America Business Conditions Index declined for the month but remained above growth neutral for the fifth straight month.

- Approximately one-third of manufacturers reported switching input providers due to tariffs, or the threat of tariffs.

- The May regional manufacturing employment index remained below growth neutral.

- More than half of supply managers reported that tariffs and impending tariffs have pushed prices higher for production inputs.

- As indicated by a supply manager in the May survey, “Tariffs are being used as a means to increase prices regardless of whether they are applicable or not.”

- As a result of slowing growth, Goss expects a cut in short-term interest rates at the Federal Reserve’s next meetings on June 17/18.

- According to U.S. International Trade Administration (ITA) data, the regional economy exported $23.4 billion in manufactured goods for the first quarter of 2025, compared to $23.7 billion for the same period in 2024, for a 1.4% decline.

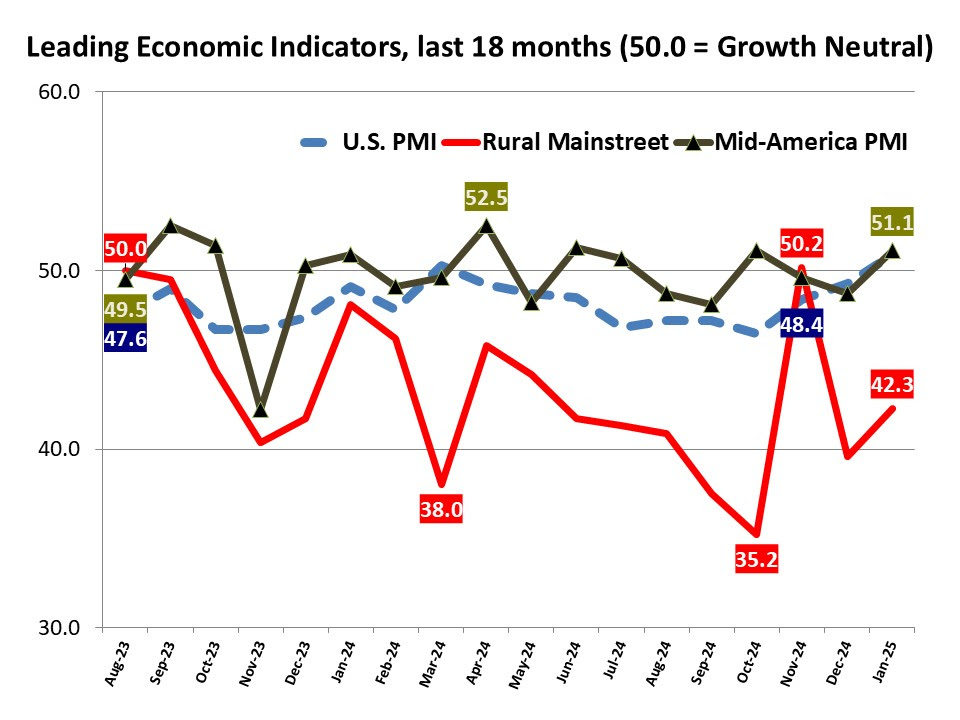

OMAHA, Neb. (June 2, 2025) — The Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, moved above growth neutral of 50.0 for a fifth straight month.

Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, declined to 51.0 from April’s higher 53.3.

“The Creighton survey is recording significant volatility, much like other regional economic measures. Proposed and implemented tariffs are producing economic volatility as well as slower growth. Approximately, 34.8% of supply reported switching suppliers due to tariffs, proposed and implemented,” said Ernie Goss, PhD, Director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business.

The Mid-America report is produced independently of the national ISM.

As indicated by a supply manager in the May survey, “I understand the significance of the tariffs and perhaps they are even warranted in some cases. However, the approach was abysmal and ultimately will hurt the American working class.”

Employment: The May employment index increased to a weak 49.4 from 44.9 in April. “First quarter employment was pushed higher due to higher production in anticipation of the fallout from tariffs. Readings from the last two month represented a return to manufacturing job losses in the region,” said Goss.

U.S. Bureau of Labor Statistics data show that the region shed 12,500 (-0.8%) manufacturing jobs over the past 12 months. The U.S. lost 82,000 (-0.6%) manufacturing jobs over the same time period.

Comments from Supply Managers in May:

- “…..we have noticed some increased prices and tracking as much as possible to understand what categories are most affected and strategize future purchases.”

- “Tariffs are being used as a means to increase price regardless of whether they are applicable or not.”

- “Highly risky times Not for the faint of heart. These are the times that try men's souls.”

- “Price increases are starting to occur across the board. It is just a matter of time until the consumer will be impacted.”

- “While prices have increased, most are within the inflationary averages. Long term contracting has limited the amount of increases and are staggered to prevent significant interruptions to project budgets during any one period.”

- “The Trump administration has done an admirable job keeping inflation, prices and interest rates down and increasing re-shoring of goods and services. His "4D Chess match" with adversaries is amazing to observe as he brings integrity and the rule of law back into the global order."

- “It will be interesting to see the domino's fall as political upheaval within the Democratic party start to reveal their egregious corruption and worse, treason!”

Wholesale Prices: The May price gauge climbed to 67.4 from 65.0 in April.. “The regional inflation yardstick has moved into a range indicating that inflationary pressures are moving higher at the wholesale level. However, due to a slowing economy, I expect the Fed to cut interest rates at its next meetings on June 17/18,” said Goss.

Approximately 56.5% of supply managers reported that tariffs and impending tariffs have pushed prices higher for production inputs.

Confidence: Looking ahead six months, economic optimism, as captured by the May Business Confidence Index, increased to 43.2 from April’s 37.5. “Due to concerns regarding global economic tensions and rising tariffs, only one in five supply managers expect improving business conditions over the next six months,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, fell to 51.6 from April’s 56.7. “In order to front-run tariffs, firms have expanded inventories for four of the first five months of 2025,” said Goss.

Trade: Recent uncertainty regarding tariffs and trade restrictions pushed new export orders lower for May. New export orders slumped to 44.8 from 46.2 in April . As result of record imports for the first two months of 2025, supply managers pulled back on purchasing from abroad in March, April and May. The May import index rose from April’s record low of 12.5 to 29.8 for May.

According to U.S. International Trade Administration (ITA) data, the regional economy exported $23.7 billion in manufactured goods for the first quarter of 2025, compared to $23.4 billion for the same period in 2024, for a 1.4% decline. In terms of export gainers, North Dakota registered the top gain with an 8.9% addition, and South Dakota recorded the largest loss with a 17.7% reduction in the export of manufactured goods.

Other survey components of the May Business Conditions Index were: new orders declined to 51.0 from 52.9 in April; the production or sales index sank to 49.4 from 55.4 in April; and the speed of deliveries of raw materials and supplies fell to 53.7 from April’s 56.8. Lower readings indicate falling supply chain disruptions or delays.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Arkansas: The state’s May Business Conditions Index decreased to 53.2 from 57.5 in April. Components from the May survey of supply managers were: new orders at 48.5 production or sales at 56.8; delivery lead time at 54.5; inventories at 54.0; and employment at 52.5. According to ITA data, the Arkansas manufacturing sector exported $1.4 billion in goods for the first quarter of 2025 compared to $1.3 billion for the same period in 2024, for a 4.8% gain.

Iowa: The state’s Business Conditions Index for May declined to 49.9 from 53.0 in April. Components of the overall May index were: new orders at 50.2; production or sales at 47.6; delivery lead time at 53.2; employment at 48.1; and inventories at 50.4. According to ITA data, the Iowa manufacturing sector exported $3.4 billion in goods for the first quarter of 2025 compared to $4.0 billion for the same period in 2024, for an 8.6% decline.

Kansas: The Kansas Business Conditions Index for May sank to 48.1 from 51.1 in April. Components of the leading economic indicators from the monthly survey of supply managers for May were: new orders at 46.8; production or sales at 49.9; delivery lead time at 52.0; employment at 44.3; and inventories at 47.3. According to ITA data, the Kansas manufacturing sector exported $2.9 billion in goods for the first quarter of 2025 compared to $3.0 billion for the same period in 2024, for a 1.8% decline.

Minnesota: The May Business Conditions Index for Minnesota declined to 52.3 from April’s 56.7. Components of the overall May index were: new orders at 50.5; production or sales at 48.6; delivery lead time at 54.7; inventories at 54.6; and employment at 53.2. According to ITA data, the Minnesota manufacturing sector exported $6.0 billion in goods for the first quarter of 2025, compared to $6.3 billion for the same period in 2024, for a 5.5% decline.

Missouri: The state’s May Business Conditions Index climbed to 53.4 from 48.1 in April. Components of the overall index from the survey of supply managers for May were: new orders at 50.7; production or sales at 49.1; delivery lead time at 55.4; inventories at 56.5; and employment at 55.4. According to ITA data, the Missouri manufacturing sector exported $4.2 billion in goods for the first quarter of 2025 compared to $3.9 billion for the same period in 2024, for a 6.5% boost.

Nebraska: For only the second time in the past 12 months, Nebraska’s overall index fell below growth neutral. The state’s May Business Conditions Index sank to 48.6 from April’s 50.1. Components of the index from the monthly survey of supply managers for May were: new orders at 50.0; production or sales at 47.1; delivery lead time at 52.3; inventories at 48.2; and employment at 45.4. According to ITA data, the Nebraska manufacturing sector exported $1.7 billion in goods for the first quarter of 2025 compared to $1.8 billion for the same period in 2024, for a 4.0% decline.

North Dakota: The state’s Business Conditions Index advanced above growth neutral for an 11th consecutive month to 50.8, which was down from April’s 52.5. Components of the overall index for May were: new orders at 50.3; production or sales at 48.0; delivery lead time at 53.7; employment at 50.0; and inventories at 52.0. According to ITA data, the North Dakota manufacturing sector exported $1.3 billion in goods for the first quarter of 2025 compared to $1.1 billion for the same period in 2024, for a 12.5% gain.

Oklahoma: The state’s Business Conditions Index for May dropped to 50.5 from April’s 56.8. Components of the overall May index were: new orders at 50.3; production or sales at 47.8; delivery lead time at 53.6; inventories at 51.5; and employment at 49.4. According to ITA data, the Oklahoma manufacturing sector exported $1.8 billion in goods for the first quarter of 2025 compared to $1.7 billion for the same period in 2024, for a 6.4% gain.

South Dakota: The May Business Conditions Index for South Dakota slumped to 48.7 from April’s 55.8. Components of the overall May index were: new orders at 50.0; production or sales at 47.1; delivery lead time at 52.4; inventories at 48.3; and employment at 45.6. According to ITA data, the South Dakota manufacturing sector exported $411.0 million in goods for the first quarter of 2025 compared to $499.1 million for the same period in 2024, for a 17.7% decline.

Survey results for the month of April will be released on July 1, 2025, the first business day of the month.

-

Mid-America Manufacturing Expands with Higher Prices

Region Loses Jobs for the Month

April 2025 Survey Highlights:

- The overall Mid-America Business Conditions Index declined for the month but remained above growth neutral for the fourth straight month.

- The April employment index tumbled to 44.9, its lowest level since November 2024.

- The wholesale price index climbed for the seventh straight month to its highest reading since May 2024.

- Approximately 65% of supply managers reported that rising tariffs and supply chain interruptions have resulted in higher input prices.

- As indicated by a supply manager in the April survey, “The uncertainty (surrounding tariffs) is paralyzing.”

- As a result of slowing growth and upward inflationary pressures, Goss expects no change in short-term interest rates at the Federal Reserve’s next meeting on May 6-7.

- According to U.S. International Trade Administration (ITA) data, the regional economy exported $14.7 billion in manufactured goods for the first two months of 2025, compared to $15.3 billion for the same period in 2024, for a 4.2% decline.

OMAHA, Neb. (May 1, 2025) — The Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, moved above growth neutral of 50.0 for a third straight month.

Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, declined to a solid 53.3 from March’s stronger 56.7.

“The Creighton survey is recording significant volatility, much like other regional economic measures. Proposed and implemented tariffs are not only producing economic volatility but are damaging supply managers’ economic outlook and pushing input prices higher,” said Ernie Goss, PhD, Director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business.

The Mid-America report is produced independently of the national ISM.

As indicated by a supply manager in the April survey, “The uncertainty (surrounding tariffs) is paralyzing.”

Employment: The April employment index tumbled to 44.9, its lowest level since November 2024, and down from 67.6 in March. “First quarter employment was pushed higher due to higher production in anticipation of the fallout from tariffs later in the year. April’s reading represented a return to manufacturing job losses in the region,” said Goss.

As reported by one supply manager in April, “Employees are concerned about the economy and their jobs.”

U.S. Bureau of Labor Statistics data show that the region shed 11,900 (-0.8%) manufacturing jobs over the past 12 months. The U.S. lost 74,000 (-0.6%) manufacturing jobs over the same time period.

Comments from Supply Managers in March:

- "While the tariffs seem painful, it is my opinion that this approach is the correct reset. The social economical great reset is theft and power.”

- “While the rest of the world seems to be focused solely on tariffs, Trump is playing 4d chess with China, who has fleckless disregard for the international community and the rule of law. They have been buying influence in the western hemisphere for years and thumbing their nose at the WTO and other world bodies who are helpless to stop them.”

- “If the U.S. doesn't curb the Chinese ambitions, we will all be speaking Mandarin and Cantonese in the next decade! The unrest in the world today was created and is being perpetuated by China, Russia, Iran and other bad actors.”

- “The Chinese want to control Taiwan to keep U.S. influence out of the region with Japan and other smaller nations in their crosshairs. The U.S. is the only one capable of restoring global order with the support of its allies. The global economy will get worse before it gets better!”

- “The impact of the tariffs is just starting to be realized. Changes will be made now that the actual dollar impact is known.”

Wholesale Prices: The April price gauge rose to 65.0, its highest reading since May 2024, and up from 63.7 in March. “The regional inflation yardstick has clearly moved into a range indicating that inflationary pressures are moving higher. Even so, I expect the Fed to leave interest rates unchanged at its next meetings on May 6-7,” said Goss.

Approximately 65% of supply managers reported that rising tariffs and supply chain interruptions have resulted in higher input prices.

Roughly 85% reported impacts from tariffs, either via higher prices or supply chain interruptions.

As reported by an April survey participant, “Some companies will push through price increases. Some won’t be able to due to the elasticity (responsiveness) of demand.”

Confidence: Looking ahead six months, economic optimism, as captured by the April Business Confidence Index, sank to 35.3, its lowest reading since September 2024, and down from 37.5 in March. “Due to concerns regarding global economic tensions and rising tariffs, only one in four of supply managers expect improving business conditions over the next six months,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, expanded to 56.7 from March’s weak 32.5. “In order to front-run tariffs, firms have expanded inventories for three of the first four months of 2025,” said Goss.

Approximately 21.1% of supply managers reported that higher tariffs have pushed their firms to switch suppliers for a share of their inputs.

Trade: Recent uncertainty regarding tariffs and trade restrictions pushed trade numbers lower for April. New export orders slumped to 46.2 from 52.6 in March. As result of record imports for the first two months of 2025, supply managers pulled back on purchasing from abroad in March and April. The April import index fell to a record low of 12.5 from March’s 32.6.

According to U.S. International Trade Administration (ITA) data, the regional economy exported $14.7 billion in manufactured goods for the first two months of 2025, compared to $15.3 billion for the same period in 2024, for a 4.2% decline. In terms of export gainers, Oklahoma registered the top gain with a 11.4% addition, and South Dakota recorded the largest loss with a 24.5% reduction in the export of manufactured goods.

Other survey components of the March Business Conditions Index were: New orders declined to 52.9 from 55.9 in March; the production or sales index was unchanged at 55.4; and the speed of deliveries of raw materials and supplies increased to 56.8 from March’s 56.0. Higher readings indicate rising supply chain disruptions or delays.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Arkansas: The state’s April Business Conditions Index decreased to 57.5 from 62.4 in March. Components from the April survey of supply managers were: new orders at 56.8; production or sales at 53.3; delivery lead time at 60.1; inventories at 64.5; and employment at 52.6. According to ITA data, the Arkansas manufacturing sector exported $920.3 million in goods for the first two months of 2025, compared to $933.1 million for the same period in 2024, for a 1.4% reduction.

Iowa: The state’s Business Conditions Index for April declined to 53.0 from 56.3 in March. Components of the overall April index were: new orders at 52.6; production or sales at 54.9; delivery lead time at 57.1; employment at 44.0; and inventories at 56.6. According to ITA data, the Iowa manufacturing sector exported $2.3 billion in goods for the first two months of 2025, compared to $2.6 billion for same period in 2024, for a 12.0% reduction.

Kansas: The Kansas Business Conditions Index for April sank to 51.1 from March’s 53.9. Components of the leading economic indicators from the monthly survey of supply managers for April were: new orders at 55.6; production or sales at 53.8; delivery lead time at 54.8; employment at 61.3; and inventories at 44.3. According to ITA data, the Kansas manufacturing sector exported $1.8 billion in goods for the first two months of 2025, compared to $2.0 billion for the same period in 2024, for a 9.2% reduction.

Minnesota: The April Business Conditions Index for Minnesota declined to 56.7 from 60.4 in March. Components of the overall April index were: new orders at 53.2; production or sales at 56.5; delivery lead time at 59.6; inventories at 63.2; and employment at 51.2. According to ITA data, the Minnesota manufacturing sector exported $3.8 billion in goods for the first two months of 2025, compared to $4.1 billion for the same period in 2024, for a 7.8% reduction.

Missouri: The state’s April Business Conditions Index fell to 48.1 from March’s 51.5. Components of the overall index from the survey of supply managers for April were: new orders at 51.9; production or sales at 52.6; delivery lead time at 53.8; inventories at 47.7; and employment at 34.3. According to ITA data, the Missouri manufacturing sector exported $2.6 billion in goods for the first two months of 2025, compared to $2.4 billion in goods for the same period in 2024, for a 7.6% gain.

Nebraska: : For the 10th time in the past 11 months, Nebraska’s overall index climbed above the growth neutral threshold. The state’s April Business Conditions Index stood at 50.1, down from 53.8 in March. Components of the index from the monthly survey of supply managers for April were: new orders at 52.2; production or sales at 53.5; delivery lead time at 55.1; inventories at 51.3; and employment at 38.2. According to ITA data, the Nebraska manufacturing sector exported $1.0 billion in goods for the first two months of 2025, compared to $1.1 billion for the same period in 2024, for a 6.5% reduction.

North Dakota: The state’s Business Conditions Index advanced above growth neutral for a 10th consecutive month to 52.5, which was down from March’s much stronger 59.0. Components of the overall index for April were: new orders at 52.6; production or sales at 54.6; delivery lead time at 56.8; employment at 42.9; and inventories at 55.6. According to ITA data, the North Dakota manufacturing sector exported $870.8 million in goods for the first two months of 2025, compared to $819.9 million for the same period in 2024, for a 6.2% gain.

Oklahoma: The state’s Business Conditions Index for April advanced to 56.8 from March’s solid 53.6. Components of the overall April index were: new orders at 53.2; production or sales at 56.5; delivery lead time at 59.6; inventories at 63.2; and employment at 51.3. According to ITA data, the Oklahoma manufacturing sector exported $1.2 billion in goods for the first two months of 2025, compared to $1.0 billion for the same period in 2024, for an 11.4% gain.

South Dakota: The April Business Conditions Index for South Dakota decreased to 55.8 from March’s 61.6. Components of the overall April index were: new orders at 53.0; production or sales at 56.1; delivery lead time at 59.0; inventories at 61.4; and employment at 49.3. According to ITA data, the South Dakota manufacturing sector exported $250.9 million for the first two months of 2025, compared to $332.1 million for the same period in 2024, for a 24.5% reduction.

Survey results for the month of April will be released on June 2, 2025, the first business day of the month.

-

The overall Mid-America Business Conditions Index climbed to 56.7, its highest level since July 2022.

- The March Business Confidence Index plummeted to its lowest level since September 2024 with supply managers voicing concerns over tariffs.

- As indicated by a participating supply manager, “Our downstream customers tell us that consumers have reduced the purchasing of big ticket items due to the turmoil at the federal level.”

- Another supply manager said they are, “Taking steps to mitigate tariff impact. Already implemented a surcharge to account for the 25% tariff on incoming steel.”

- For a sixth straight month, the wholesale price inflation gauge increased, indicating expanding inflationary pressures. Even so, Goss expects the Federal Reserve to hold off on any interest rate change at its next meetings on May 6-7.

- The March employment index soared to its highest level since July 2022.

- According to U.S. International Trade Administration (ITA) data, the regional economy began the year with manufacturing exports at $7.1 billion, essentially flat from the same period in 2024.

-

For only the fourth time since July 2024, the overall, or Business Conditions Index, climbed above growth neutral to 52.0 in February.

- For a fifth straight month, the wholesale price inflation gauge increased, indicating expanding inflationary pressures. Even so, Goss expects the Federal Reserve to hold off on any interest rate change at its next meeting on March 18-19.

- On average, supply managers expect tariffs, if implemented, to increase input prices by 9.6%.

- Fears of rising tariffs pushed imports to a record-high level.

- According to 2024 U.S. International Trade Administration data, the regional economy expanded 2024 manufacturing exports by $1.0 billion from 2023 for a 1.1% gain.

- In terms of 2023 to 2024 export gainers and losers, Minnesota registered the top increase with a $2.1 billion addition, while North Dakota recorded the largest loss with a $3.1 billion reduction in the export of manufactured goods.

-

For only the third time since July 2024, the overall Mid-American PMI Business Conditions Index, climbed above growth neutral to 51.1 in January.

- For a fourth straight month, the wholesale price inflation gauge rose but continues to indicate modest inflation.

- Due to modest inflationary pressures, Goss expects the Federal Reserve to hold on any interest rate change at its next meeting on March 18-19.

- After 12 straight months of job losses, the region’s employment gauge climbed above growth neutral.

- In anticipation of higher costs from tariff implementation, firms increased their inventory levels in January and increased imports to a record high.

- According to the latest U.S. International Trade Administration data, the regional economy expanded 2024 year-to-date manufacturing exports by $797.2 million from the same period in 2023 for a 0.9% gain.

- Mexico was the top 2024 destination for regional agriculture and livestock exports.