2026-05-11 · 10:00

Average New Vehicle Transaction Price: April 2026

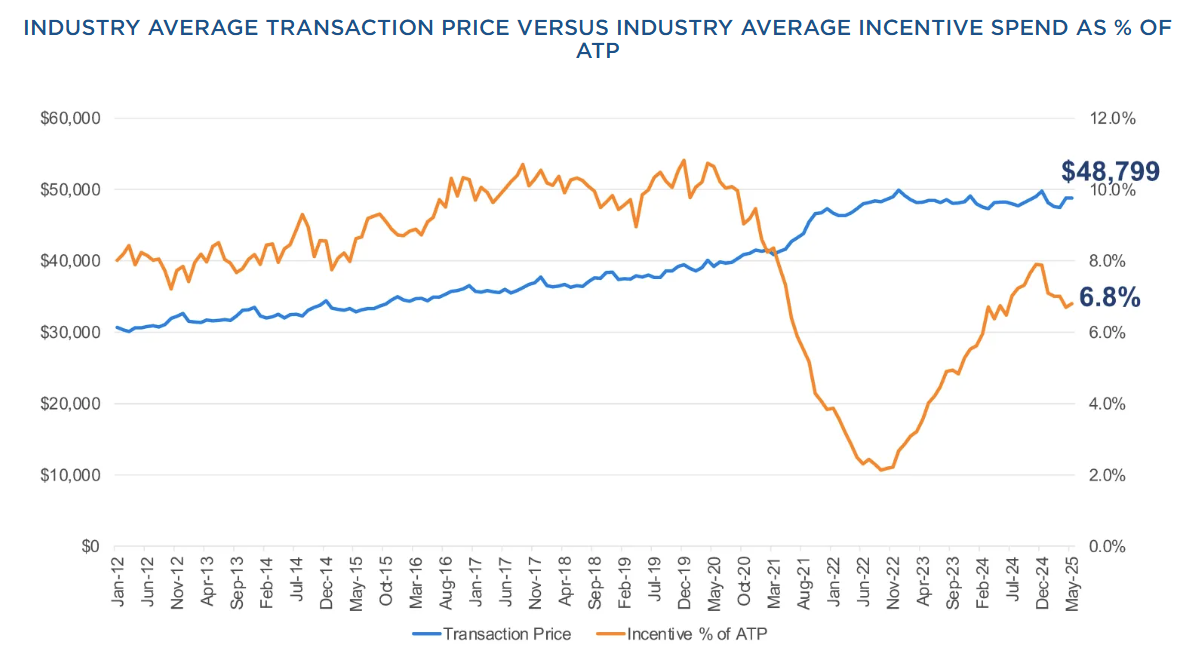

Cox Automotive Average New Vehicle Transaction Price

About

Latest Releases

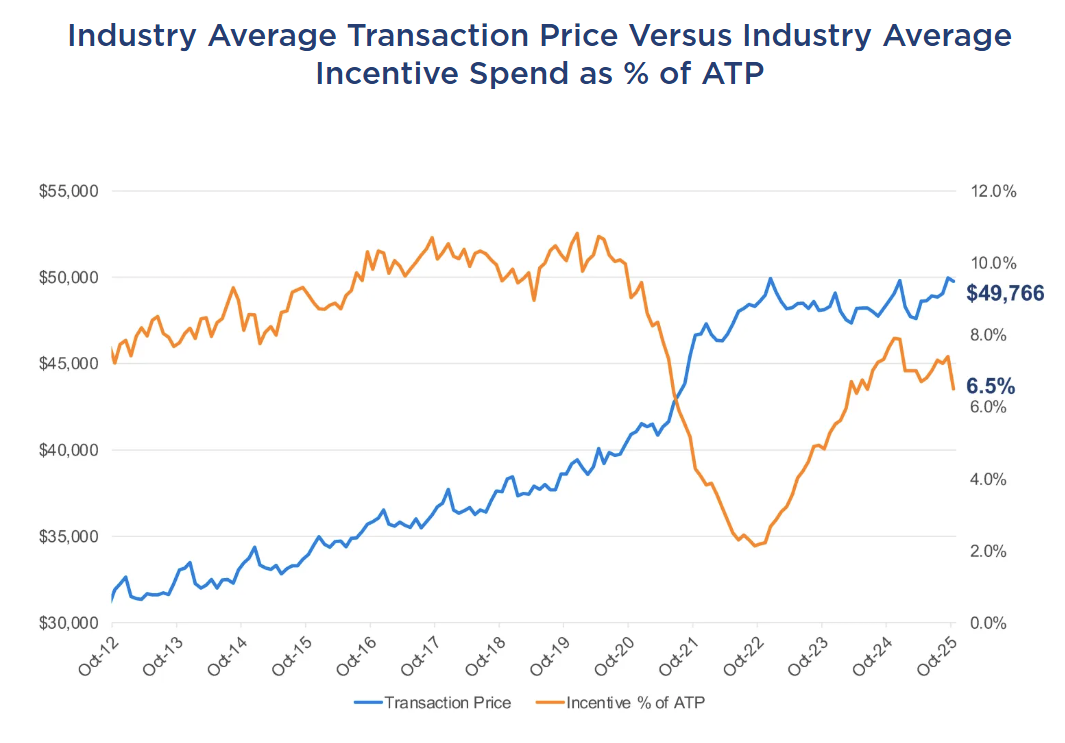

12

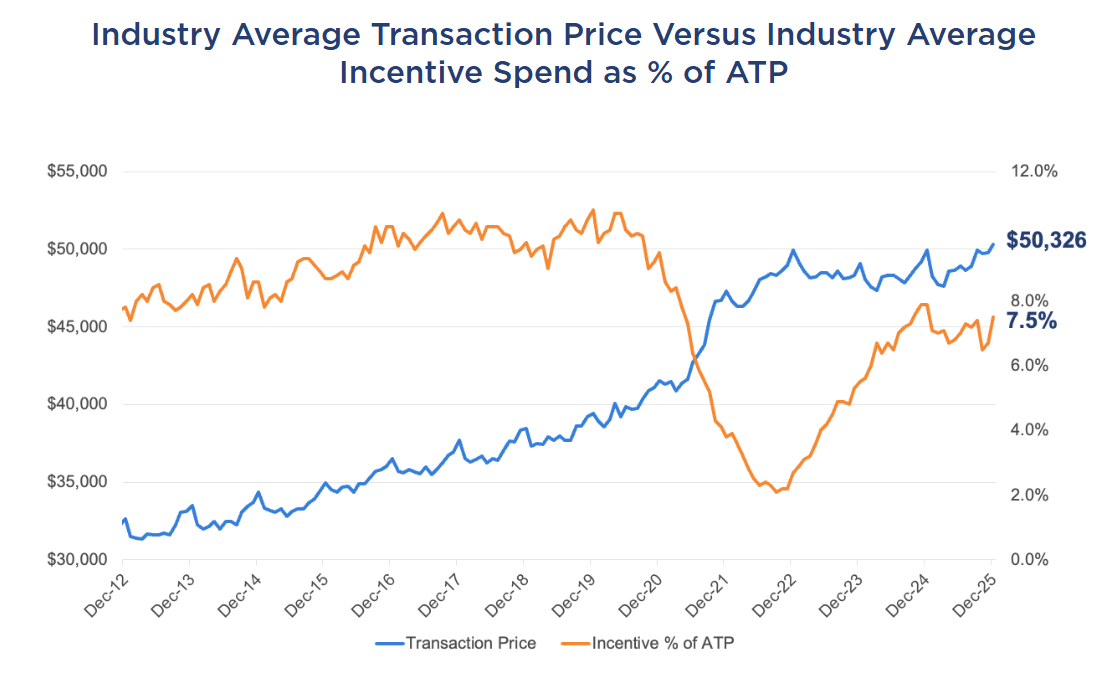

2026-04-10 · 10:00

Average New Vehicle Transaction Price: March 2026

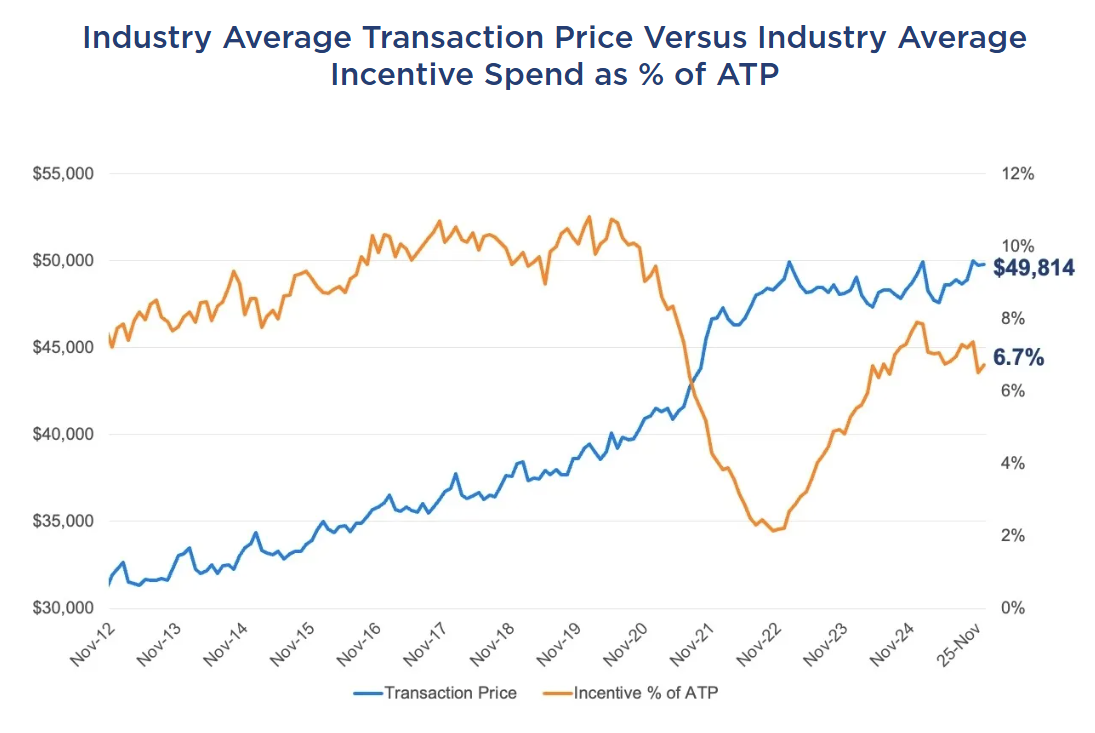

2026-03-10 · 10:00

Average New Vehicle Transaction Price: February 2026