Conference Board Leading Economic Index

About

Latest Releases

12

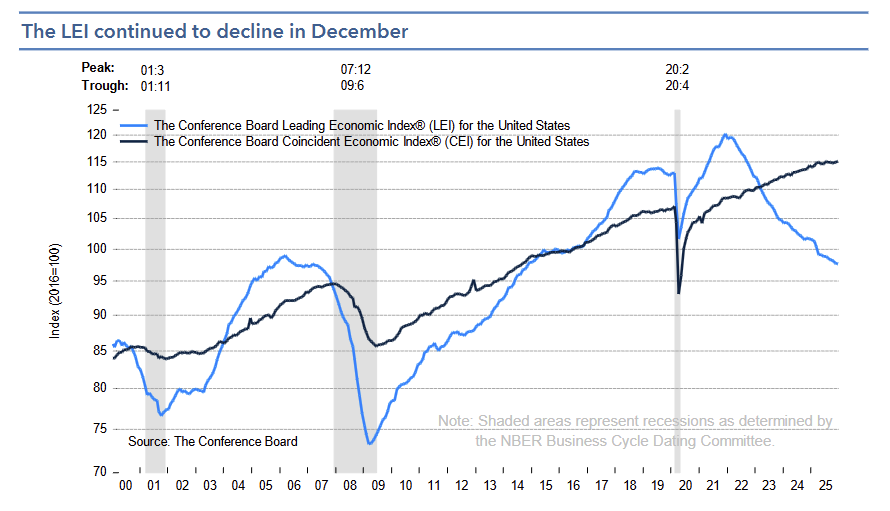

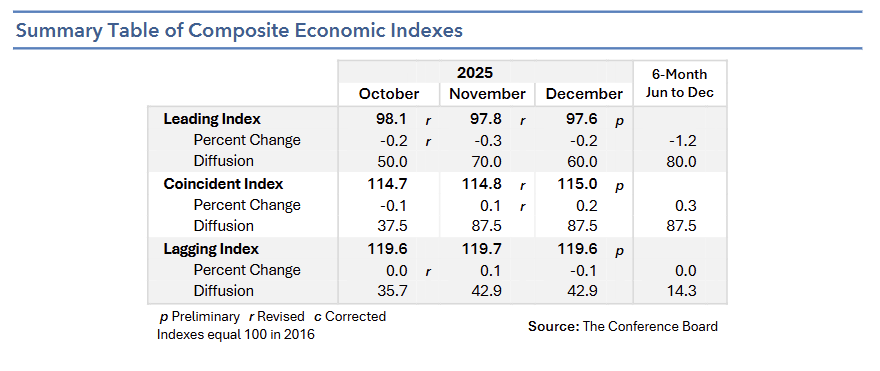

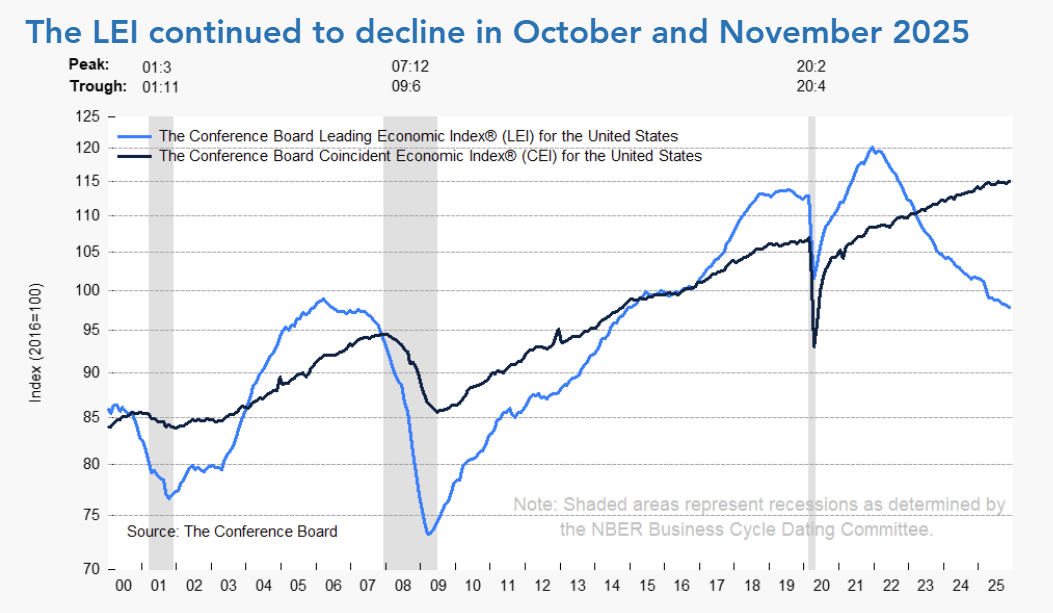

The Conference Board LEI fell -0.2% MoM in December 2025 (fifth straight decline), signaling continued early-2026 softness.

-

The LEI declined to 97.6 after -0.3% MoM in November and -0.2% MoM in October, extending a multi-month weakening trend.

-

Over H2 2025, the LEI fell -1.2% vs -2.8% in H1 2025, indicating a slower pace of deterioration compared with earlier in the year.

-

Positive contributors included building permits and financial components, with the yield spread turning positive in November and December.

-

Negative contributors were consumer expectations, ISM new orders, higher unemployment claims, and lower manufacturing hours, pointing to softer demand and labor indicators.

-

The CEI rose +0.2% MoM to 115.0 after +0.1% in November and grew +0.3% in H2 2025, showing modest improvement in current-activity measures.

-

The LAG edged down -0.1% MoM to 119.6 and was unchanged in H2 2025, slowing from a +1.2% gain in H1 2025, indicating fading momentum in backward-looking indicators.

-

The Conference Board expects GDP growth of 2.1% YoY in 2026 vs 2.2% in 2025, consistent with a projected slowdown into early 2026.

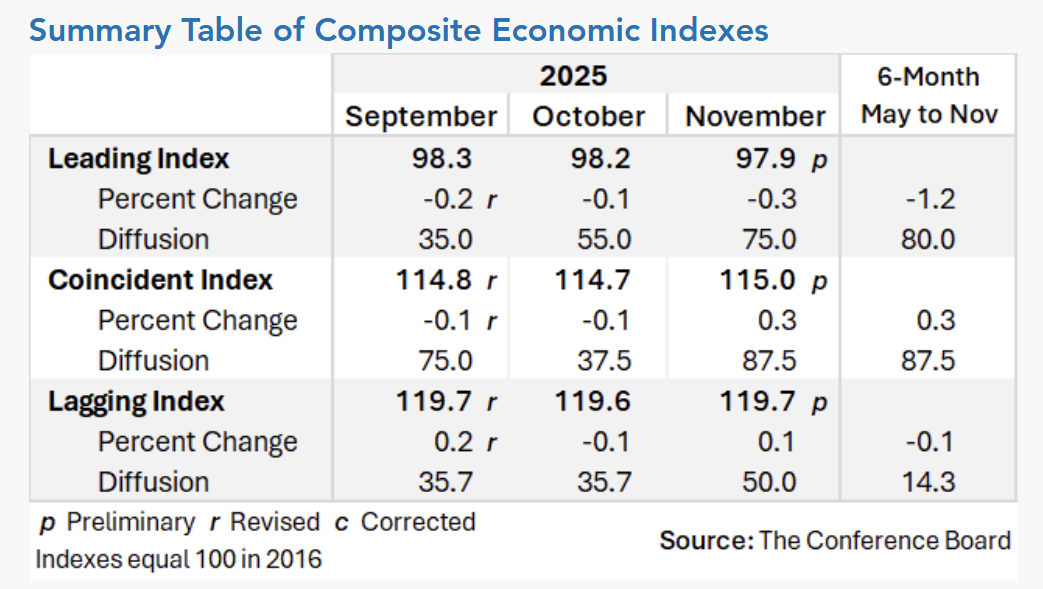

The Conference Board’s US Leading Economic Index (LEI) fell -0.3% MoM in November 2025 to 97.9, extending the mild downtrend in forward-looking conditions.

-

The LEI decline followed a -0.1% MoM drop in October (to 98.2) and a level of 98.3 in September, indicating back-to-back monthly softening.

-

Over the six months from May to November 2025, the LEI fell -1.2%, a slower contraction than the prior six-month decline of -2.6% (Nov 2024 to May 2025), suggesting the pace of deterioration has moderated.

-

The main drags in 2025 were weak consumer expectations and softer new orders, highlighting continued caution in forward demand signals.

-

Positive contributions in November were led by labor market related components such as initial claims for unemployment insurance and weekly hours worked in manufacturing, partially offsetting broader weakness.

-

The Coincident Economic Index (CEI) rose +0.3% MoM in November to 115.0 after -0.1% declines in Aug-Sep-Oct, showing a near-term rebound in current-activity indicators.

-

Over May to November 2025, the CEI increased +0.3%, slower than the +0.9% gain in the prior six months, indicating softer trend growth in coincident measures.

-

The Lagging Economic Index (LAG) edged up +0.1% MoM in November to 119.7, reversing October’s -0.1% decline, but was down -0.1% over the past six months after rising +0.9% in the prior period.

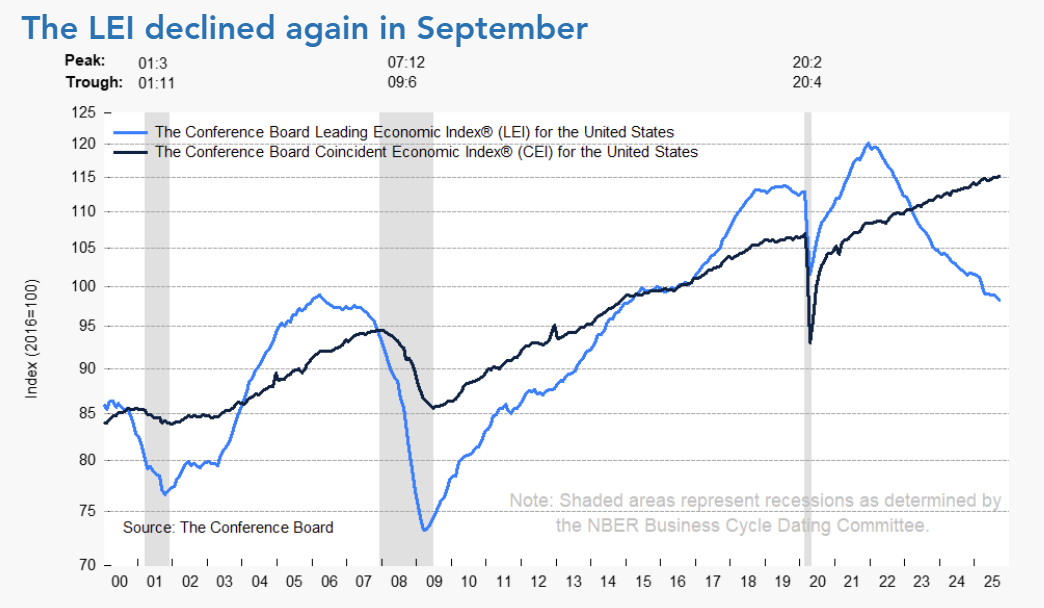

The US Leading Economic Index (LEI) fell -0.3% MoM to 98.3 in September 2025, marking a second straight monthly decline and reflecting weakening expectations from consumers and businesses.

-

The LEI contracted -2.1% over the six months ending in September, a faster decline than the -1.3% drop in the prior six-month period, indicating a steady loss of momentum through 2025.

-

Negative contributors to the LEI included consumer expectations, the ISM New Orders Index, manufacturers’ new orders for consumer goods and materials, inverted initial jobless claims, and the yield curve, all highlighting softer forward-looking demand signals.

-

Stock prices, the Leading Credit Index, and manufacturers’ new orders of nondefense capital goods excluding aircraft contributed positively, offering limited offsets to the broader weakness.

-

The Coincident Economic Index (CEI) rose +0.1% MoM to 115.1, with a six-month gain of +0.3%, down from +1.1% in the prior period; three of the four CEI components improved slightly in September.

-

The Lagging Index (LAG) increased +0.1% MoM to 119.6 and was up +0.5% over the past six months, a modest deceleration from the +0.6% gain in the previous interval.

-

The Conference Board noted that GDP growth is expected to slow to 1.8% in 2025 and 1.5% in 2026, with end-of-year activity pressured by tariff adjustments, softer consumer momentum, and disruptions from the federal government shutdown.

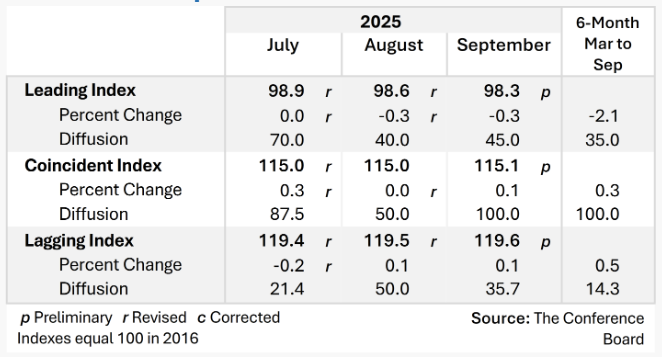

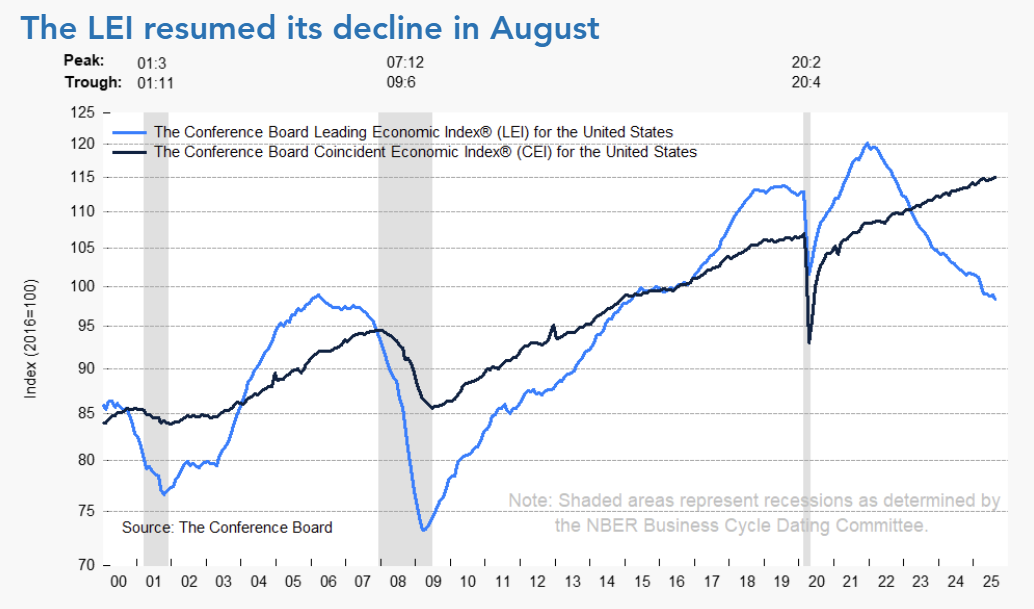

The Conference Board Leading Economic Index (LEI) for the US fell -0.5% MoM to 98.4 in August 2025, its steepest drop since April, and is down -2.8% over the past six months, pointing to persistent headwinds.

-

The decline was broad-based, with negative contributions from consumer expectations (-0.19 pts), ISM New Orders (-0.08 pts), building permits (-0.11 pts), average weekly hours in manufacturing (-0.12 pts), and higher initial jobless claims (-0.06 pts).

-

Only stock prices (+0.07 pts) and the Leading Credit Index (+0.05 pts) contributed positively in August, while the yield spread turned slightly negative for the first time since April.

-

The Coincident Economic Index (CEI) rose +0.2% MoM to 115.0, extending its six-month gain to +0.6%, though growth slowed compared with the previous period (+0.9%).

-

The Lagging Index (LAG) edged up +0.1% MoM to 120.0 in August, with a six-month gain of +0.7%, more than double the +0.3% increase recorded previously.

-

The Conference Board noted that tariffs have already weighed on H1 2025 growth and will remain a drag on GDP in H2 2025 and into H1 2026, with US GDP projected to grow just +1.6% in 2025, down from +2.8% in 2024.

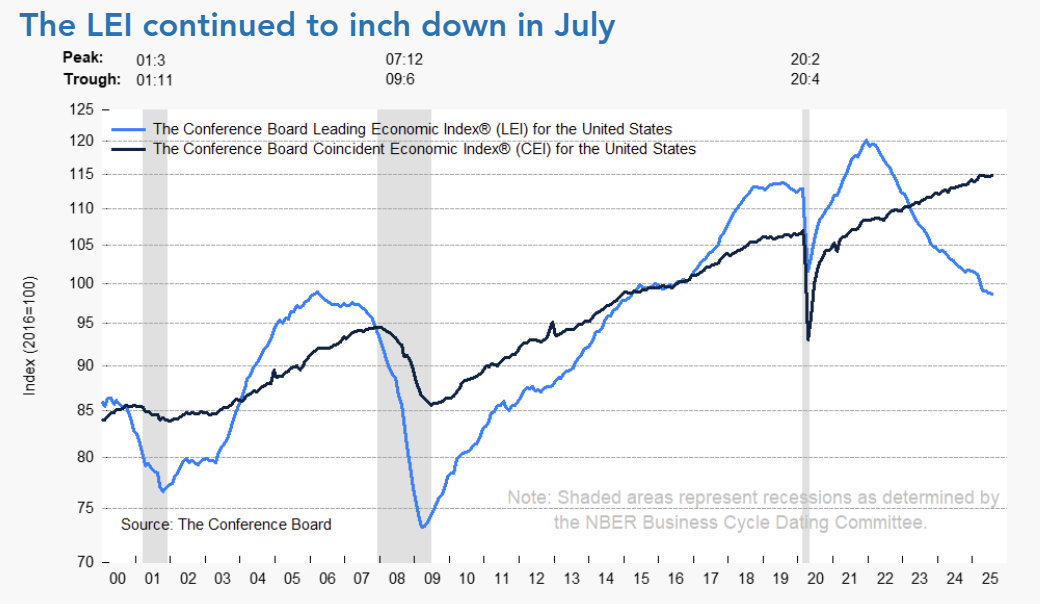

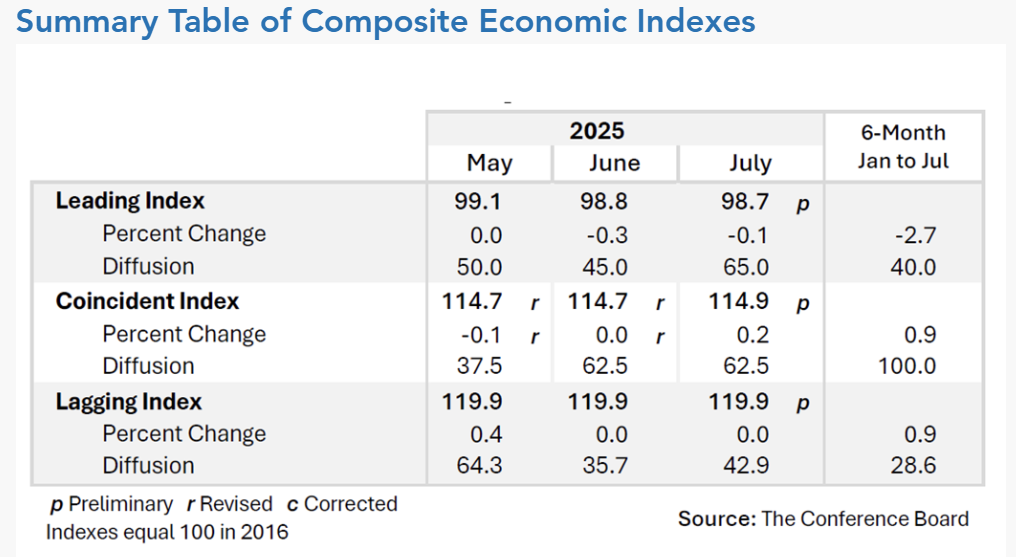

The Conference Board Leading Economic Index (LEI) edged down -0.1% MoM to 98.7 in July 2025, extending its six-month decline to -2.7% and triggering another recession signal.

-

June’s LEI was revised to -0.3% MoM, with pessimistic consumer expectations and weak new orders offsetting support from stock prices and lower jobless claims.

-

The six-month contraction of -2.7% (Jan–Jul 2025) was steeper than the prior -1.0% decline (Jul 2024–Jan 2025).

-

The Coincident Economic Index (CEI) rose +0.2% MoM to 114.9, with all components except industrial production improving; CEI is up +0.9% in H1 2025.

-

The Lagging Economic Index (LAG) was flat at 119.9, but its six-month growth turned positive at +0.9%, reversing a -0.1% decline in the prior period.

-

The Conference Board expects US GDP growth at +1.6% in 2025, though tariffs are projected to weigh on activity in H2 and slow growth to 1.3% in 2026.

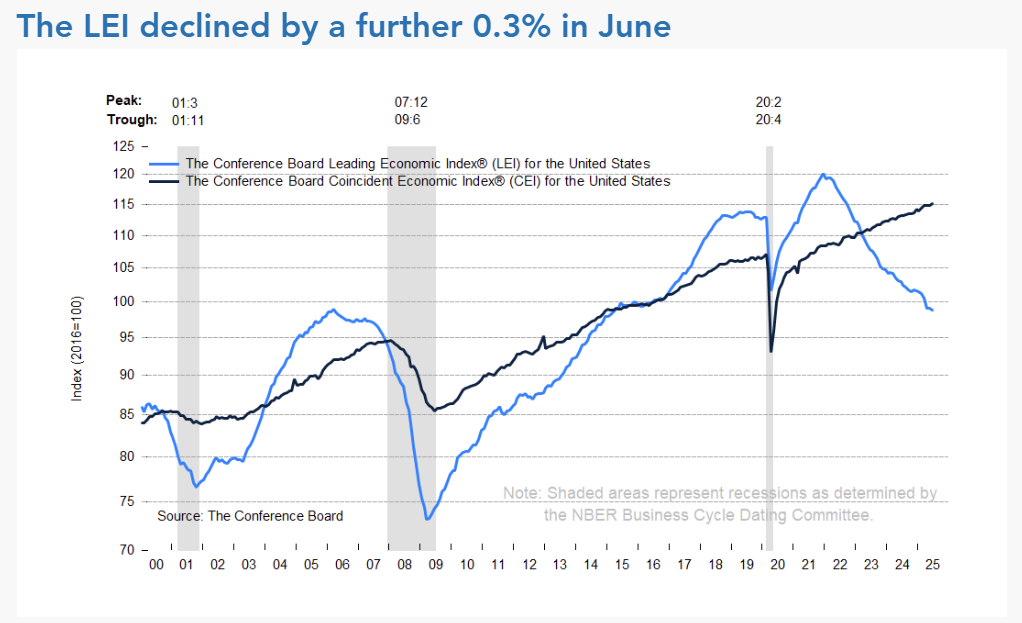

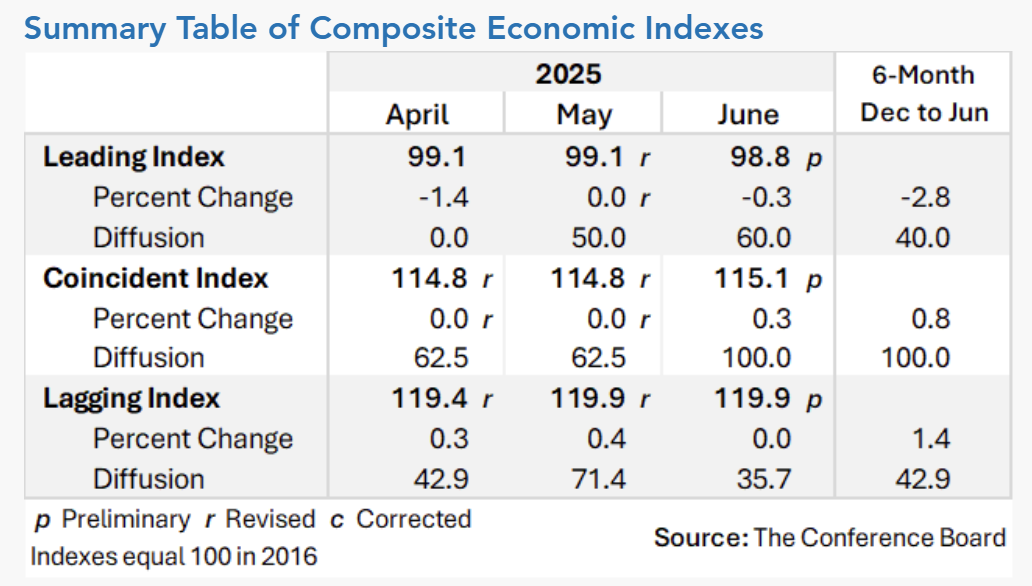

The Conference Board Leading Economic Index (LEI) declined -0.3% MoM to 98.8 in June 2025, marking a -2.8% drop over H1 2025 and triggering a third consecutive recession signal based on the six-month diffusion index.

- May’s LEI was revised up to 0.0% from the originally reported -0.1%.

- Weakness in consumer expectations, new manufacturing orders, and rising jobless claims outweighed support from rising equity prices.

- The Coincident Economic Index (CEI) rose 0.3% MoM to 115.1, with all four components improving; CEI is up 0.8% in H1 2025.

- The Lagging Economic Index (LAG) was flat at 119.9, but the six-month rate turned positive at +1.4% after falling -0.8% in H2 2024.

- The Conference Board expects 2025 GDP growth at 1.6%, with tariffs likely to weigh on H2 consumption.

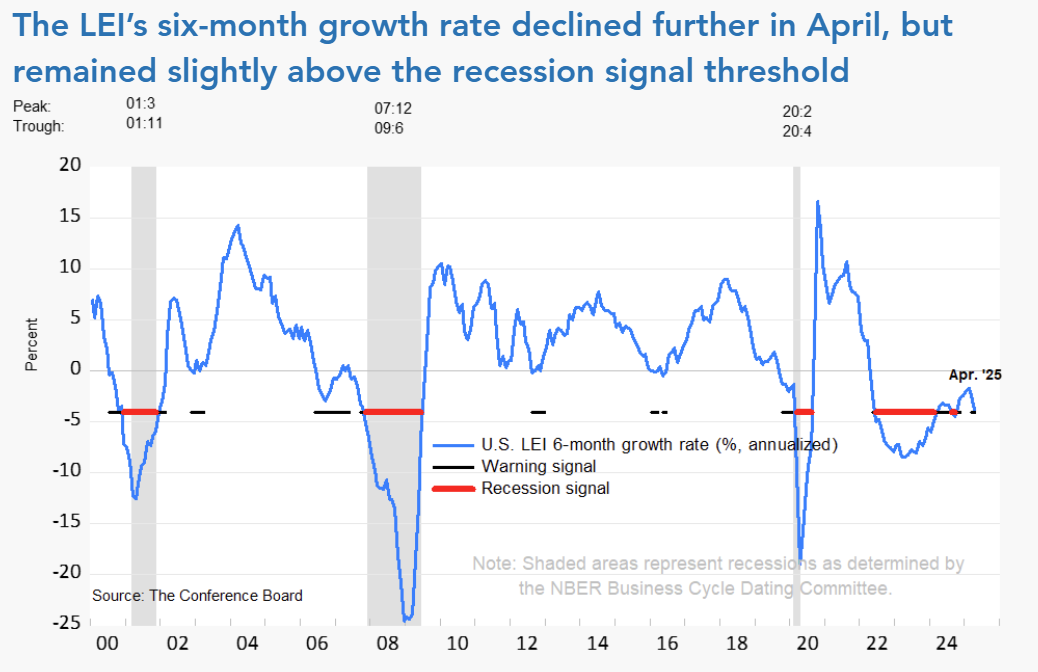

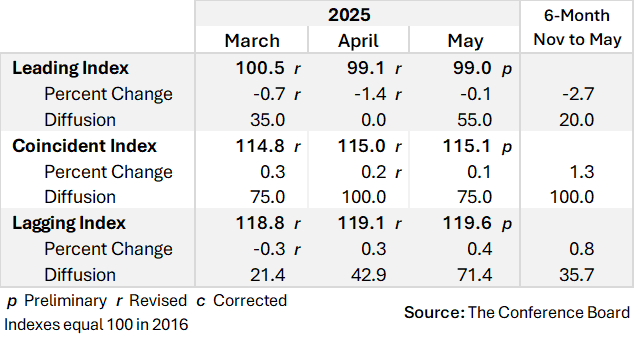

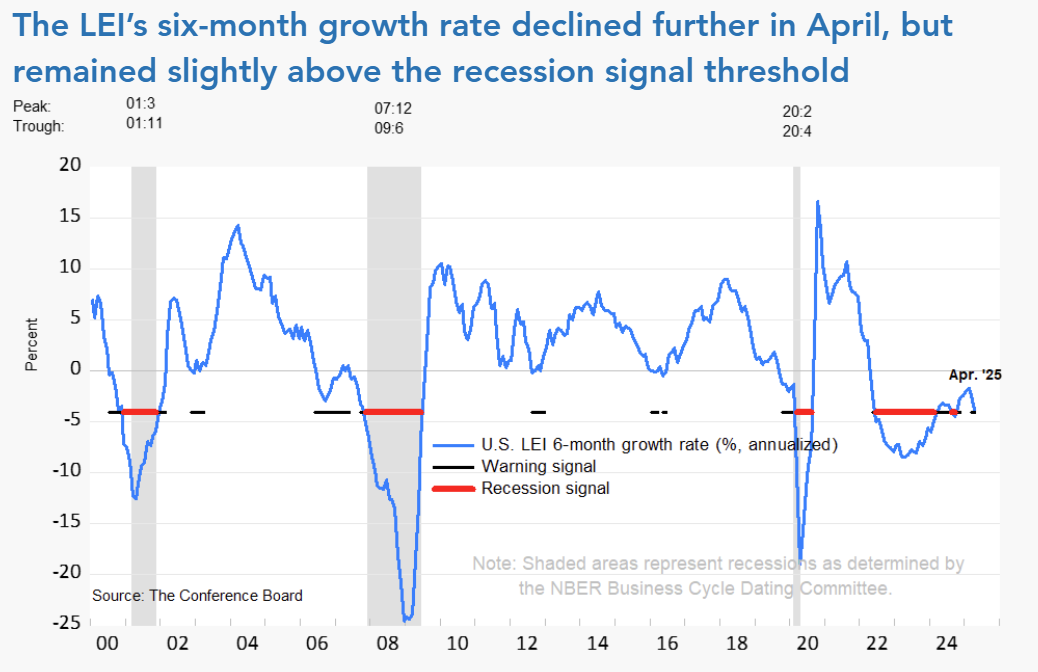

The Conference Board Leading Economic Index (LEI) fell -0.1% MoM to 99.0 in May 2025, marking its third consecutive monthly decline and down -2.7% over the past six months.

- April’s LEI was revised lower to -1.4% MoM from -1.0% previously reported.

- Weakness came from initial jobless claims, consumer expectations, new manufacturing orders, and housing permits; equity markets were a positive contributor.

- The Coincident Index rose 0.1% MoM to 115.1 and is up 1.3% over the past six months, supported by gains in employment and income.

- The Lagging Index increased 0.4% MoM to 119.6 and is up 0.8% over the past six months, reversing a previous six-month decline.

- The Conference Board projects 2025 GDP growth at 1.6%, with risks tilted toward further deceleration due to persistent tariff effects.

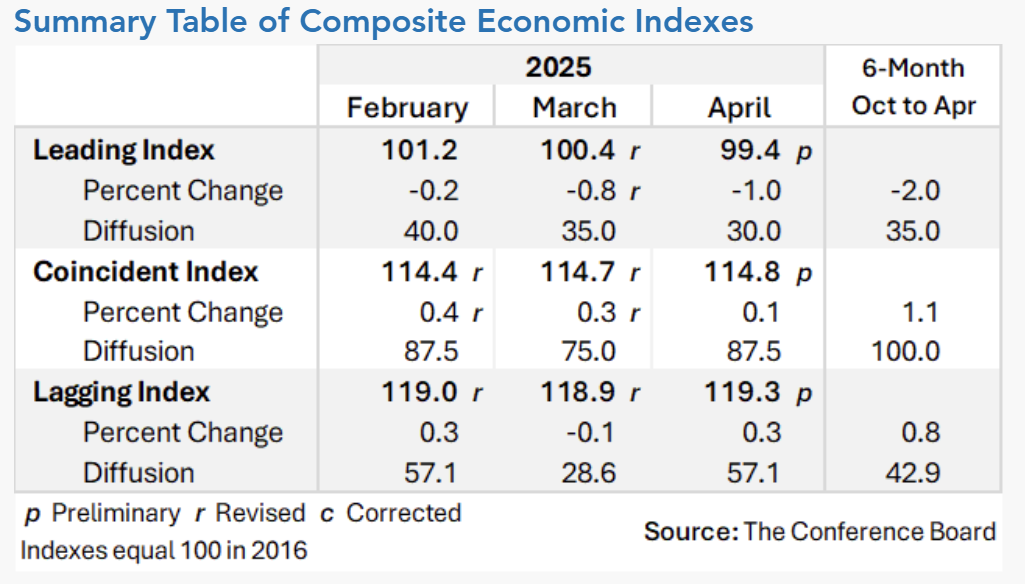

The Conference Board Leading Economic Index fell -1.0% MoM in April to 99.4, the largest monthly drop since March 2023, and is down -2.0% over the past six months.

- March’s LEI decline was revised down to -0.8% MoM from the initially reported -0.7%.

- Consumer expectations worsened for the fourth consecutive month, and building permits and manufacturing hours turned negative.

- The Coincident Economic Index rose 0.1% MoM to 114.8 and is up 1.1% over the past six months.

- The Lagging Economic Index increased 0.3% MoM to 119.3, reversing a previous six-month decline with a +0.8% gain over the latest six months.

- The Conference Board expects US GDP to grow 1.6% in 2025, down from 2.8% in 2024, with Q3 likely bearing the brunt of tariff impacts.