Conference Board Consumer Confidence

About

-

July 28th, 2026 · 10:00 AM

-

August 25th, 2026 · 10:00 AM

-

September 29th, 2026 · 10:00 AM

-

October 27th, 2026 · 10:00 AM

-

November 24th, 2026 · 10:00 AM

-

December 22nd, 2026 · 10:00 AM

Latest Releases

12

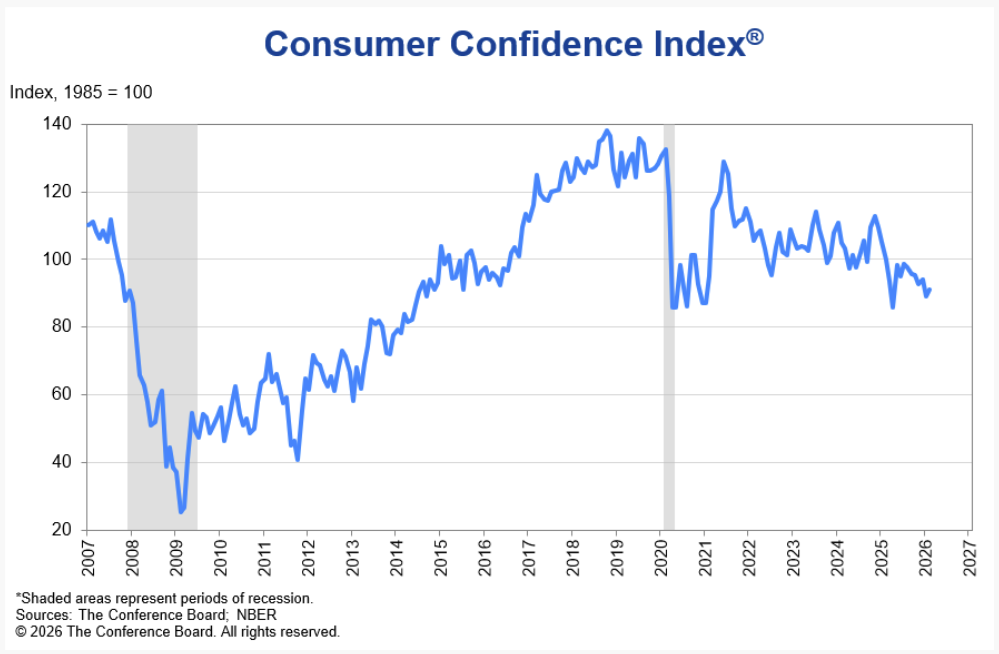

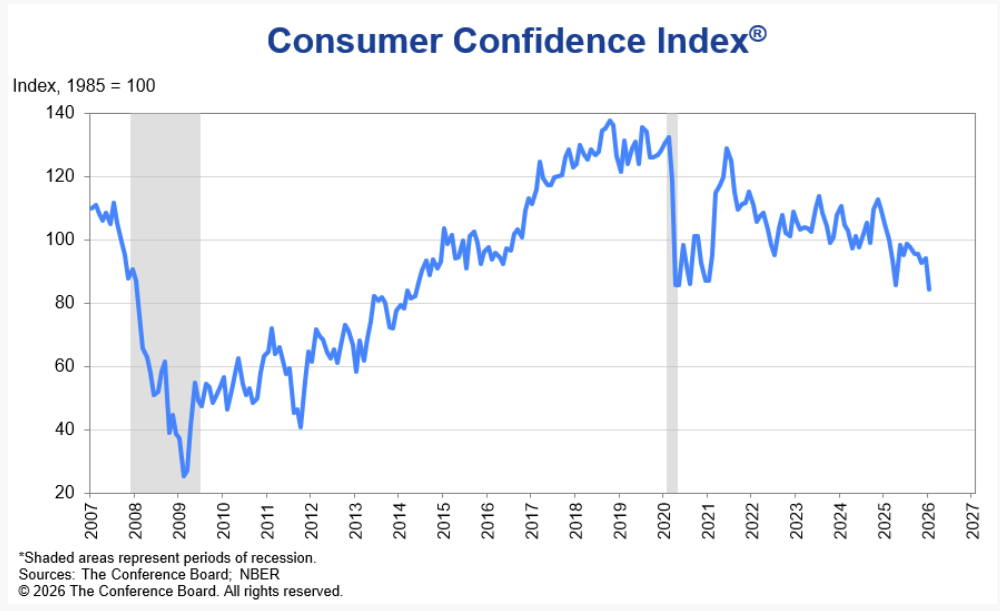

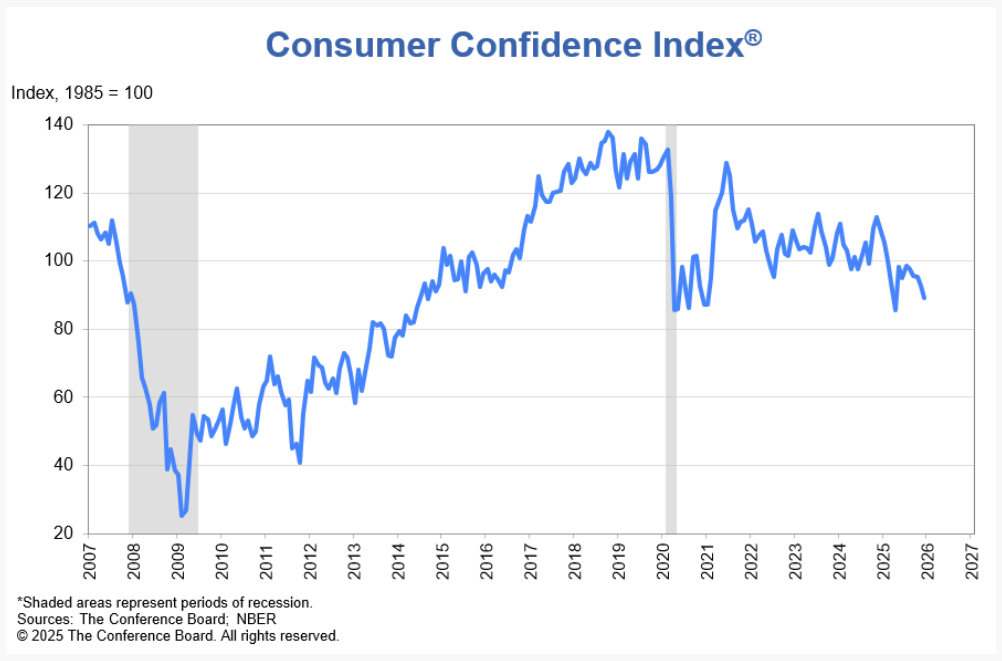

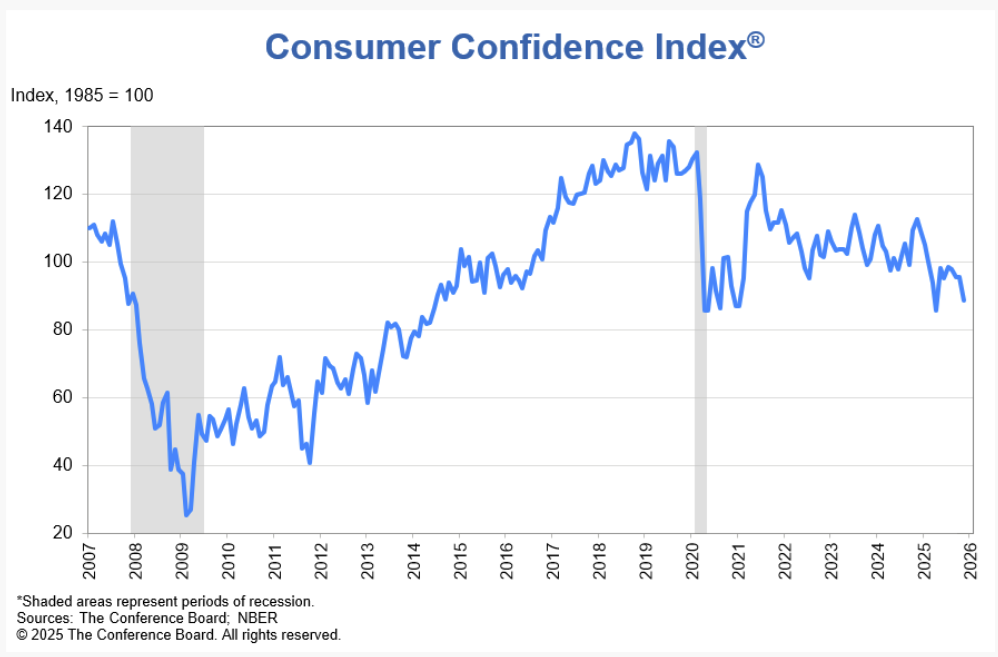

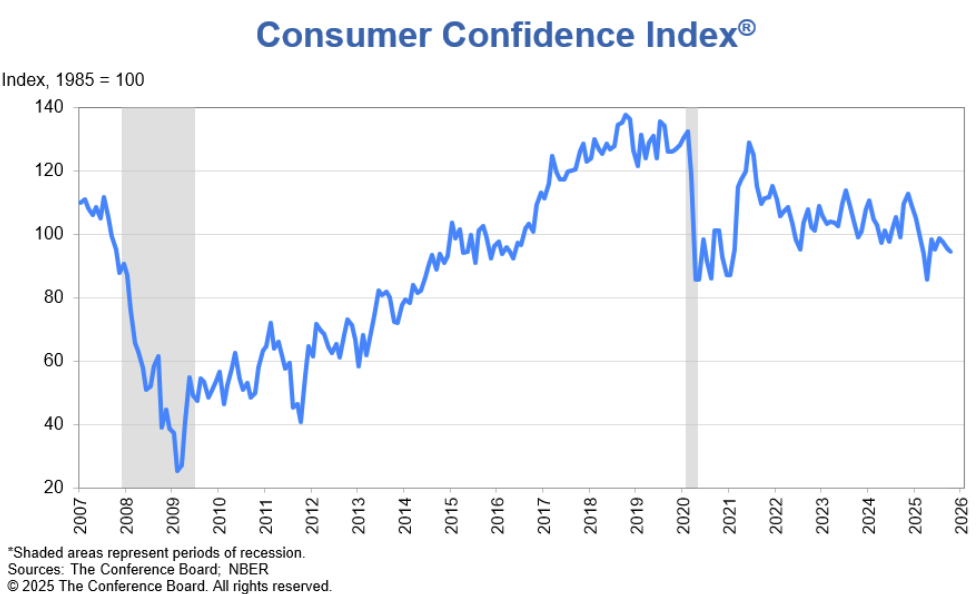

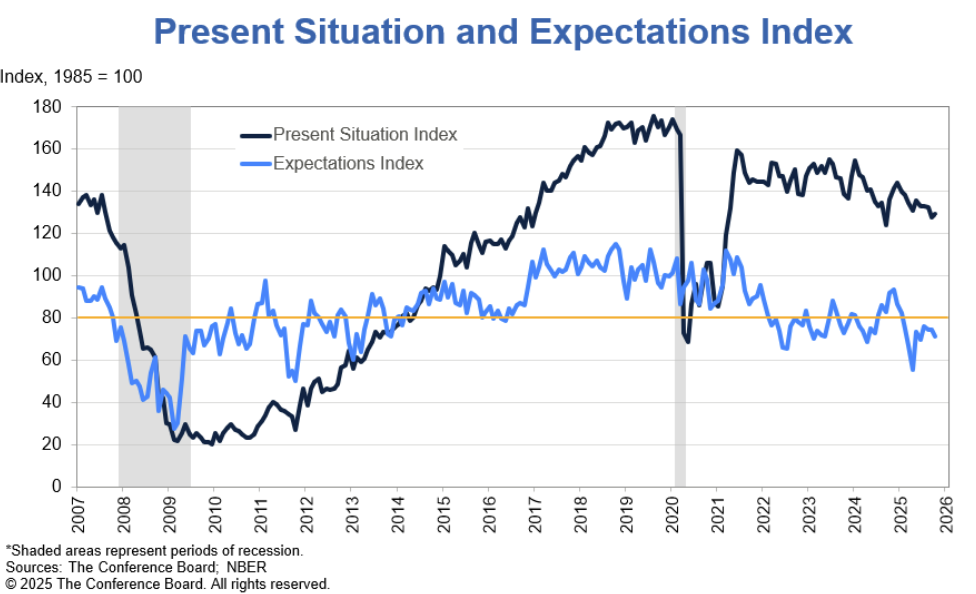

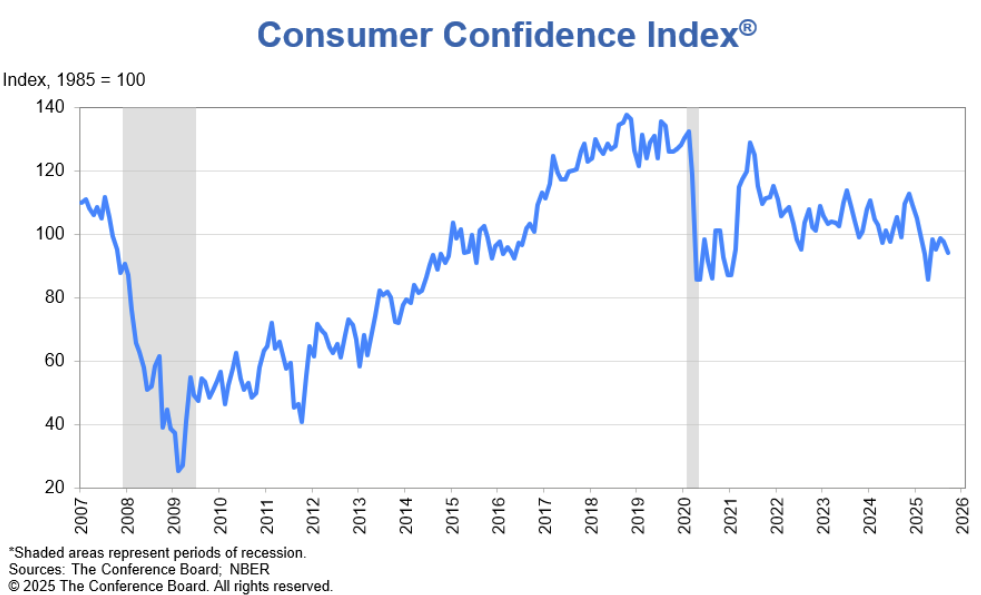

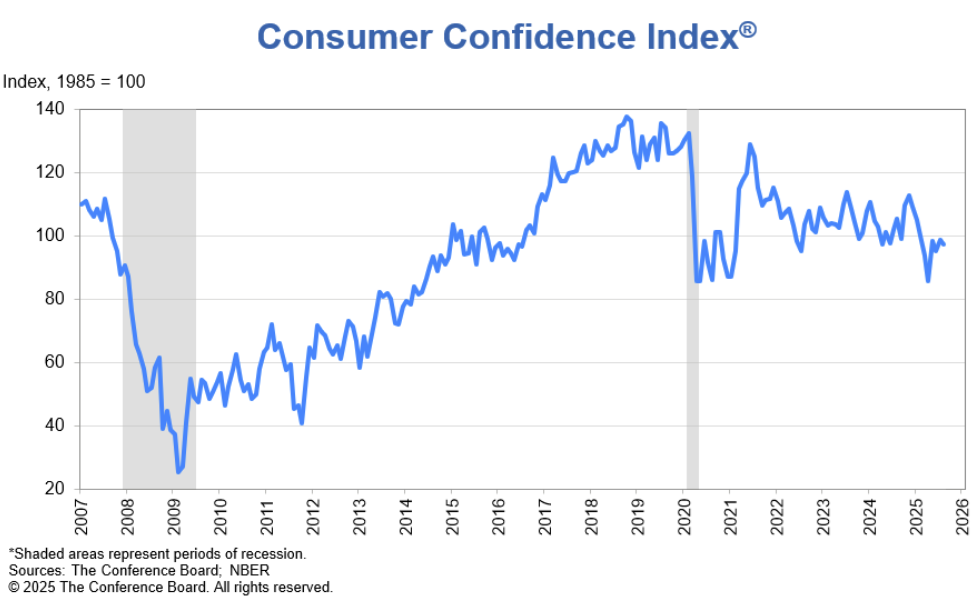

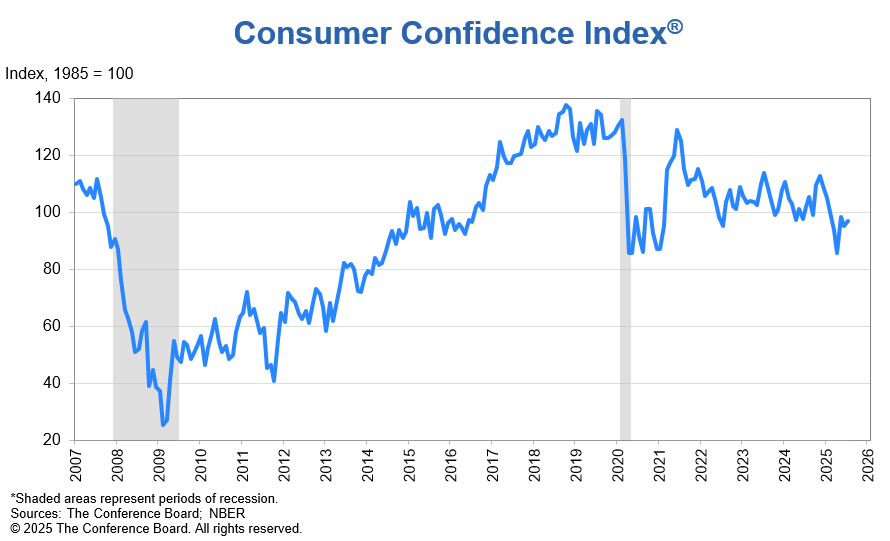

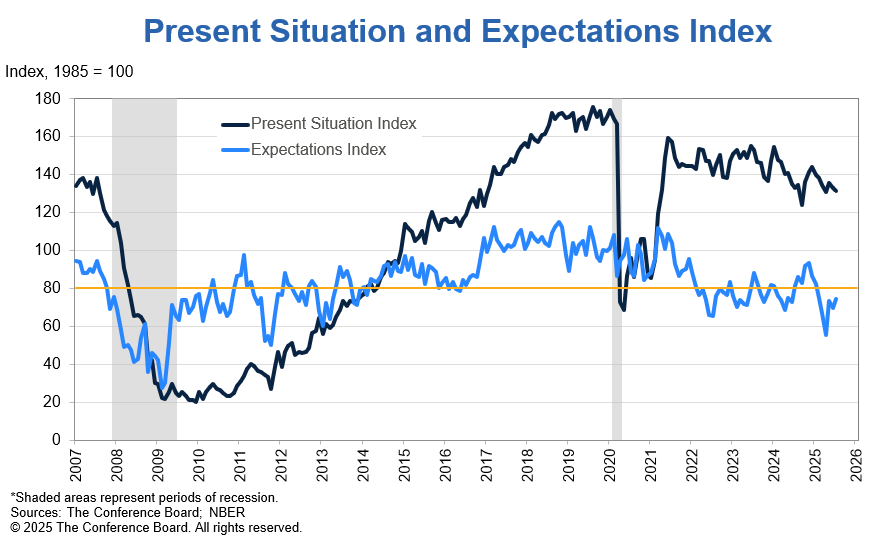

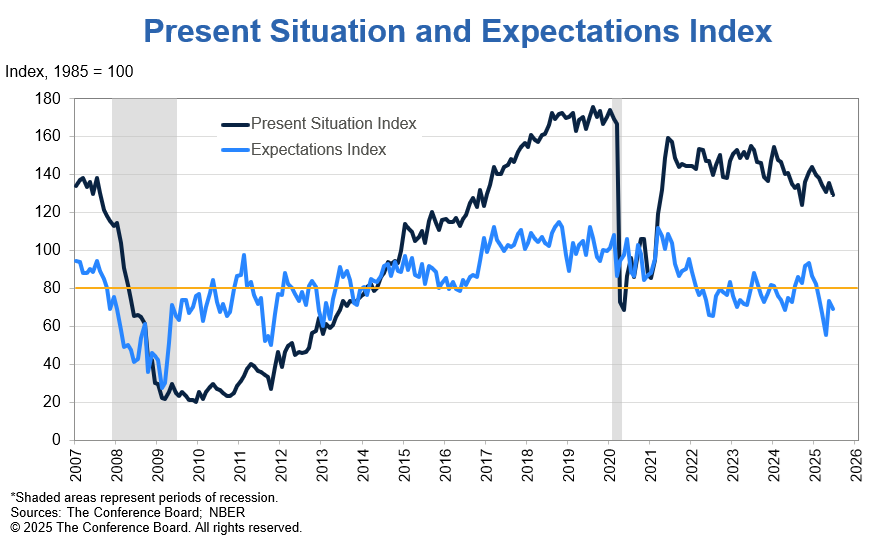

The Conference Board Consumer Confidence Index rose to 91.2 in February (+2.2 pts MoM), showing modest rebound but subdued sentiment.

-

The Present Situation Index fell to 120.0 (-1.8 pts MoM), indicating slightly weaker views of current business and labor conditions.

-

The Expectations Index increased to 72.0 (+4.8 pts MoM), reflecting less pessimistic short-term outlooks for income, business, and jobs.

-

Net business condition views softened as 19.7% said conditions were “good” (Jan: 19.6%) and 19.0% said “bad” (Jan: 17.3%), showing deterioration on balance.

-

Labor market perceptions improved modestly, with jobs “plentiful” at 28.0% (Jan: 25.8%) and “hard to get” at 20.6% (Jan: 19.0%), lifting the labor differential to +7.4%.

-

Future expectations improved as 17.6% expected better business conditions (Jan: 16.5%) and 21.0% expected worsening (Jan: 23.7%), indicating reduced pessimism.

-

Job outlook expectations strengthened, with 15.7% expecting more jobs (Jan: 14.8%) and 26.1% expecting fewer (Jan: 28.7%), pointing to a less negative labor outlook.

-

Income expectations edged higher as 17.3% expected income gains (Jan: 17.2%) while 12.3% expected declines (Jan: 12.7%), suggesting slightly firmer household prospects.

-

Inflation expectations remained elevated and consumers anticipated persistently high interest rates, while big-ticket purchase plans rose and service spending plans softened somewhat.

The Conference Board Consumer Confidence Index fell to 84.5 in January (-9.7 pts MoM), marking a sharp pullback in household sentiment.

-

The headline index dropped to 84.5 from 94.2 in December, reversing last month’s revised uptick and reaching its lowest level since May 2014.

-

The Present Situation Index declined to 113.7 (-9.9 pts MoM), as views on current business and labor market conditions weakened toward neutral.

-

The Expectations Index fell to 65.1 (-9.5 pts MoM), remaining well below the 80 recession-signal threshold and reflecting increasingly negative outlooks.

-

The share saying jobs were plentiful slipped to 23.9% (from 27.5%), while those saying jobs were hard to get rose to 20.8% (from 19.1%), showing softer labor market perceptions.

-

Consumers expecting business conditions to improve declined to 15.6% (from 18.7%), while those expecting conditions to worsen increased to 22.9% (from 21.3%), indicating rising pessimism.

-

Expectations for more job availability fell to 13.9% (from 17.4%), and expectations for fewer jobs increased to 28.5% (from 26.0%), signaling weaker labor market outlooks.

-

Plans for big-ticket purchases and homebuying retreated, while intentions to spend on services softened overall despite continued strength in restaurants and travel-related categories.

The Conference Board Consumer Confidence Index fell to 89.1 in December (from 92.9 in November), marking a fifth consecutive monthly decline and signaling continued erosion in household sentiment.

-

The Present Situation Index dropped sharply to 116.8 (from 126.3; -9.5 pts MoM), as assessments of current business and labor market conditions turned negative for the first time since September 2024.

-

The Expectations Index held steady at 70.7, remaining below the 80 recession-signal threshold for an eleventh straight month, indicating persistently weak views of future income, business, and labor conditions.

-

Labor market perceptions softened further, with the labor market differential continuing to deteriorate as fewer consumers viewed jobs as plentiful relative to those seeing jobs as hard to get.

-

Income expectations weakened, as outlooks for household income growth became less positive compared with November, contributing to the overall decline in expectations.

-

Consumers’ views of their family’s current financial situation moved into negative territory for the first time in nearly four years, highlighting increased financial strain at the household level.

-

Median and average 12-month inflation expectations declined in December after rising in November, while expectations for stock prices over the next year improved to their most positive reading since January 2025.

U.S. consumer confidence fell sharply in November, with the Conference Board Consumer Confidence Index dropping -6.8 pts to 88.7 (from 95.5 in October), reflecting broad deterioration across assessments of current conditions and expectations.

-

The Present Situation Index declined -4.3 pts to 126.9, as fewer consumers viewed business conditions as “good” (19.1 percent vs 20.7 percent) and more viewed them as “bad” (14.9 percent vs 14.5 percent).

-

The Expectations Index fell -8.6 pts to 63.2, remaining below the recession-signal threshold of 80 for the tenth straight month, with weaker outlooks for business conditions, jobs, and incomes.

-

Labor market perceptions softened: the “jobs plentiful” share dropped to 27.6 percent (from 28.6 percent), while “jobs hard to get” dipped to 17.9 percent (from 18.3 percent), continuing a year-long downward drift in the labor differential.

-

Income expectations weakened materially, with only 13.3 percent expecting higher incomes (from 18.2 percent) and 13.8 percent expecting declines (from 11.8 percent), marking the sharpest pullback in six months.

-

Inflation expectations stayed elevated, with median 12-month expectations rising to 4.8 percent, while about half of consumers anticipated higher interest rates ahead.

-

Assessments of current family finances fell to their lowest level since August 2024, while expectations for future finances also worsened, reflecting more cautious household sentiment.

-

Buying plans for big-ticket goods declined, including autos, major appliances, and electronics, and intentions to travel or spend on most services moved lower after a brief October rebound.

The Conference Board Consumer Confidence Index edged down -1.0 pt to 94.6 in October 2025 (from 95.6 in September), reflecting stronger views of current conditions offset by weaker expectations for the months ahead.

-

Present Situation Index rose +1.8 pts to 129.3, supported by improved assessments of business conditions and job availability.

-

Expectations Index declined -2.9 pts to 71.5, remaining below the recession-warning threshold of 80 for the ninth consecutive month.

-

Business conditions (current): 20.2% said conditions were “good” (Sep: 19.9%), while 14.7% said they were “bad” (Sep: 15.3%).

-

Labor market (current): 27.8% said jobs were “plentiful” (Sep: 26.9%) and 18.4% said jobs were “hard to get” (Sep: 18.2%).

-

Future business conditions: 19.0% expected improvement (Sep: 19.3%) and 22.6% expected worsening (unchanged).

-

Future jobs outlook: 15.8% expected more jobs (Sep: 16.6%), while 27.8% expected fewer (Sep: 25.7%).

-

Income expectations softened, with 17.9% anticipating higher incomes (Sep: 18.2%) and 12.5% expecting declines (Sep: 11.7%).

-

Inflation expectations edged up to 5.9% (Sep: 5.8%), while interest rate expectations also rose, with 52.8% expecting increases (Sep: 51.1%).

-

Holiday spending intentions fell, with consumers planning to spend -3.9% less on gifts and -12% less on non-gifts YoY.

-

Buying plans were mixed: used car and travel plans rose, homebuying plans weakened, and big-ticket goods intentions stabilized.

The Conference Board Consumer Confidence Index fell -3.6 pts to 94.2 in September 2025 (from 97.8 in August), marking the lowest level since April as weaker current conditions outweighed modestly firmer income expectations.

-

Present Situation Index dropped -7.0 pts to 125.4, the steepest monthly fall in a year, reflecting weaker views on business conditions and labor markets.

-

Expectations Index edged down -1.3 pts to 73.4, remaining below the recession-warning threshold of 80 for the eighth straight month.

-

Job availability perceptions weakened further: 26.9% said jobs were “plentiful” (down from 30.2%), while 19.1% said jobs were “hard to get” (unchanged).

-

Business conditions views worsened, with 19.5% saying they were “good” (vs 21.8%) and 15.4% calling them “bad” (vs 14.6%).

-

Inflation expectations eased to 5.8% (from 6.1%) but remained well above the 5.0% level at end-2024, with consumer write-ins citing inflation and tariffs as key concerns.

-

Stock market outlook improved modestly, with fewer consumers expecting declines (27.6% vs 30.2% in August).

-

Buying intentions for cars fell, homebuying plans rose to a 4-month high, and big-ticket goods demand was mixed—TVs and dryers stronger, refrigerators weaker.

-

Service spending plans deteriorated broadly, with travel and vacation intentions dropping to their lowest since April.

The Conference Board Consumer Confidence Index fell -1.3 pts to 97.4 in August (from 98.7 in July), with both the Present Situation Index (131.2) and Expectations Index (74.8) declining, the latter staying below the recession-warning threshold of 80.

-

Job availability perceptions weakened for an eighth month, with 29.7% saying jobs were “plentiful” (down from 29.9%) and 20.0% saying jobs were “hard to get” (up from 18.9%).

-

Inflation expectations rose to 6.2% (from 5.7%), marking the highest since April, as consumer write-ins increasingly cited tariffs and higher food and grocery prices.

-

Expectations for future business conditions improved slightly, with 19.5% expecting improvement (vs 19.0%) and 21.9% expecting worsening (vs 22.7%).

-

Income expectations softened, with 18.3% anticipating an increase (down from 18.7%) and 12.6% expecting a decrease (up from 11.8%).

-

Buying intentions for cars strengthened, homebuying plans held steady, but discretionary purchases (TVs, tablets, dining out, entertainment) fell; vacation plans declined for a second month.

The Conference Board Consumer Confidence Index rose 2.0 pts to 97.2 in July, recovering modestly from June's revised 95.2 but remaining below historical norms.

- The Expectations Index rose 4.5 pts to 74.4, improving for all components but remaining below the recession-warning threshold of 80 for a sixth month.

- The Present Situation Index fell -1.5 pts to 131.5, as more consumers reported jobs were “hard to get” (18.9%, up from 17.2%).

- Average 12-month inflation expectations edged down to 5.8% (from 5.9%), but concerns about tariffs and high prices remained elevated in write-in responses.

- Stock market sentiment improved, with 47.9% expecting higher stock prices over the next year; expectations for interest rate increases declined to 53% (from 57.1%).

- Buying plans for cars and homes fell in July, and intentions to purchase services weakened for a second straight month—especially for dining out, travel, and lodging.

The Conference Board Consumer Confidence Index fell -5.4 pts to 93.0 (vs 99.4 expected) in June, reversing nearly half of May’s rebound and driven by weaker views of both current conditions and future expectations.

- The Present Situation Index declined -6.4 pts to 129.1, as views on business conditions and job availability softened.

- The Expectations Index dropped -4.6 pts to 69.0, remaining well below the recession-warning threshold of 80.

- Average 12-month inflation expectations eased to 6.0%, down from 6.4% in May and 7.0% in April.

- 45.6% of consumers expect stock prices to rise in the next year, up from 37.6% in April; 57% expect interest rates to rise, the highest since Oct 2023.

- Plans to purchase cars held at the highest level since Dec 2024, while home buying plans declined and intentions to purchase services weakened.