China Real Estate Investment

China Real Estate Investment

- Source

- National Bureau of Statistics China

- Source Link

- https://www.stats.gov.cn/

- Frequency

- Monthly

- Next Release(s)

- March 15th, 2026 10:00 PM

-

April 15th, 2026 10:00 PM

-

May 17th, 2026 10:00 PM

-

June 15th, 2026 10:00 PM

-

July 14th, 2026 10:00 PM

-

August 16th, 2026 10:00 PM

-

September 14th, 2026 10:00 PM

-

October 18th, 2026 10:00 PM

-

November 15th, 2026 9:00 PM

-

December 14th, 2026 9:00 PM

Latest Updates

-

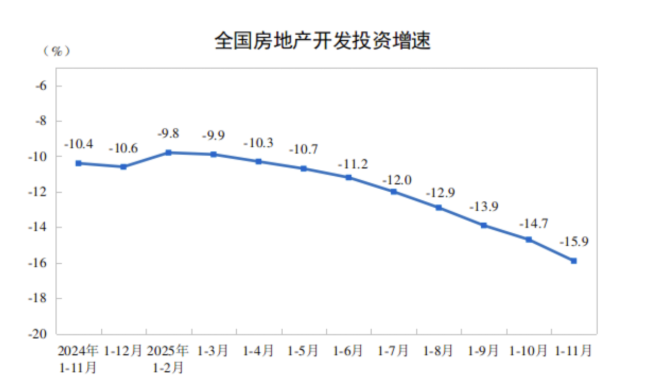

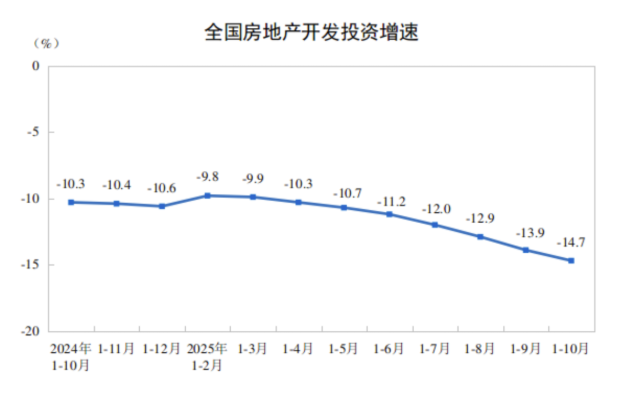

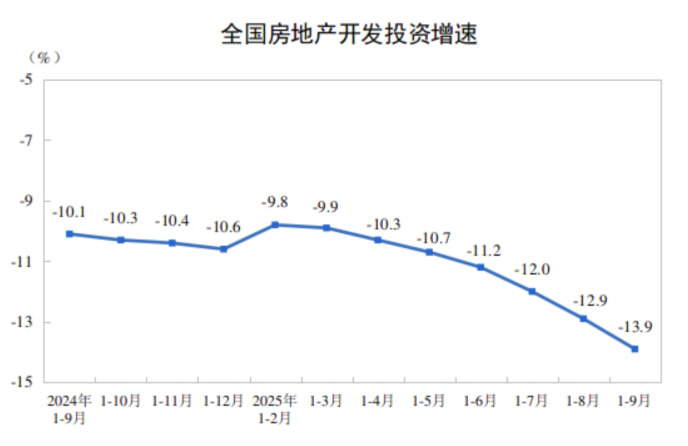

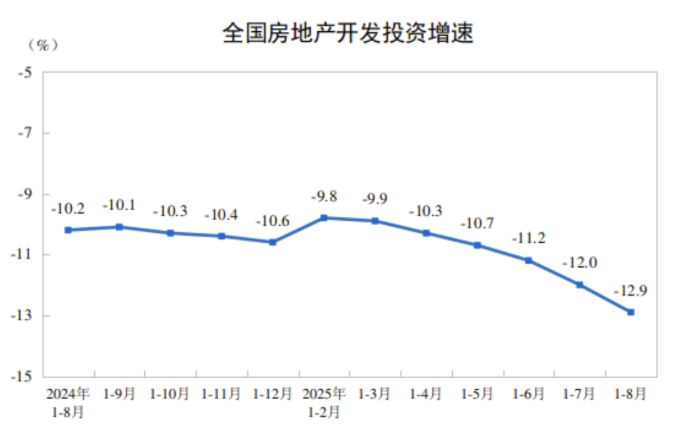

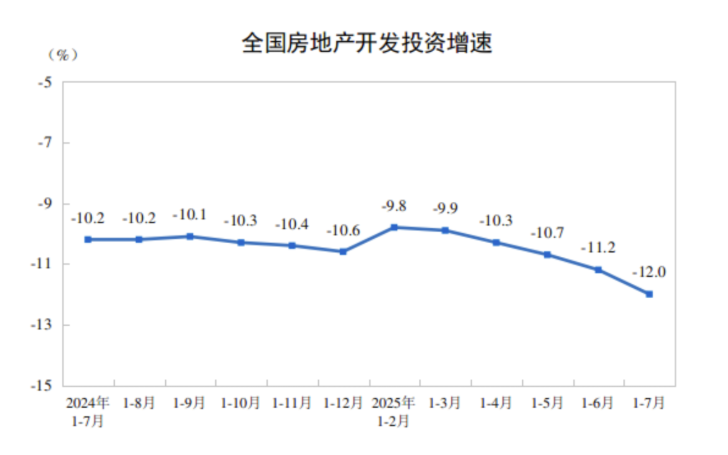

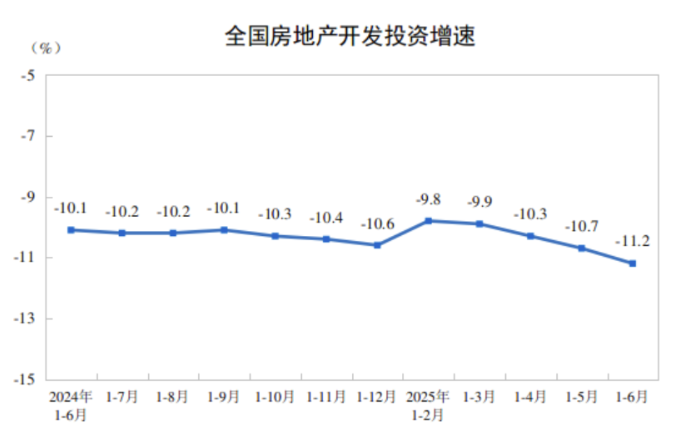

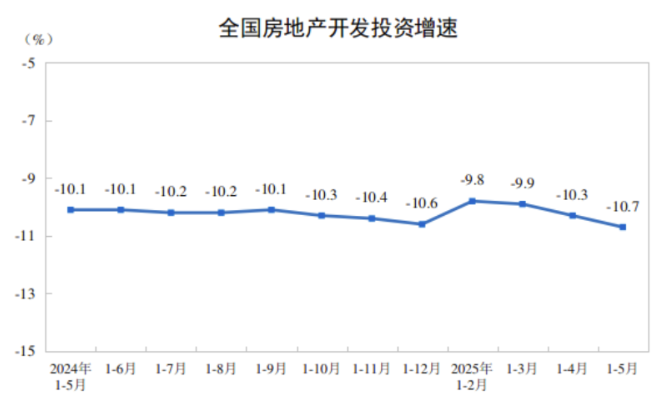

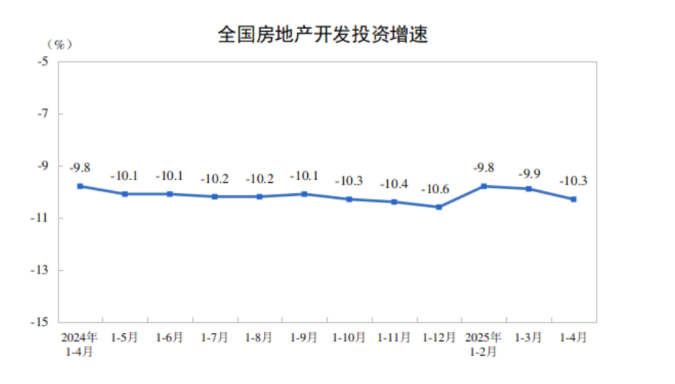

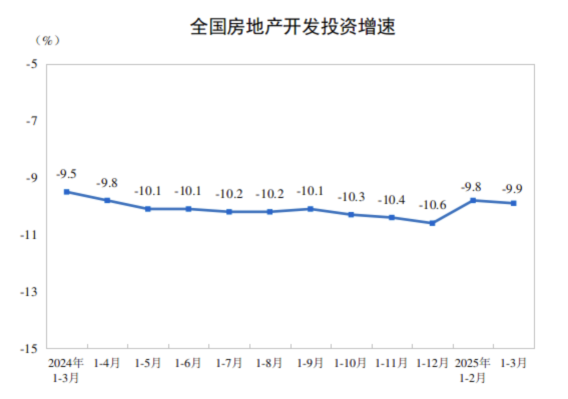

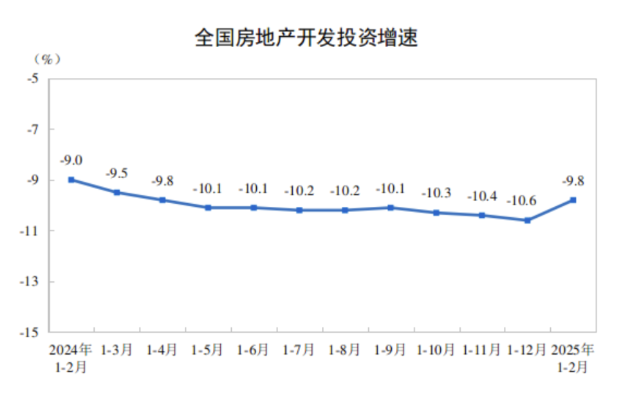

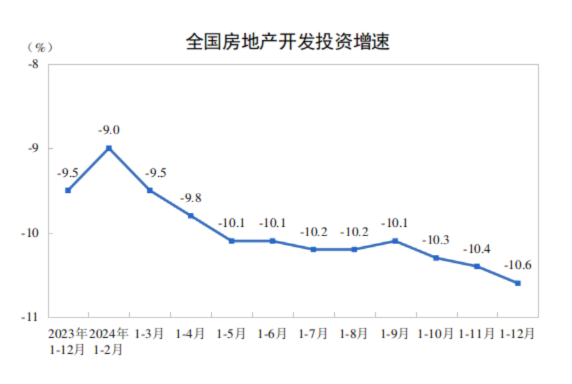

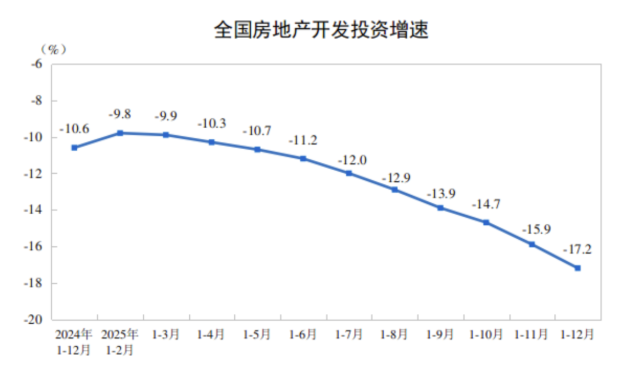

China’s real estate development investment fell -17.2% YoY in 2025, reflecting broad-based contraction across construction, sales, and developer financing.

-

Real estate development investment totaled CNY 8,278.8bn (-17.2% YoY), with residential investment at CNY 6,351.4bn (-16.3%), showing declines across the largest property segment.

-

Construction activity remained weak, with total construction area at 6,598.9m sq m (-10.0% YoY) and residential construction area at 4,601.23m sq m (-10.3%).

-

New project initiation continued to fall sharply, as new housing starts declined to 587.7m sq m (-20.4% YoY), including new residential starts of 429.84m sq m (-19.8%).

-

Housing delivery also declined, with completed floor area at 603.48m sq m (-18.1% YoY), while residential completions fell -20.2% to 428.3m sq m, indicating continued contraction in both starts and completions.

-

Housing demand and pricing conditions remained soft, with new commercial housing sales area down -8.7% YoY to 881.01m sq m and sales value falling -12.6% YoY to CNY 8,393.7bn; residential sales value dropped -13.0%.

-

Inventory edged higher versus the prior year, with commercial housing for sale rising +1.6% YoY to 766.32m sq m at end-2025, including residential inventory up +2.8%, suggesting slower clearing despite weak new construction.

-

Developer funding fell further, with funds in place at CNY 9,311.7bn (-13.4% YoY), led by declines in self-raised funds (-12.2%), deposits/advance receipts (-16.2%), and personal mortgage loans (-17.8%).

-

The National Housing Prosperity Index stood at 91.45 in December 2025, remaining well below neutral and consistent with ongoing sector weakness.

-