China NBS PMIs

China NBS PMIs

- Source

- National Bureau of Statistics China

- Source Link

- https://www.stats.gov.cn/

- Frequency

- Monthly

- Next Release(s)

- April 29th, 2026 9:30 PM

-

May 30th, 2026 9:30 PM

-

June 29th, 2026 9:30 PM

-

July 30th, 2026 9:30 PM

-

August 30th, 2026 9:30 PM

-

September 29th, 2026 9:30 PM

-

October 30th, 2026 9:30 PM

-

November 29th, 2026 8:30 PM

-

December 30th, 2026 8:30 PM

Latest Updates

-

China NBS PMIs: March 2026

-

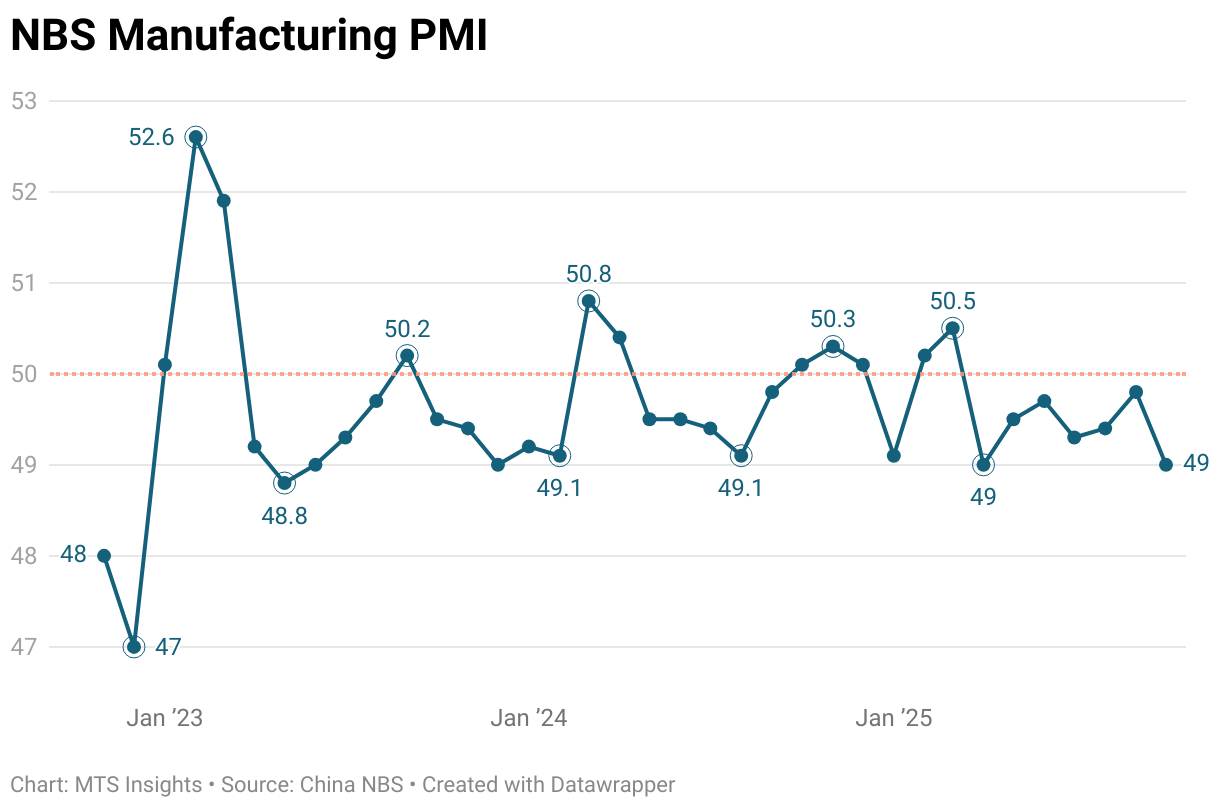

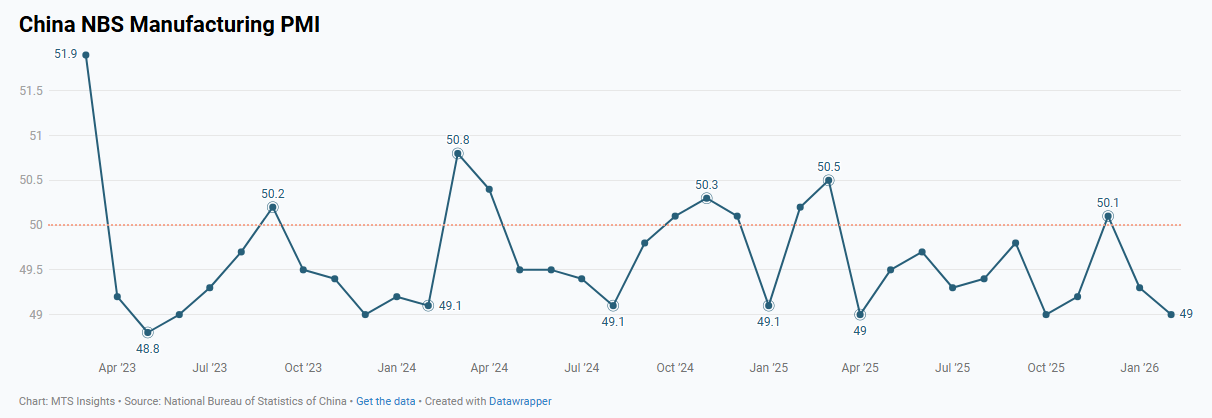

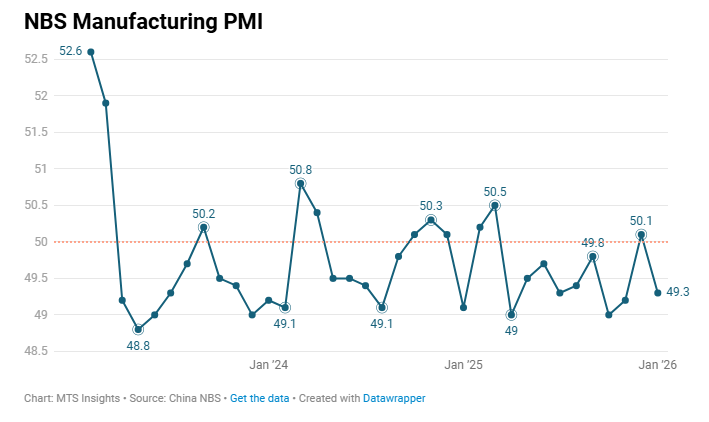

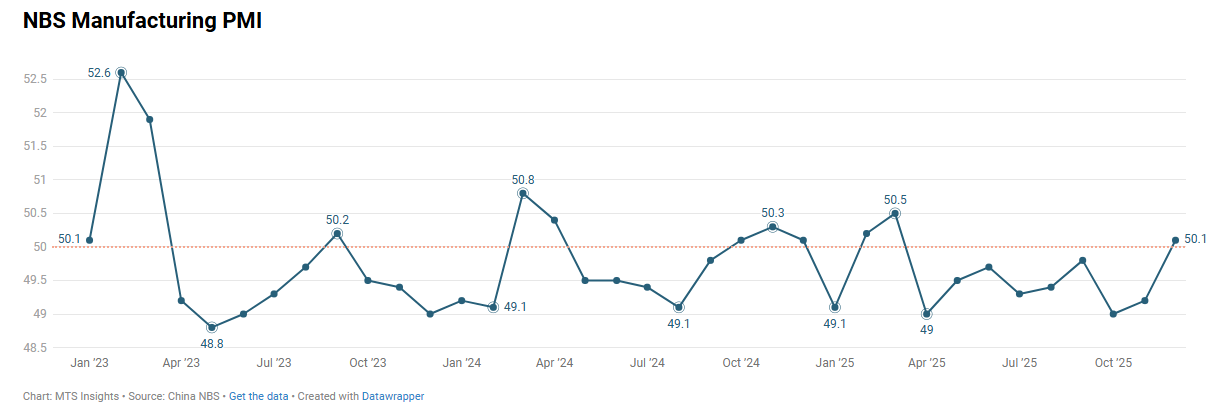

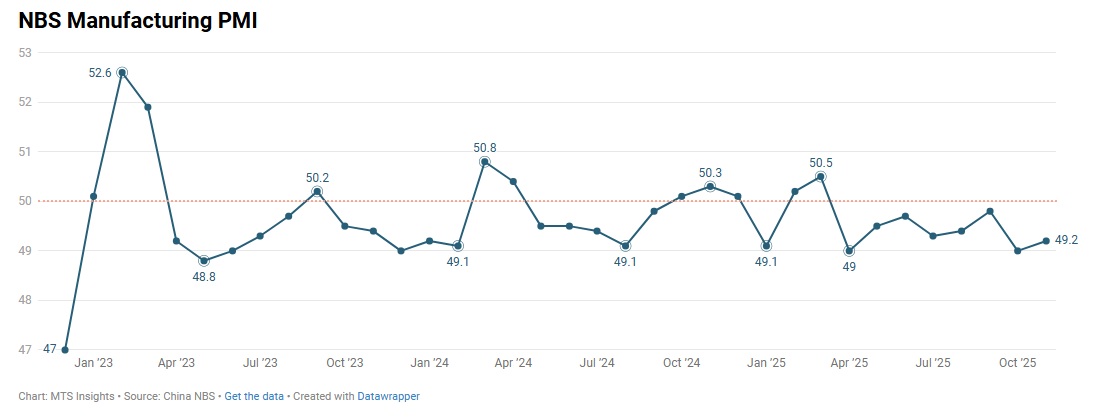

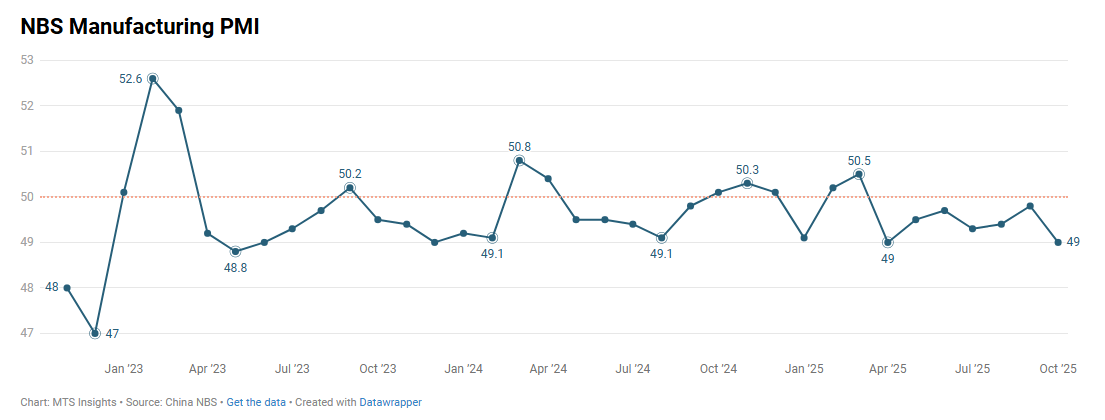

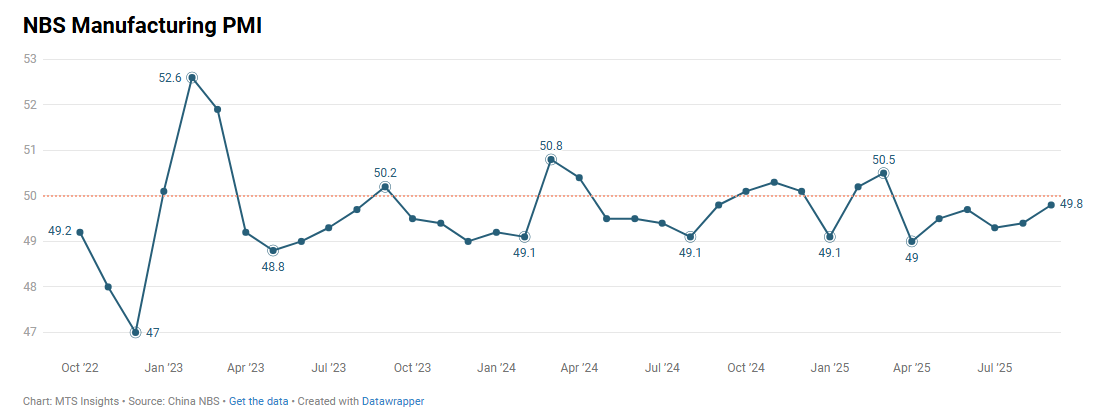

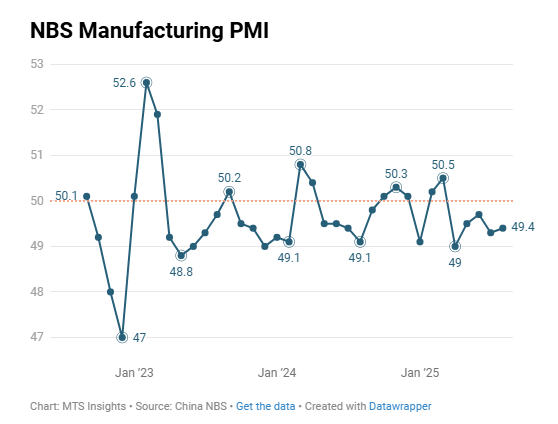

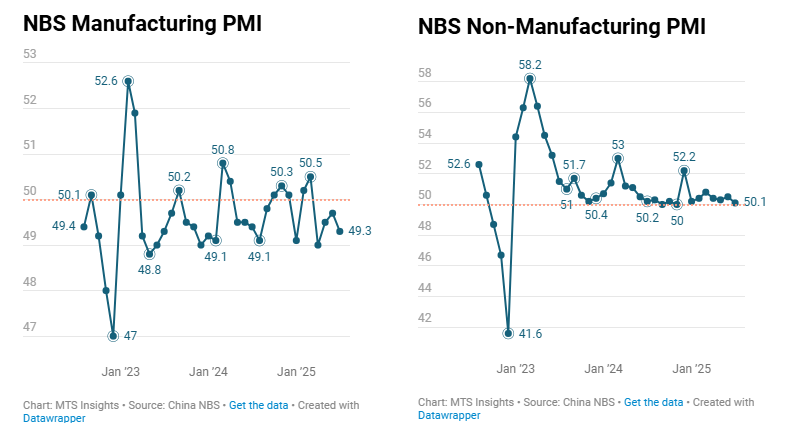

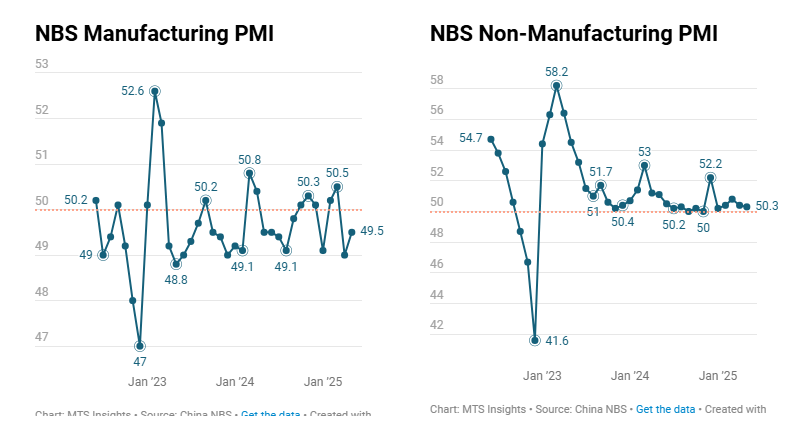

China’s NBS Manufacturing PMI declined to 49.0 in February 2026 (-0.3 pts MoM), remaining below the 50 threshold and signaling a further weakening in manufacturing conditions alongside softer production and demand indicators.

-

The Production Index fell to 49.6 (-1.0 pts MoM), dropping below the 50 expansion threshold and indicating a slowdown in manufacturing output during the month.

-

The New Orders Index declined to 48.6 (-0.6 pts MoM), pointing to weaker demand conditions in the manufacturing sector compared with January.

-

The Raw Material Inventory Index rose slightly to 47.5 (+0.1 pts MoM), though it remained below 50, indicating that inventory contraction persisted but narrowed marginally.

-

The Employment Index slipped to 48.0 (-0.1 pts MoM), suggesting a slight deterioration in labor market conditions among manufacturing firms.

-

The Supplier Delivery Time Index fell to 49.1 (-1.0 pts MoM), indicating that delivery times slowed compared with the previous month.

-

By enterprise size, the PMI for large firms rose to 51.5 (+1.2 pts MoM) and remained in expansion territory, while medium-sized firms declined to 47.5 (-1.2 pts MoM) and small firms dropped to 44.8 (-2.6 pts MoM), highlighting a divergence in conditions between large manufacturers and smaller enterprises.

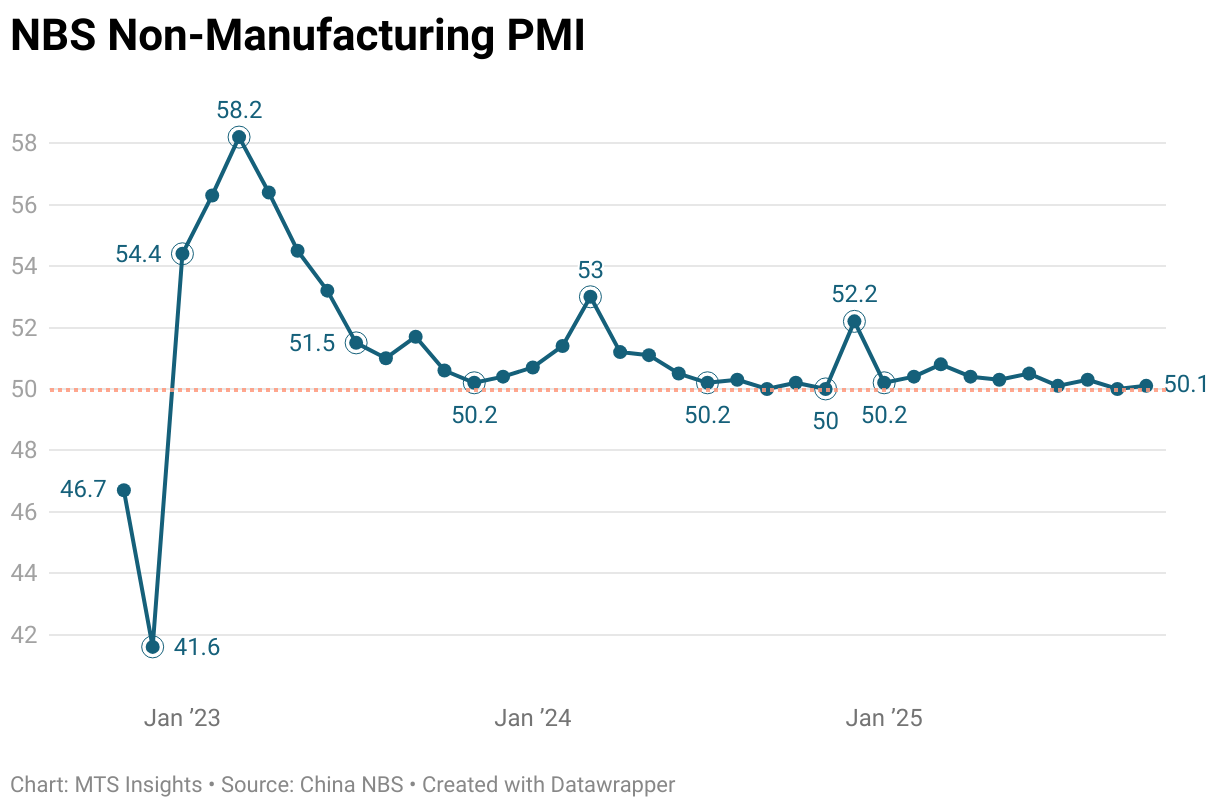

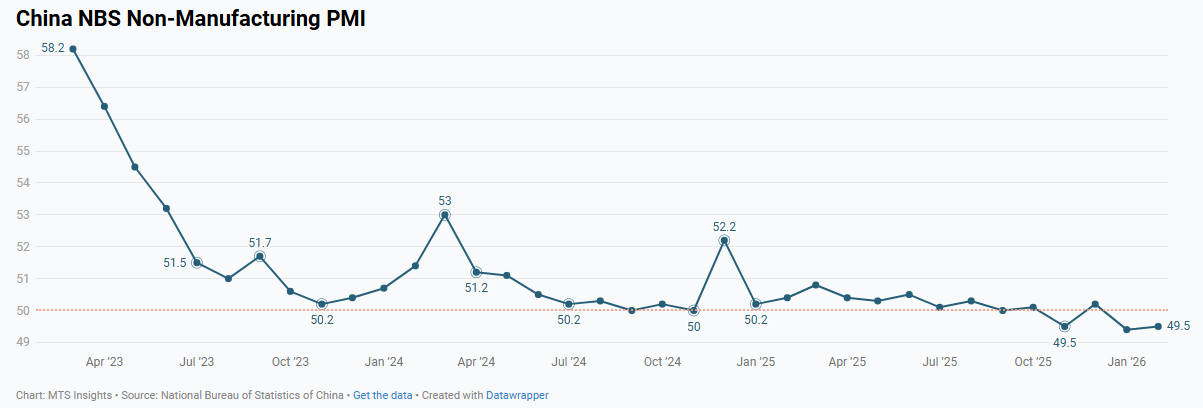

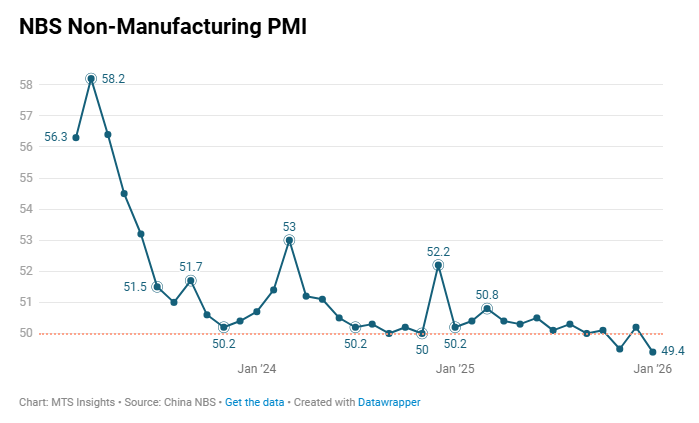

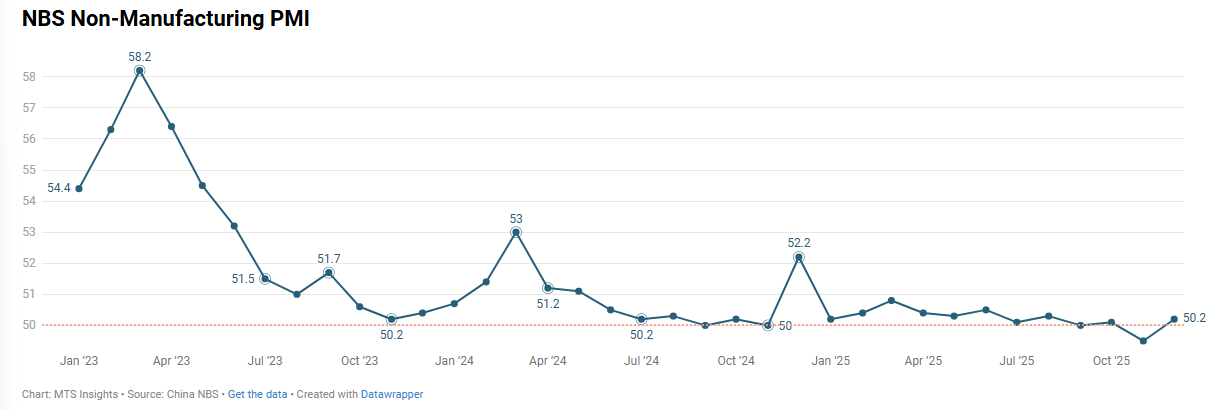

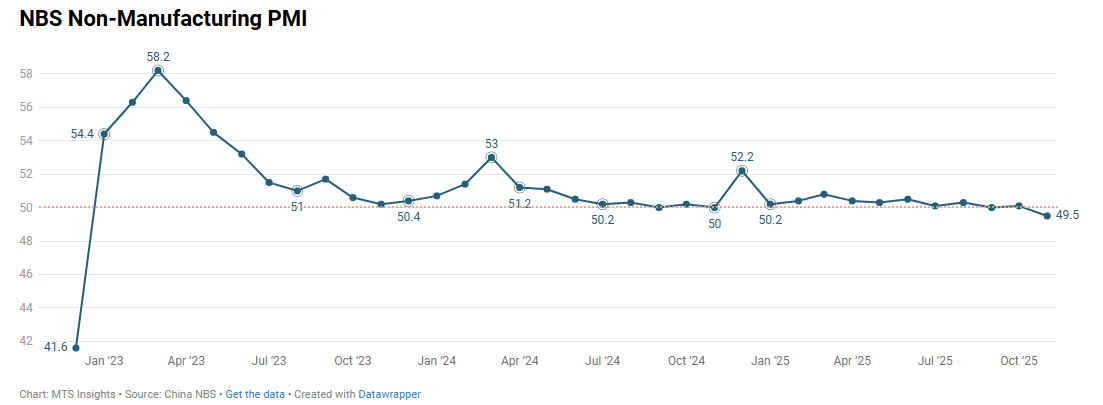

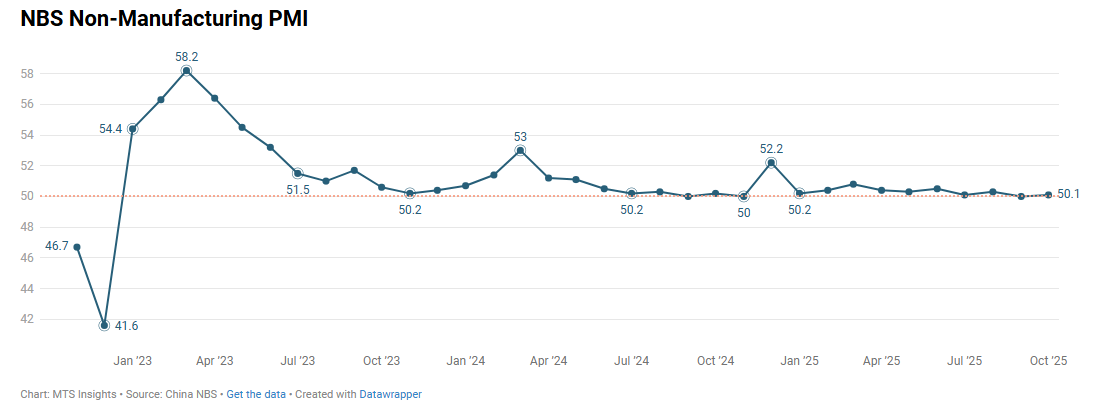

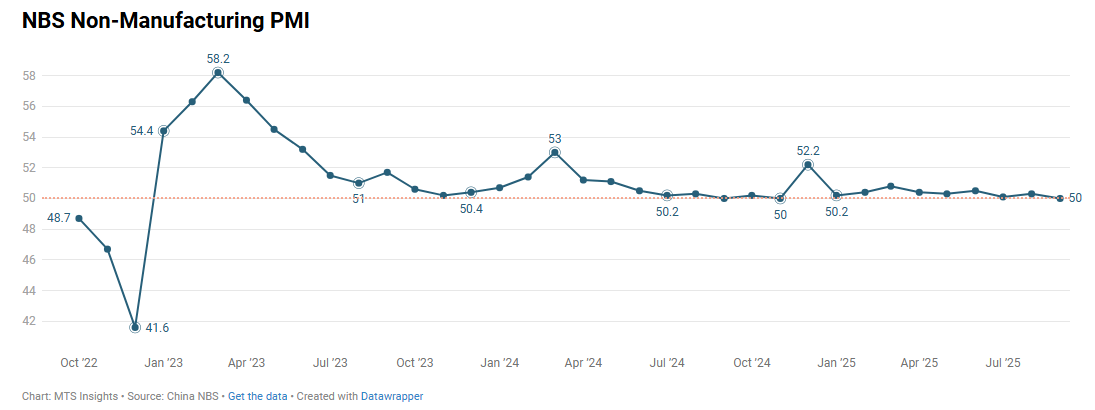

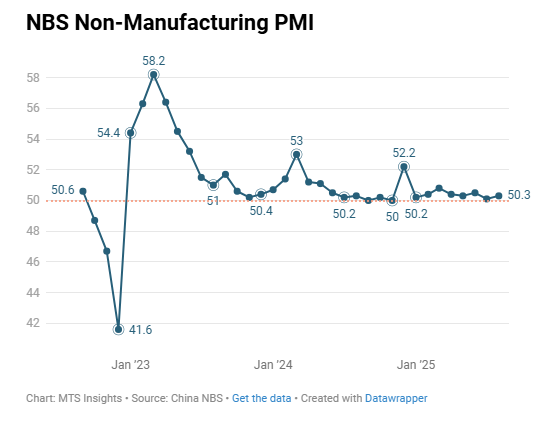

China’s NBS Non-manufacturing PMI edged up to 49.5 in February 2026 (+0.1 pts MoM), remaining below the 50 expansion threshold as demand conditions weakened while services activity improved slightly and construction activity softened.

-

The Business Activity Index increased marginally to 49.5 (+0.1 pts MoM), indicating a slight improvement in overall non-manufacturing activity but still reflecting contractionary conditions below the neutral 50 level.

-

By sector, the Construction Activity Index declined to 48.2 (-0.6 pts MoM) while the Services Activity Index rose to 49.7 (+0.2 pts MoM), highlighting continued divergence as services showed modest improvement while construction conditions weakened.

-

Within services, industries such as accommodation, catering, culture, sports, and entertainment reported activity readings above 60.0, signaling strong expansion, while capital market services and real estate remained below the expansion threshold.

-

The New Orders Index fell to 45.2 (-0.9 pts MoM), indicating weaker demand across the non-manufacturing sector; construction orders rose to 42.2 (+2.1 pts MoM) but remained deeply contractionary, while services new orders declined to 45.7 (-1.4 pts MoM).

-

The Input Price Index increased to 50.9 (+0.9 pts MoM), suggesting rising input costs overall; construction input prices declined to 49.1 (-2.9 pts MoM) while services input prices rose to 51.2 (+1.5 pts MoM).

-

The Sales Price Index held steady at 48.8 (flat MoM), remaining below the critical threshold and indicating continued declines in selling prices overall, with construction prices falling to 47.6 (-0.6 pts MoM) while services prices edged up to 49.0 (+0.1 pts MoM).

-

The Employment Index slipped to 46.0 (-0.1 pts MoM), indicating a slight deterioration in labor conditions; construction employment improved to 42.5 (+1.4 pts MoM) but remained weak, while services employment declined to 46.6 (-0.4 pts MoM).

-

The Business Activity Expectations Index declined to 55.0 (-1.0 pts MoM) but remained firmly in expansion territory, indicating that firms continued to maintain relatively strong expectations for future activity despite softer current conditions.

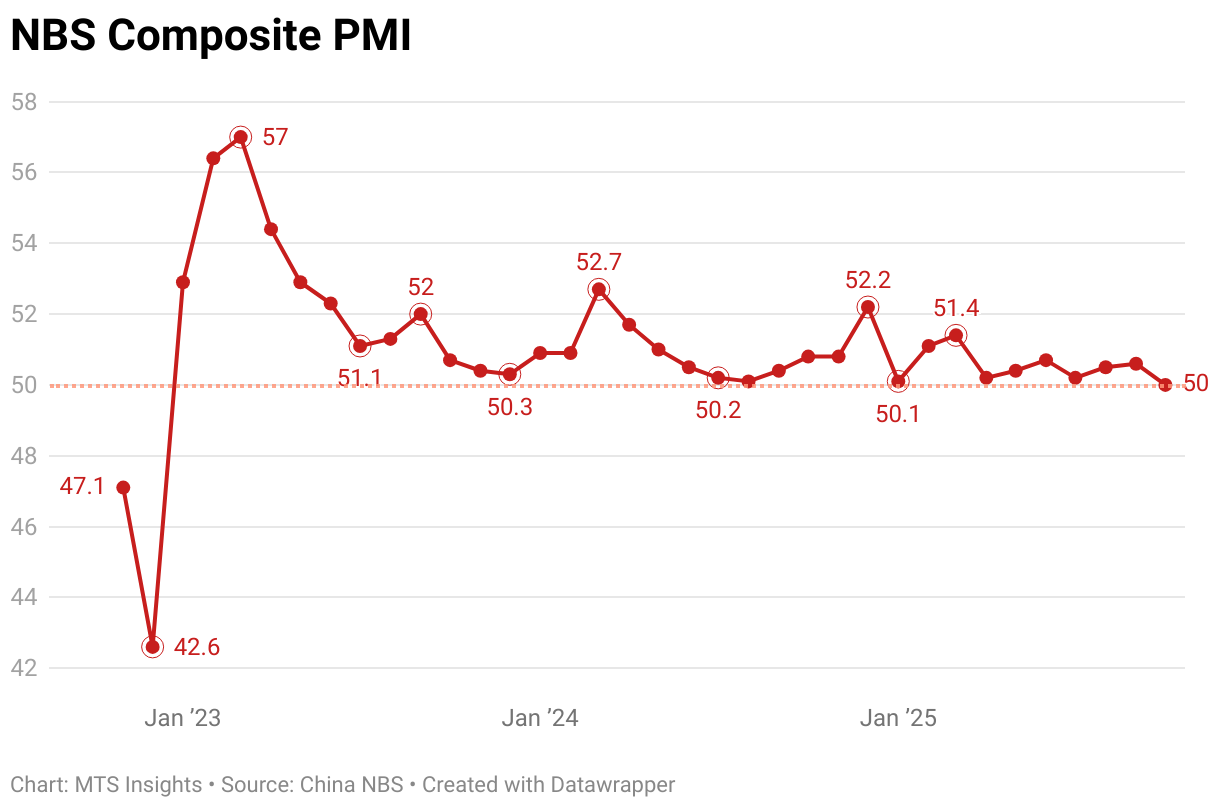

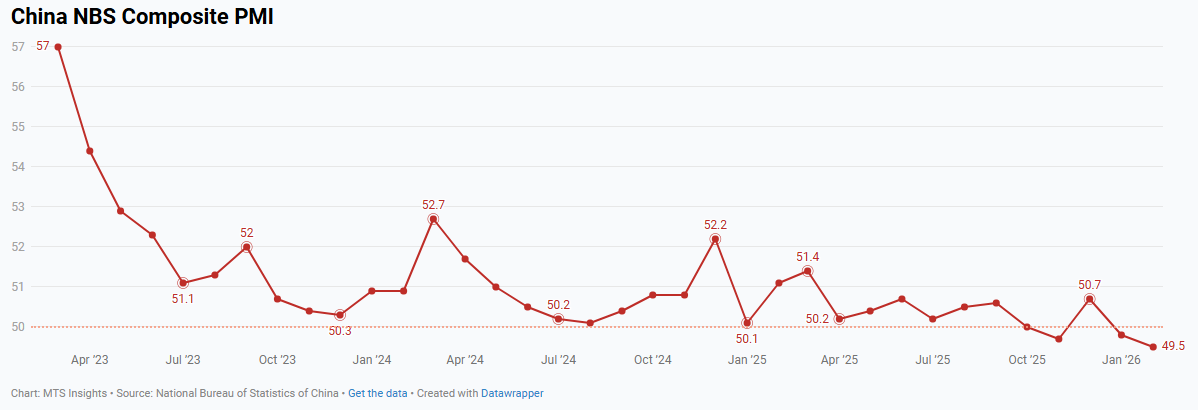

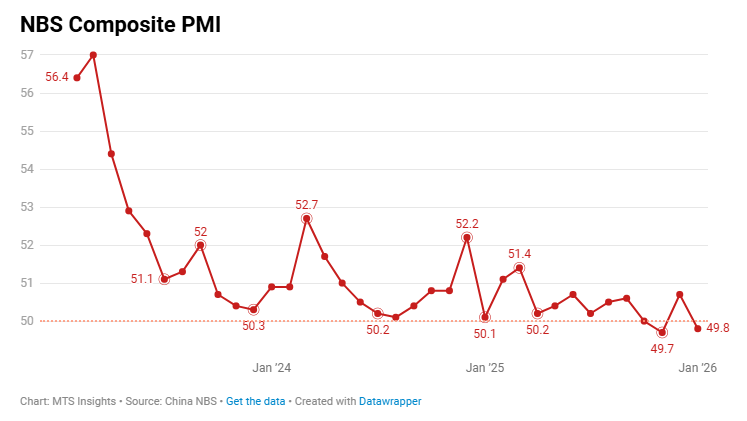

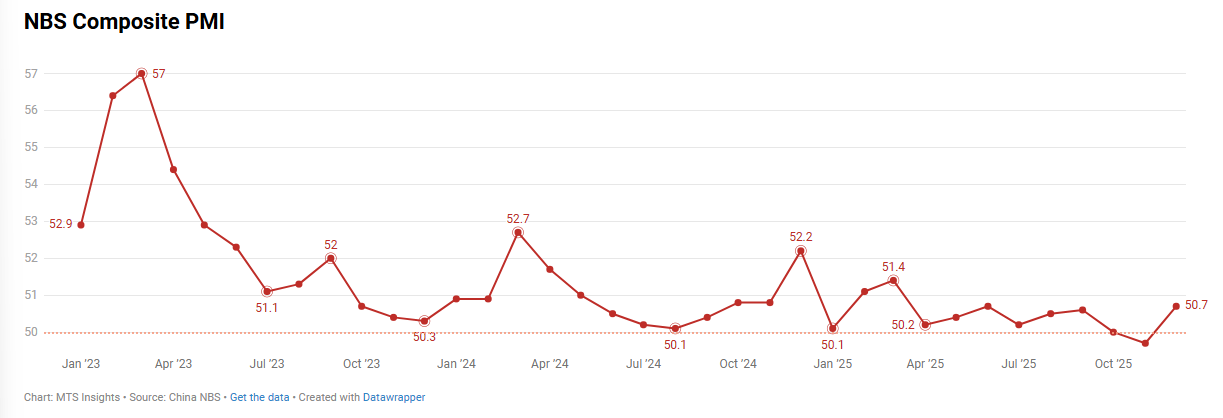

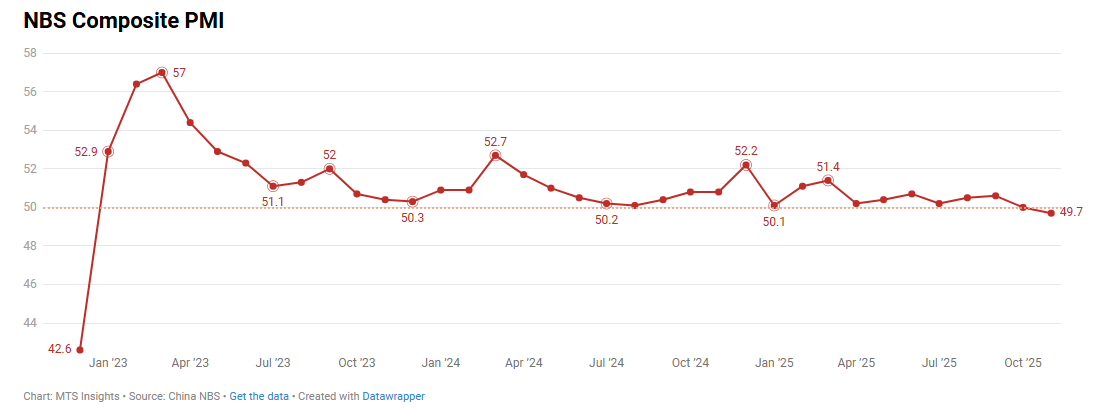

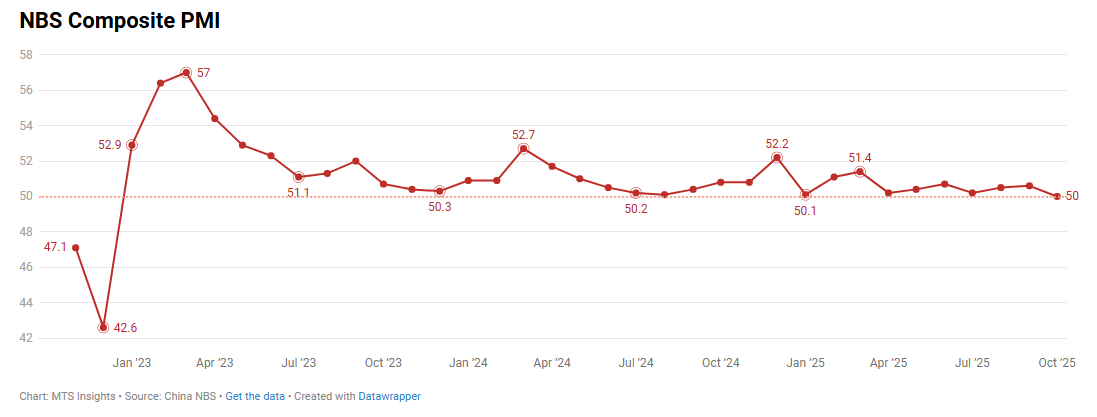

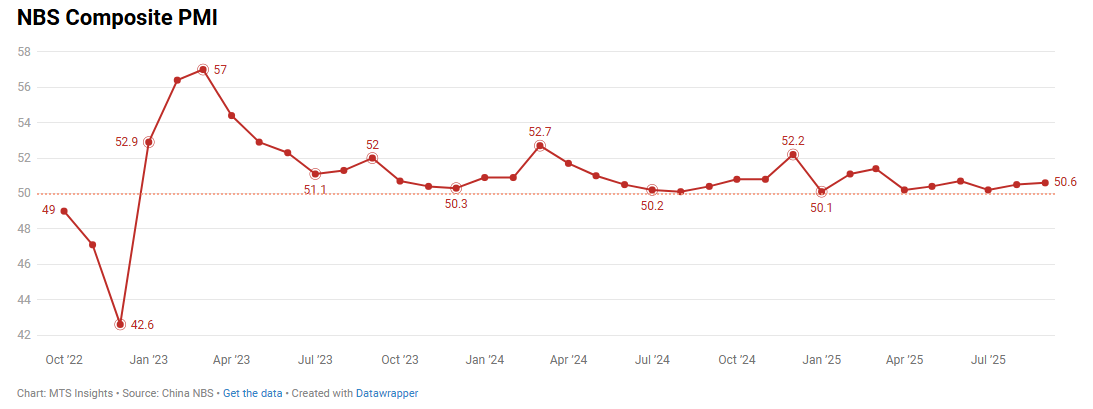

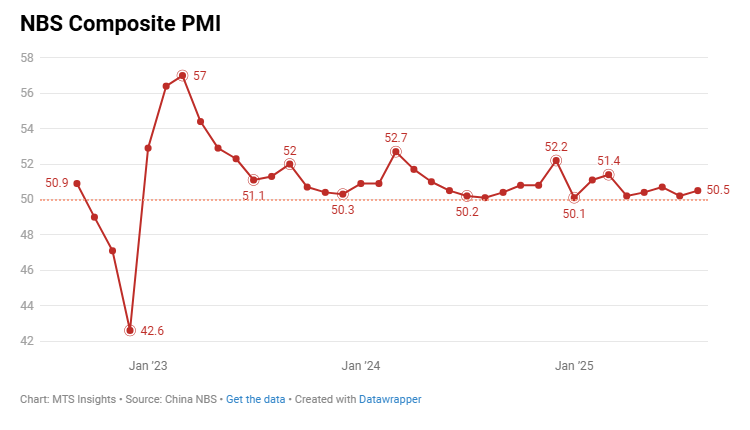

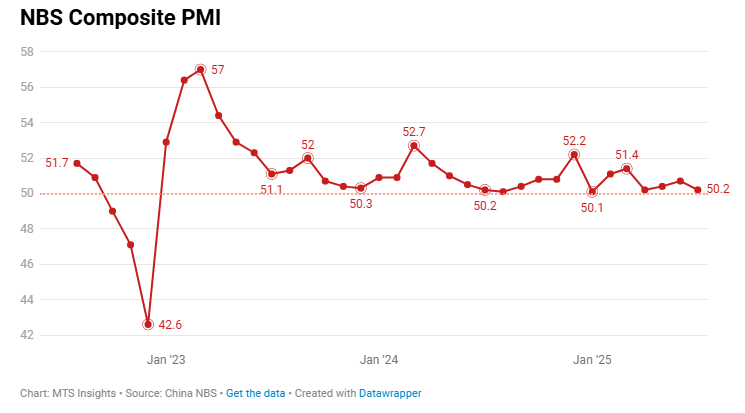

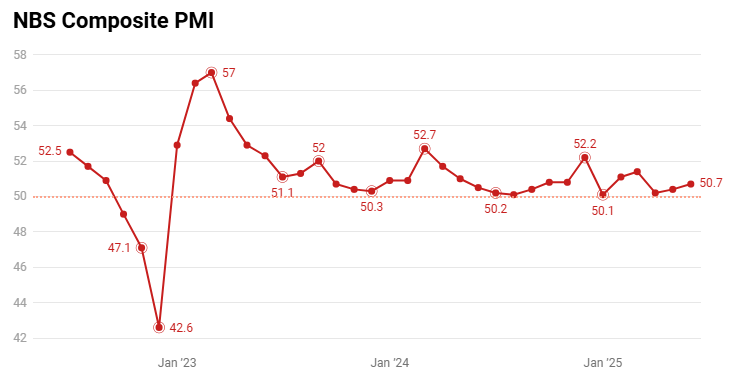

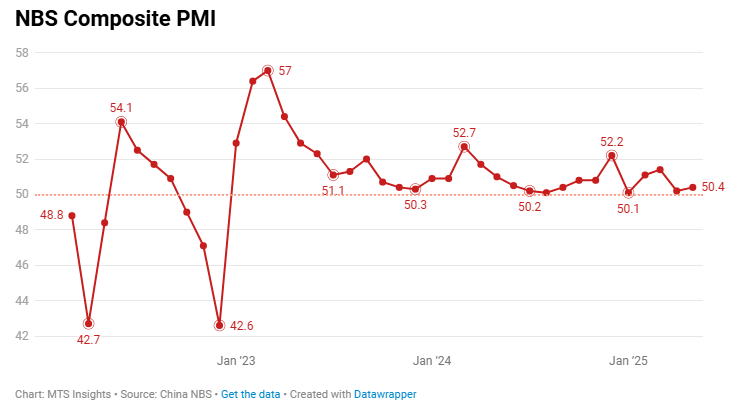

With both manufacturing and non-manufacturing PMIs declining, the NBS Composite PMI also fell, down -0.3 pts to 49.5, the lowest reading since December 2022.

-

-

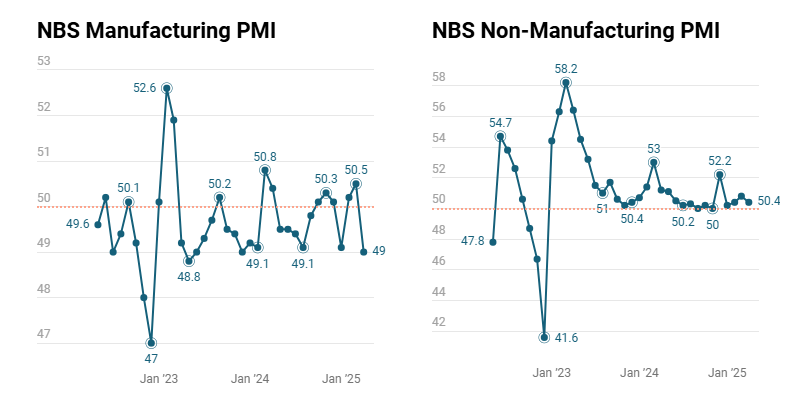

China’s NBS Manufacturing PMI fell to 49.3 in January 2026 (-0.8 pts MoM), slipping back into contraction alongside weaker demand conditions.

-

The Production Index eased to 50.6 (-1.1 pts MoM) but remained above 50, showing output continued to expand despite slowing momentum.

-

The New Orders Index fell to 49.2 (-1.6 pts MoM), signaling softer manufacturing demand conditions entering the new year.

-

The Raw Material Inventory Index declined to 47.4 (-0.4 pts MoM), pointing to continued inventory drawdowns among manufacturers.

-

The Employment Index slipped to 48.1 (-0.1 pts MoM), indicating a slight further weakening in manufacturing labor conditions.

-

The Supplier Delivery Time Index edged down to 50.1 (-0.1 pts MoM) but stayed above 50, suggesting deliveries continued to accelerate marginally.

-

By firm size, large enterprises remained in expansion at 50.3 (-0.5 pts MoM), while medium firms fell to 48.7 (-1.1 pts MoM) and small firms to 47.4 (-1.2 pts MoM), reflecting broader contraction outside large producers.

China’s NBS Non-manufacturing PMI slipped to 49.4 in January 2026 (-0.8 pts MoM), reflecting softer service and construction activity.

-

Construction activity declined sharply to 48.8 (-4.0 pts MoM), while services eased to 49.5 (-0.2 pts MoM), showing broader weakness across non-manufacturing segments.

-

The New Orders Index dropped to 46.1 (-1.2 pts MoM), indicating weaker demand conditions, led by construction orders at 40.1 (-7.3 pts MoM) and softer services orders at 47.1 (-0.2 pts MoM).

-

The Input Price Index edged down to 50.0 (-0.2 pts MoM), holding at the neutral level as construction input costs rose to 52.0 (+1.2 pts) while services inputs eased to 49.7 (-0.4 pts).

-

The Sales Price Index increased to 48.8 (+0.8 pts MoM), signaling a narrowing decline in selling prices across both construction (48.2) and services (48.9).

-

The Employment Index held steady at 46.1 (flat MoM), with construction employment at 41.1 (+0.1 pts) and services employment unchanged at 47.0.

-

The Business Activity Expectations Index eased to 56.0 (-0.5 pts MoM) but remained elevated, with construction expectations falling to 49.8 (-7.6 pts) and services expectations rising to 57.1 (+0.7 pts).

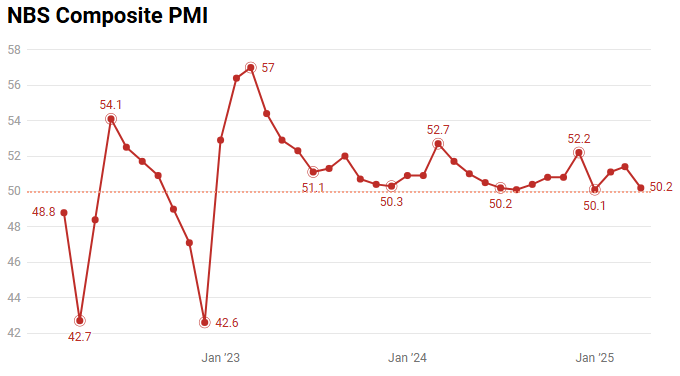

The NBS Composite PMI reversed the November gain, dropping -0.9 pts to 49.8 in December, the second lowest reading since December 2022.

-

-

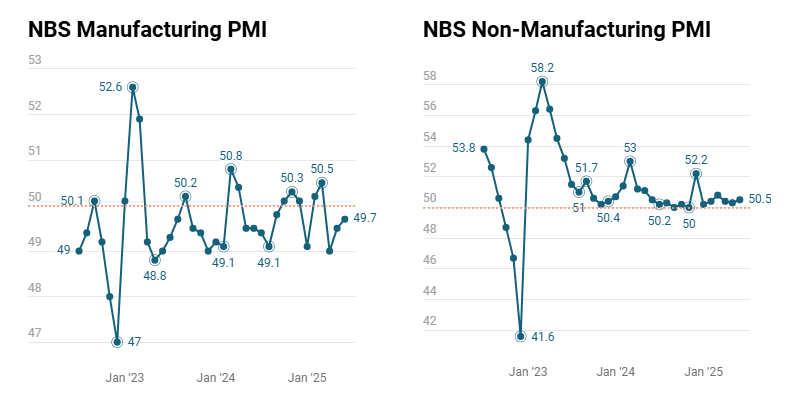

China’s NBS Manufacturing PMI rose to 50.1 in December 2025 (from 49.2 in November), moving back into expansion territory after several months below the threshold.

-

The headline PMI increased +0.9 pts MoM to 50.1, marking a return to expansion and the highest reading since March 2025.

-

The Production Index rose to 51.7 (+1.7 pts MoM), indicating faster manufacturing output growth.

-

The New Orders Index climbed to 50.8 (+1.6 pts MoM), signaling an improvement in domestic demand conditions.

-

Supplier Delivery Times edged up to 50.2 (+0.1 pts MoM), remaining above the 50 level and indicating continued acceleration in deliveries.

-

The Raw Material Inventory Index increased to 47.8 (+0.5 pts MoM) but stayed below 50, showing that inventory drawdowns continued, though at a slower pace.

-

The Employment Index slipped to 48.2 (-0.2 pts MoM), indicating a slight deterioration in manufacturing labor conditions.

-

By firm size, large enterprises expanded with a PMI of 50.8 (+1.5 pts), medium-sized firms improved to 49.8 (+0.9 pts) but remained in contraction, while small enterprises fell further to 48.6 (-0.5 pts).

-

Other indicators showed mixed conditions, with New Export Orders rising to 49.0 (from 47.6) and Purchase Prices increasing to 48.9 (from 48.2), both still below the expansion threshold.

China’s NBS Non-Manufacturing PMI rose to 50.2 in December (from 49.5 in November), returning overall activity to expansion territory.

-

The headline non-manufacturing business activity index increased +0.7 pts MoM to 50.2, marking a rebound into expansion after dipping below 50 in November.

-

Construction activity strengthened sharply, with the construction business activity index rising to 52.8 (+3.2 pts MoM), while the services activity index edged up to 49.7 (+0.2 pts) but remained in contraction.

-

The New Orders Index improved to 47.3 (+1.6 pts MoM), indicating a rebound in demand that nonetheless stayed below the expansion threshold for both services (47.3, +1.7 pts) and construction (47.4, +1.3 pts).

-

Input prices eased slightly to 50.2 (-0.2 pts MoM) but remained above 50, showing continued cost increases, driven by construction inputs at 50.8 (+1.1 pts).

-

The Sales Price Index fell to 48.0 (-1.1 pts MoM), signaling a renewed decline in selling prices across both construction (47.4) and services (48.1).

-

Employment improved modestly, with the Employee Index rising to 46.1 (+0.8 pts), reflecting gains in services employment (47.0, +1.1 pts) that offset weaker construction employment (41.0, -0.8 pts).

-

Business activity expectations strengthened further, with the Expectations Index increasing to 56.5 (+0.3 pts MoM), indicating rising confidence for the period ahead in both services and construction.

The NBS Composite PMI ended up a full point higher in December at 50.7, up from 49.7 in November. This suggests China's economy is expanding at the joint fastest pace since March (June 2025 was also at 50.7).

-

-

China’s Manufacturing PMI edged up to 49.2 in November 2025 (from 49.0 in October), marking a modest improvement but remaining below the 50 threshold, reflecting continued mild contraction with slightly better production and demand conditions.

-

The Production Index rose to 50.0 (from 49.7), reaching the critical point and indicating broadly stable manufacturing output.

-

New Orders increased to 49.2 (from 48.8), showing a small pickup in demand even as the index remained below the expansion threshold.

-

Raw Material Inventories held at 47.3, unchanged from October, signaling ongoing drawdowns of key inputs.

-

The Employment Index increased slightly to 48.4 (from 48.3), suggesting a marginal improvement in labor conditions but still indicating contraction.

-

Supplier Delivery Times rose to 50.1 (from 50.0), a slight acceleration that points to marginally faster logistics performance.

-

By firm size, the PMI for large enterprises fell to 49.3 (-0.6 pts), while medium and small firms improved to 49.1 (+2.0 pts) and 48.9 (+0.2 pts), respectively, with all categories remaining below 50.

-

Related indicators showed New Export Orders at 47.6 (from 45.9) and Imports at 47.0 (from 46.8), indicating mildly improved but still weak trade activity.

-

Input price momentum was steady, with the Purchase Price Index at 48.2 (from 47.5), while the Factory Price Index eased to 47.3 (from 48.1), suggesting subdued cost pressures and weak pricing power.

China’s Non-Manufacturing Business Activity Index fell to 49.5 in November (from 50.1 in October), reflecting a mild weakening in overall activity driven by softer service-sector momentum.

-

The services activity index declined to 49.5 (-0.7 pts), while construction activity rose to 49.6 (+0.5 pts), showing mixed sector performance.

-

New orders eased to 45.7 (-0.3 pts), remaining well below 50 and indicating continued weak demand across both services (45.6, -0.4 pts) and construction (46.1, +0.2 pts).

-

Input prices increased to 50.4 (+1.0 pt), with costs rising in both construction (49.7, +0.1 pt) and services (50.5, +1.1 pts), pointing to firmer input cost pressures.

-

The sales price index improved to 49.1 (+1.3 pts) but stayed below the critical level, suggesting that price declines persist but have narrowed.

-

Employment edged up to 45.3 (+0.1 pt), showing only a slight improvement; construction employment rose to 41.8 (+1.9 pts), while services dipped to 45.9 (-0.2 pts).

-

Business activity expectations remained strong at 56.2 (+0.1 pt), with confidence higher in construction (57.9, +1.9 pts) and slightly weaker in services (55.9, -0.2 pts).

-

Among auxiliary indicators, new export orders softened to 47.9 (-0.3 pts), orders in hand stayed flat at 43.6, and supplier delivery times held steady at 51.2, indicating stable logistics conditions.

The Composite Index fell -0.3 pts to 49.7, the first time this index fell below 50 into contraction territory since December 2022.

-

-

China’s Manufacturing PMI fell to 49.0 in October 2025 (from 49.8 in September), marking a return to contraction and reflecting weaker production and demand conditions across most enterprise sizes.

-

By enterprise size, the PMI for large firms was 49.9 (-1.1 pts MoM), medium firms 48.7 (-0.1), and small firms 47.1 (-1.1), all remaining below the 50 threshold, indicating broad-based weakness.

-

Production slowed notably, with the Production Index at 49.7 (-2.2 pts), signaling reduced manufacturing activity.

-

New orders fell further to 48.8 (-0.9 pts), showing declining demand and ongoing weakness in the manufacturing market.

-

Raw material inventories dropped to 47.3 (-1.2 pts), marking continued inventory drawdowns amid slower purchasing activity.

-

Employment edged down to 48.3 (-0.2 pts), suggesting a slight deterioration in labor market conditions within manufacturing.

-

Supplier delivery times stood at 50.0 (-0.8 pts), indicating broadly stable logistics conditions compared with the prior month.

-

Among related indicators, new export orders declined sharply to 45.9 (-1.9 pts), while imports eased to 46.8 (-1.3 pts), underscoring soft trade activity.

-

Input prices eased to 52.5 (-0.7 pts) and factory-gate prices to 47.5 (-0.7 pts), reflecting weaker pricing momentum and subdued cost pressures.

-

Business expectations moderated to 52.8 (-1.3 pts), suggesting confidence remains positive but has softened compared with September.

China’s Non-Manufacturing PMI edged up +0.1 pts to 50.1 in October 2025, signaling broadly stable activity across services and construction with mild improvement in employment and optimism.

-

By sector, the services activity index rose slightly to 50.2 (+0.1 pts), while construction dipped to 49.1 (-0.2 pts), showing modest divergence between the two industries.

-

New orders held at 46.0 (unchanged), remaining below 50 and indicating continued weak demand; construction new orders improved to 45.9 (+3.7 pts), while services slipped to 46.0 (-0.7 pts).

-

Input prices rose to 49.4 (+0.4 pts), narrowing the overall pace of cost declines; construction input prices climbed to 49.6 (+2.4 pts), while services were nearly steady at 49.4 (+0.1 pts).

-

Sales prices increased to 47.8 (+0.5 pts) but remained below the neutral level, suggesting continued price softness; construction rose to 48.4 (+0.3 pts) and services to 47.7 (+0.5 pts).

-

Employment improved modestly to 45.2 (+0.2 pts), led by a small uptick in construction (39.9, +0.2 pts) and services (46.1, +0.2 pts).

-

Business activity expectations strengthened to 56.1 (+0.4 pts), reflecting sustained optimism about future conditions; construction expectations rose sharply to 56.0 (+3.6 pts), while services eased slightly to 56.1 (-0.2 pts).

-

Among secondary indicators, new export orders fell sharply to 46.2 (-3.6 pts), backlogs declined to 43.6 (-0.8 pts), and supplier delivery times eased slightly to 50.9 (-0.2 pts), signaling a mild softening in external demand and operational momentum.

China’s Composite PMI Output Index fell -0.6 pts to 50.0 in October 2025, the weakest since December 2022 as the economy moved from marginal growth to stagnation.

-

-

China’s NBS Manufacturing PMI rose 0.4 pts to 49.8 in September 2025, remaining below the 50 threshold but signaling a modest improvement in overall manufacturing conditions.

-

The Production index climbed to 51.9 (+1.1 pts), marking faster expansion in output.

-

New Orders rose slightly to 49.7 (+0.2 pts), showing gradual improvement in demand though still in contraction territory.

-

The Raw Material Inventory index increased to 48.5 (+0.5 pts), indicating the pace of inventory drawdowns slowed.

-

The Employment index improved to 48.5 (+0.6 pts), suggesting modest gains in labor market stability.

-

The Supplier Delivery Time index rose to 50.8 (+0.3 pts), pointing to quicker delivery times from suppliers.

-

By enterprise size, large firms stayed in expansion (51.0), while medium (48.8) and small enterprises (48.2) remained in contraction, though small firms saw the strongest monthly improvement.

China’s NBS Non-Manufacturing PMI edged down -0.3 pts to 50.0 in September 2025, sitting at the threshold and indicating broadly stable activity across services and construction.

-

The Service Business Activity Index fell -0.4 pts to 50.1, while Construction activity rose +0.2 pts to 49.3, showing mixed momentum across sectors.

-

The New Orders index slipped -0.6 pts to 46.0, pointing to weaker demand; service new orders fell to 46.7, while construction new orders improved to 42.2.

-

The Input Price index dropped -1.3 pts to 49.0, reflecting softer cost pressures; construction input prices fell sharply to 47.2, while services eased to 49.3.

-

The Sales Price index declined -1.3 pts to 47.3, with both construction (48.1) and services (47.2) below the 50 threshold, indicating ongoing price contraction.

-

The Employment index slipped -0.6 pts to 45.0, signaling weaker labor market conditions, led by construction (39.7) while services held steady at 45.9.

-

Business Activity Expectations eased -0.5 pts to 55.7, still firmly expansionary; construction expectations rose to 52.4, while services dipped to 56.3.

China’s Composite PMI Output Index rose +0.1 pts to 50.6 in September 2025, remaining above the 50 threshold and signaling continued modest expansion in overall business activity.

-

-

China’s NBS Manufacturing PMI edged up 0.1 pts to 49.4 in August 2025, remaining below the 50 threshold but signaling a slight improvement in manufacturing activity.

-

The Production index rose 0.3 pts to 50.8, showing a modest pickup in output expansion.

-

The New Orders index improved 0.1 pts to 49.5, suggesting a slight recovery in demand, though still in contraction territory.

-

The Raw Materials Inventory index increased 0.3 pts to 48.0, with the pace of inventory decline narrowing.

-

The Employment index slipped 0.1 pts to 47.9, indicating a further mild weakening in labor conditions.

-

The Supplier Delivery Time index rose 0.2 pts to 50.5, pointing to continued acceleration in delivery times.

China’s NBS Non-Manufacturing PMI rose 0.2 pts to 50.3 in August 2025, remaining above the 50 threshold and indicating continued expansion.

-

The Service industry activity index increased 0.5 pts to 50.5, while the Construction industry index fell -1.5 pts to 49.1 (lowest since records start in 2021), showing divergent momentum between the two sectors.

-

The New Orders index improved 0.9 pts to 46.6, reflecting a modest pickup in demand; service new orders rose to 47.7, but construction new orders dropped to 40.6.

-

The Input Price index stayed at 50.3, with construction costs higher (54.6) while service input prices eased slightly to 49.5.

-

The Sales Price index rose 0.7 pts to 48.6, narrowing the pace of declines across both construction (49.7) and services (48.5).

-

The Employment index held at 45.6, signaling ongoing labor market weakness, while business expectations strengthened to 56.2, pointing to greater optimism about future activity.

The Composite PMI edged up 0.3 pts to 50.5 in August, indicating that China continues to grow at a gradual pace.

-

-

China’s Composite PMI Output Index fell -0.5 pts to 50.2 in July 2025, indicating continued but slower expansion in overall business activity across manufacturing and services.

- The Manufacturing PMI declined -0.4 pts to 49.3, with weakness in new orders (49.4) and inventories (47.7); production remained above 50 at 50.5.

- Large manufacturers stayed in expansion (50.3), while small firms weakened further to 46.4.

- The Non-Manufacturing Business Activity Index slipped -0.4 pts to 50.1; construction fell sharply to 50.6, while services were flat at 50.0.

- Non-manufacturing new orders dropped to 45.7, and sales prices fell to 47.9, indicating soft demand and pricing pressure.

- Business activity expectations in both sectors remained optimistic, with the non-manufacturing outlook index rising to 55.8.

-

The NBS Manufacturing PMI rose 0.2 pts to 49.7, remaining in contraction but showing improvement; production (51.0) and new orders (50.2) moved above 50, while employment declined slightly to 47.9.

- Large manufacturers expanded (PMI at 51.2), while small firms contracted sharply (47.3); medium firms remained just below neutral (48.6).

- The Non-Manufacturing Business Activity Index edged up 0.2 pts to 50.5, with construction improving to 52.8 and services steady at 50.1; employment remained weak at 45.5.

- New export orders and input prices improved in both sectors; manufacturing export orders rose to 47.7 and non-manufacturing export orders to 49.8.

- Business activity expectations remained optimistic at 55.6, though slightly lower than May (55.9).

China’s Composite PMI Output Index rose 0.3 pts to 50.7 in June 2025, signaling a modest acceleration in overall economic activity, with both manufacturing and non-manufacturing sectors contributing to the expansion.

-

China’s NBS Manufacturing PMI rose 0.5 pts to 49.5 in May, marking a modest improvement but still signaling contraction.

- The Production Index rose 0.9 pts to 50.7, returning to expansion, while New Orders increased 0.6 pts to 49.8, nearing the neutral threshold.

- Export Orders recovered 2.8 pts to 47.5 after plunging in April, and Imports rebounded to 47.1.

- Input prices and factory prices remained weak, at 46.9 and 44.7, respectively, continuing to pressure margins.

- Employment edged up to 48.1 (vs 47.9 prior), still in contraction, and Inventory of Raw Materials remained subdued at 47.4.

- All enterprise sizes below 50 except large firms (50.7), which led the stabilization; medium-sized firms dropped to 47.5.

China’s Non-Manufacturing PMI dipped -0.1 pts to 50.3 in May, suggesting continued but slower expansion in services and construction.

- Construction activity slowed (-0.9 pts to 51.0), while services held steady (0.1 pts to 50.2); sectors like transport, telecoms, and software remained strong.

- New Orders rose 1.2 pts to 46.1, signaling a modest demand rebound, especially in construction (3.7 pts to 43.3).

- Input Prices (48.2) and Sales Prices (47.3) remained in contraction but improved MoM.

- Employment was unchanged at 45.5, with a divergence between construction (1.7 pts to 39.5) and services (-0.2 pts to 46.6).

- Business expectations remained optimistic at 55.9, despite a slight dip.

China’s Composite PMI Output Index rose 0.2 pts to 50.4 in May, indicating modest expansion across the economy.

-

China’s NBS Manufacturing PMI fell -1.5 pts to 49.0 (vs 49.8 expected) in April, signaling a contraction in factory activity that was the worst since December 2023.

- The Production Index dropped -2.8 pts to 49.8, and New Orders fell -2.6 pts to 49.2, both slipping back into contraction.

- Notably, the Export Orders Index dropped -4.3 pts to 44.7, the weakest since December 2022, as a result of US tariffs slowing US-China trade.

- The Imports Index also fell, down -4.1 pts to 43.4, also the weakest since December 2022.

- Employment weakened, with the Employment Index down -0.3 pts to 47.9, while Inventories of Raw Materials remained weak at 47.0.

- The Supplier Delivery Time Index held just above the 50 mark at 50.2, indicating slightly faster deliveries.

- All enterprise sizes (large, medium, small) reported PMIs below 50, with large firms at 49.2 and small firms at 48.7.

China’s Non-Manufacturing PMI declined -0.4 pts to 50.4 (vs 50.7 expected) in April, still above the expansion threshold, but momentum weakened across sectors.

- Construction Business Activity fell -1.5 pts to 51.9; Services edged down -0.2 pts to 50.1.

- New Orders Index fell sharply to 44.9 (-1.7 pts), with construction orders plunging to 39.6.

- The New Export Orders Index crashed -7.6 pts to 42.2, signaling a sharp contraction and the lowest reading since April 2020.

- Input Prices (47.8) and Sales Prices (46.6) declined, reflecting softening pricing power.

- Employment Index dropped to 45.5, as construction hiring fell sharply (-3.6 pts to 37.8).

The Composite PMI Output Index fell -1.2 pts to 50.2 in April, suggesting continued but marginal growth in business activity across sectors.