CBI Service Sector Survey

CBI Service Sector Survey

Data

Services

- Source

- CBI Economics

- Source Link

- https://www.cbi.org.uk/

- Frequency

- Monthly

- Next Release(s)

- April 29th, 2026 4:30 AM

Latest Updates

-

The survey based on the responses of 351 services firms found that:

Business & Professional Services

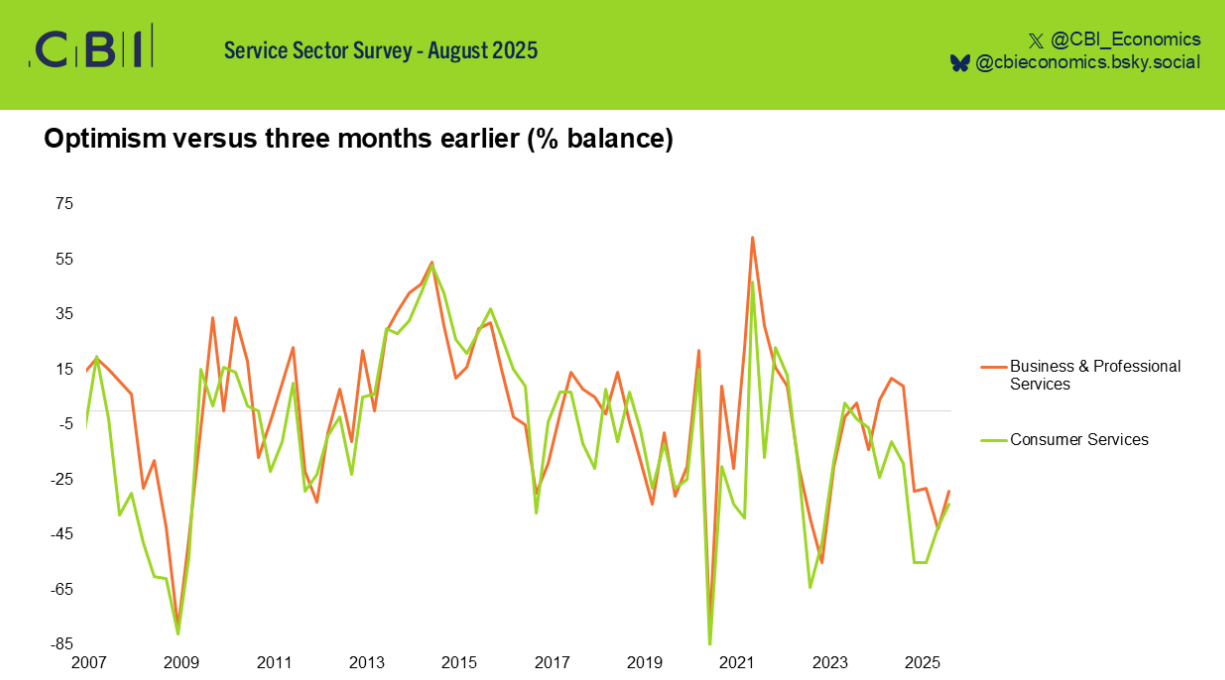

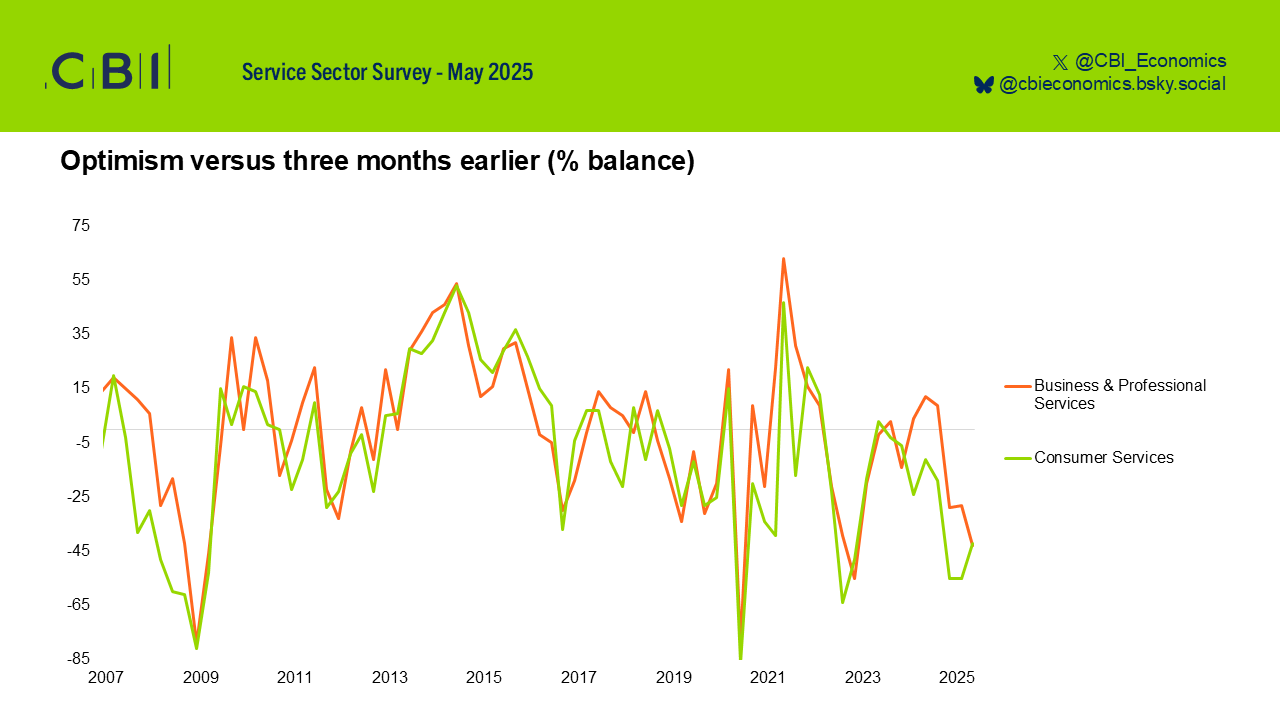

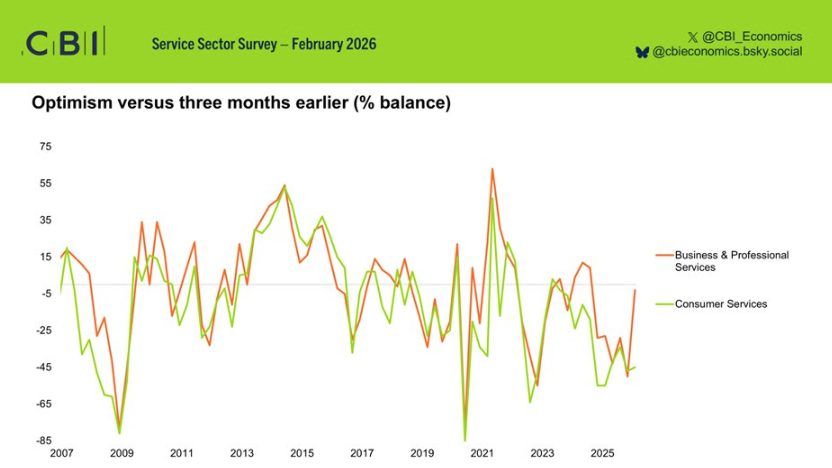

- Optimism about the general business situation was broadly unchanged in the three months to February, marking the end of five consecutive quarters of deteriorating confidence (-3% from -50% in November).

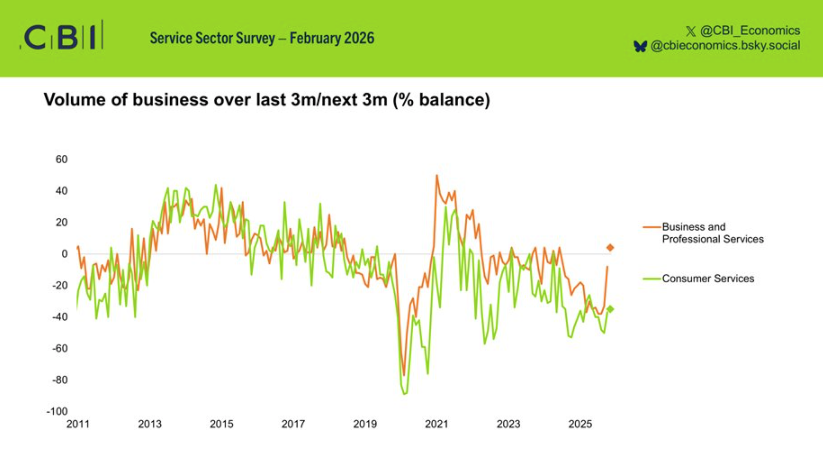

- Volume of business continued to decline in the quarter to February, but at a slower pace than in the quarter to January (-8% from -33% in January) and at the slowest pace since November 2024. Volumes are expected to grow slightly in the quarter ahead (+4%), the most positive expectations since October 2024.

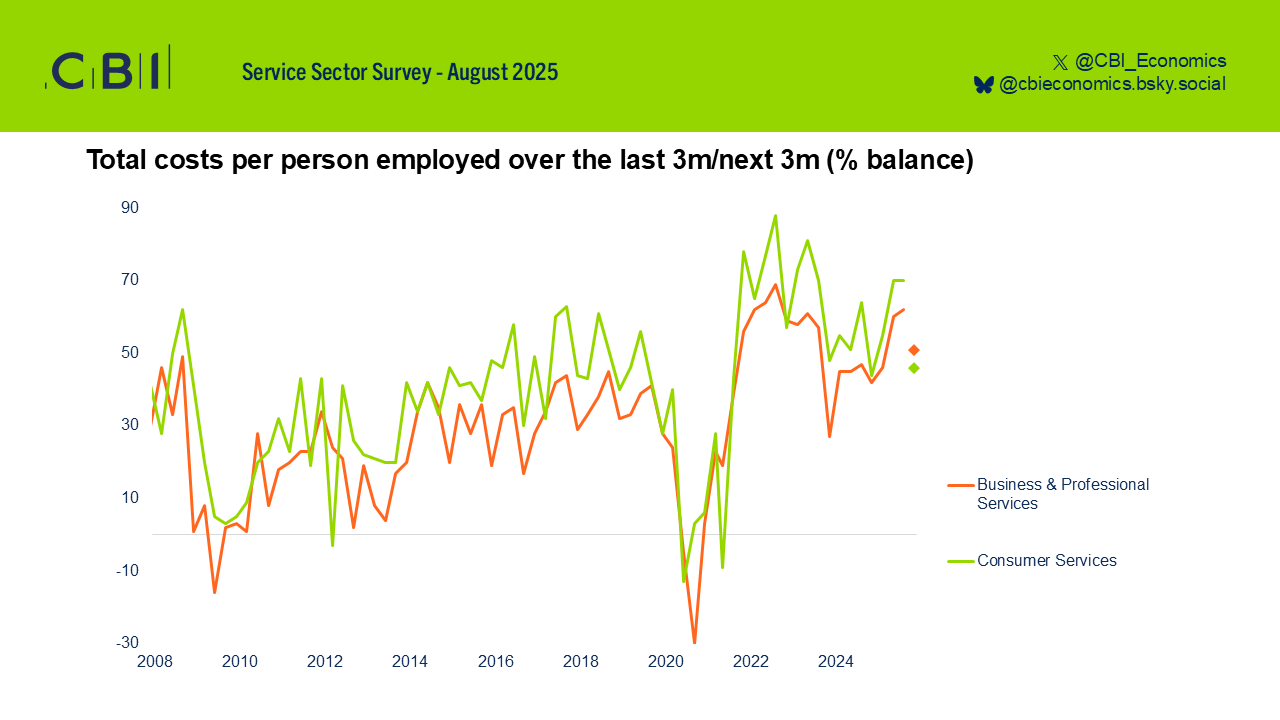

- Growth in costs per person employed remained elevated in the three months to February. Although growth has slowed compared to the three months to November (+43% from +58% in November), it remained above the long-run average (+31%). In the quarter ahead, cost growth is expected to accelerate and remain elevated (+54%).

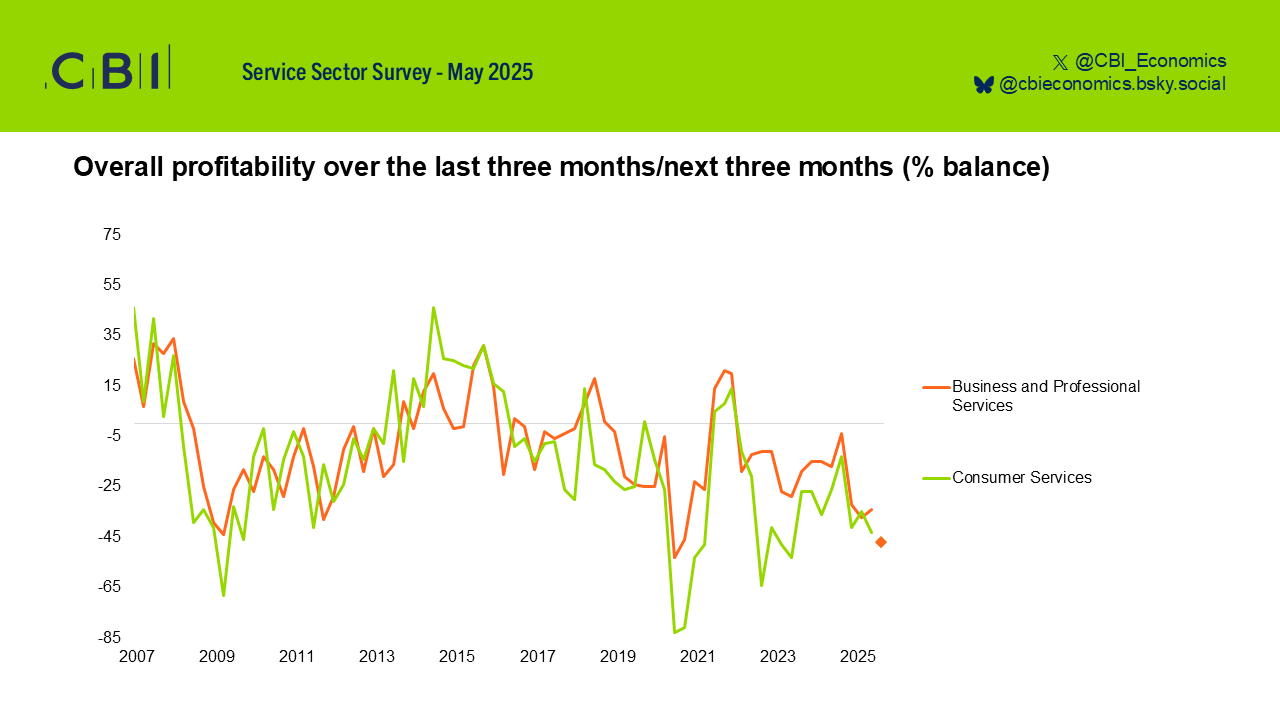

- Profitability declined (-28%) for the seventeenth consecutive quarter, albeit at the slowest pace since Q3 2024 (-4%). Overall, profitability is expected to continue falling in the quarter ahead but at a slightly slower pace (-24%).

- Average selling prices grew gradually in the three months to February (+6% from 0% in November), and growth is expected to accelerate in the next quarter (+19%).

- Employment continued contracting in the three months to February, albeit at a slower pace than in the three months to January (-15% from -26% in January) and at the slowest pace since May 2025 (-2%). Headcount is expected to fall at a broadly unchanged pace in the quarter to come (-14%).

- Uncertainty about demand was the most cited factor limiting capital expenditure (cited by 55% of respondents). This was followed by inadequate net returns (33%), a shortage of internal finance (23%), and the cost of finance (21%).

- Firms anticipate cutbacks in investment into both land & buildings (-9% from -24% in November) and vehicles, plant & machinery (-17% from -23% in November). Meanwhile, IT investment is expected to pick up (+17% from -5% in November), the most positive expectations in a year.

Consumer Services

- General optimism continued to deteriorate sharply for the eleventh consecutive quarter, and at a broadly unchanged pace compared to the quarter to November (-45% from -47% in November).

- Business volumes declined further in the three months to February, albeit at a slower pace than in the three months to January (-37% from -50% in January). This extends a period of flat or falling volumes that began in March 2022. In the next three months, volumes are expected to continue declining at a broadly unchanged pace (-35%).

- Total costs per person employed continued rising in the quarter to February, but at a slower pace than in the quarter to November (+46% from +66% in November). Cost growth remains above the long-run average (+40%), and expectations are for cost pressures to rise again in the next three months (+60%).

- Overall profitability fell again sharply in the quarter to February (-49% from -49% in November), at the joint fastest pace since May 2023. Profitability is expected to continue declining in the quarter ahead, and at an unchanged pace (-49%).

- Average selling price growth picked up in the three months to February, after being broadly flat in the three months to November (+9% from +1% in November). This is the nineteenth consecutive quarter of flat or growing selling prices. In the three months to come, selling prices are expected to grow further and at a faster pace (+28%).

- Headcount continued to fall for the twenty-first consecutive month, albeit at a slower pace than in January (-32% from -39% in January). In the three months to May, employment is expected to continue declining sharply (-36%).

- Uncertainty about demand remained the most cited factor limiting investment (cited by 58% of respondents). This was followed by inadequate net returns (43%) and a shortage of internal finance (28%).

- Firms are expecting to cut back capital expenditure in all investment categories: land & buildings (-16% from -32% in November), vehicles, plant & machinery (-31% from -29% in November), and IT (-7% from -1% in November).