CBI Growth Indicator

CBI Growth Indicator

- Source

- CBI Economics

- Source Link

- https://www.cbi.org.uk/

- Frequency

-

Monthly

1st business day of the month

- Next Release(s)

- April 29th, 2026 4:30 AM

Latest Updates

-

Outlook for private sector activity remains subdued - CBI Growth Indicator

-

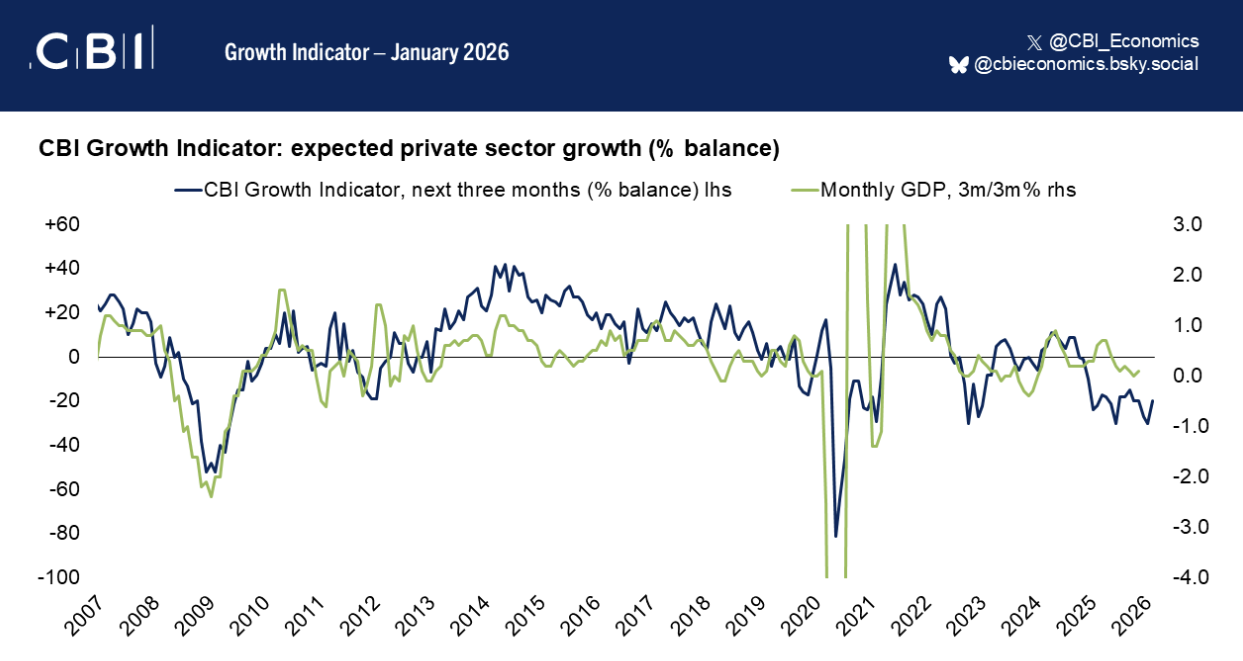

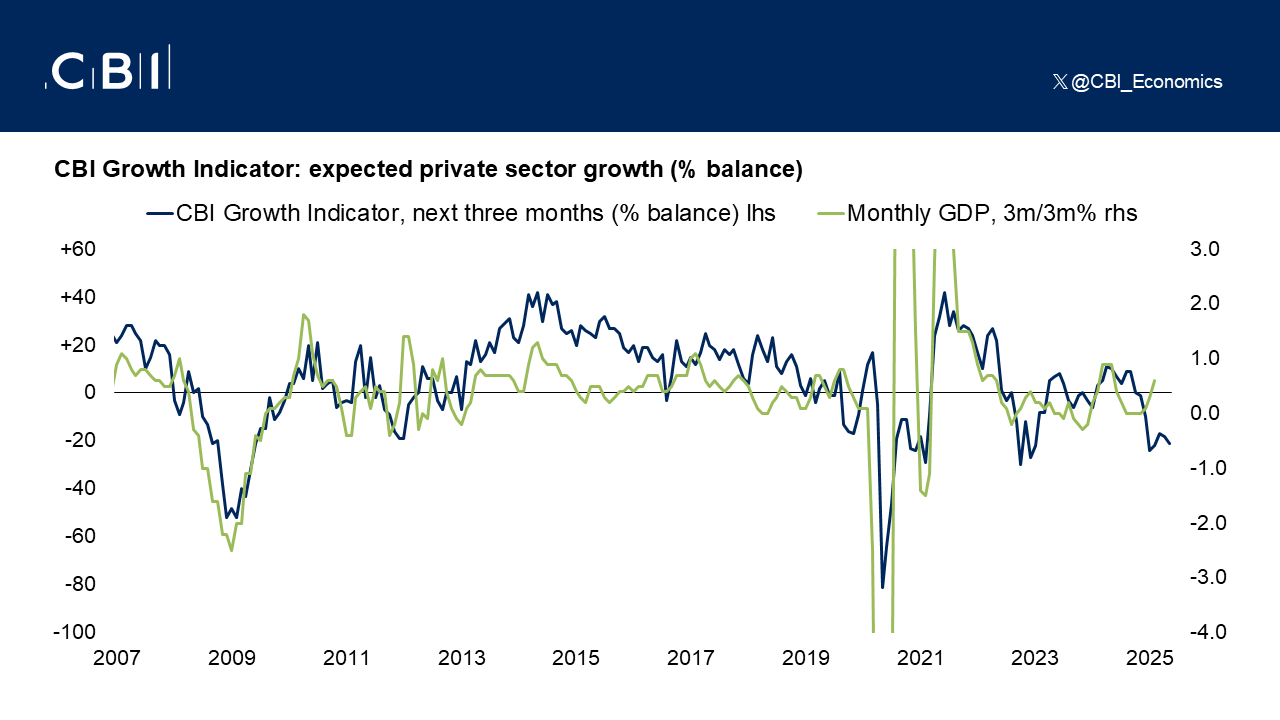

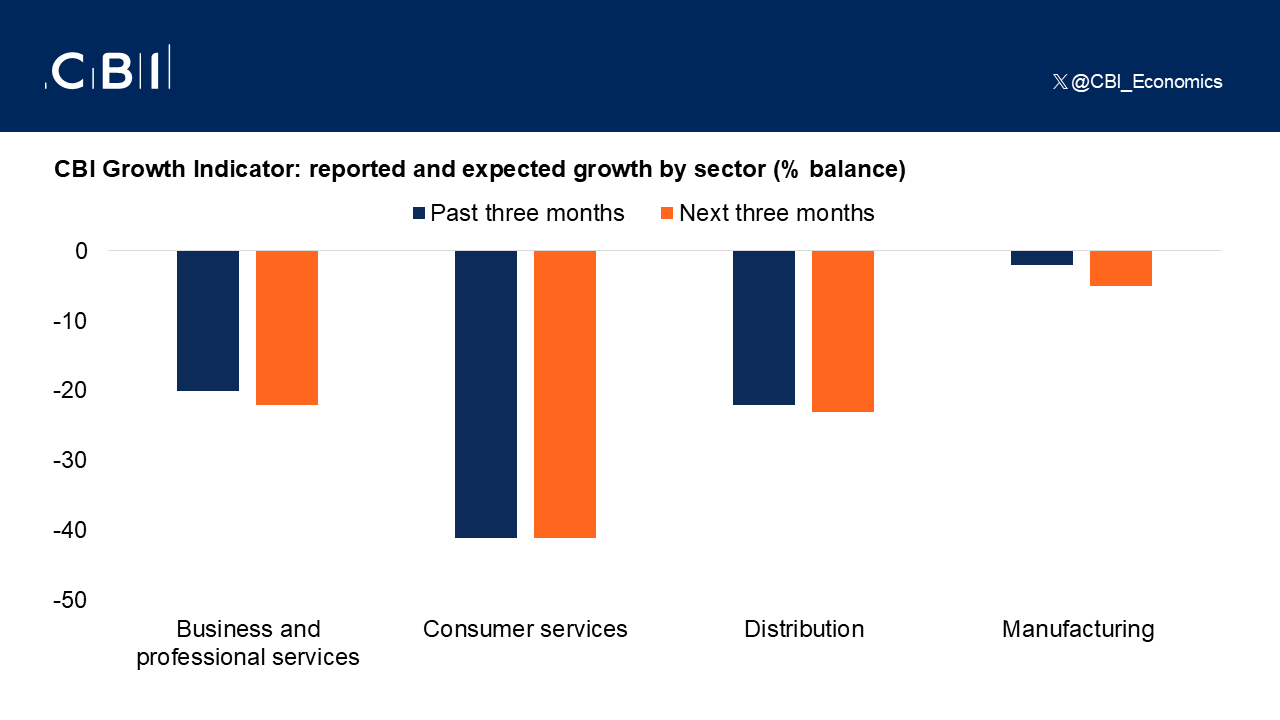

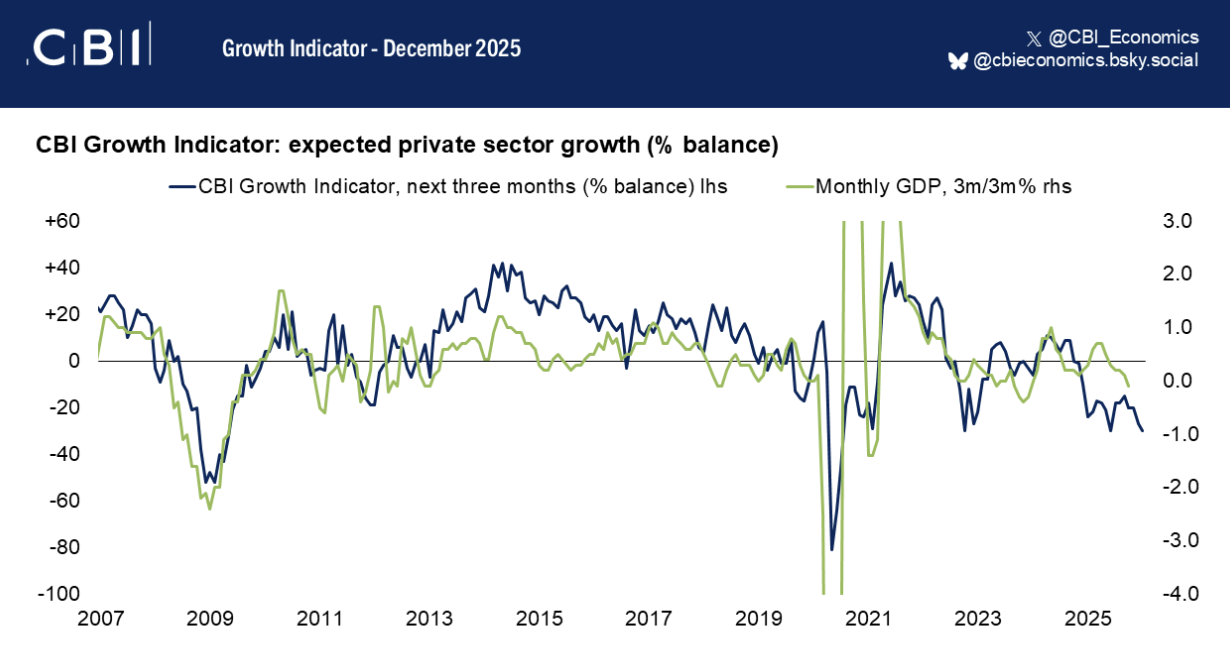

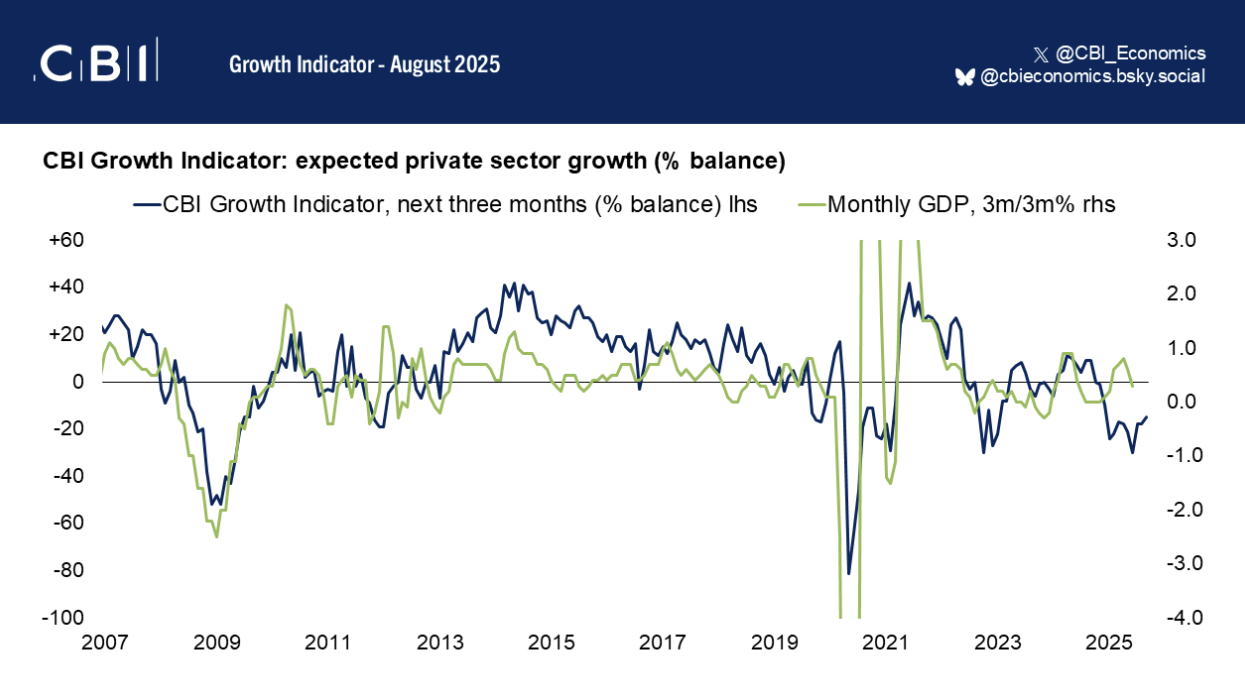

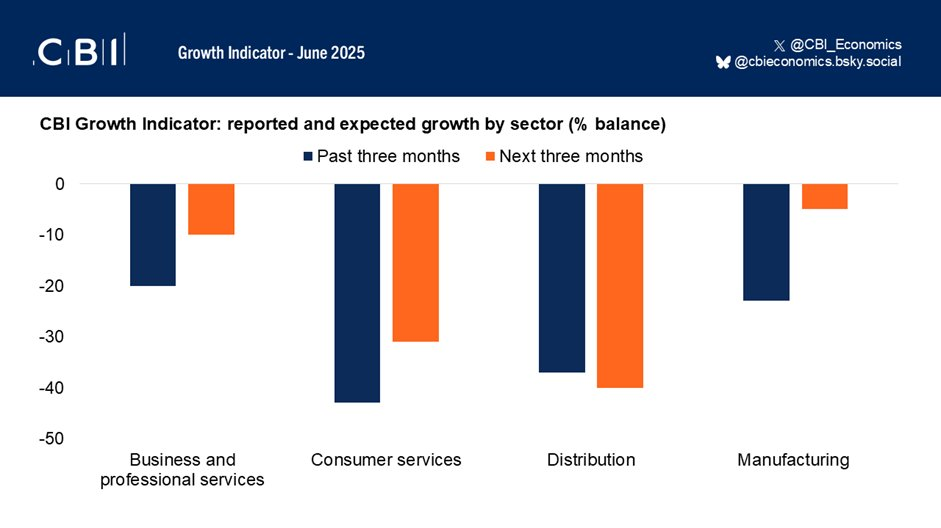

Firms across the private sector expect activity to fall in the next three months (weighted balance of -13%), according to the CBI’s latest Growth Indicator. Nonetheless the pessimism has eased noticeably, with expectations at their least negative since November 2024.

The downturn is expected to be driven by falling distribution sales (-36%) and a modest decline in manufacturing output (-12%). Business volumes in the services sector are also set to drop, albeit marginally (-5%). Within services, February saw another bleak outlook for consumer services volumes (-38%), whereas business & professional services firms expect activity to rise in the three months to May (+4%). This marks the most positive expectations for business and professional services since the quarter to October 2024.

The subdued outlook comes as private sector activity fell in the three months to February (-19%, at a slower pace from -33% in the three months to January). All sub-sectors reported falling activity.

Charlotte Dendy, CBI Economic Surveys & Data Manager, said:

“While private sector firms still expect activity to fall over the next three months, the improvement in the outlook is notable – with expectations at their least negative since November 2024. Nevertheless, expectations remain well below their long-run average, underscoring the fact that firms continue to face a challenging trading environment.

“Businesses continue to highlight the impact of recent Budgets on costs, alongside weak customer confidence and a broader lack of demand indicating that the mood remains fragile.

“While the Spring Forecast may not carry the full weight of a Budget, it still provides an important moment for the Chancellor to double down on the government’s growth mission. With business costs continuing to weigh on private sector activity, growth and investment, broader solutions must be found on lowering business energy costs and on the practical implementation of the Employment Rights Act.”

-

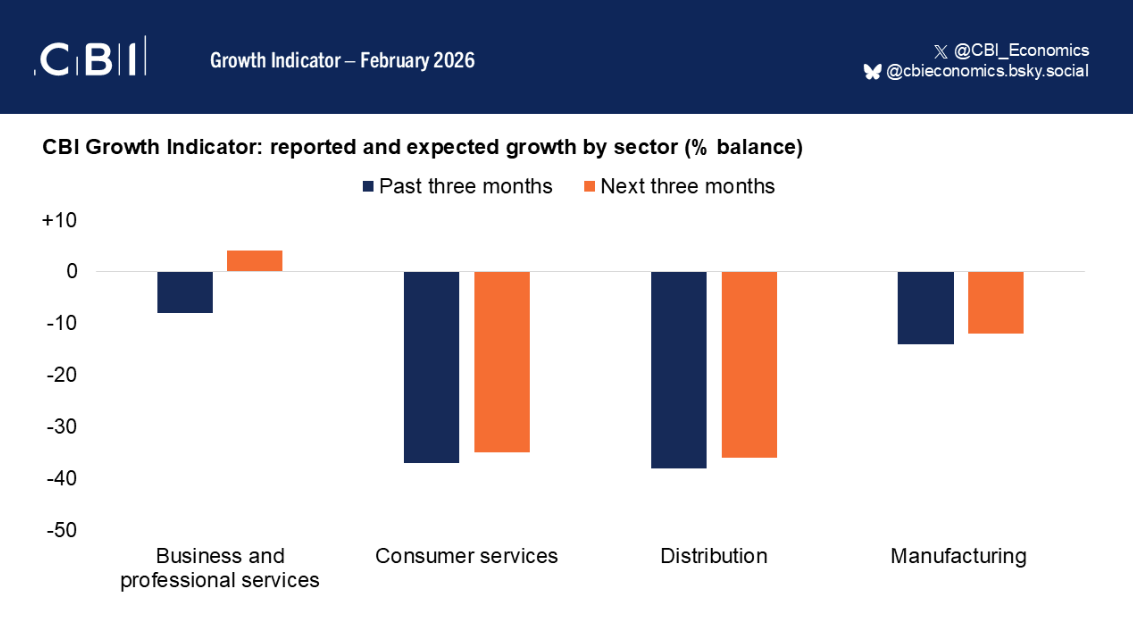

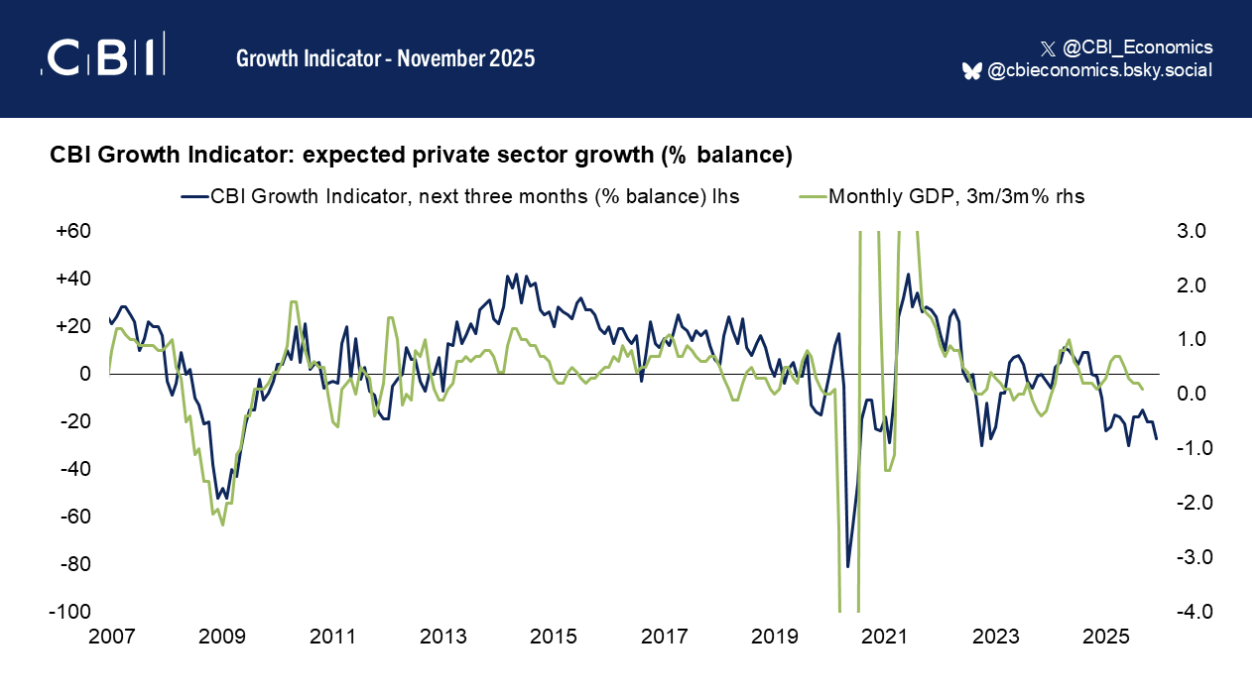

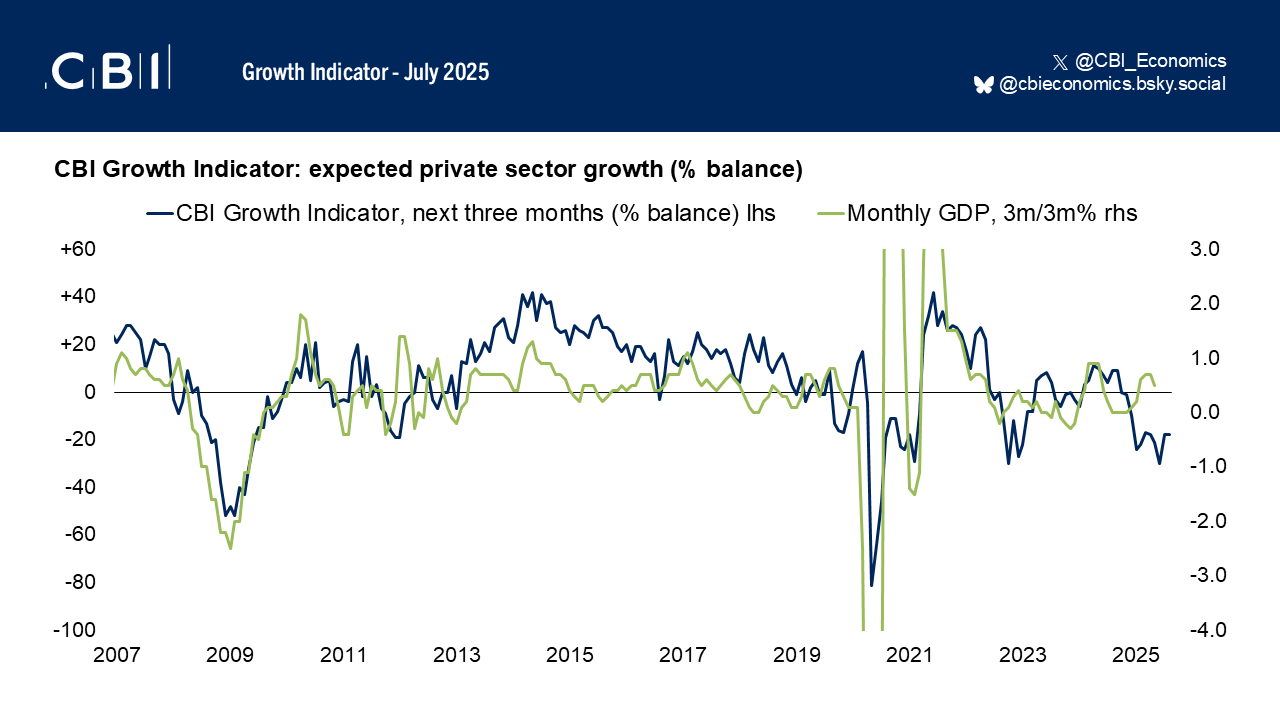

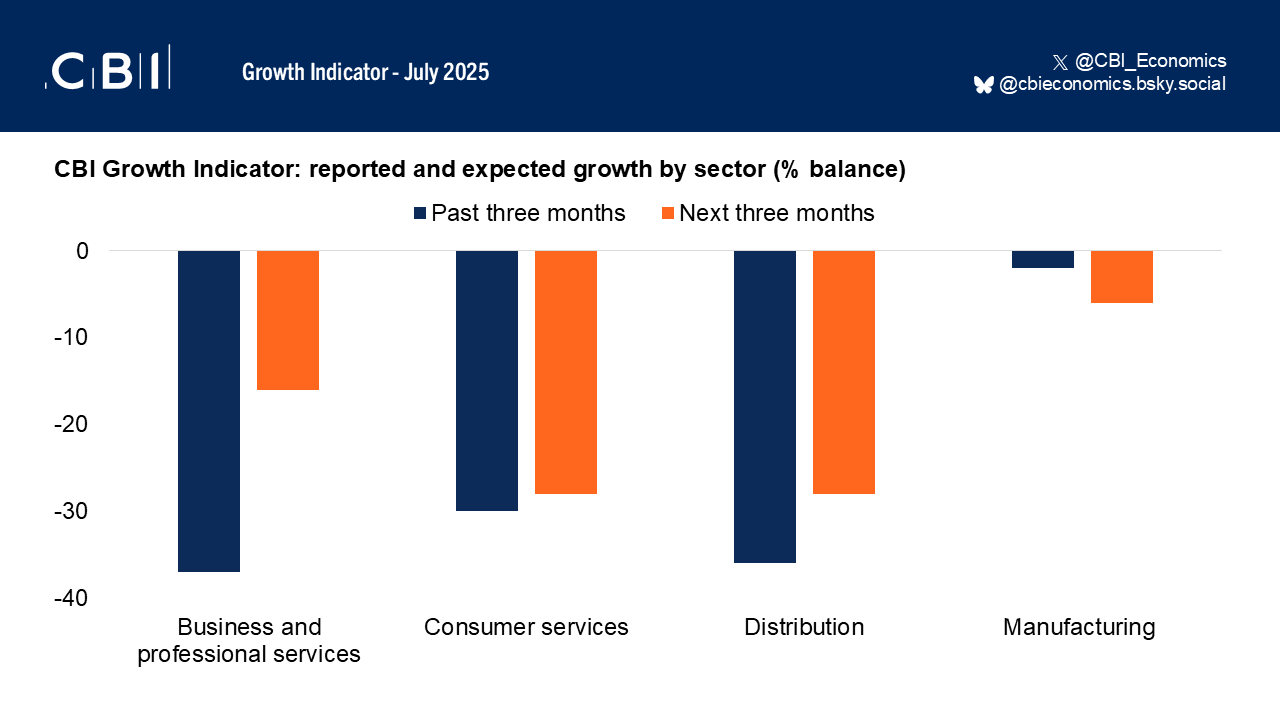

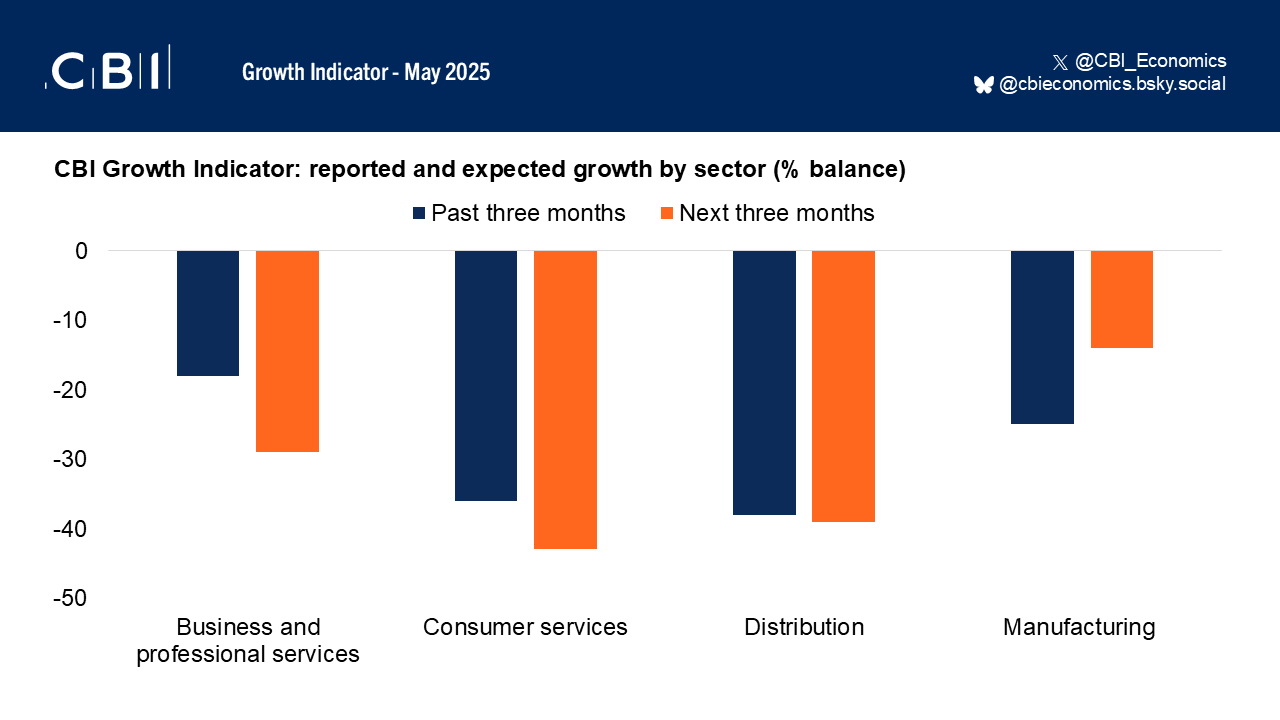

Firms across the private sector once again expect activity to fall in the next three months (weighted balance of -30%), according to the CBI’s latest Growth Indicator. This extends a run of negative predictions that began in late 2024.

The downturn is expected to be broad-based, with business volumes in the services sector set to decline (-29%), driven by weak expectations in both business & professional services (-24%) and consumer services (-46%). Expectations for distribution sales deteriorated significantly, to their weakest since June 2020 (-47%). In contrast, while manufacturers predict another modest fall in output (-17%), expectations were less negative than last month, moving roughly back to where they were in October.

The disappointing outlook comes as private sector activity fell again in the three months to December (-34%, broadly unchanged from -35% in the three months to November). All sub-sectors reported falling activity.

Key findings from our monthly Services Sector Survey showed:

- Business volumes in the services sector fell in the three months to December (-40%), at a broadly similar pace as in the three months to November.

- Both business & professional services (-34%) and consumer services (-40%) volumes fell heavily through the quarter.

- Hiring intentions within the services sector remain weak (-34%), now at their lowest since July 2020. Business & professional services companies expect headcount to fall over the next three months (-24%), while consumer services firms expect a sharp fall in numbers employed (-51%)

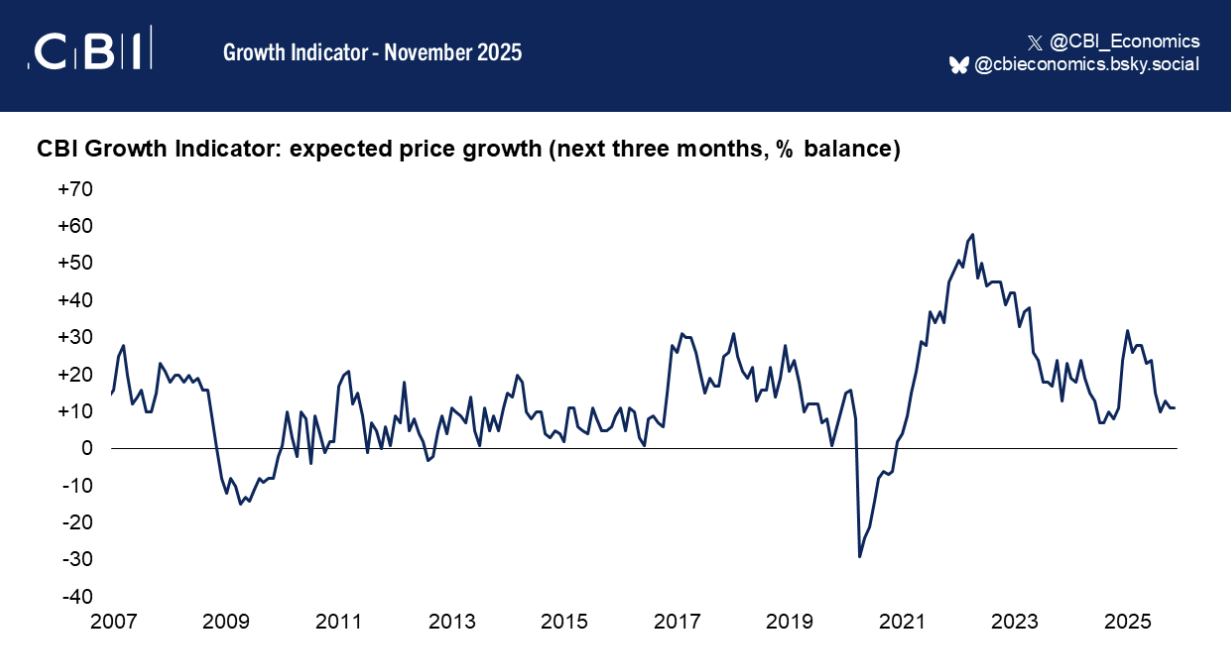

- Selling price inflation expectations in the services sector accelerated in December (+15%, from +7% in November). This reflects a pick up in expectations for both business & professional services firms (+12%) and consumer services (+26%).

Alpesh Paleja, CBI Deputy Chief Economist, said:

“Our latest surveys round off a disappointing year for private sector growth. They mark a continuation of the headwinds that have plagued businesses over the past 12 months: tepid demand conditions, with households cautious around spending; and strong cost pressures squeezing margins.

“Uncertainty ahead of November’s Budget also put the brakes on key spending decisions and big projects, choking up pipelines of work. The latest Growth Indicator suggests that the alleviation of this uncertainty hasn’t materially boosted activity.

“Business cannot face another year of stasis and will be looking for the government to expedite delivery in 2026. The effective model of compromise and partnership achieved on the Employment Rights Bill demonstrates what can be achieved through meaningful collaboration. The government must now further leverage private sector expertise to broaden industrial energy cost support and simplify the tax system in pursuit of its growth mission.”

-

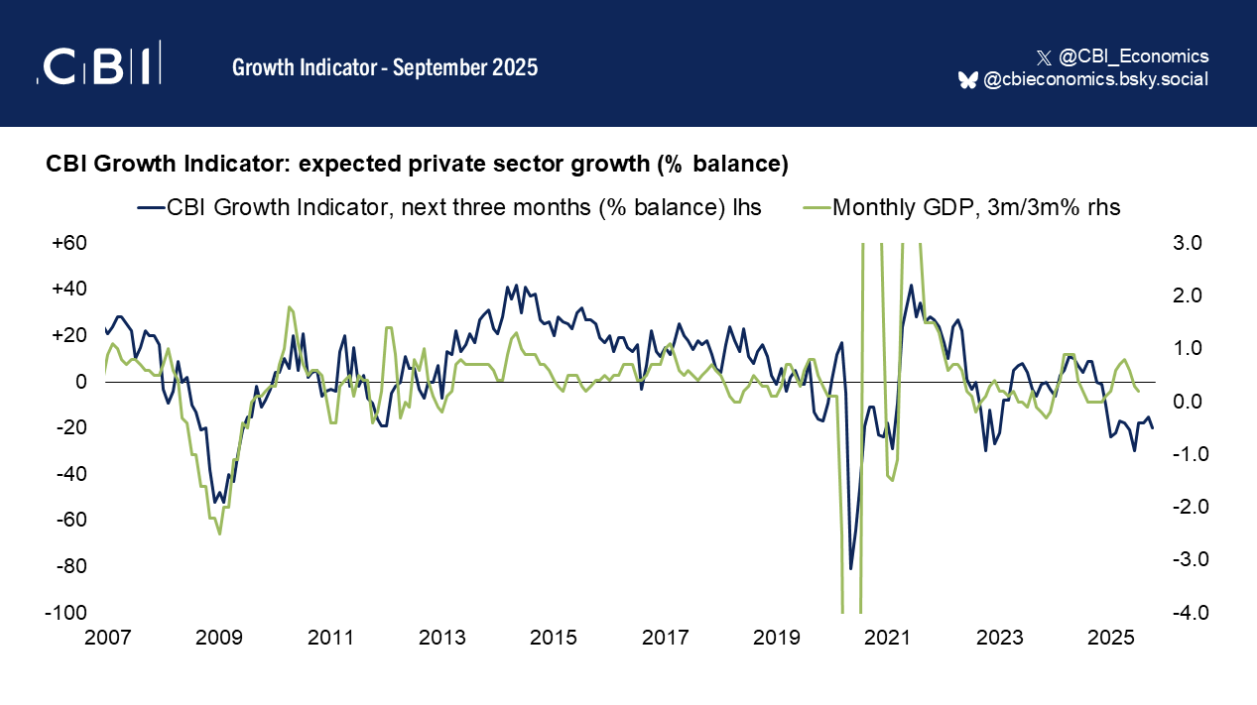

Firms across the private sector once again expect activity to fall in the next three months (weighted balance of -27%), according to the CBI’s latest Growth Indicator. This extends a run of negative predictions that began in late 2024.

The downturn is expected to be broad-based, with business volumes in the services sector set to decline (-26%), driven by weak expectations in both business & professional services (-23%) and consumer services (-40%). In both sectors, predictions for growth are at their weakest in six months. Both distribution sales (-26%) and manufacturing output (-30%) are also expected to fall, the latter seeing the most negative expectations in almost a year.

The disappointing outlook comes as private sector activity fell in the three months to November (-35%), at the fastest pace since August 2020. All sub-sectors reported falling activity.

The CBI’s November surveys – which comprise this month’s Growth Indicator – were in field before the Budget.

Alpesh Paleja, CBI Deputy Chief Economist, said:

“Growth expectations weakened in November, some of which may be down to jitters ahead of last week’s Budget. Businesses tell us that much of the month passed in limbo ahead of that, with big discretionary spending and investment on hold. “However, this only compounded the headwinds to growth that have been apparent throughout the year: cautious spending behaviour by households and clients making demand conditions tepid, against a backdrop of persistent cost pressures for corporates.

“Stability is the precursor to growth. While last week’s Budget is likely to add further costs to businesses, notably with the addition of NICs to salary sacrifice pension contributions, the fiscal headroom created may provide some stability going forward.

“The government must now leverage enterprise expertise to unlock economic growth. This starts by applying the effective model of compromise and partnership achieved on the Employment Rights Bill, by collaborating directly with business to boost growth.”

A balance is the weighted percentage of companies reporting an increase minus those reporting a decrease.

-

Firms across the private sector expect activity to fall in the next three months (weighted balance of -20%), extending a run of negative predictions that began in late 2024, according to the CBI’s latest Growth Indicator.

The downturn is expected to be broad-based, with business volumes in the services sector set to decline (-15%), driven by weak expectations in both business & professional services (-12%) and consumer services (-28%). Distribution sales are expected to fall sharply (-34%), alongside a contraction in manufacturing output (-19%).

The disappointing outlook comes as private sector activity fell in the three months to October (-32%), the same pace as in the three months to September. All sub-sectors reported falling activity.

Alpesh Paleja, Deputy Chief Economist, CBI, said:

“Firms are facing a difficult winter, with private sector momentum weak and confidence fragile. Uncertainty around the upcoming Budget is weighing heavily on sentiment, with many firms keeping key decisions on hold until more clarity is forthcoming. Cost pressures from a variety of sources remain strong, with last year’s tax rises adding to the drag.

“As a result, tough decisions to deliver policy stability and address fiscal pressures will be needed at the Budget. Our surveys clearly show that the private sector cannot bear the brunt of these decisions once again. The business tax burden is already at a 25-year high and – rather than tinkering around the edges – the Chancellor must strategically address the tax system’s complexities that are undermining growth and deliver a Budget and tax system that helps businesses invest, hire, and scale.”

-

Firms across the private sector expect activity to fall in the next three months (weighted balance of -20%), extending a run of negative predictions that began in late 2024, according to the CBI’s latest Growth Indicator.

The downturn is expected to be broad-based, with business volumes in the services sector set to decline (-18%), driven by weak expectations in both business & professional services (-14%) and consumer services (-31%). Distribution sales are expected to fall at significantly (-33%), alongside a contraction in manufacturing output (-14%).

The disappointing outlook comes as private sector activity fell in the three months to September (-32%). All sub-sectors reported falling activity.

Alpesh Paleja, CBI Deputy Chief Economist, said:

“The weakness in private sector activity doesn’t show any signs of letting up and is now expected to persist to the end of this year. The themes cited by businesses paint a, by now, familiar picture: demand conditions are lacklustre, with firms feeling the knock-on impact of cautious spending and investment behaviour across the economy. Wrapped into this, the rise in employer NICs and the National Living Wage continue to bite on bottom lines. And a persistent climate of global economic uncertainty is further hampering decision making.

“This is now accompanied by renewed nervousness around the November Budget, with businesses concerned about being asked to again shoulder the burden of fixing the public finances. The business tax burden is already at a 25-year high and the Chancellor must quickly reaffirm last year’s commitment to no more business tax rises, avoiding Budget speculation further curtailing sentiment in the run up to 26 November. Doing so will boost confidence and accelerate the significant contribution businesses want to be making to the shared growth mission.”

-

Firms across the private sector expect activity to fall modestly in the three months to November (weighted balance of -15%), extending a run of negative predictions that began in late 2024, according to the CBI’s latest Growth Indicator.

The downturn is expected to be broad-based, with business volumes in the services sector set to decline (-15%), driven by weak expectations in business & professional services (-13%) and consumer services (-22%). Distribution sales (-19%) and manufacturing output are also set to contract (-13%). Nonetheless, expectations across most sectors are less weak than those seen in the first half of the year.

The fragile outlook comes as private sector activity fell in the three months to August (-26%). All sub-sectors reported falling activity.

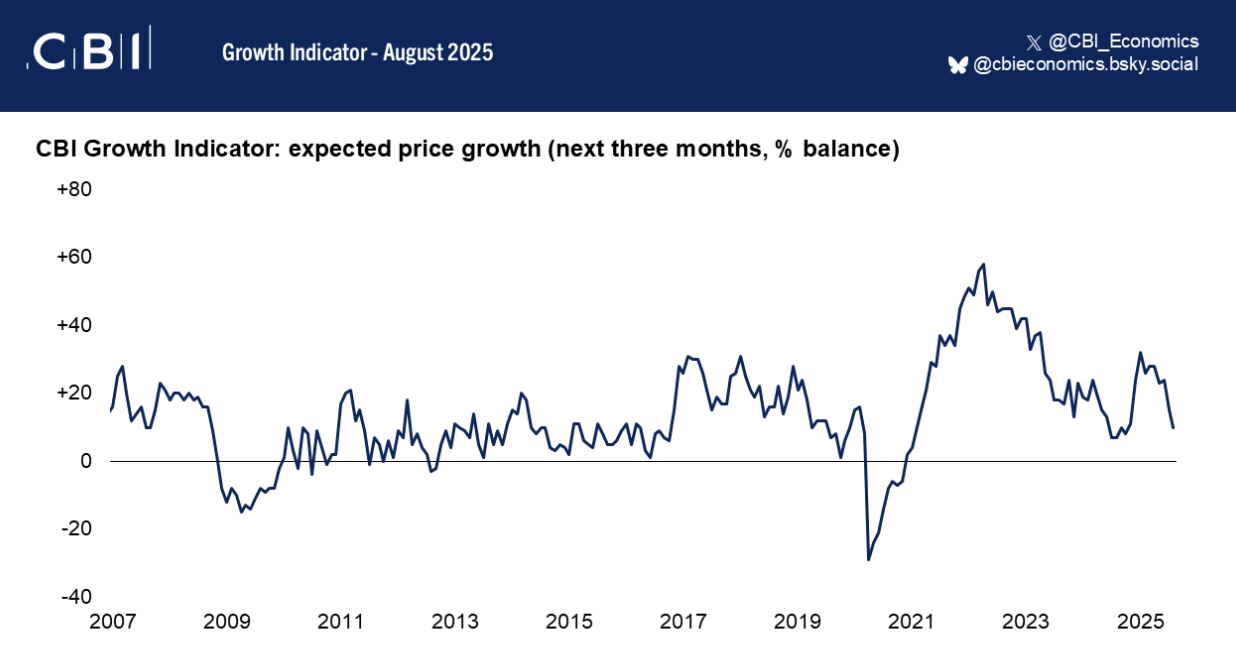

Expected price growth has eased steadily. At +10%, inflation expectations are the softest since October 2024, broadly in line with their our long-run average.

Alpesh Paleja, CBI Deputy Chief Economist, said:

“The outlook remains subdued across the private sector, as businesses continue to grapple with sluggish demand, higher employment costs, increasing uncertainty, and squeezed margins. However, expectations for activity are less negative than in the first half of the year, which is a thin silver lining.

“Even so, there’s little evidence yet of a meaningful turnaround, and firms are increasingly focusing on building resilience and efficiency as they navigate a challenging economic environment – at the expense of capital spending and longer-term growth ambitions.

"Firms are already shouldering the cost of the government’s fiscal decisions. The Autumn Budget must not add to that strain with further tax rises that risk undermining investment and growth. If the government wants to unlock growth, it must cut the cost of doing business, give firms tax certainty, deliver further flexibility to the Growth and Skills Levy, and rethink the Employment Rights Bill.”

A balance is the weighted percentage of companies reporting an increase minus those reporting a decrease.

-

Firms across the private sector expect activity to fall in the next three months (weighted balance of -18%), extending a run of negative sentiment that began in late 2024, according to the CBI’s latest Growth Indicator.

The downturn is expected to be broad-based, with business volumes in the services sector set to decline (-19%), driven by weaker expectations in business & professional services (-16%) and a continually negative outlook in consumer services (-28%). A sizeable fall is also anticipated in distribution sales (-28%), while manufacturing output is expected to dip modestly (-6%).

The weak outlook follows a sharp fall in activity in the three months to July (-29%). Most sub-sectors reported falling activity, while manufacturing output was stagnant.

Alpesh Paleja, CBI Deputy Chief Economist, said:

- “Firms continue to face testing conditions, with expectations pointing to another quarter of falling activity across the economy. While not worsening, the persistently negative outlook underlines the fragility of demand conditions.

- “Against this backdrop, businesses continue to cite headwinds from adjusting to higher employment costs, energy prices and continued uncertainty from a volatile global environment. With few signs of recovery on the horizon, firms are focused on managing costs and streamlining processes in what looks set to be a subdued second half of the year

- “Building positive business sentiment will require the government to translate its long-term strategic thinking into short-term delivery progress. The government must work collaboratively with business in the lead up to this year’s Autumn Budget: acknowledging the significant burdens that firms are facing and mitigating the damaging impact on sentiment from continued fiscal uncertainty.

- “Detailing how the government will deliver its action plan to tackle regulatory barriers to growth; positioning businesses to invest in the people they need through a flexible Growth and Skills Levy; and finding an appropriate landing zone for the Employment Rights Bill are positive next steps the government should be prioritising to build confidence in its growth mission.”

-

Private sector companies expect activity to fall at a firm pace in the three months to September (weighted balance of -18%), according to the CBI’s latest Growth Indicator. Expectations are less negative relative to May, but extend a period of pessimism that began late last year.

Business volumes in the services sector are anticipated to decline (-14%), driven by expected falls in both business & professional services (-10%) and consumer services (-31%) volumes. Distribution sales are expected to fall in the three months to September (-40%, the weakest expectations since September 2022), while manufacturers expect output to fall only slightly (-5%).

The negative outlook comes as private sector activity fell again in the three months to June, at the same pace as in May (-26%). The decline in activity was broad-based across all sectors.

-

Private sector firms once again expect activity to fall in the three months to August (weighted balance of -30%), according to the CBI's latest Growth Indicator. Expectations have deteriorated further, and are now at their weakest since September 2022.

Business volumes in the services sector are expected to decline (-32%), with expectations at their weakest since November 2022. The anticipated fall is driven by predictions of decline in both business & professional services (-29%) and consumer services (-43%) volumes. Distribution sales are also expected to fall in the three months to August (-39%, also the weakest expectations since September 2022), alongside manufacturing output (-14%).

The negative outlook comes as private sector activity fell again in the three months to May (-26%, from -19% in April). The decline in activity was broad-based across all sectors.