2026-06-12 · 15:00

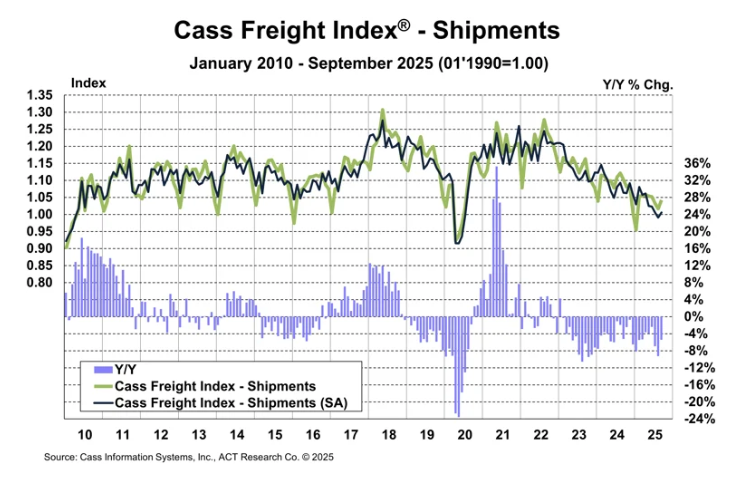

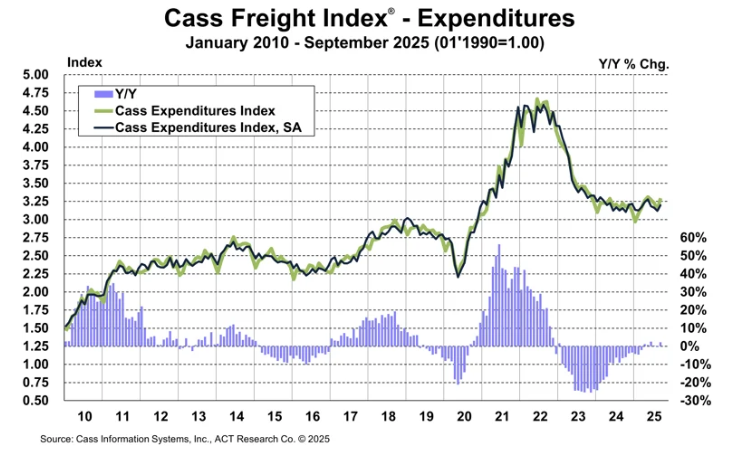

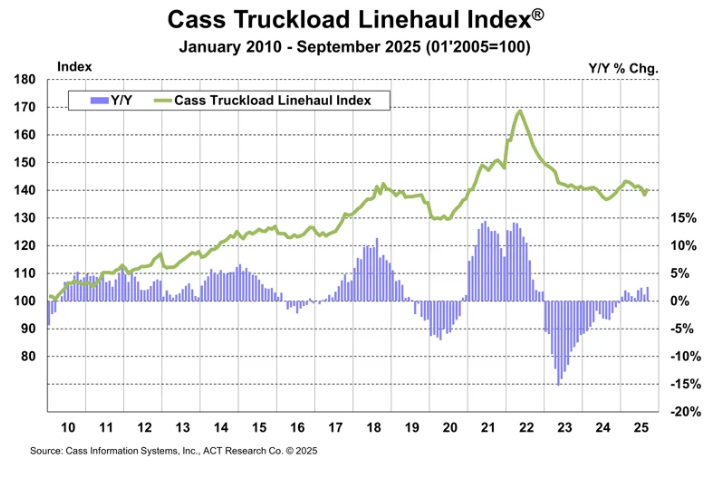

Cass Freight Index: May 2026

Cass Freight Index

About

Source

Cass Information Systems

Source Link

Frequency

Monthly

13th of the month

Region

USA

Latest Releases

12

2026-05-13 · 15:00

Cass Freight Index: April 2026

2026-04-13 · 15:00

Cass Freight Index: March 2026

2026-03-13 · 15:00

Cass Freight Index: February 2026