Cass Freight Index

Cass Freight Index

- Source

- Cass Information Systems

- Source Link

- https://www.cassinfo.com/

- Frequency

-

Monthly

13th of the month

Latest Updates

-

Cass Freight Index: February 2026

-

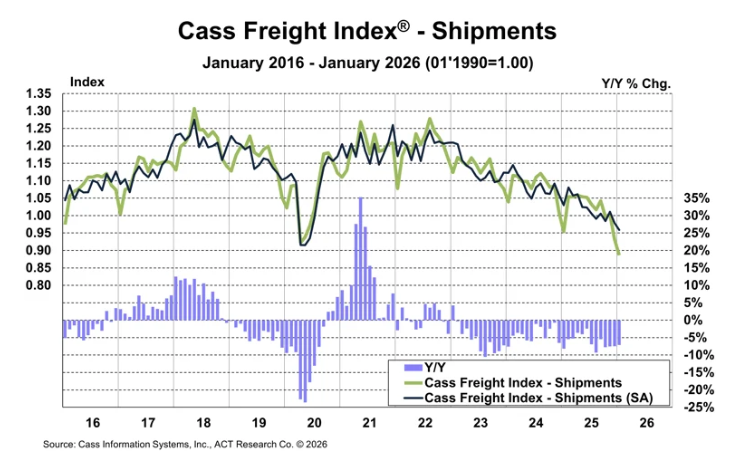

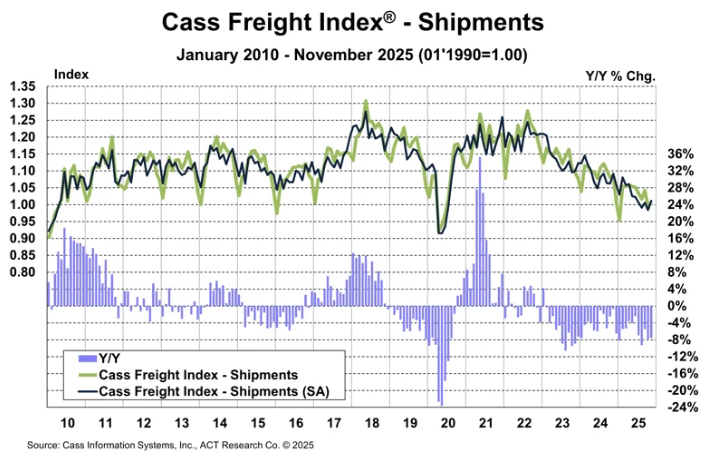

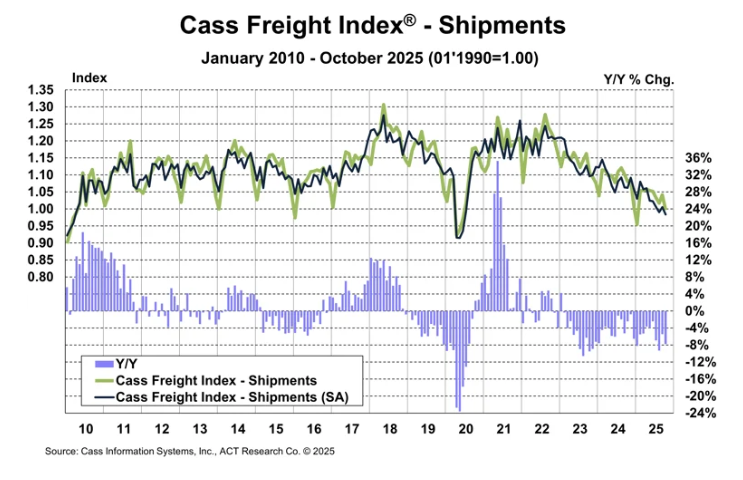

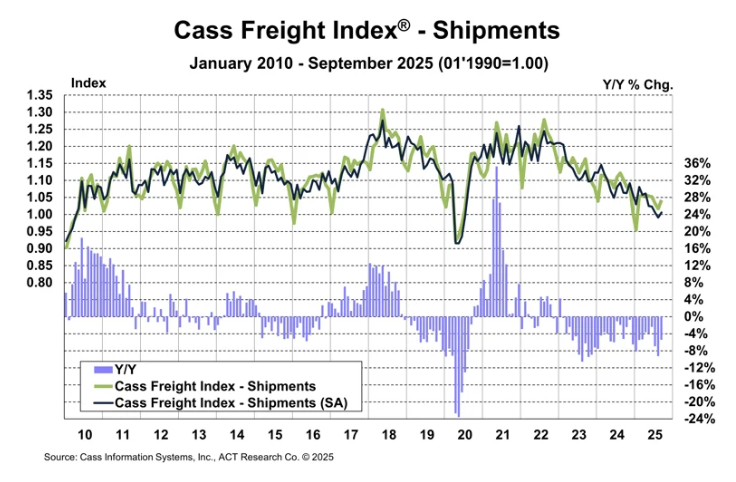

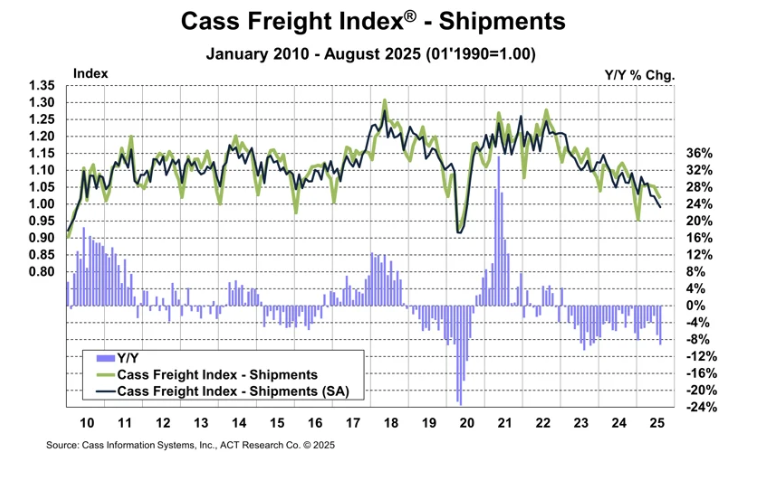

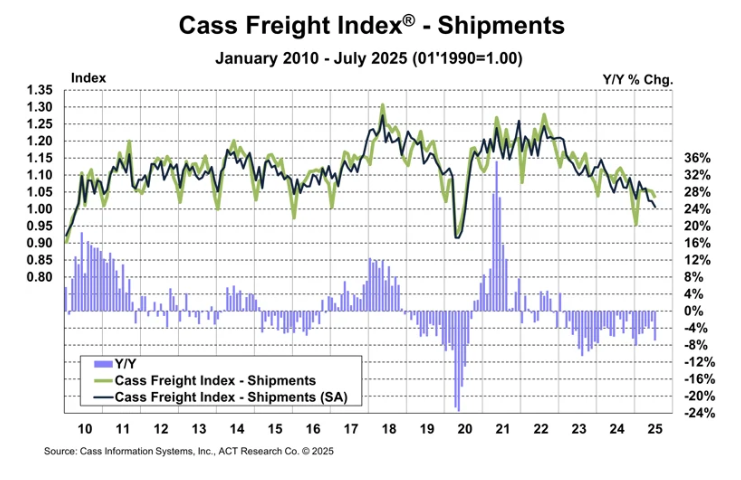

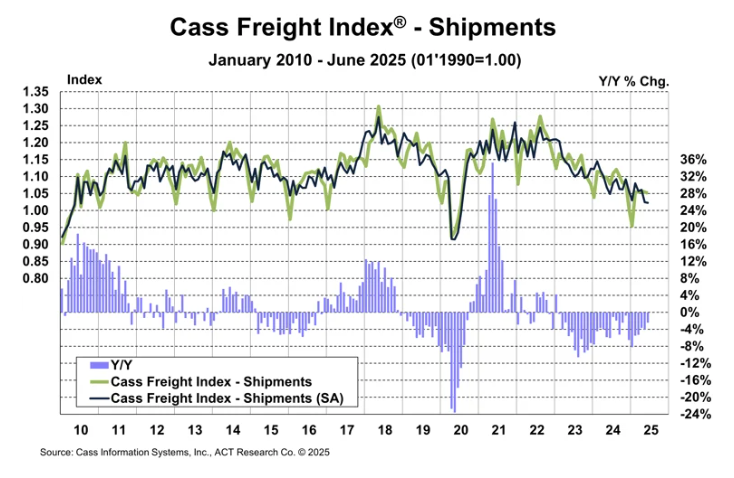

The Cass Freight Index showed shipments down -4.9% MoM (-2.0% SA) and -7.1% YoY in January, reaching a new freight cycle low.

- The normal seasonal trend would have the shipments component of the Cass Freight Index down -11% YoY in February, although a rebound from the weather could support volumes above this.

-

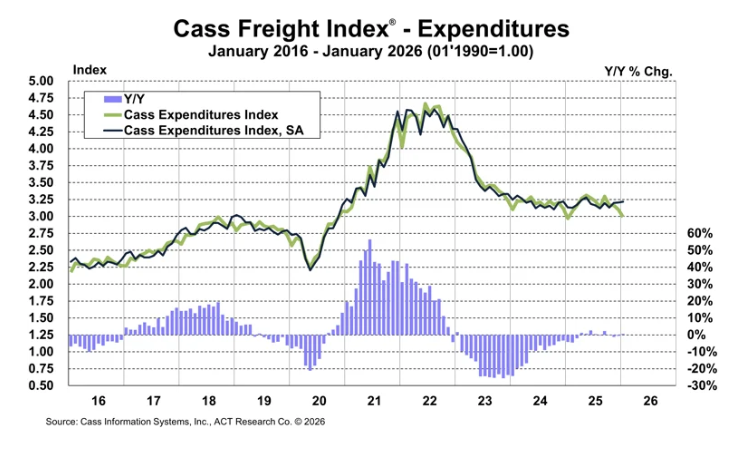

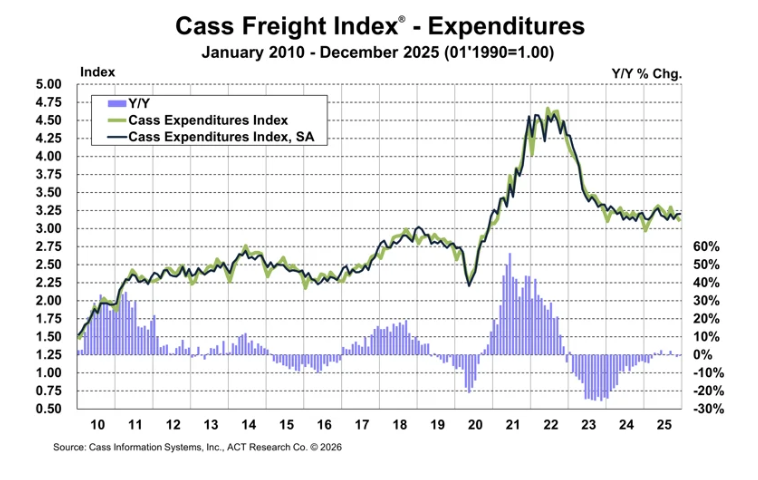

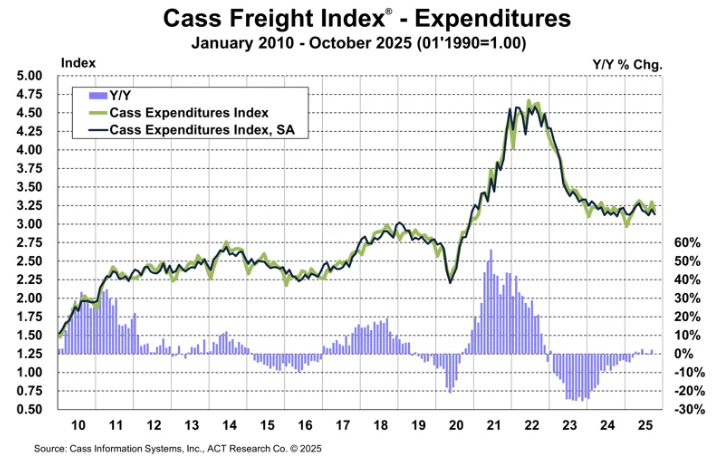

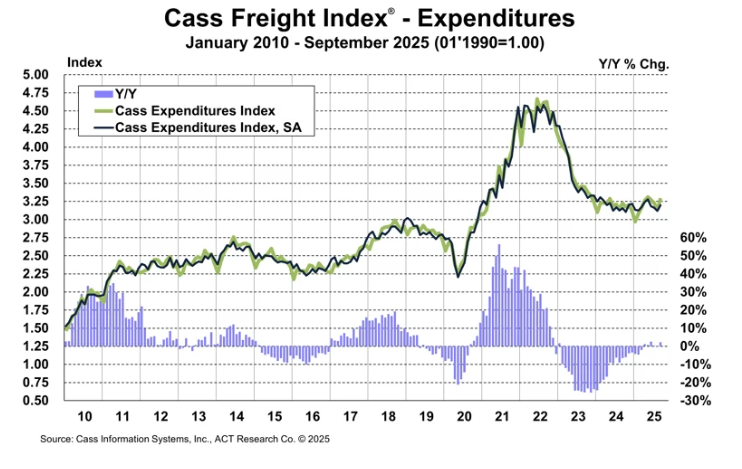

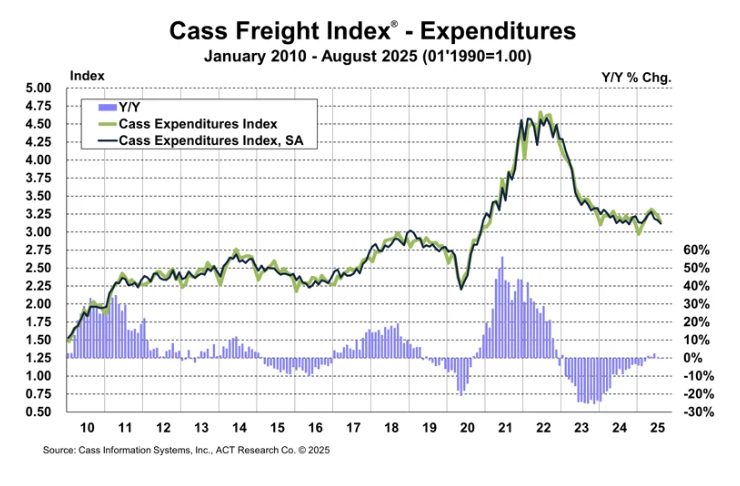

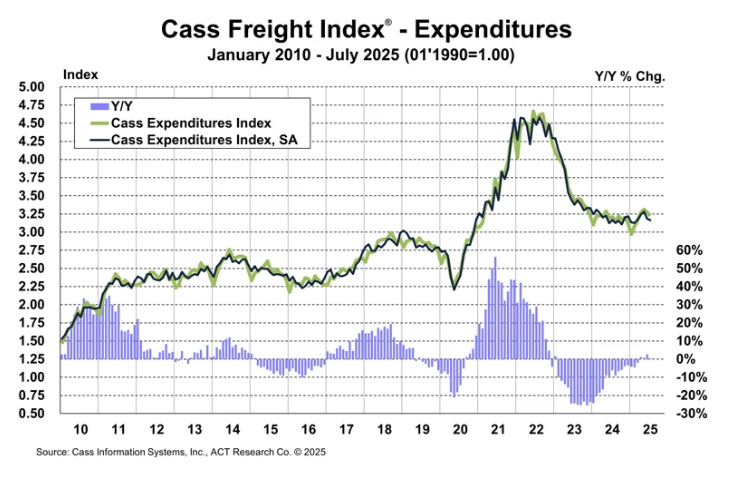

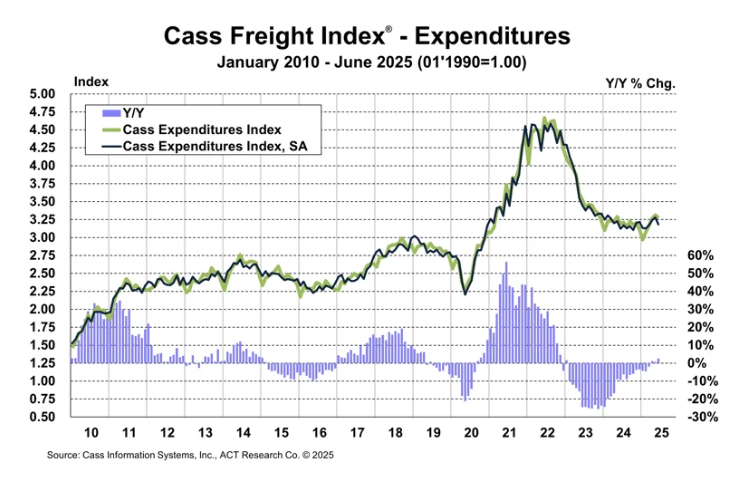

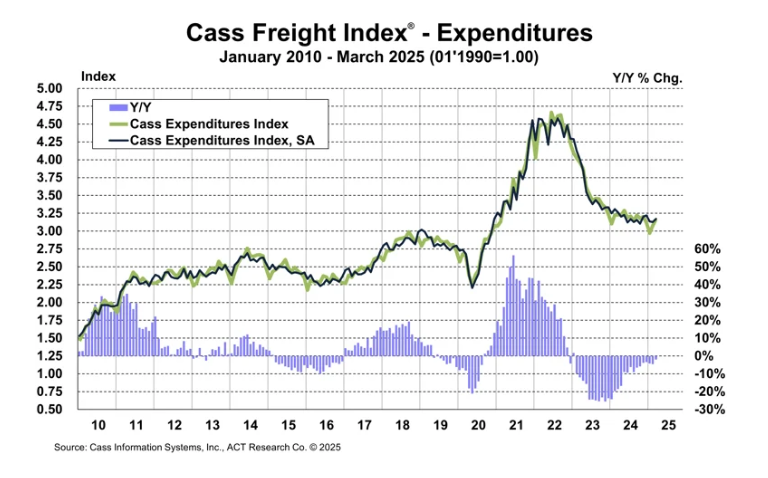

Freight expenditures declined -3.6% MoM but rose +0.6% YoY, suggesting higher rates offset weaker shipment activity.

-

In seasonally adjusted terms, expenditures increased +0.4% MoM after +0.2% in December, pointing to modest underlying spending firmness.

-

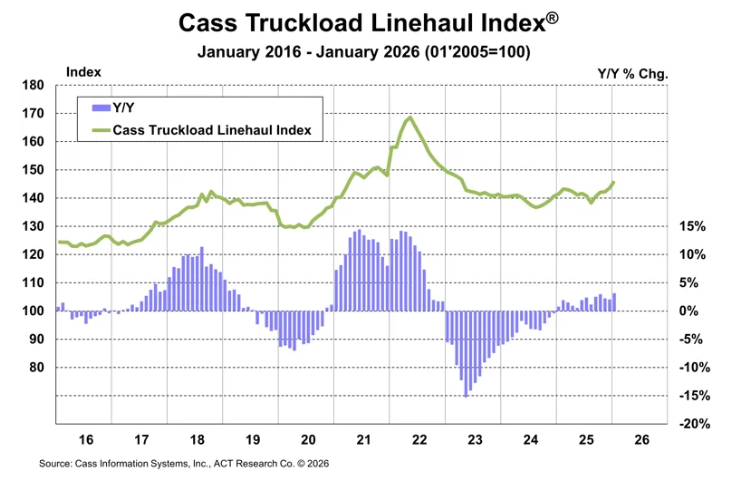

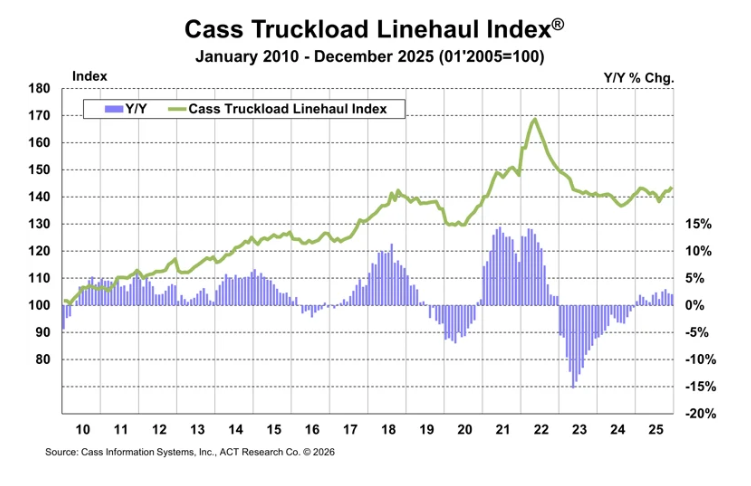

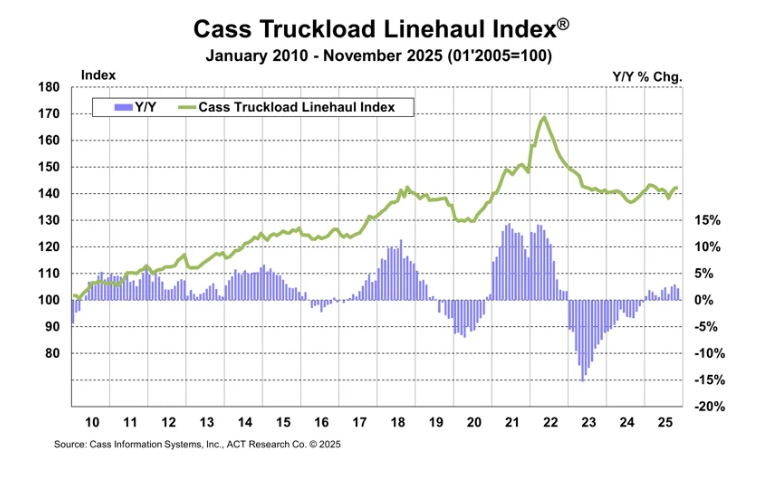

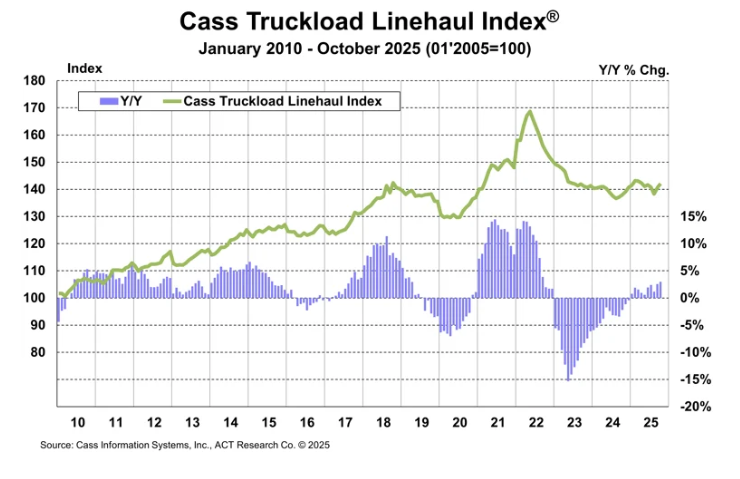

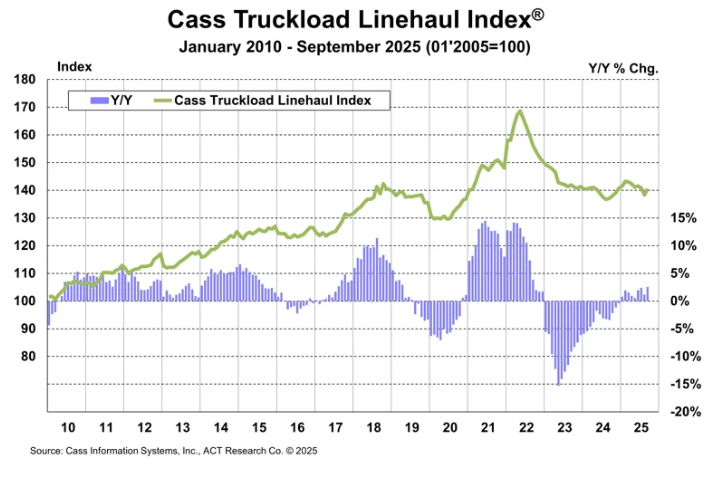

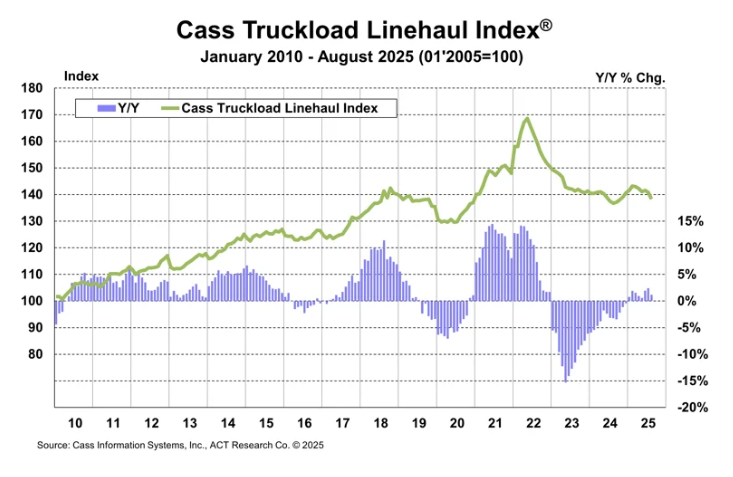

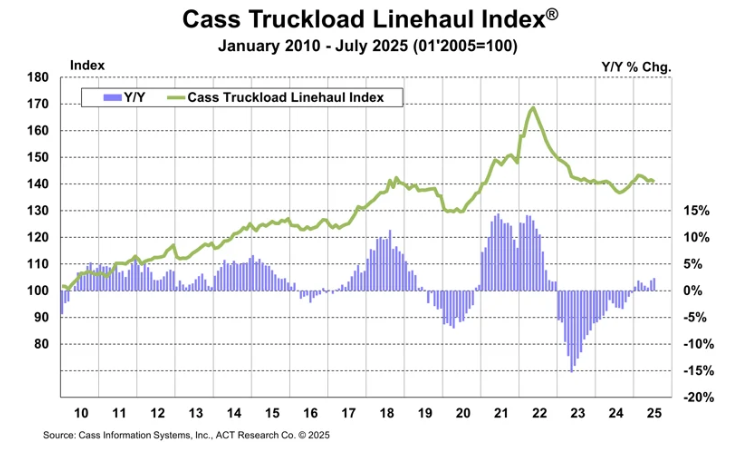

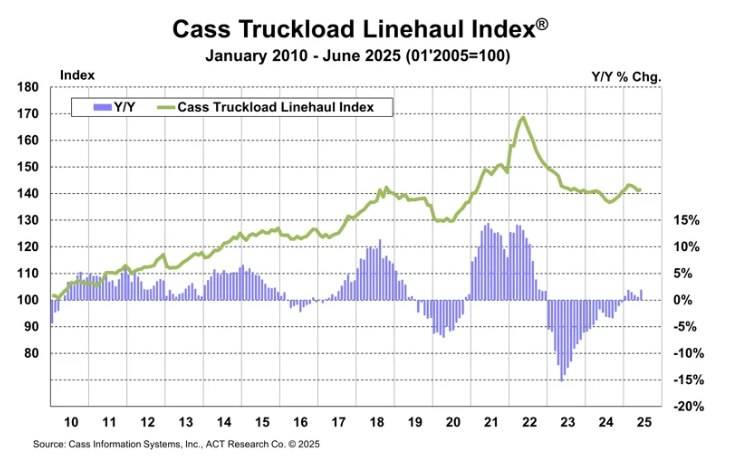

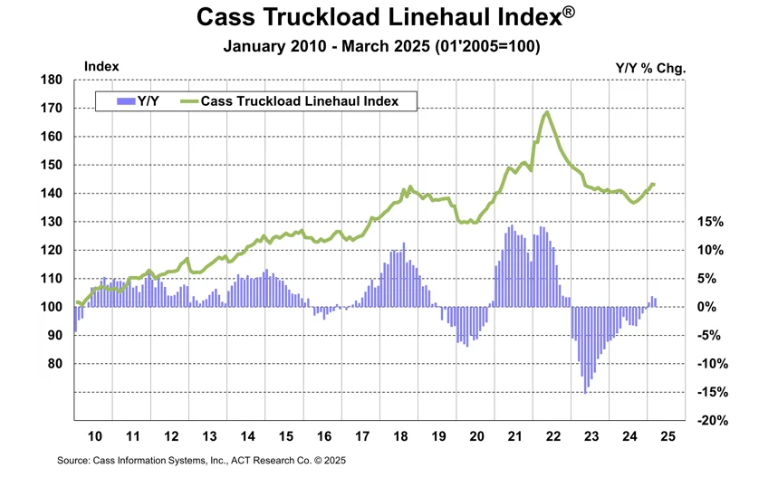

The Truckload Linehaul Index rose +1.7% MoM and +3.2% YoY, reflecting higher contract freight rates amid weather disruptions and tightening capacity.

-

Shipments weakness contrasted with rising rates, indicating freight costs increased despite lower demand volumes.

-

The report noted capacity contraction across equipment, drivers, and operating authorities, while demand continues to grow, supporting rate increases.

-

Prior trends showed expenditures down -19% in 2023, -11% in 2024, and -0.5% in 2025, with the linehaul index turning positive in 2025 (+1.8%), signaling a gradual shift toward recovery.

-

The Cass Freight Index signaled continued freight softness in December 2025, with shipments down -7.2% MoM (-3.2% SA) and -7.5% YoY, reaching a new cycle low.

-

Cass Freight Index shipments fell -7.2% MoM in December (or -3.2% SA), marking a new cycle low and pointing to a sharp monthly pullback in freight volumes.

-

Shipments were down -7.5% YoY in December, slightly worse than the full-year decline of -6.1%, underscoring continued contraction in freight activity.

-

The report noted three winter storms in early December slowed the highway network and created pent-up demand that was still evident in the spot market in early January.

-

Holiday consumer spending was described as stronger than inventory trends, with the report suggesting retail inventories have been destocking in recent months as freight volumes lagged spending.

-

Cass expenditures fell -1.9% MoM in December and were down -0.6% YoY, indicating total freight spend declined less than volumes, consistent with higher rates offsetting lower shipments.

-

In seasonally adjusted terms, expenditures rose +0.2% MoM after a +2.1% SA increase in November, suggesting a modest underlying uptick in spending momentum despite the headline decline.

-

The Truckload Linehaul Index rose +1.0% MoM and +2.1% YoY in December, with the report attributing rate gains amid lower volumes largely to weather disruptions that may prove temporary as backlogs clear.

-

-

The Cass Freight Index showed mixed signals in November 2025, with shipments up modestly MoM but still sharply lower YoY, reflecting ongoing freight market softness despite a short-term rebound.

-

Cass Freight Index shipments rose +0.7% MoM (+2.7% SA) in November, reversing October’s -2.1% SA decline but remaining down -7.6% YoY, underscoring weak annual volume trends.

-

On a 2-year stacked basis, shipments were down -8.2%, highlighting the cumulative contraction following declines in 2023 and 2024.

-

The report noted that truckload volumes softened again in Q4 as pre-tariff inventory buildups were drawn down after a brief Q3 improvement.

-

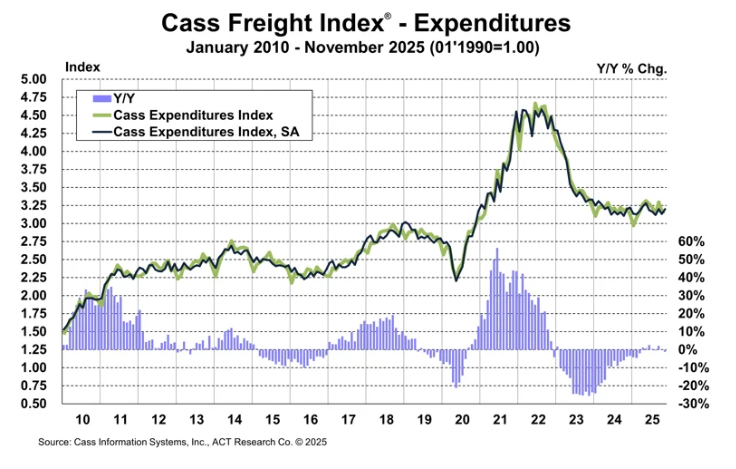

Cass Freight Index expenditures fell -0.2% MoM and were -1.2% YoY in November, reflecting fewer shipments offset by higher freight rates.

-

In seasonally adjusted terms, expenditures rose +2.1% MoM, lagging the shipment gain, implying slightly softer rate momentum.

-

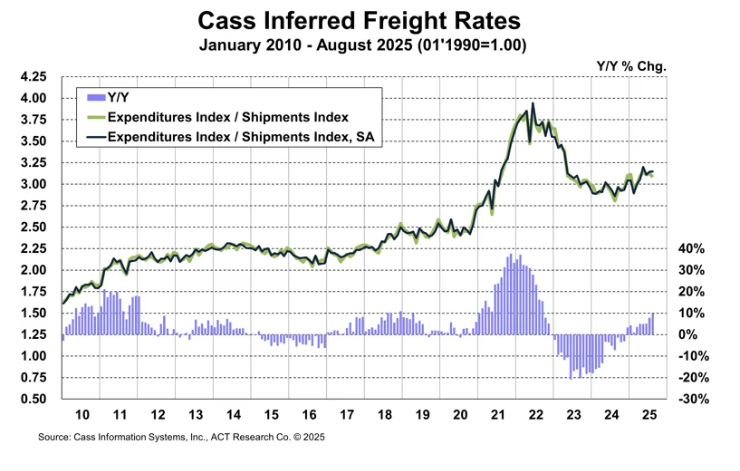

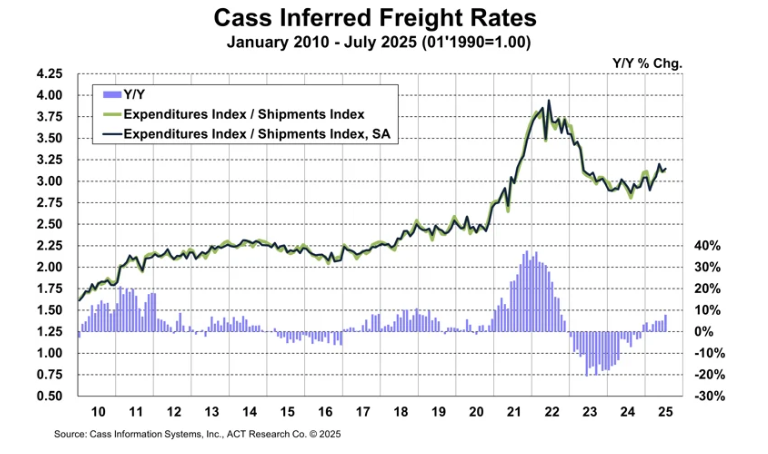

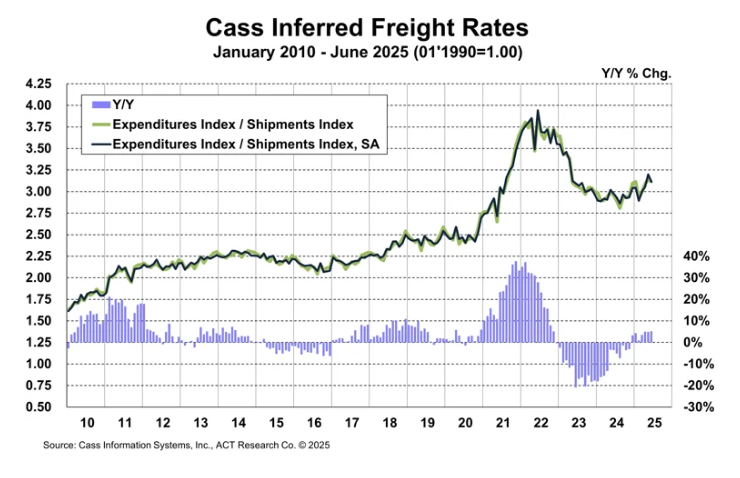

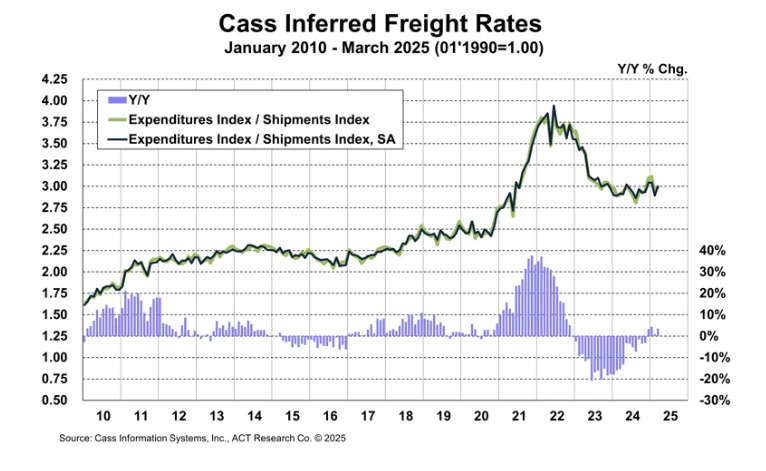

Implied freight rates increased an estimated +6.8% YoY, driven largely by modal mix shifts toward truckload and away from LTL.

-

The Truckload Linehaul Index edged up +0.1% MoM and +2.2% YoY, decelerating from October’s pace and pointing to modest but positive rate pressure late in the year.

-

-

The Cass Freight Index showed broad weakness in October 2025, with shipments down -4.3% MoM (-2.1% SA) and -7.8% YoY, reflecting a reversal of September’s gain and continued soft demand across freight markets.

-

Shipments fell -4.3% MoM (-2.1% SA) to 0.997, with the YoY decline widening to -7.8%, as LTL volumes continued to contract while consolidation into TL persisted.

-

On a 2-year stacked basis, shipments were down -10.0%, underscoring the multi-year downtrend following declines in 2023 and 2024 and a trajectory pointing to another sizable drop in 2025.

-

Expenditures decreased -3.9% MoM (-2.1% SA) to 3.169 and were -0.2% YoY, reversing the +2.2% YoY gain in September as fewer shipments offset higher rates.

-

Rate trends implied by the index point to an estimated +8.2% YoY increase, driven largely by a modal shift toward TL as LTL costs rise, leaving overall expenditures flattish in recent months.

-

The Truckload Linehaul Index rose +1.1% MoM to 142.1 and accelerated to +3.0% YoY, though the report notes some of the recent increase may prove temporary as pre-tariff activity fades.

-

On a 2-year stacked basis the linehaul index was up +0.7%, indicating modest cumulative gains despite prior declines in 2023 and 2024.

-

Broader freight conditions remain strained as capacity continues to contract, fleet profitability remains weak, and tariffs elevate cost pressure, with the outlook hinging partly on the pending Supreme Court ruling on IEEPA tariffs.

-

-

The Cass Freight Index showed modest improvement in September 2025, with shipments up +2.5% MoM (+1.5% SA) but still down -5.4% YoY, signaling a partial rebound after August’s weakness.

-

Shipments rose +1.5% SA MoM, reversing the prior month’s -1.5% decline, as truckload volumes improved while LTL volumes fell amid continued rate-driven consolidation.

-

Expenditures increased +5.1% MoM (+2.5% SA) and +2.2% YoY, reflecting higher rates and modestly stronger volumes.

-

The Truckload Linehaul Index rose +1.7% MoM and +2.6% YoY, accelerating from +1.2% YoY in August.

-

On a two-year basis, shipments were down -10.4% and expenditures -4.5%, underscoring lingering weakness since 2022.

-

Freight capacity continues to tighten, with Class 8 tractor production expected to decline -32% from 1H to 2H 2025, potentially setting the stage for future rebalancing in the for-hire market.

-

Despite short-term gains, the index remains on track for another annual decline in 2025, extending the downtrend that began in 2023.

-

-

The Cass Freight Index showed further weakness in August 2025, with shipments falling -1.5% MoM (-1.5% SA) and down -9.3% YoY, reflecting the persistence of the freight downturn.

-

Shipments fell -1.5% MoM (-1.5% SA) and were down -9.3% YoY. The downturn continues, with declines across LTL shipments while truckload and intermodal volumes held firmer.

-

Expenditures dropped -2.8% MoM (-1.4% SA) and slipped -0.4% YoY. This reflects lower shipment volumes offset by higher average freight rates.

-

Rates fell -1.3% MoM but edged up +0.1% SA. On a yearly basis, they rose +9.8%, driven largely by modal shifts from LTL to truckload.

-

The Truckload Linehaul Index fell -1.8% MoM, after a smaller decline in July, while YoY growth slowed to +1.2%. This index has weakened notably from earlier in the year.

-

Shipments have now declined in consecutive years after strong gains in 2021–22, with 2025 on track for another significant drop. Expenditures show a similar pattern, having retrenched after large increases earlier in the cycle.

-

Freight demand remains soft amid tariff-related headwinds, though moderating Class 8 tractor orders suggest capacity growth is slowing, which could eventually support the for-hire market.

-

-

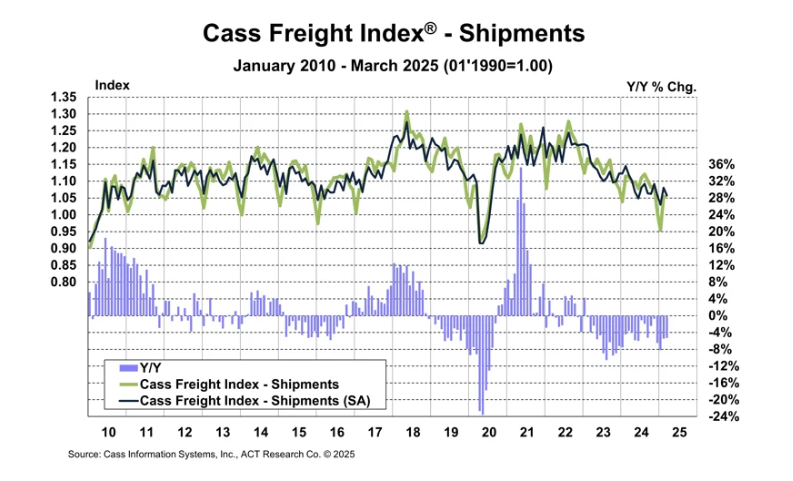

The Cass Freight Shipments Index fell -1.8% MoM (-1.7% SA) in July 2025 and was down -6.9% YoY, marking the sharpest annual drop since early 2024.

- Tariffs hit shipments harder in the most recent data, as paybacks began from demand pull-forwards earlier in the year, though goods prices are still relatively steady.

- The Cass Freight Expenditures Index declined -1.5% MoM (-0.6% SA) but edged up +0.4% YoY, with the gain driven entirely by higher rates.

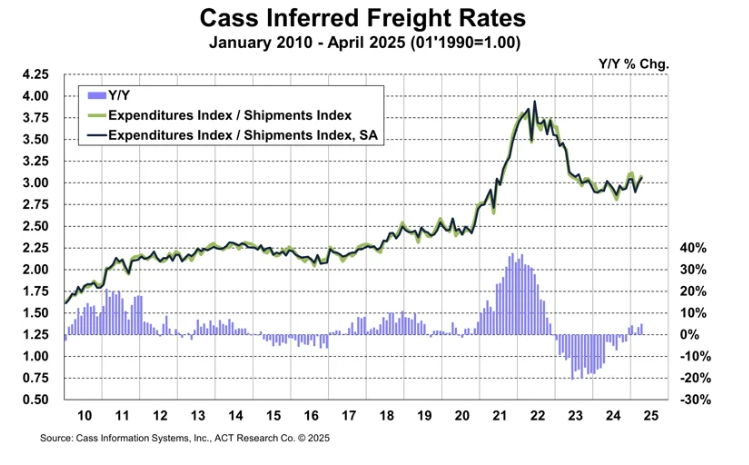

- Inferred Freight Rates rose +0.4% MoM (+1.1% SA) and +7.9% YoY, reflecting modal shifts toward truckload from LTL.

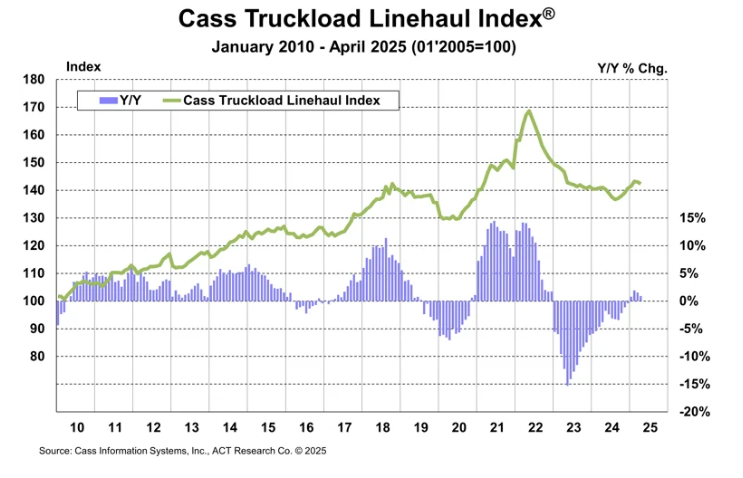

- The Cass Truckload Linehaul Index fell -0.6% MoM but was up +2.4% YoY, supported by easier annual comparisons.

- Freight volumes remain soft, with 2025 on track for another annual decline despite rate increases.

-

The Cass Freight Shipments Index fell -0.2% MoM (-0.2% SA) and -2.4% YoY in June 2025, continuing its multi-year downtrend in volume despite some stability in monthly trends.

- The trade war is having a variety of effects, with a few waves of pre-tariff inventory building and subsequent drawing down, but volumes were steady from May.

- The Cass Freight Expenditures Index dropped -1.2% MoM (-2.9% SA) but rose 2.6% YoY, its third consecutive YoY gain, driven entirely by higher rates.

- Inferred Freight Rates declined -1.0% MoM (-2.8% SA) but rose 5.2% YoY, reflecting modal shifts favoring truckload (TL) over less-than-truckload (LTL).

- The Truckload Linehaul Index rose 0.4% MoM and 1.9% YoY, signaling a modest recovery in per-mile pricing amid easier base comparisons.

- Freight volumes remain soft, and shipment levels are on track for a third straight annual decline, despite rate stabilization.

-

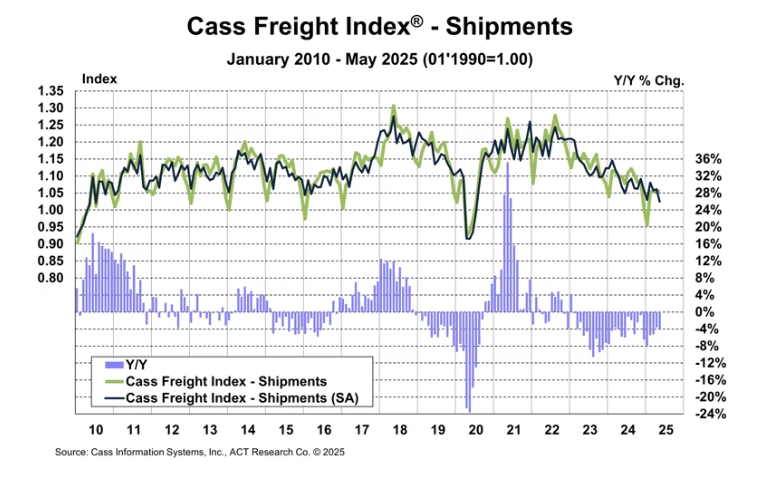

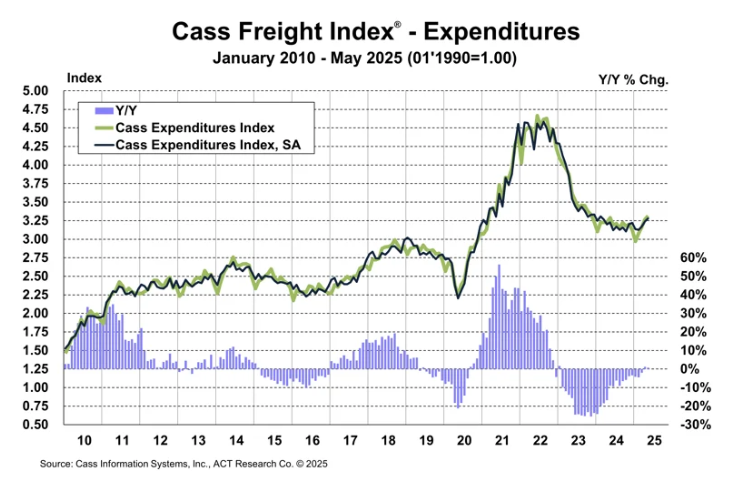

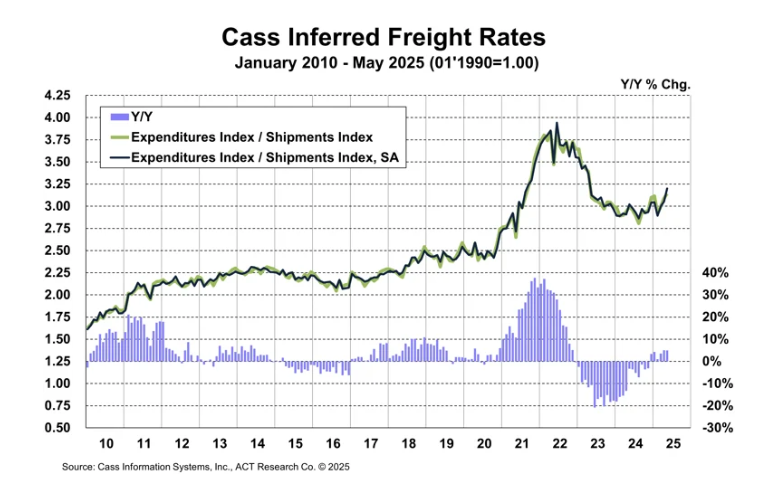

The Cass Freight Shipments Index fell -0.4% MoM in May 2025 and -3.4% MoM on a seasonally adjusted basis, with shipments down -4.0% YoY as pre-tariff inventory stocking began reversing into destocking.

- The Cass Freight Expenditures Index rose 1.4% MoM (1.2% SA) and 0.8% YoY, marking the second consecutive YoY gain after over two years of declines.

- Inferred Freight Rates increased 1.8% MoM (4.8% SA) and 5.0% YoY, with a modal shift toward truckload (TL) supporting average rates.

- The Cass Truckload Linehaul Index declined -0.8% MoM and slowed to +0.6% YoY, suggesting weak underlying rate momentum.

- Freight demand remains soft overall, and the data continue to point toward a third straight year of YoY shipment declines in 2025.

-

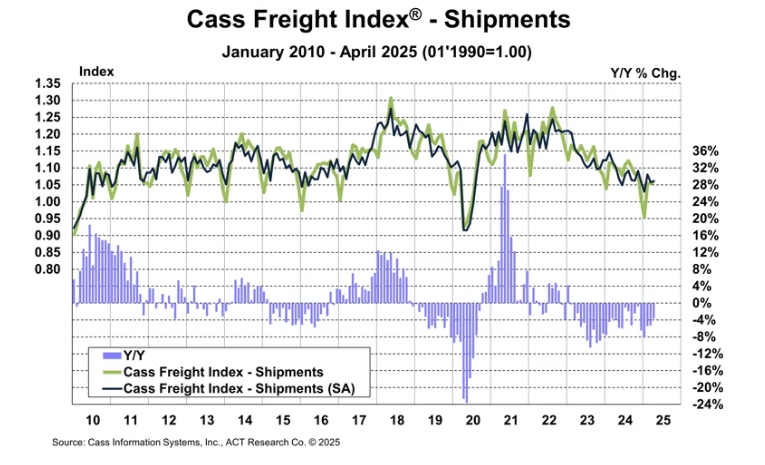

The Cass Freight Shipments Index rose 0.4% MoM (seasonally adjusted, 0.3% MoM) in April and was down -3.6% YoY, a smaller annual decline than March’s -5.3% YoY drop.

- The 6-month trend still points to another annual decline in 2025 after a -4.1% drop in 2024.

- The trade war is having a variety of effects on freight volumes, with significant decreases likely in May and June in international volumes, but likely a rebound in Q3 due to the recent 90-day U.S./China trade deal.

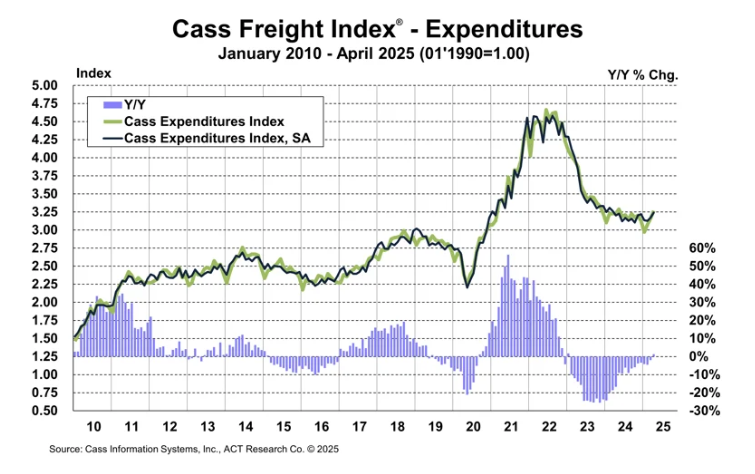

The Cass Freight Expenditures Index rose 3.3% MoM (seasonally adjusted, 2.2% MoM) and turned positive YoY for the first time in 28 months, up 1.2% YoY.

- Inferred Freight Rates rose 2.9% MoM (seasonally adjusted, 1.8% MoM) and 5.1% YoY, up from 3.5% YoY in March.

- Tougher comparisons in May and June suggest the rate may slow. After a 7% decline in 2024, freight rates are on track for low-single-digit increases in 2025.

- The Cass Truckload Linehaul Index fell -0.5% MoM and slowed to +0.9% YoY, from +1.5% YoY in March.

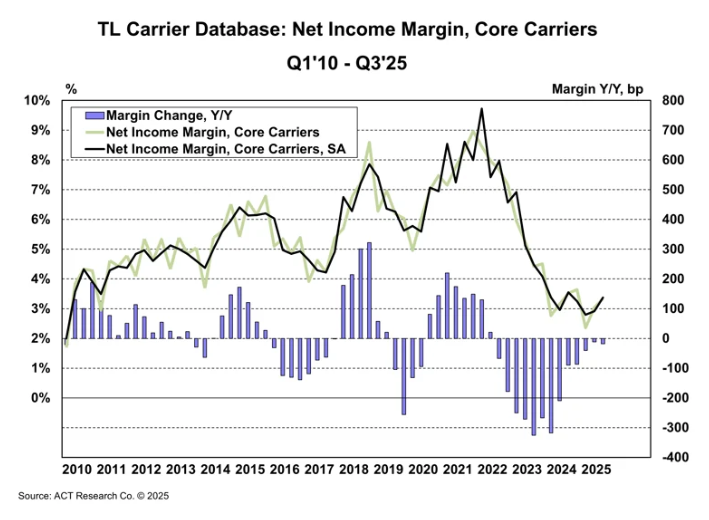

- The freight market remains weak, with TL carrier margins hitting a 15-year low in Q1 and continued pressure from trade-related demand shifts.

-

The Cass Freight Shipments Index fell -2.1% MoM and -5.3% YoY in March, slightly higher from a -5.5% YoY decline in February.

- The decline on the month was a result of shipments falling back from a February bounce that was a result of bad weather in January and an increase in activity ahead of tariffs.

- The recent 90-day pause on most reciprocal tariffs will likely lead to more pre-tariff shipping in Q2. However, this will contend with adverse effects from the extreme tariffs on China at this writing, and other tariffs.

- Volumes may also be temporarily supported in the coming months as consumers scoop up pre-tariff goods before prices go up. But thereafter, the trade war is likely to extend the for-hire freight recession as higher prices reduce goods affordability and consumers’ real incomes.

The Cass Freight Expenditures Index (total amount spent on freight) grew 1.5% MoM but were still down -2.0% YoY in March, up from -4.6% YoY in February.

- The increase in spending came even though shipments fell, suggesting that freight costs increased significantly.

- The Cass Inferred Freight Rates measure was up 3.7% MoM and 3.5% YoY in March, up from 1.0% YoY in February.

- After a -7% decline in 2024, freight rates are starting 2025 on track for low- to mid-single-digit increases in 2025.

- The Cass Truckload Linehaul Index fell -0.1% MoM in March, after six straight small increases. The index was up 1.5% YoY (up from 1.9% YoY previously) and 4.7% above that August low in March.