Canada GDP

Canada GDP

- Source

- Statistics Canada

- Source Link

- https://www150.statcan.gc.ca/

- Frequency

- Monthly

- Next Release(s)

- April 30th, 2026 8:30 AM

-

May 29th, 2026 8:30 AM

-

June 30th, 2026 8:30 AM

-

July 31st, 2026 8:30 AM

-

August 28th, 2026 8:30 AM

-

September 29th, 2026 8:30 AM

-

October 30th, 2026 8:30 AM

-

November 30th, 2026 8:30 AM

-

December 23rd, 2026 8:30 AM

-

January 29th, 2027 8:30 AM

-

March 1st, 2027 8:30 AM

-

March 31st, 2027 8:30 AM

Latest Updates

-

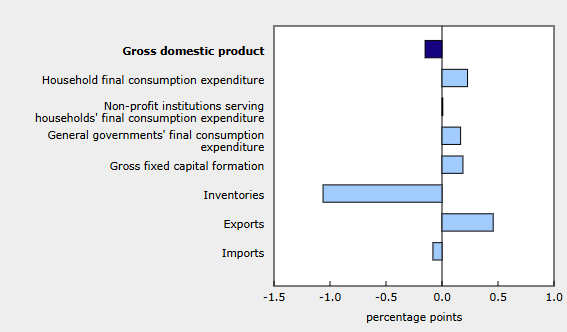

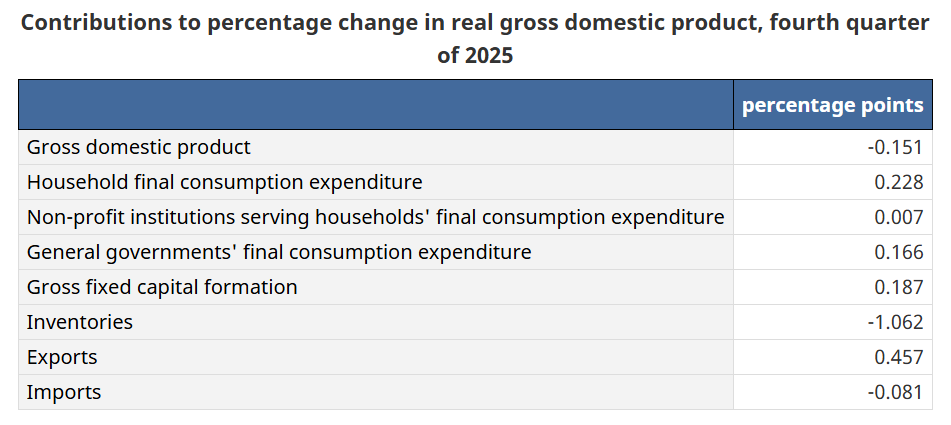

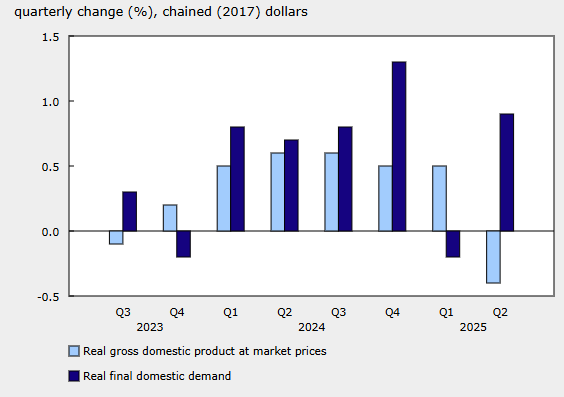

Canada’s real GDP declined -0.2% QoQ in Q4 2025 after +0.6% in Q3, as inventory withdrawals offset stronger spending and trade.

-

Businesses withdrew from non farm inventories in Q4 following two quarters of accumulation, with the largest reductions in manufacturing and wholesale trade and falling motor vehicle inventories in retail.

-

Exports rose +1.5% QoQ (Q3: +0.9%) and imports +0.3% QoQ, though exports fell -1.7% YoY and imports -0.4% YoY in 2025, indicating weaker trade performance over the year.

-

Household spending increased +0.4% QoQ after -0.2%, supported by rent and financial services while goods spending declined for a second consecutive quarter.

-

Total capital investment grew +0.8% QoQ driven by government weapons systems spending, whereas business investment edged down -0.1% as residential and non residential investment both declined.

-

Residential investment fell QoQ led by ownership transfer costs (-2.4%), renovations (-1.3%), and new construction (-0.5%), though it increased for full year 2025.

-

The GDP deflator rose +0.7% QoQ following +0.9% in Q3, with export prices +1.6% and import prices +1.1% lifting terms of trade +0.5%.

-

Compensation of employees increased +0.5% QoQ and +3.9% YoY in 2025, the slowest annual rise since 2016 outside the pandemic period.

-

Corporate income rose +1.3% QoQ supported by mining and primary metals, partially offset by declines in energy, wholesale trade, and some manufacturing industries.

-

The household saving rate fell to 4.4% from 5.2% as disposable income rose +0.6% but spending increased +1.2%.

-

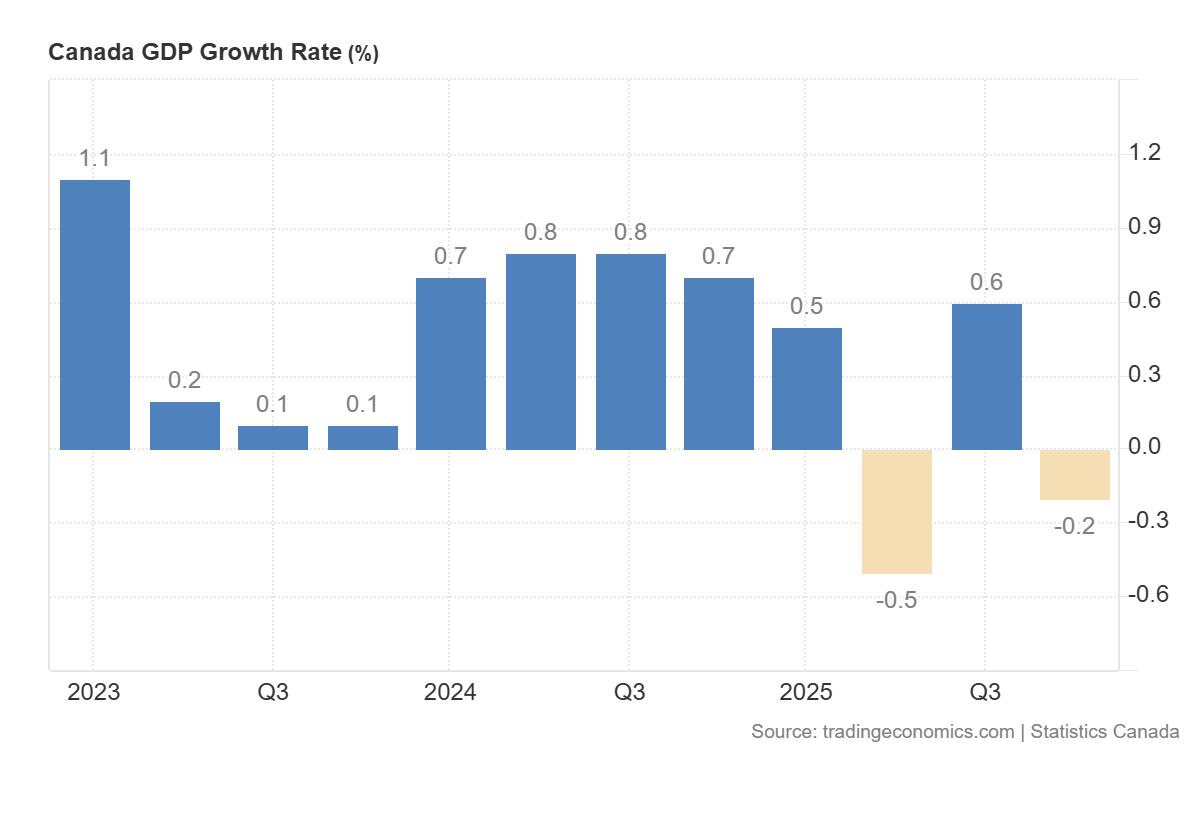

Real GDP rose +1.7% YoY in 2025, the slowest annual growth since 2020, largely due to weaker exports to the United States.

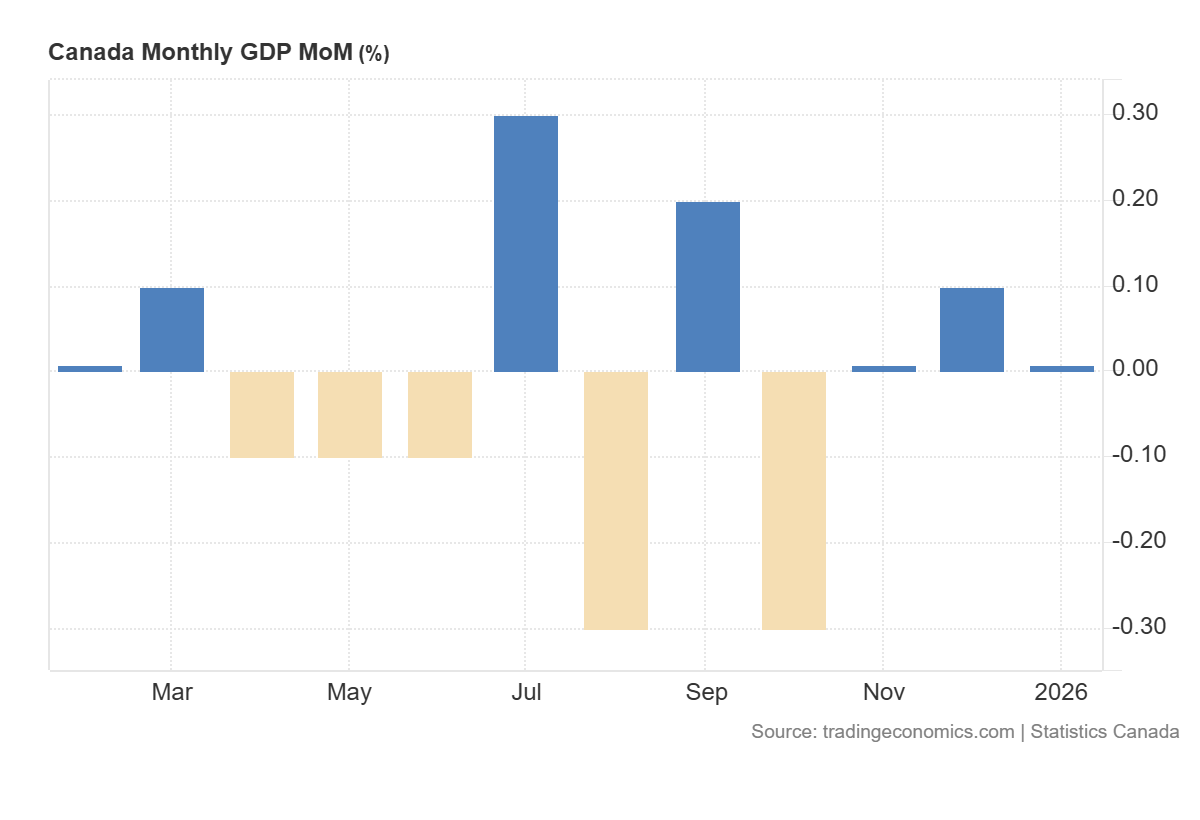

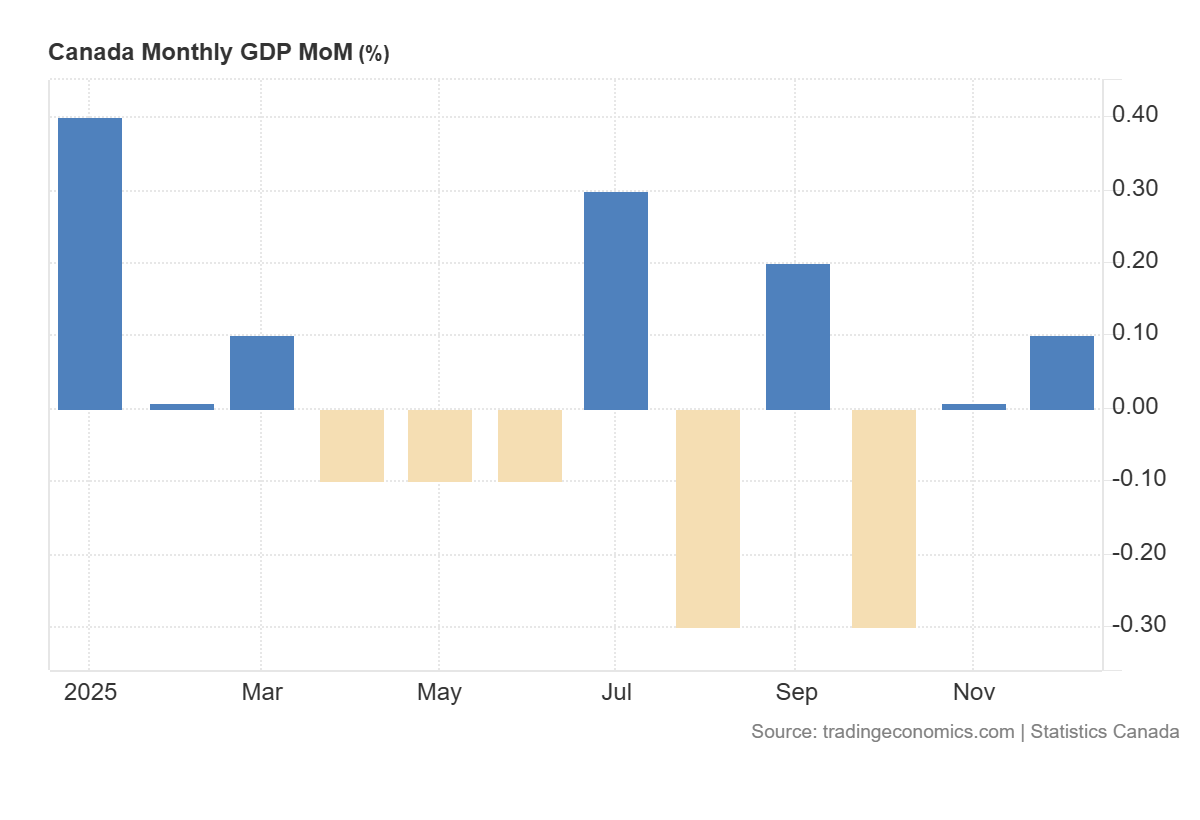

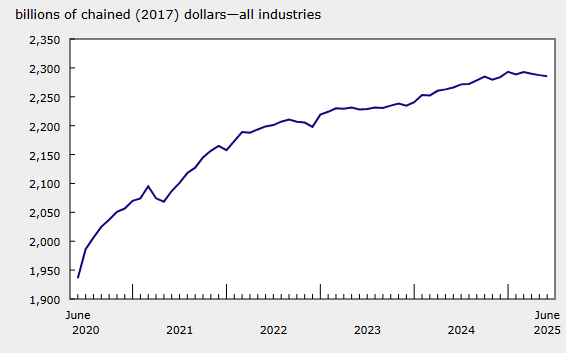

Canada’s real GDP rose +0.2% MoM in December while Q4 fell -0.1% QoQ and 2025 grew +1.6% YoY, showing mixed short and longer term momentum.

-

The advance estimate for January 2026 GDP growth is +0.0% MoM, as increases in mining, quarrying, and oil and gas extraction and finance and insurance were offset by decreases in manufacturing and real estate and rental and leasing.

-

Services-producing industries increased +0.2% MoM and goods-producing industries +0.2% MoM in December, with 11 of 20 sectors expanding.

-

Manufacturing rose +1.2% MoM after two monthly declines, including durable goods +1.8% and non-durable goods +0.5%, indicating a rebound at year end.

-

Wholesale trade grew +1.7% MoM led by motor vehicle wholesalers +10.9%, largely reversing November weakness tied to semiconductor shortages.

-

Utilities expanded +2.7% MoM and transportation and warehousing +0.7% MoM, reflecting broad-based services strength.

-

Mining, quarrying, and oil and gas extraction fell -0.9% MoM, with oil and gas extraction down -1.1%, offsetting some monthly gains.

-

GDP by industry declined -0.1% QoQ in Q4 as manufacturing fell -1.5% and educational services dropped -1.7%, partly offset by health care +0.7% and public administration +0.5%.

-

Real GDP by industry increased +1.6% YoY in 2025, the slowest pace in five years, with services +1.6% and goods +1.5%.

-

Finance and insurance rose +4.0% YoY while mining, quarrying, oil and gas extraction increased +4.0%, whereas manufacturing declined -2.6% YoY for a third consecutive year.

-

-

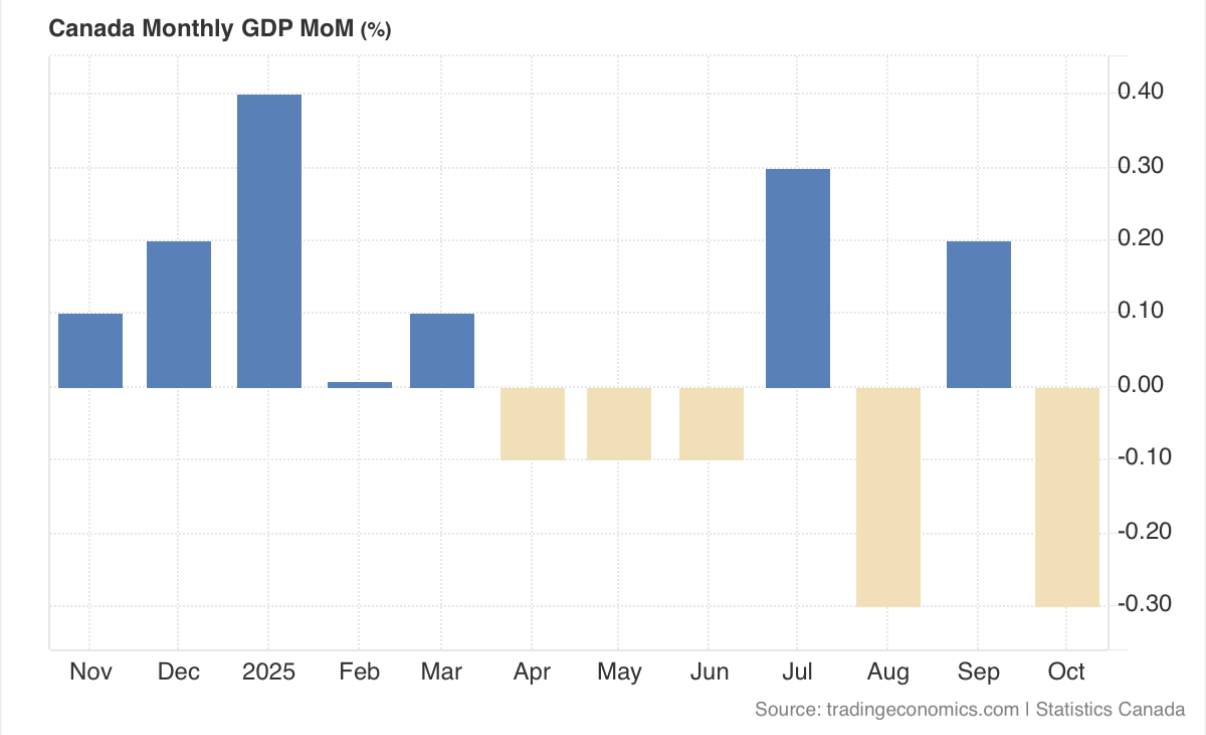

Canada’s real GDP was flat in November 2025 (0.0% MoM after -0.3% MoM in October), with goods-sector contractions offset by services growth amid uneven industry performance.

- The advance estimate shows GDP up +0.1% MoM in December, placing Q4 2025 growth at -0.1% QoQ and full-year 2025 growth at +1.3%, indicating weak late-year momentum despite modest annual expansion.

-

Goods-producing industries declined -0.3% MoM, driven by weakness in manufacturing and agriculture, forestry, fishing and hunting, while services-producing industries edged up +0.1% MoM, leaving overall output unchanged.

-

The manufacturing sector fell -1.3% MoM, with durable goods down -1.9% and non-durable goods down -0.8%, indicating broad-based factory weakness.

-

Within durables, transportation equipment manufacturing dropped -3.8%, including motor vehicles and parts at -6.4%, reflecting production constraints tied to the semiconductor shortage.

-

Non-durable manufacturing was pulled lower by food manufacturing (-1.6%) and plastics and rubber products (-3.7%), partly offset by chemical manufacturing (+1.9%) and petroleum and coal products (+0.2%).

-

Wholesale trade contracted -2.1% MoM, the largest drop since April 2025, led by a -12.6% plunge in motor vehicle and parts wholesaling, aligning with weaker auto production.

-

Retail trade rebounded +1.3% MoM, with all subsectors expanding, including a +2.5% rise in food and beverage retailers, reversing prior monthly declines.

-

Transportation and warehousing rose +0.9% MoM, supported by a +41.7% rebound in postal services after labor disruptions and gains in warehousing (+2.7%) and pipeline transportation (+1.4%).

-

Canada’s real GDP fell -0.3% MoM in October 2025, reversing September’s +0.2% gain amid broad-based sectoral weakness.- An advance estimate points to +0.1% MoM growth in November, suggesting stabilization after October’s contraction.

- Goods-producing industries declined -0.7% MoM, led by a sharp pullback in manufacturing, while services-producing industries fell -0.2% MoM, partly reflecting labor disruptions.

- Manufacturing output dropped -1.5% MoM, fully offsetting September’s expansion, with durable goods down -2.3% and machinery manufacturing plunging -6.9%.

- Wood product manufacturing fell -7.3%, its largest decline since April 2020, driven by sawmills (-9.0%) following the announcement of additional U.S. tariffs on Canadian lumber.

- Non-durable manufacturing decreased -0.4% MoM, led by chemicals (-3.4%), while petroleum and coal products rose +2.5%, partially cushioning the sector.

- Mining, quarrying, and oil & gas extraction declined -0.6% MoM, as oil sands extraction fell -2.7% amid maintenance, offset in part by gains in non-oil mining (+2.6%).

- Transportation and warehousing contracted -1.1% MoM, driven by a -32.1% drop in postal services due to ongoing labor strikes.

- Retail trade fell -0.6% MoM for a second straight month, led by food and beverage retailers (-2.3%) and gasoline stations (-1.0%), while housing-related retail segments posted modest gains.

-

Canada’s real GDP rose +0.6% QoQ in Q3 2025 (after -0.5% in Q2), marking a rebound driven primarily by a stronger trade balance as imports fell sharply and exports edged higher.

-

Imports dropped -2.2% QoQ, the largest decline since Q4 2022, reflecting lower inflows of precious metals and industrial machinery after unusually strong Q2 volumes.

-

Exports increased +0.2% QoQ (after -7.0% in Q2), supported by crude oil and bitumen (+6.7%) and commercial services (+1.7%), while precious metal exports declined.

-

Government capital investment rose +2.9% QoQ, led by an +82.0% surge in spending on weapon systems and additional investment in non-residential structures such as hospitals.

-

Business capital investment was flat overall, as gains in residential structures (+1.6%) and engineering structures (+0.2%) were offset by declines in machinery and equipment (-2.7%) and non-residential buildings (-1.5%).

-

Residential investment grew on ownership transfer costs (+9.1%) and renovations (+1.2%), while new construction fell -0.8% due to broad declines in apartment building activity.

-

Household final consumption slipped -0.1% QoQ, with vehicle purchases down -2.3% and spending abroad falling -3.9%, partly offset by higher expenditures on rent and financial services.

-

Government final consumption contracted -0.4% QoQ, the first decline since late 2023, reflecting lower federal spending following election-related outlays in Q2.

-

The GDP deflator rose +0.8% QoQ, driven by higher export prices (+1.6%), improving Canada’s terms of trade by +1.0%, the strongest gain since Q3 2023.

-

Compensation of employees increased +1.1% QoQ, with wage gains across nearly all industries and provinces; New Brunswick saw the fastest growth (+1.7%).

-

The household saving rate rose to 4.7% as disposable income (+0.8%) outpaced nominal consumption (+0.7%), helped by higher wage, self-employment, and dividend income and lower interest payments.

-

Corporate income increased +2.5% QoQ, supported by higher energy production, stronger mining sector earnings, improved refined energy product sales, and continued gains among financial corporations.

Canada’s real GDP rose +0.2% MoM in September 2025 (after -0.1% in August), marking a modest rebound led by goods-producing industries and a broad pickup in manufacturing.

-

Goods-producing industries increased +0.6% MoM, while services edged up +0.1%, with 10 sectors expanding and manufacturing providing the largest boost.

-

Manufacturing output rose +1.6% MoM, driven by durable goods (+2.1%) and non-durable goods (+1.0%); machinery and wood products each gained +5.5%, and motor vehicles and parts climbed +3.7% as Ontario auto plants resumed production.

-

Transportation and warehousing rebounded +1.2% MoM (after -1.3% in August), as air transportation surged +6.0% following the end of a flight attendants’ strike, and support activities rose +2.2%.

-

Oil and gas extraction increased +0.9% MoM, its fourth consecutive gain, with oil sands output up +1.3% and conventional extraction up +0.5%; support activities for extraction rose +1.6%.

-

Mining and quarrying excluding oil and gas fell -2.2% MoM, led by non-metallic minerals (-3.9%) and potash (-4.9%), partly offsetting sector gains.

-

Wholesale trade rose +0.6% MoM, supported by building materials (+3.4%) and food, beverage, and tobacco wholesaling (+1.6%).

-

Retail trade declined -0.7% MoM, weighed by motor vehicle and parts dealers (-2.1%), general merchandise (-1.1%), building and garden equipment (-1.1%), and gasoline stations (-1.0%).

-

Construction fell -0.2% MoM, as residential building dropped -1.4%, while engineering construction (+1.2%) and non-residential building (+0.1%) provided partial offsets.

-

The advance estimate for October 2025 points to a -0.3% MoM decline, with decreases in oil and gas extraction, educational services, and manufacturing partly offset by gains in mining and support services.

-

-

Canada’s real GDP fell -0.3% MoM in August 2025, reversing July’s +0.3% gain, as both goods-producing and services-producing industries contracted amid widespread declines across key sectors.

-

Statistics Canada’s advance estimate points to a +0.1% GDP increase in September, implying roughly +0.1% growth for Q3 2025 overall.

-

Goods-producing industries dropped -0.6% MoM, marking the fifth decline of the year, while services-producing industries edged down -0.1% for the first time in six months.

-

Transportation and warehousing fell -1.7% MoM, led by air transportation (-4.6%), which saw its largest drop since January 2022 due to a mid-month flight attendants’ strike affecting 10,000 workers.

-

Wholesale trade declined -1.2%, the first drop in four months, driven by motor vehicle and parts wholesalers (-8.3%) and food, beverage, and tobacco wholesalers (-5.2%).

-

Mining, quarrying, and oil & gas extraction fell -0.7%, weighed down by lower drilling (-5.0%) and mining activity (-1.3%), though oil & gas extraction rose slightly (+0.2%) for a third month.

-

The utilities sector contracted -2.3%, its sixth straight monthly decline, as drought conditions reduced hydroelectric generation.

-

Manufacturing output fell -0.5%, with durable goods (-0.8%) led by machinery (-2.8%) and fabricated metals (-2.4%), while primary metals rose +3.7% on stronger aluminum exports.

-

Retail trade expanded +0.9%, its second consecutive gain, driven by auto dealers (+2.5%), clothing stores (+2.7%), and sporting goods retailers (+6.9%).

-

-

Canada’s real GDP rose +0.2% MoM in July 2025, the first increase in four months, driven by a rebound in goods-producing industries and steady gains in services.

-

Statistics Canada’s advance estimate suggests GDP was flat in August, with retail and wholesale gains offset by declines in mining, manufacturing, and transportation.

-

Goods-producing industries expanded +0.6% MoM, with all sectors contributing after three straight months of contraction.

-

Mining, quarrying, and oil & gas grew +1.4% MoM, led by metal ore mining (+2.6%) and oil sands extraction (+1.2%) as production ramped up post-maintenance.

-

Transportation & warehousing rose +0.6% MoM, supported by pipeline transportation (+2.8%) and higher LNG-related activity at Kitimat.

-

Manufacturing increased +0.7% MoM, with durable goods up +1.0% on strong motor vehicle (+9.1%) and parts (+10.5%) output, while primary metals fell -5.5% amid weaker steel exports under new U.S. tariffs.

-

Non-durable manufacturing rose +0.4% MoM, driven by chemical products (+4.8%) and pharmaceuticals (+12.6%).

-

Wholesale trade climbed +0.6% MoM, its third monthly gain, boosted by motor vehicles (+5.4%) and building materials (+2.5%).

-

Real estate & rental leasing rose +0.3% MoM, with home resale activity (+3.6%) in Ontario and B.C. driving a second consecutive record high.

-

Retail trade fell -1.0% MoM, weighed by food & beverage (-2.0%), clothing (-3.4%), and sporting goods (-8.2%), though non-store retailers rose +2.4%.

-

-

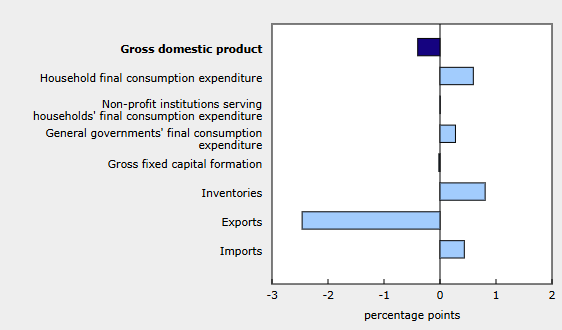

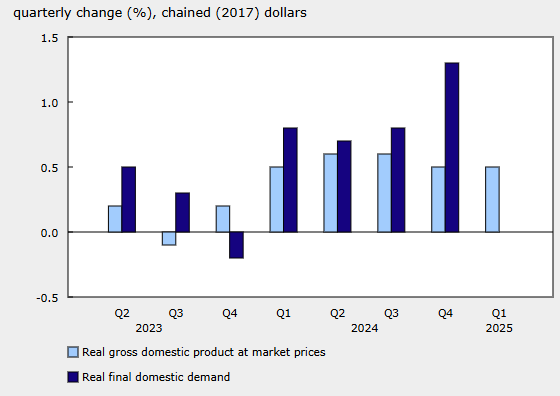

Canada’s real GDP contracted -0.4% QoQ in Q2 2025 (vs +0.5% in Q1), while annual growth slowed to +0.4% YoY, as weaker exports and business investment outweighed gains in household spending and inventories. Growth at an annualized rate was -1.6%, well below the forecast of -0.6%.

-

Exports fell -7.5% QoQ, led by sharp declines in passenger vehicles (-24.7%), industrial machinery (-18.5%), and travel services (-11.1%), reflecting the impact of US tariffs.

-

Imports declined -1.3% QoQ, with vehicle imports down -9.2% and travel services -8.5%, partly offset by a +35.8% surge in intermediate metal imports.

-

Business investment dropped -0.6% QoQ, with machinery and equipment plunging -9.4% (worst since 2016 outside 2020), while non-residential buildings fell -3.3%; engineering structures rose +3.6% on a large offshore oil project delivery.

-

Household consumption rebounded +1.1% QoQ, supported by autos (+5.6%), food (+0.9%), and services, though electricity (-3.2%) and alcohol (-3.9%) declined.

-

Residential investment rose +1.5% QoQ on new construction (+3.7%) and resale activity (+1.0%), though renovations fell -1.1%.

-

The household saving rate fell to 5.0% (from 6.0% in Q1), as weak income growth (+0.3% QoQ) lagged consumption (+1.2% QoQ).

-

Corporate operating surplus declined -1.9%, dragged by lower energy sector earnings, while financial corporations posted modest gains.

-

Federal government net borrowing increased, with revenue down -4.2% after the carbon tax removal, while expenditures rose +1.8% on higher goods/services purchases and settlement payments.

Canada’s real GDP edged down -0.1% MoM in June 2025, the third consecutive monthly decline, as contractions in goods-producing industries outweighed modest gains in services. An advance estimate points to a +0.1% rebound in July.

-

Goods-producing industries contracted -0.5% MoM, led by manufacturing (-1.5%) and utilities (-1.2%); 11 of 20 sectors overall saw declines.

-

Durable manufacturing dropped -2.1% MoM, with motor vehicles (-12.6%), wood products (-4.3%), and transportation equipment (-4.4%) hit by US tariffs and weak exports.

-

Non-durable manufacturing fell -0.7% MoM, led by chemicals (-10.4%) and pharmaceuticals (-20.7%); petroleum products rebounded +11.0% as refineries resumed activity.

-

Services rose +0.1% MoM, supported by retail trade (+1.4%), wholesale trade (+0.5%), and real estate (+0.3%), though public sector activity softened.

-

Oil and gas extraction rebounded strongly (+2.6% MoM, with oil sands +6.4%), offsetting declines in natural gas (-1.0%) and support activities (-9.7%).

-

Construction grew +0.3% MoM on residential building (+1.6%), while non-residential (-1.0%) and engineering (-0.4%) weighed on overall activity.

-

-

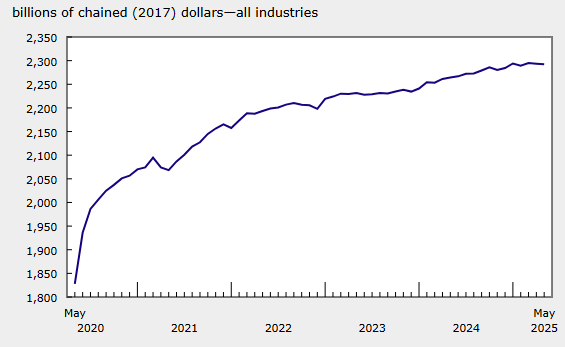

Canada’s real GDP fell -0.1% MoM in May 2025, marking a second straight monthly contraction, as weakness in mining and retail offset gains in manufacturing and real estate.

- Manufacturing rebounded +0.7% MoM, with durable goods up +1.2% and non-durables up +0.2%, led by strong gains in chemicals and fabricated metals.

- Mining, quarrying, and oil & gas declined -1.0% MoM; oil sands extraction fell -3.0% due to maintenance disruptions.

- Retail trade fell -1.2% MoM, dragged down by motor vehicle & parts (-4.8%), food & beverage (-2.5%), and gas stations (-3.1%).

- Real estate and rental & leasing rose +0.3% MoM, with resale activity (+3.5%) recovering for a second straight month.

- Public sector output declined -0.2% MoM, driven by a -3.2% drop in federal government activity post-election.

- StatsCan’s advance estimate shows a +0.1% MoM rebound in June 2025, suggesting flat GDP for Q2 overall.

-

Canada’s real GDP fell -0.1% MoM in April, reversing the 0.2% gain in March, as sharp declines in manufacturing and wholesale trade outweighed modest strength in services and public sector activity.

- Manufacturing dropped -1.9% MoM, the steepest since April 2021, with declines across both durable (-2.2%) and non-durable (-1.6%) goods; transportation equipment and petroleum products were key drags.

- Wholesale trade declined -1.9% MoM, its worst performance since June 2023, led by a -6.8% fall in motor vehicle wholesaling.

- Finance and insurance rose 0.7% MoM, driven by a 3.5% jump in investment services amid volatile equity market activity linked to U.S. tariff announcements.

- Public sector output increased 0.4% MoM, with a 2.2% rise in federal government activity tied to the Canadian election.

- Arts, entertainment and recreation surged 2.8% MoM, aided by strong spectator sports attendance during the NHL playoffs.

- Real GDP is expected to decline another -0.1% MoM in May 2025, with weakness in mining, public administration, and retail trade partly offset by gains in real estate and leasing.

-

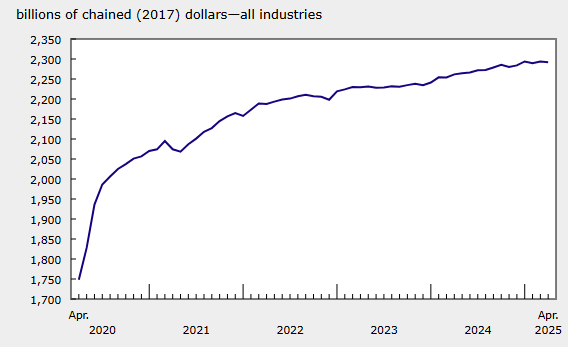

Canada’s real GDP grew 0.5% QoQ in Q1 2025, matching Q4 2024’s pace, driven by goods exports and business non-farm inventory accumulation, while final domestic demand was flat.

- GDP growth on an annualized basis was 2.2%, above expectations of a 1.7% gain.

- Exports rose 1.6% QoQ, led by passenger vehicles (+16.7%) and industrial machinery (+12.0%), while imports rose 1.1% QoQ on tariff-anticipation stocking.

- Household spending slowed to 0.3% QoQ (0.1% per capita), with gains in rent and financial services offset by lower auto purchases.

- Government consumption fell -0.1% QoQ, the weakest since Q4 2023.

- GFCF fell -0.8% QoQ with both business and government fixed capital formation down -0.8% QoQ each.

- Residential investment declined -2.8% QoQ, led by a sharp -18.6% drop in ownership transfer costs, despite gains in new construction (+1.7%) and renovations (+0.5%).

- Business investment was mixed: non-residential structures fell -1.6%, intellectual property products declined -0.4%, but machinery and equipment surged +5.3%.

- Compensation of employees rose 0.8% QoQ, with fastest wage growth in Saskatchewan, Alberta, and B.C.; household saving rate fell to 5.7% as consumption outpaced income growth.

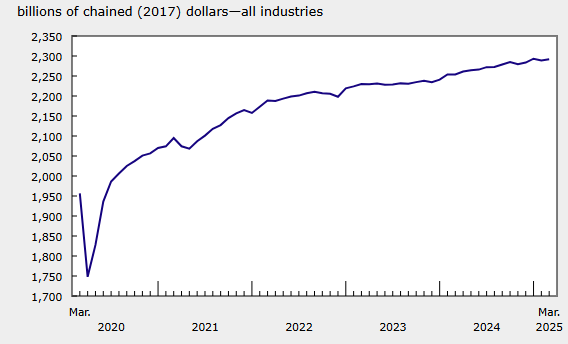

Canada’s real GDP rose 0.1% MoM in March 2025, partially recovering from a -0.2% decline in February, driven by gains in goods-producing sectors and select services. Advance estimates suggest another 0.1% GDP increase in April.

- Mining, quarrying, and oil & gas extraction jumped 2.2% MoM, with crude petroleum rebounding and coal mining surging 16.8%.

- Construction grew 0.5% MoM, led by residential (+1.3%) and non-residential (+1.5%) building construction.

- Manufacturing fell -0.4% MoM, as both chemical (-6.1%) and machinery (-3.8%) manufacturing declined, partially offset by transportation equipment (+3.1%).

- Retail trade rose 0.8% MoM, boosted by motor vehicle & parts dealers (+4.0%).

- Utilities declined -4.1% MoM due to milder weather lowering electricity demand.

-

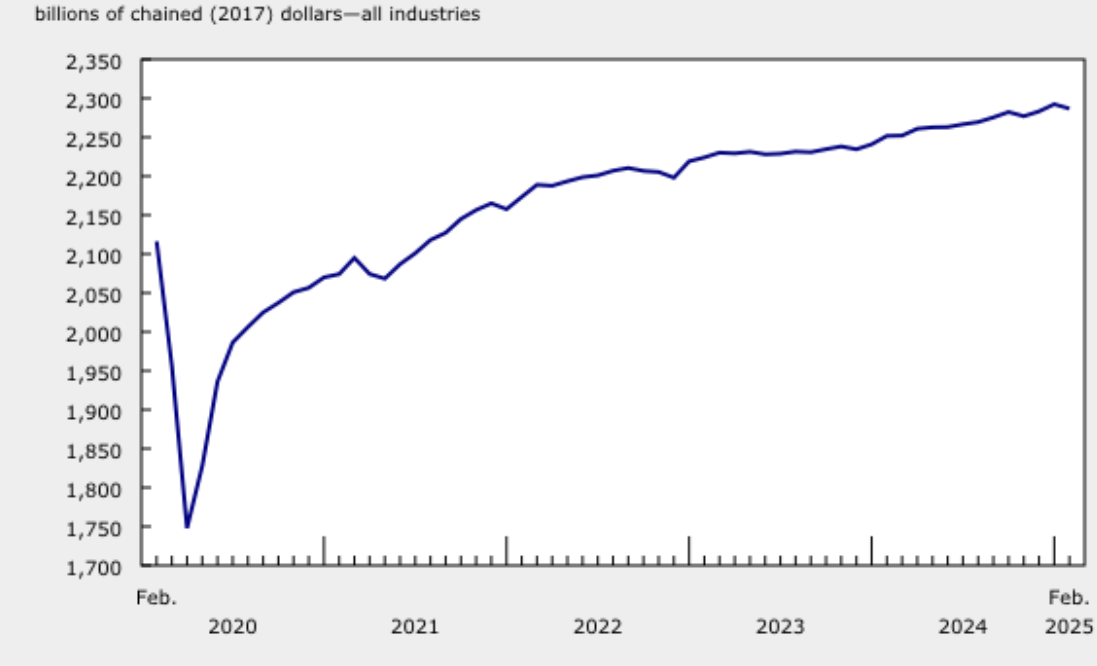

Canada’s GDP fell -0.2% MoM (vs 0.0% MoM expected) in February, partially offsetting the 0.4% MoM increase in January.

- After driving growth in January, goods-producing industries (-0.6% MoM) drove the decline in February, as mining, quarrying, and oil and gas extraction and construction contributed the most to the aggregate's decline.

- Services-producing industries edged down -0.1% MoM in February as contractions in transportation and warehousing and real estate and rental and leasing were partially offset by a rise in finance and insurance.

- Overall, 12 of 20 industrial sectors declined in February.

- The mining, quarrying, and oil and gas extraction sector was the largest detractor from growth, down -2.5% MoM.

- Advance information indicates that real GDP increased 0.1% MoM in March.