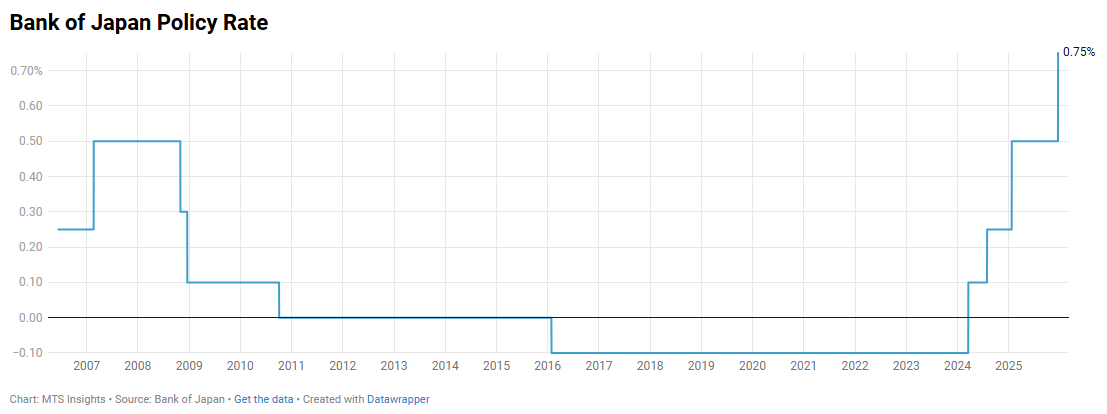

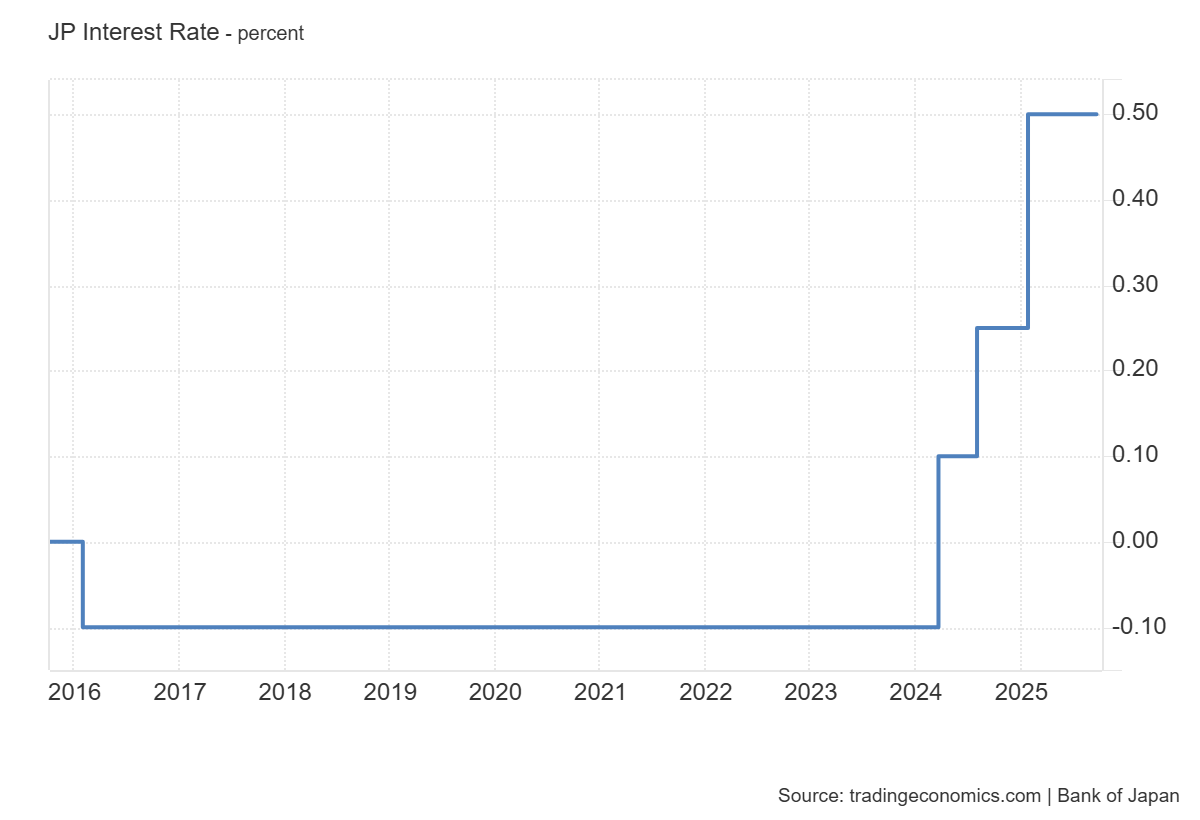

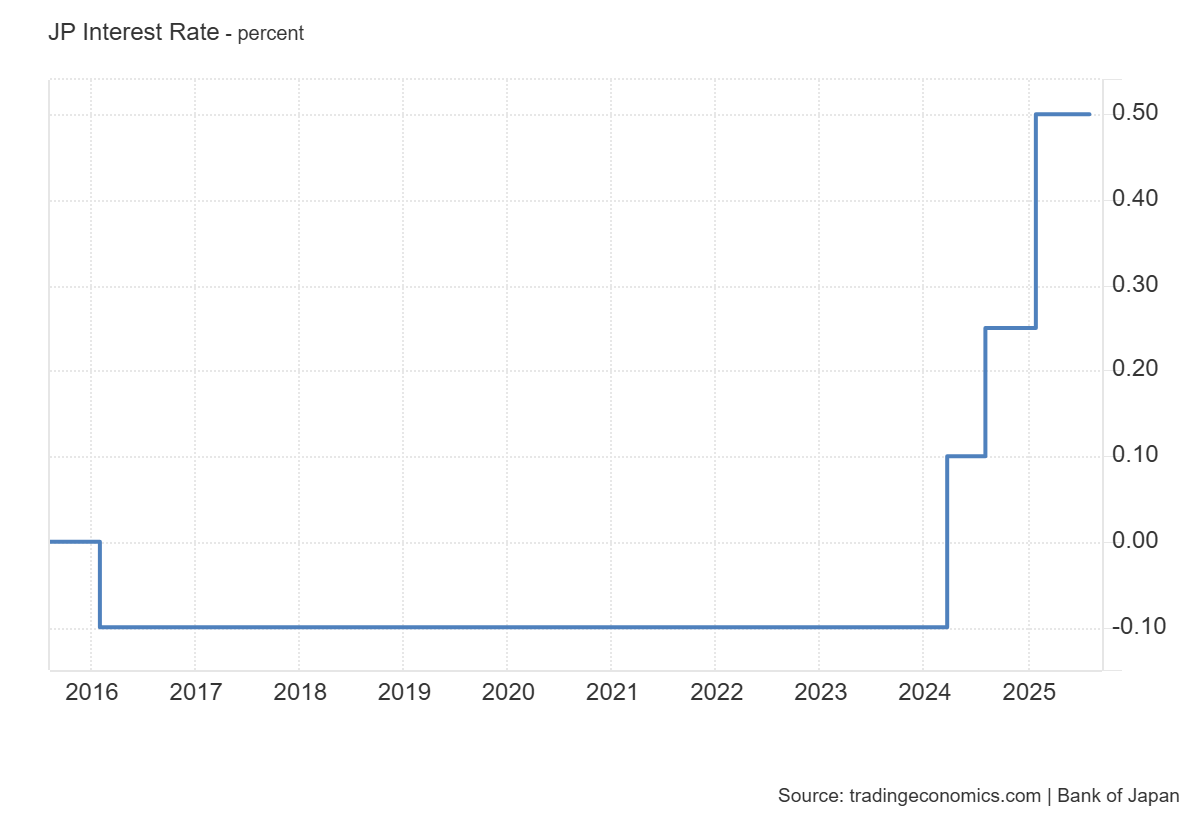

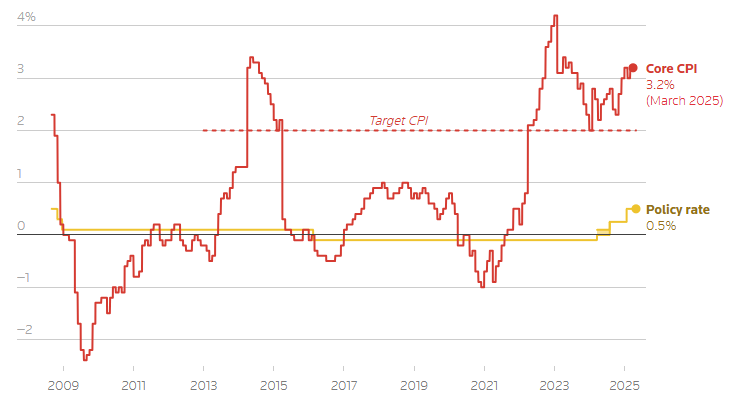

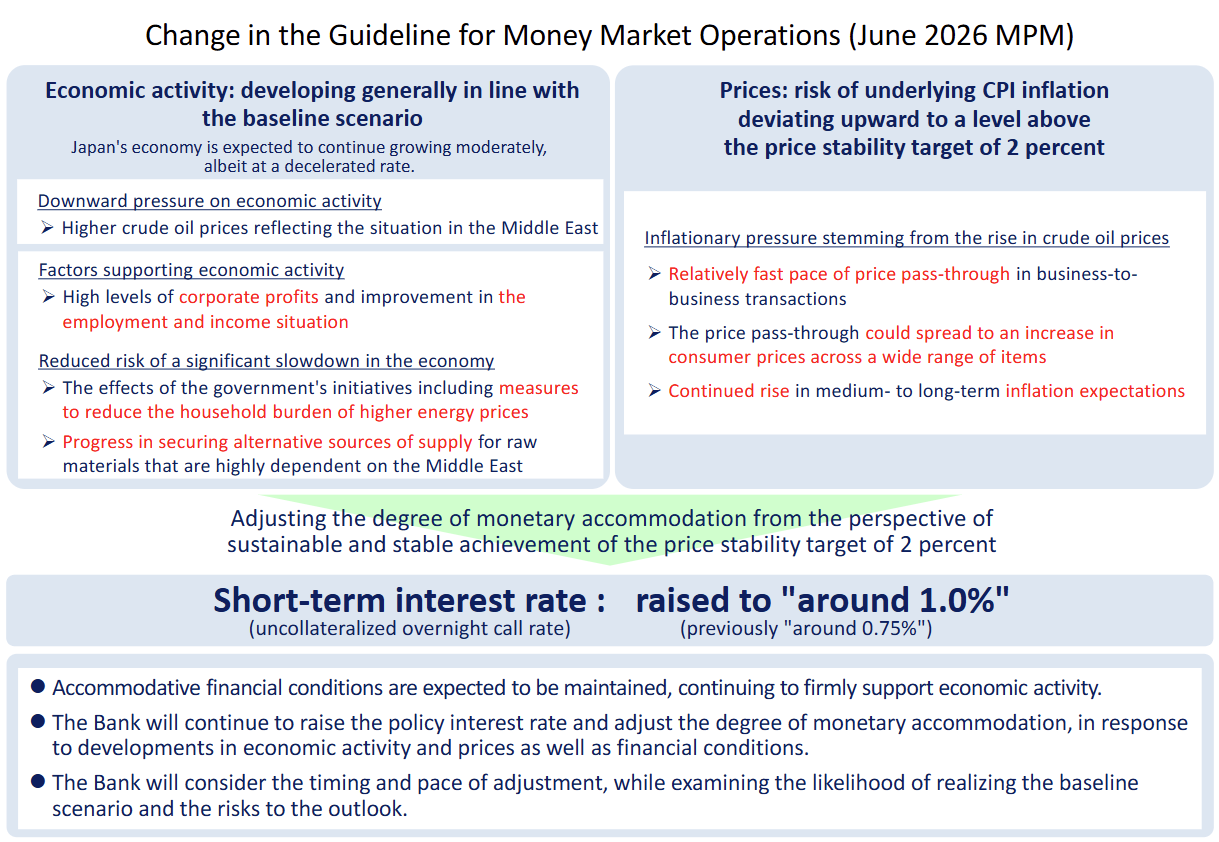

The Bank of Japan set the uncollateralized overnight call rate at around 1.0% while noting CPI (ex-fresh food) remains below 2% YoY and signaling a gradual tightening bias amid rising inflation risks and accommodative financial conditions.

- The BOJ decided by a 7–1 vote to guide the overnight call rate at ~1.0%, with the complementary deposit facility also set at 1.0% and the basic loan rate at 1.25%, indicating a policy adjustment toward less accommodation.

- Japan’s economy was described as recovering moderately, though with some weakness due to higher crude oil prices, suggesting continued expansion but with external cost pressures weighing on activity.

- Economic support factors included high corporate profits and improvements in employment and income conditions, indicating underlying resilience despite energy-related headwinds.

- The risk of a significant economic slowdown has decreased compared with earlier periods, reflecting government measures to offset energy costs and progress in securing alternative supply sources.

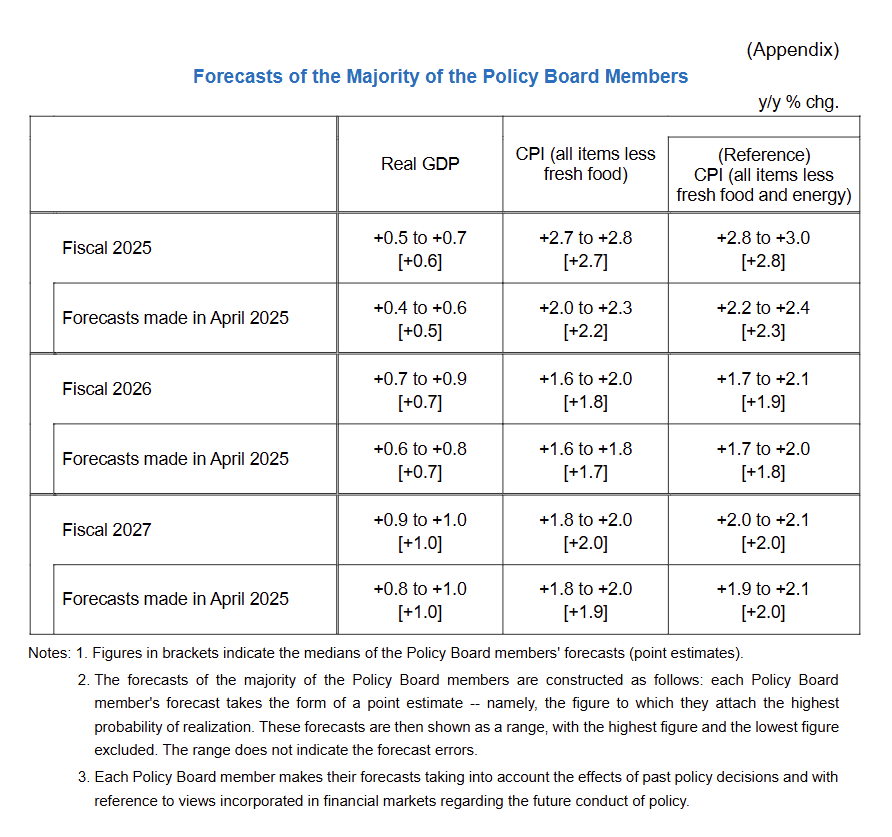

- CPI (ex-fresh food) inflation has been below 2% YoY recently, partly due to government measures to reduce household energy burdens, indicating subdued headline inflation in the near term.

- At the same time, upstream price pass-through from higher crude oil prices has been progressing relatively quickly, suggesting potential for broader increases in consumer prices over time.

- Medium- to long-term inflation expectations have continued to rise, with the BOJ noting a risk that underlying CPI inflation could exceed the 2% target, highlighting upward inflation risks.

- Financial conditions remain accommodative, with negative real interest rates and favorable corporate financing conditions, indicating continued support for economic activity even as policy is adjusted.

- The BOJ signaled it will continue raising the policy rate and adjusting accommodation in response to economic and price developments, reflecting a gradual normalization path while monitoring risks from the Middle East situation.