Bank of England Monetary Policy Decision

Bank of England Monetary Policy Decision

- Source

- Bank of England

- Source Link

- https://www.bankofengland.co.uk/

- Next Release(s)

- March 19th, 2026 7:00 AM

-

April 30th, 2026 7:00 AM

-

June 18th, 2026 7:00 AM

-

July 30th, 2026 7:00 AM

-

September 17th, 2026 7:00 AM

-

November 5th, 2026 7:00 AM

-

December 17th, 2026 7:00 AM

Latest Updates

-

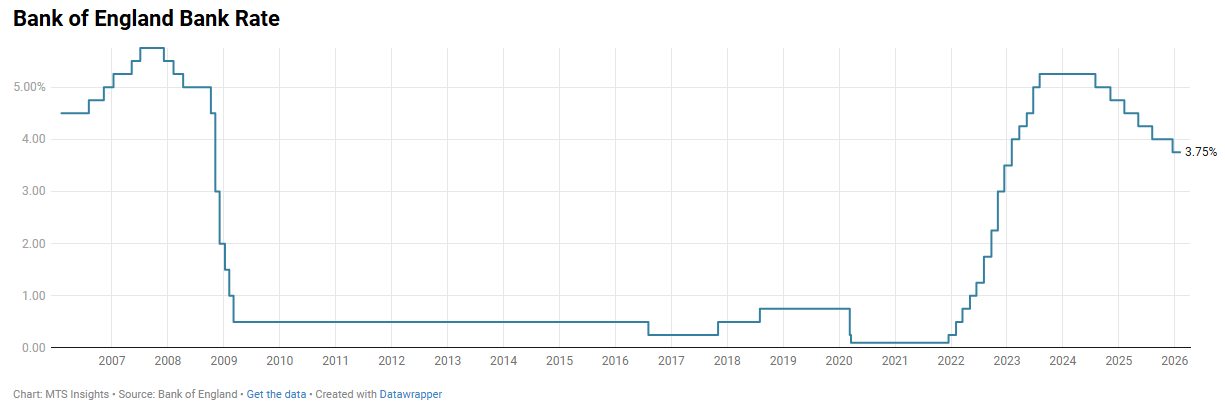

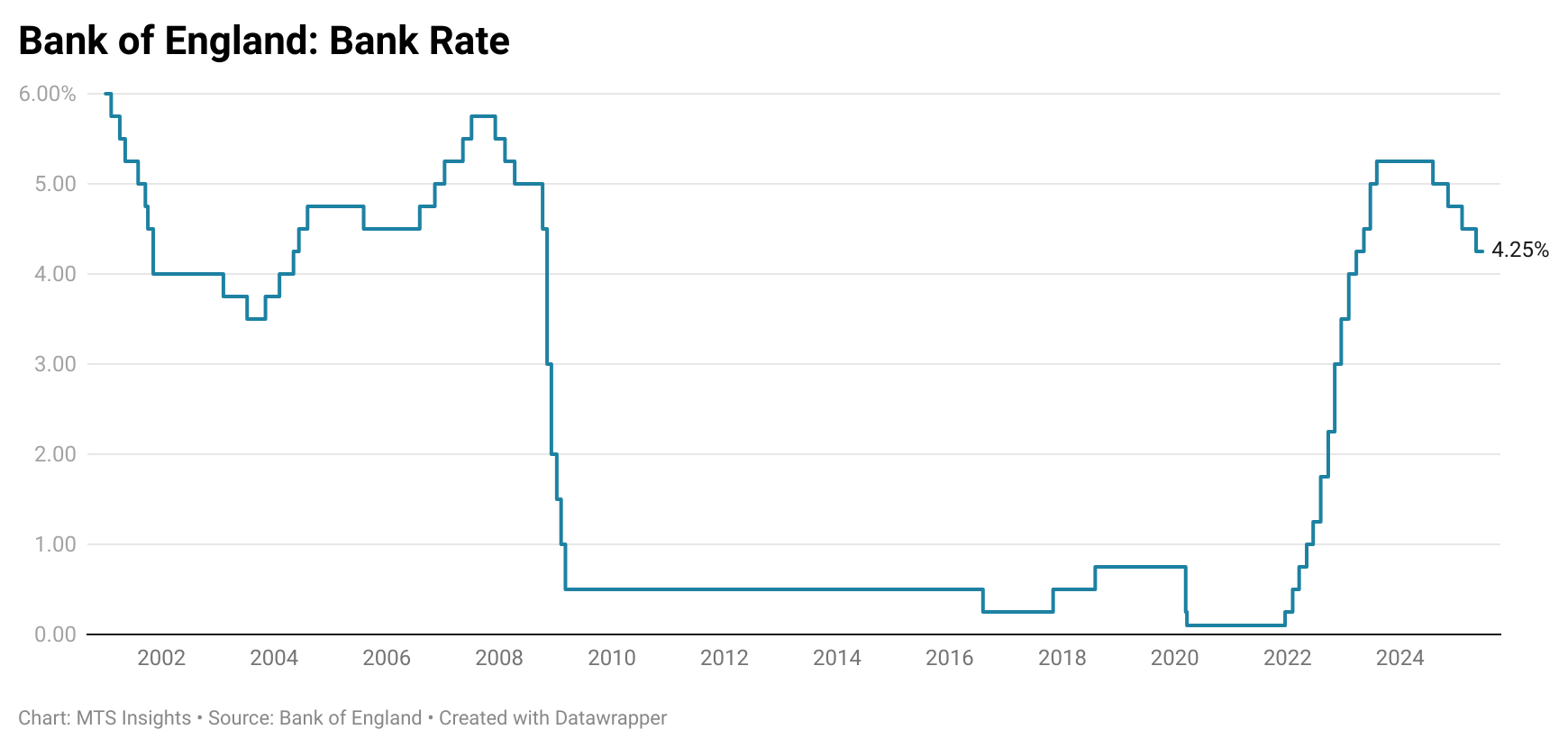

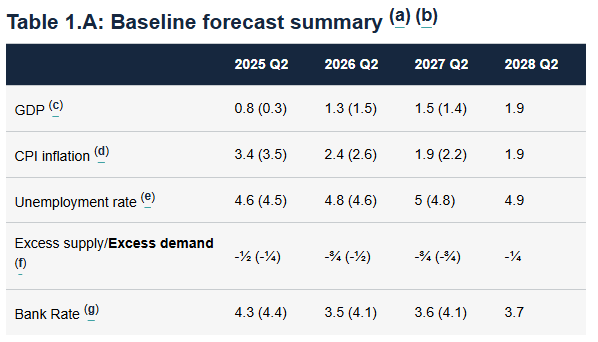

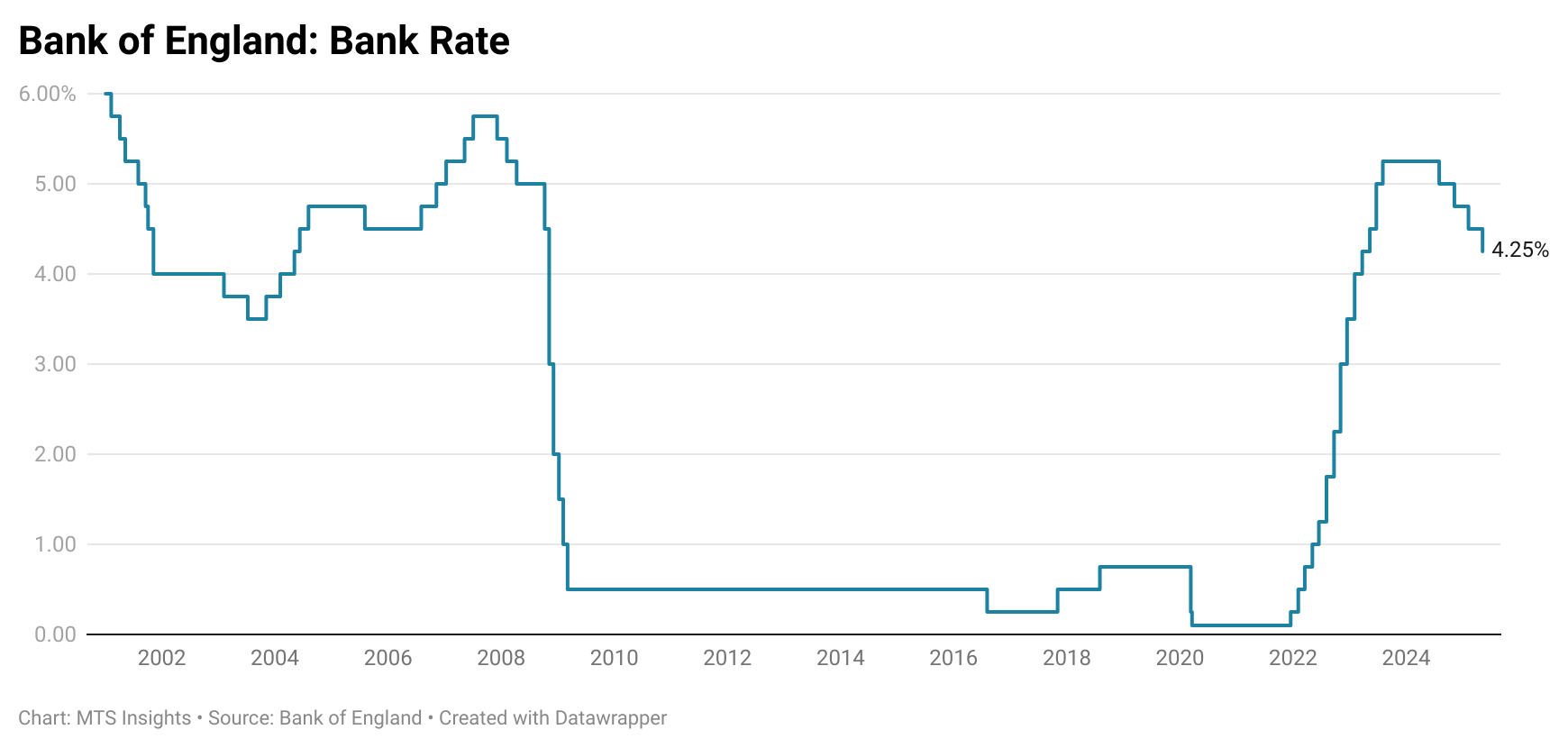

The Bank of England held Bank Rate at 3.75% in February 2026 on a 5–4 vote, reflecting easing inflation pressures but continued caution over persistence risks.

-

The MPC voted 5–4 to keep rates unchanged, with four members favoring a 25 bp cut to 3.5%, underscoring a close balance between disinflation progress and downside growth risks.

-

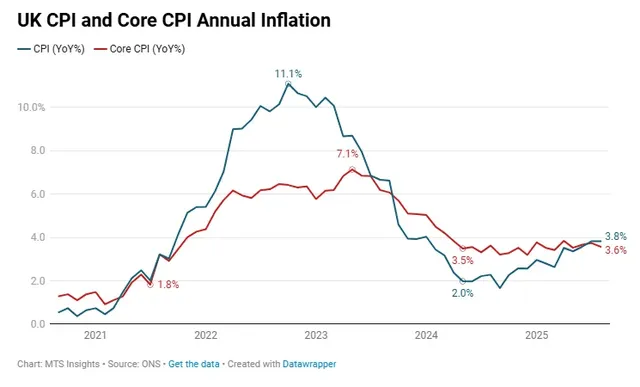

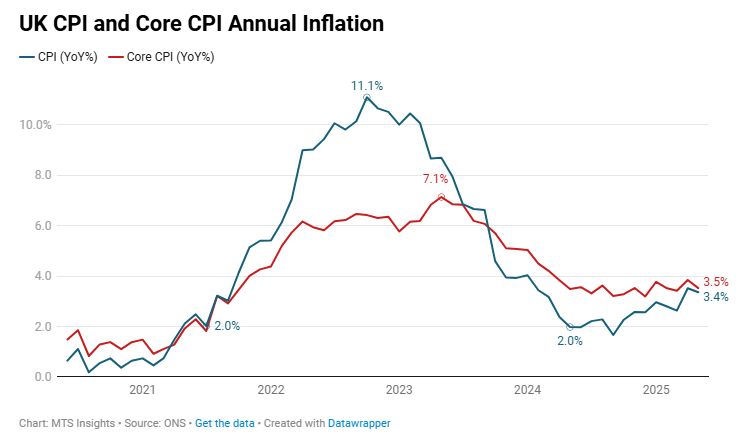

CPI inflation fell from 3.8% YoY in September to 3.4% YoY in December and was projected to return to around the 2% target from April, largely due to lower energy prices and Budget 2025 measures.

-

Pay growth and services price inflation continued to ease, though they remained above levels consistent with the inflation target, indicating underlying pressures were moderating but not fully normalized.

-

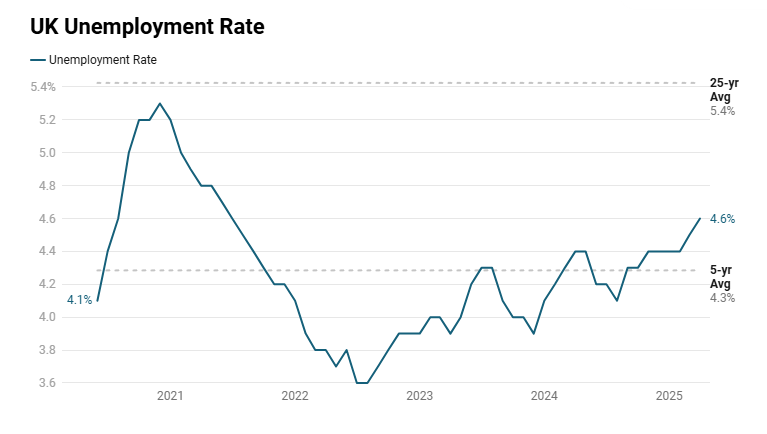

The labour market loosened further, with unemployment rising to just over 5% and underlying GDP growth staying below potential, leading staff to project a slightly wider output gap than in November.

-

The MPC assessed that risks from inflation persistence had become less pronounced, while risks from weaker demand and further labour market slack remained present.

-

Bank Rate has been reduced by 150 bps since August 2024, lowering the overall restrictiveness of policy while maintaining a stance aimed at anchoring inflation sustainably at 2%.

-

The Committee signaled that further rate cuts are likely but described future easing decisions as a “closer call,” with timing dependent on inflation and wage developments.

-

Market pricing implied a gradual decline in Bank Rate through 2026, while survey respondents expected rates to fall to around 3.25% and remain there, highlighting differing expectations for the easing path.

-

-

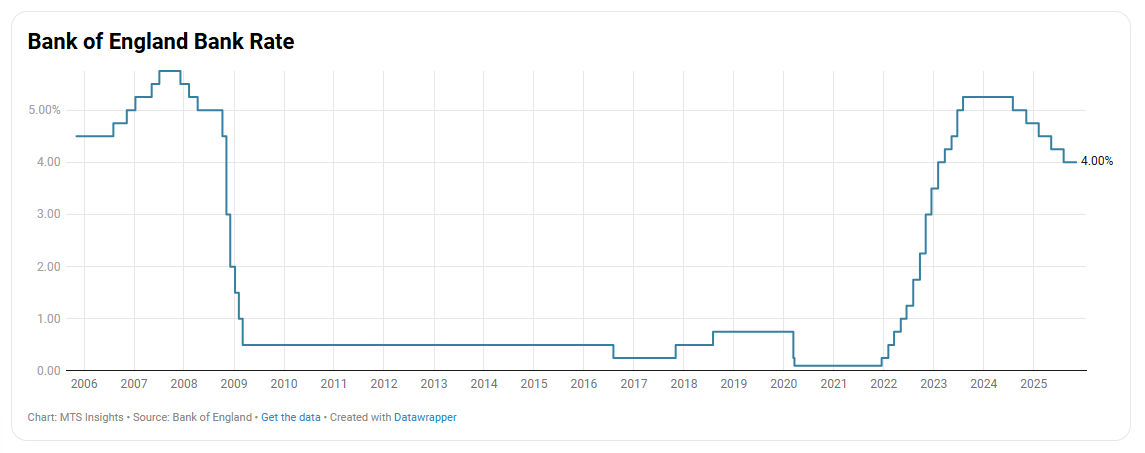

The Bank of England cut Bank Rate by 25 bps to 3.75% on a 5-4 vote, reflecting a slightly faster expected return of inflation toward target amid subdued growth and rising labour market slack.

-

The Bank Rate has fallen 150 bps since peaking in August 2023 after six quarter point cuts. The Rate is now the lowest at the lowest level since January 2023.

-

Vote split: 5 members supported the 25 bps cut to 3.75%, while 4 preferred to hold at 4.00%, highlighting a close balance between persistence risks and weaker-demand risks.

-

Inflation update: CPI eased to 3.2% YoY in November (from 3.6% in October and 3.8% in September) and was below the BoE’s short-term November MPR forecast, largely due to downside food-price news.

-

Near-term path: CPI was expected to fall further in 2026 Q1 to around 3%, with a temporary rise anticipated in December 2025 tied to tobacco duty and firmer airfares inflation.

-

Underlying pressures: Services inflation was 4.4% YoY in November (vs a 5.4% peak in April), with the BoE noting continued easing in pay growth and services inflation, though one-off factors earlier in the year still restrained the downtrend.

-

Labour market and wages: The LFS unemployment rate rose to 5.1% (three months to October), AWE whole-economy growth was 4.7% (three months to October), and private-sector regular pay growth was 3.9%, consistent with easing wage momentum alongside further loosening.

-

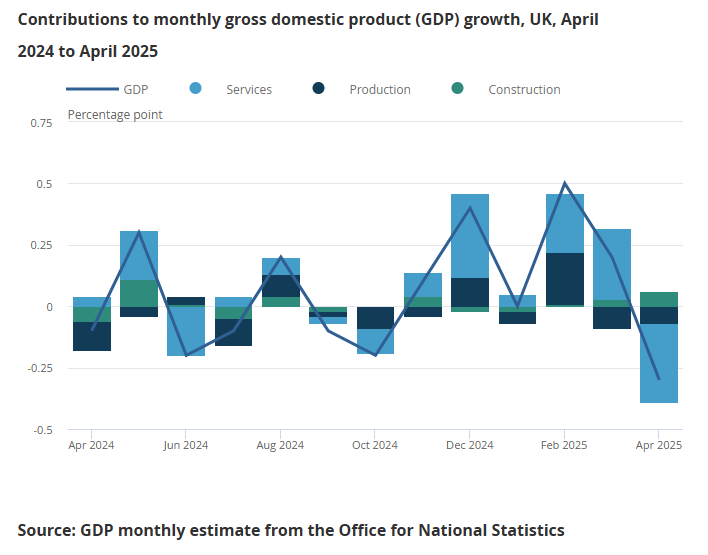

Growth backdrop: GDP growth slowed to 0.1% QoQ in 2025 Q3; monthly GDP fell -0.1% MoM in October, and staff expected 0.0% growth in 2025 Q4, underscoring subdued activity.

-

Risk balance and guidance: The MPC said inflation-persistence risk was “somewhat less pronounced,” while weaker-demand risks remained, and reiterated Bank Rate is likely to follow a “gradual downward path,” though future easing decisions were described as becoming a “closer call.”

-

-

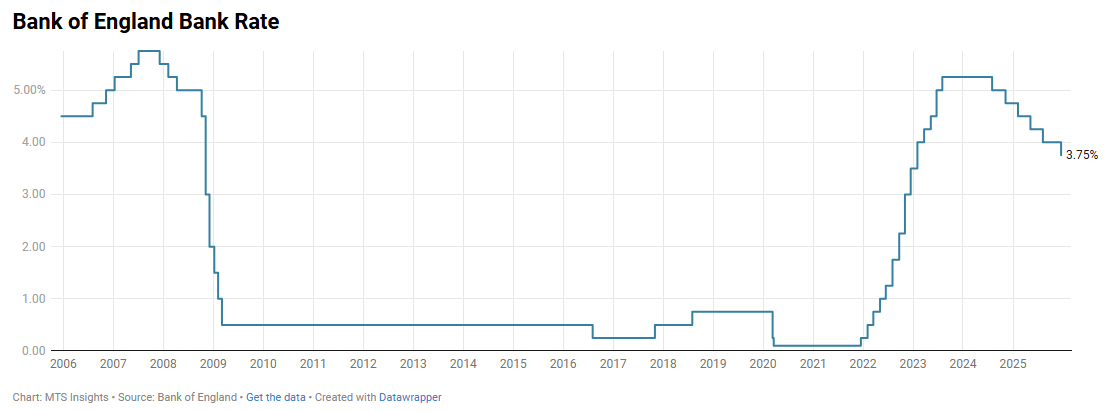

The Bank of England voted 5–4 to hold the Bank Rate at 4.00% in November 2025, with four members preferring a 25 bps cut to 3.75%, as the MPC judged that inflation had peaked and risks to price stability and growth had become more balanced.

-

Inflation outlook: CPI inflation was judged to have peaked, with underlying disinflation progressing amid easing pay growth and softer services prices. The recent rise in headline inflation was attributed to temporary base effects in energy and administered prices.

-

Labour market and growth: Economic growth remained subdued and labour market slack was increasing, helping to moderate wage pressures, though members differed on how much spare capacity had emerged.

-

Risk assessment: The Committee noted that upside risks from inflation persistence had diminished, while downside risks from weak demand had become more apparent, leaving the risk balance broadly even.

-

Policy stance: Members agreed that monetary policy remained restrictive and continued to weigh on demand, contributing to disinflation; however, its restrictiveness had lessened as prior rate cuts took effect.

-

Majority view (5 votes): Those voting to hold highlighted lingering risks of inflation persistence, elevated wage growth, and uncertainty around structural labour market shifts, arguing that premature easing could stall disinflation.

-

Minority view (4 votes): Members preferring a cut cited established disinflation, rising slack, and restrictive policy conditions that risked an inflation undershoot and excessive drag on consumption and employment.

-

Forward guidance: The MPC reaffirmed that further reductions in Bank Rate would depend on the pace of disinflation, suggesting that gradual easing remained likely if inflation continued to trend toward target.

-

-

The Bank of England held rates steady in September, extending its pattern of alternating between cuts and pauses while signaling a more unified stance than in recent months. The decision reflects a balance between acknowledging the progress made in bringing inflation lower and maintaining caution as price pressures remain elevated. With growth and employment proving more resilient than expected earlier in the year, the Committee’s attention is increasingly centered on inflation risks, which continue to play a decisive role in shaping policy.

Decision

The Bank of England (BOE) decided to maintain its Bank Rate at 4.00% at the conclusion of the September meeting, continuing the pattern of alternating between cuts and pauses for the 10th straight meeting. The decision was less divided than the early August cut (which barely made it over the line), with 7 members voting for the pause and 2 members voting for a quarter-point cut. This vote was also more decisive than the June pause, which was decided with a 6-3 vote. Overall, the Bank of England’s pause today has the strongest majority since March.

In addition to the pause, the BoE’s Monetary Policy Committee (MPC) voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £70 billion over the next twelve months, bringing the total to £488 billion, down from the total of £558 billion set in the September 2024 meeting. Seven members backed the £70 billion path, while Catherine Mann preferred a slightly smaller £62 billion reduction and Huw Pill a larger £100 billion reduction, and the Committee reaffirmed that any change to the pace outside the annual review would face a high bar. This decision represents the Bank of England’s continuation of quantitative tightening with most members aligned on the chosen pace, and only modest debate over whether the process should be somewhat slower or faster, reinforcing the Bank’s preference for a steady and predictable approach.

The focus of the statement given today is inflation as it appears to be the main thinking keeping the MPC from cutting rates further (coincidentally, this decision was immediately preceded by a UK CPI release). The MPC starts out by pointing out the “substantial disinflation” that has occurred over the past two and a half years and explains that this “progress has allowed for reductions in [the] Bank Rate over the past year.” While inflation has generally fallen, there is still work to be done with both CPI and core CPI annual inflation above 3.5%. The MPC continues to describe the stickiness in inflation this year as a “temporary increase,” but at the same time, it highlights that “upside risks” to inflationary pressures are a “prominent” part of the outlook.

The general stance on inflation is a bit mixed. The MPC wants to point to a trend of disinflation that “has generally continued,” but it also must voice a concern of upside risks in its economic outlook. This echoes the sentiment in the last few announcements, but interestingly, the assessment of upside inflation risks looks to be getting stronger. Specifically, we can see a difference in how it is referenced in the August statement and today’s statement:

- August: “The MPC judges that the upside risks around medium-term inflationary pressures have moved slightly higher since May.”

- September: “Upside risks around medium-term inflationary pressures remain prominent in the Committee’s assessment of the outlook.”

Using the word “prominent” does not feel like an accident. I believe that several members of the MPC have become very vigilant of inflationary pressures and are unlikely to vote for another cut unless inflation starts to come down again.

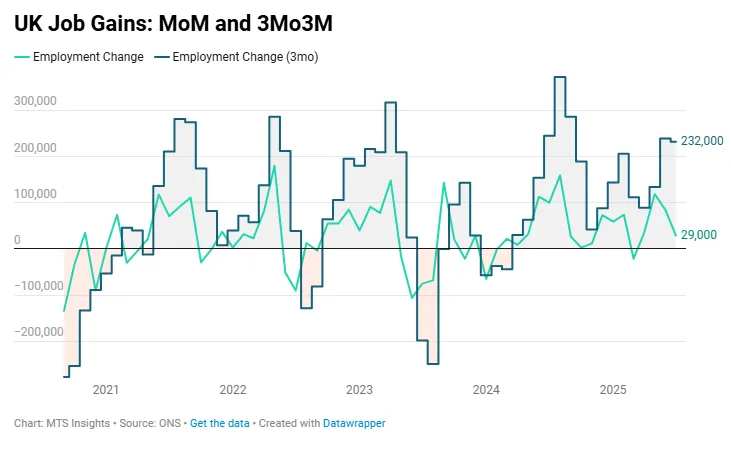

Why can the BoE move towards a more intense focus on inflation? A large part of it is because trends in growth and the labor market have been more resilient than the they were expected to be. In the first half of the year, US tariff policy and global trade uncertainty cast a shadow over the UK economic outlook, but those factors have not been as detrimental as previously thought. Employment gains have actually been pretty solid recently, increasing 232k in the three months to July and the unemployment rate at 4.7% is a tick below the Bank of England’s Q3 2025 forecast. GDP growth in Q2 2025 surprised to the upside, increasing 0.3% QoQ when growth was expected at 0.1% QoQ. This stronger data suggests that growth and employment are now less of a concern for the MPC than they appeared in Q1 and Q2, which is reflected in the September monetary policy statement, where the Committee devoted just three sentences to the topic.

-

The Bank of England cut the Bank Rate by 25 bps to 4.00% in August 2025, its fifth rate reduction since the easing cycle began in August 2024, amid signs of continued disinflation and soft economic growth. The decision was passed narrowly in a 5–4 vote.

- CPI inflation rose to 3.6% in June and is expected to peak near 4.0% in Q3 before falling back toward the 2% target.

- Private sector wage growth continued to slow, with regular AWE growth falling below 5% and expected to decline further to around 3.75% by year-end.

- GDP growth was weak in Q2 (+0.1% QoQ) and projected to pick up only modestly in Q3 (+0.3%), with April and May both posting negative monthly readings.

- Labor market slack continued to build: unemployment rose, vacancies stayed below equilibrium, and employment growth weakened.

- One member voted for a 50 bps cut, citing downside risks to inflation and activity, while four members voted to hold, citing persistent inflation expectations and elevated services prices.

- Monetary Policy Report - August 2025

-

The Bank of England kept its main policy rate, the Bank Rate, unchanged at 4.25% following the June 2025 meeting. The decision to pause maintains the cadence of interest rate cuts that has led to a gradual easing in monetary policy since August 2024. While there was a pause today, recent growth and employment data have tilted the Monetary Policy Committee members to be a bit more dovish as it appears that the economy could be weakening more than they expect.

Decision

The Bank of England (BoE) opted to leave the Bank Rate unchanged at 4.25%. Six members voted for a pause and outnumbered the three members who voted for a 25 bps cut. Of the three members voting for a cut, two of those members had voted for a 50 bps cut in the May meeting (Dhingra and Taylor), and one voted for the 25 bps cut that occurred (Ramsden). The other four members who voted for a cut in the May meeting (Bailey, Breeden, Greene, Lombardelli) joined the two who voted for a pause (Mann, Pill) to create the majority that decided on no change in June.

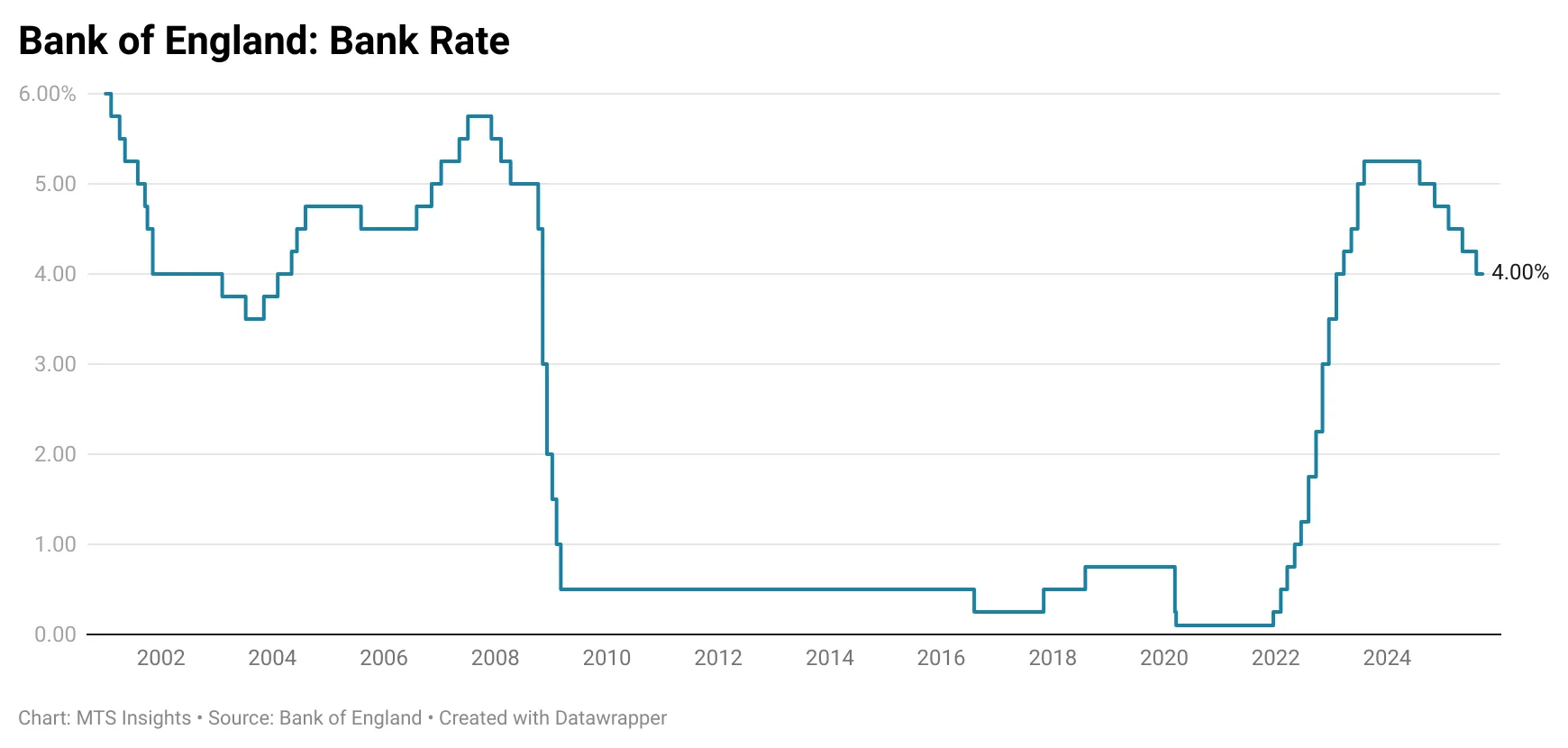

The decision maintains the pattern of alternating between a pause and a cut that was set after the first quarter point cut in August 2024. Since then, we have had 25 bps cuts in November 2024, February 2025, and May 2025 and pauses in September 2024, December 2024, March 2025, and now June 2025. In total, the Bank of England has cut rates by 100 bps over that timeframe.

Minutes

Throughout its rate-cutting cycle, the Bank of England has been navigating a balance between a gradual weakening in UK economic growth and employment and expectations of a resurgence in inflation this year. So far, the data points have drifted around the forecasts of the Monetary Policy Committee (MPC) members such that a gradual easing of the Bank Rate was possible. In the June meeting, the MPC members paused to reassess the developments in the global economy and recent UK data points to decide what the decision in early August will be.

Inflation

Inflation data for May was released the day before the Bank of England’s decision on June 18th, so the MPC had plenty to discuss ahead of the decision today. The UK CPI inflation rate ended up at 3.4% YoY in May with core CPI inflation coming in at 3.5% YoY (below analyst expectations). The details of the report showed goods CPI inflation on the rise, up to the highest since November 2023 at 2.0% YoY. About 0.2 ppts of the acceleration in the headline rate came from three goods categories: food & non-alcoholic beverages (+0.11 ppts), furniture & household goods (+0.07 ppts), and miscellaneous goods & services (+0.03 ppts). The energy aggregate, which the BoE expects will become an upward pressure on inflation, fell -0.8% MoM and -1.7% YoY.

In a nod towards the new data, the Bank of England points out that CPI inflation of 3.4% in May is “in line with expectations in the May Monetary Policy Report.” This recent rise is expected to be the peak for inflation in 2025 before it flattens out and starts to ease before “falling back towards the target next year.” The Bank of England’s tone on inflation in the June statement and minutes suggests that prices are developing largely as expected, but members will be monitoring the persistence of these current inflation rates. Notably, it also shares that the MPC members see “two-sided risks to inflation.”

Growth and Employment

The downside risk to inflation comes from the Bank of England’s view that UK growth has “remained weak” and the labor market has “continued to loosen” which suggests that economic slack has increased since the cutting cycle began.

- GDP data has been volatile over the last few months, with strong monthly reports in February and March to cap off a strong Q1, but the most recent April data point revealed a drop of -0.3% MoM, led by weak services. The BoE also points out that the strong readings in February and March “could have been affected by a front-loading of activity ahead of the imposition of new tariffs by the United States and related trade policy developments.” On an annual basis, GDP growth slowed to 0.9% YoY, which is slightly ahead of the May forecast for Q2 2025. Economic activity is expected to continue to soften in May and June, especially with US trade policy continuing to create growth headwinds in the broader global economy.

- The labor market report for April was also weak as it showed the unemployment rate ticked up 0.2 ppts to 4.6%, the highest since July 2021. This rise has been a little bit ahead of schedule as the Bank of England forecasted in the May meeting that it would reach that level by the end of Q2 2024, and in fact, the flash estimate of May payrolls, a drop of -274k in employment, suggests the unemployment rate might overshoot the projection. The easing in the labor market has led to a not insignificant decline in wage growth that has contributed to the disinflationary trend. The MPC members are confident that the still “elevated” wage growth will see “a significant slowing over the rest of the year.”

The growth and employment data were the main arguments wielded by the three MPC members who voted for a quarter-point rate cut today. Alongside the progress on inflation, the members assessed that “the cumulative evidence from a range of labour market data pointed to a material further loosening in labour market conditions.” Compared to other central banks, the Bank of England does appear to be facing more loosening in the labor market, so these arguments are not invalid and would probably become the basis of a cut in August.

In my opinion, unless data suddenly shifts before the next meeting, GDP growth easing at the BoE’s expected pace and a faster-than-expected increase in the unemployment rate will lead to a quarter point cut in August. The trend in hiring is especially concerning given the flash figures and the fact that UK firms have faced broadly weaker global economic conditions in Q2 2025 due to US tariffs. The Bank of England briefly mentions a potential spike in energy prices due to the Middle East, but the inflationary pressures from this will almost certainly be transitory and something that the BoE can look through.

-

The Bank of England moved forward in a contested decision with a quarter point rate cut following its May meeting. There were supporters that were both more hawkish and more dovish in the deliberations, and ultimately, the more neutral position won out. The division is a good representation of the Bank of England walking a tightrope, trying to balance the hotter inflation outlook and cooler growth expectations.

Decision

The Bank of England voted by a narrow 5–4 margin to lower its Bank Rate by 25 bps to 4.25% at its May meeting, marking the start of a gradual policy easing cycle. The decision was highly contested: two members pushed for a larger 50 bp cut, arguing that persistent disinflation and weak domestic demand justified more accommodation, while two others voted to hold rates steady, citing continued inflationary pressures and firming household inflation expectations. The majority ultimately favored a middle ground, judging that inflation progress had been sufficient to begin withdrawing some policy restraint without abandoning a restrictive stance altogether.

The decision reflects growing concern about weakening global growth and uncertainty surrounding new trade policies, as well as slowing domestic momentum. The Bank still expects headline inflation to temporarily rise in Q3 due to energy-related base effects, but sees that increase as transitory. Importantly, the MPC emphasized that monetary policy is not on a pre-set course and remains data-dependent. However, for those observing the trend, the cut today continues a pattern of alternating between a pause and a 25 bps cut that has been evident since August 2024.

Monetary Policy Report

The May policy announcement comes with an update to the Monetary Policy Report put together by the BoE members which features key forecasts updates and discussion about the economic and monetary policy outlooks. The key parts of the report are updates to the inflation and growth forecasts which reflect some shifts in data since the last Monetary Policy Report (MPR).

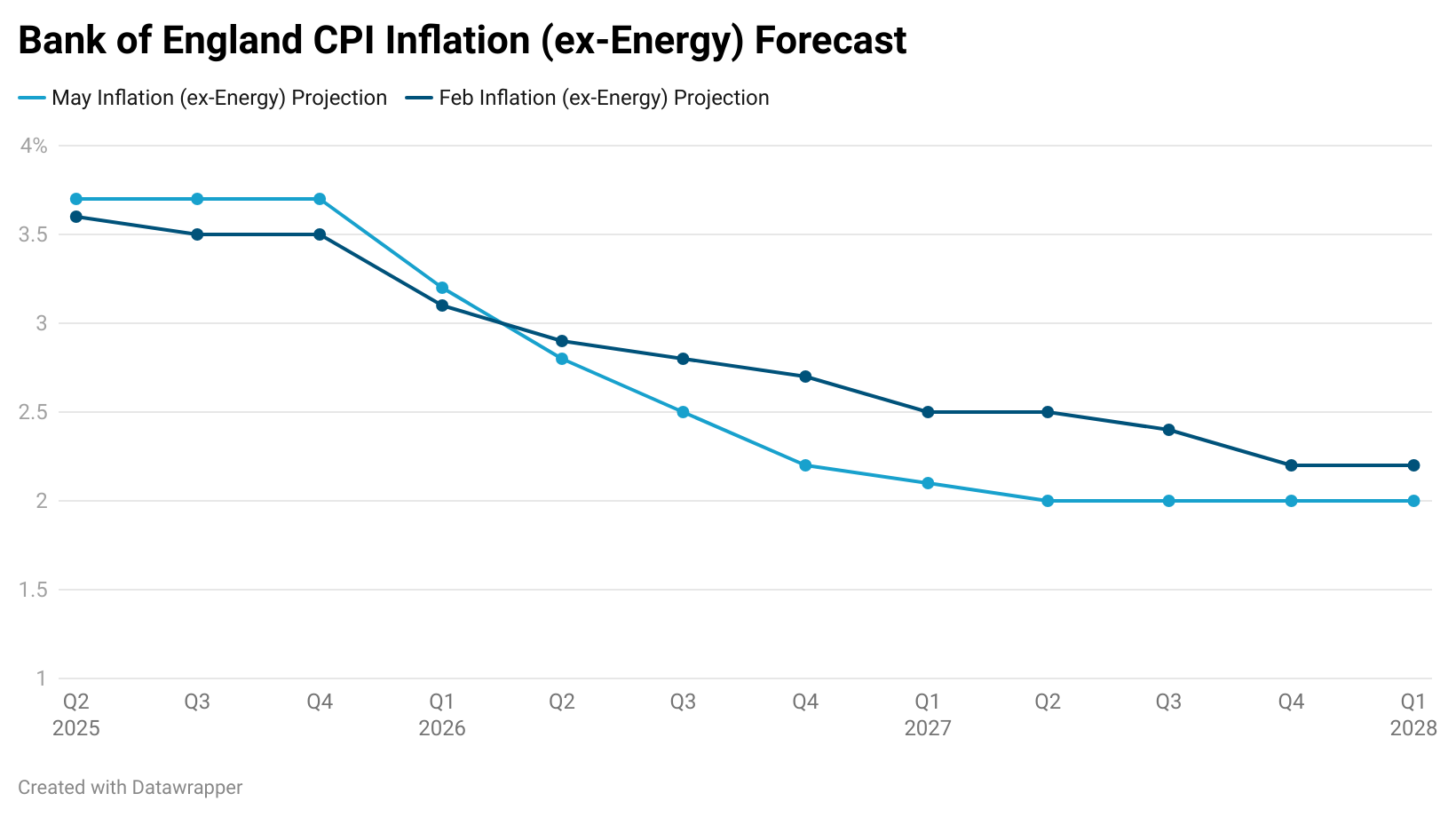

The BoE updated its forecast for inflation after price growth in the first quarter of the year was reported in line with expectations. The estimates for inflation in the next four quarters were raised in the May update, only slightly above the February estimates, but in the medium- to long-term, the BoE actually sees significant disinflation. It now projects CPI inflation (ex-energy) to fall to 2.0% by Q2 2027, while the February forecast did not reach that level. The BoE maintains its position that the increase in inflation in the near term is transitory and that inflationary pressures would dissipate due to “a period of excess economic slack” or weaker growth.

The BoE also updated its forecast for GDP growth, and it reflects some of the upside surprises that we have seen in the monthly data from the ONS. The February forecast for four-quarter GDP growth was well beaten at 1.2% vs the expected 0.4%. Because of that, the near-term estimates of GDP growth have been moved up to reflect a smoother path of real GDP growth over the next few quarters as the BoE still sees economic growth weakening in the short-term. This partly incorporates expectations that the volatile trade environment will cause excess supply to ”widen over the next couple of years, to just under 1% of potential GDP, before narrowing by the end of the forecast period.”

The May edition of the Monetary Policy Report made clear that the primary reason for today’s rate cut was the ongoing “progress in reducing domestic inflationary pressures,” which gave the Bank enough confidence to begin gradually withdrawing policy restraint. At the same time, the BoE flagged growing global trade uncertainty, particularly around US tariffs, as an additional downside risk to UK growth and a counterweight to any potential upside inflation risks. This caution comes despite stronger-than-expected GDP growth in late 2024 and early 2025. Still, the Bank did not commit to any future path of policy, noting that monetary policy would need to stay restrictive “until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further,” signaling a continued emphasis on a data-dependent approach.

-

The Bank of England opted to keep its policy interest rate unchanged following its March meeting with a solid majority voting for the action. This pause appears to be in line with the Bank of England’s cadence of cuts that started when the central bank first cut rates in August 2024. Since then, the policy rate is down 75 bps, but a cautious outlook clouded by uncertainty kept the Bank of England on the sideline today.

Decision

By a vote of 8 to 1, the Bank of England opted to keep the Bank Rate unchanged at 4.5% in March 2025. The sole dissenter, Swati Dhingra, voted for a 25 bps cuts after disagreeing with the February decision as well, voting for a larger 50 bps cut. The pause confirms that the Bank of England wants to move forward with its cutting cycle gradually, and it appears to be doing that through a pattern of rate cuts every other meeting. So far three cuts have followed this pattern: 25 bps cut in August, pause in September, 25 bps cut in November, pause in December, 25 bps cut in February, pause in March. This suggests that the Bank of England will be considering a cut in the next meeting in May if disinflation continues as the it expects.

Inflation Outlook

The BoE remains fixated on the goal of combatting inflation which is the main reason why we are seeing pauses every other meeting. The inflation situation has improved significantly since 2023, but the BoE still wants to maintain the Bank Rate “in restrictive territory so as to continue to squeeze out persistent inflationary pressures.” That hawkish sentiment is tempered by the fact that the Bank admits that “there has been substantial progress on disinflation” which has allowed them to ease monetary policy in the last six months.

Unfortunately, recent data has started to run against the Bank of England. The annual increase in CPI inflation increased to 3.0% in January which was above the BoE’s forecast in the February Monetary Policy Report. Core inflation ticked up as well, rising to 3.8% YoY, the highest since April 2024. The inflation forecast did account for a rebound in energy prices in the first half of the year, but that rebound might be happening faster than expected. With trade uncertainty on the rise and threatening to become a new inflationary pressure in supply chains, the BoE was probably correct to pause today and may be likely to break its rate cut cadence in the next meeting.

Growth Outlook

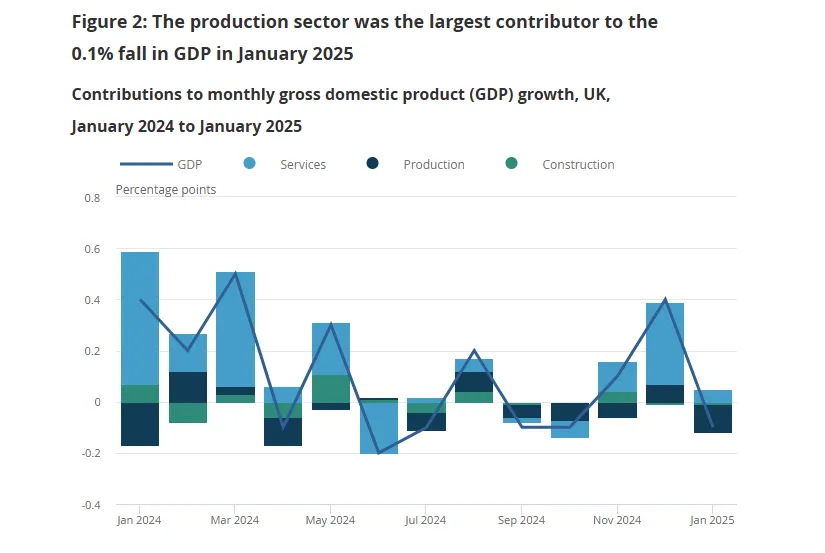

A key downside risk to the inflation outlook is a slowdown in growth that would create some downside pressure on prices from the demand side. The Bank of England likely scrutinized the GDP report in January which revealed that the UK economy contracted to start the year to decipher whether or not a new downtrend in growth is coming. Its growth outlook appears to be a bit dim as in the BoE’s Minutes it noted that “growth was expected to slow on the back of tariff and wider policy uncertainty, among other factors” and that indicators for Q1 2025 growth reflected “a weakening in household consumption growth” and that “firms’ output and investment expectations had also fallen.”

Despite hard data signaling some weakness, the outlook is still for slight growth in Q1 2025. The BoE makes it clear in its statement that growth is an important consideration in its inflation outlook: “Should there be greater or longer-lasting weakness in demand relative to supply, this could push down on inflationary pressures, warranting a less restrictive path of Bank Rate.” This balance of inflation and growth is key in the BoE’s decision-making.

Monetary Policy Outlook

While the March decision was relatively settled and a pause was largely expected, the next May decision to cut will be more uncertain. The BoE has not given any direct guidance on next month’s decision, but instead, it reaffirmed its intention to maintain “a gradual and careful approach to the further withdrawal of monetary policy restraint.” Guidance leaves open two paths that are will be determined by the balance between supply and demand pressures. If demand sees a “longer-lasting weakness” relative to supply, the BoE might opt for a less restrictive Bank Rate. If supply is more constrained relative to demand, putting upward pressure on inflation, the BoE might opt for a tighter monetary policy path.

While it seems like both paths are weighted similarly, the Bank of England does appear to be leaning in one direction. Based on its forecasts and language, it likely sees more upside risk to the inflation outlook than downside risks to the growth outlook. The March deliberations ended with a clear hawkish tilt: “Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further.” With that being said, I believe that the BoE is more likely to pause in May unless data changes the outlook significantly.

-

The Bank of England voted 7-2 to cut the Bank Rate by 25 bps to 4.5% with the two dissenting members preferring a larger 50 bps cut to 4.25%. This marks a significant shift in policy stance as the Bank acknowledges substantial progress in its fight against inflation while maintaining a cautious approach to policy easing.

- Economic Outlook:

- Policy Stance & Forward Guidance:

- Key Risks:

- Monetary Policy Report: February 2025

-

The Bank of England keeps rates unchanged at 4.75% following its December meeting by a vote of 6-3 with the minority opting for a 25 bps cut. The members voting for a pause pointed out that "CPI inflation, wage growth and some indicators of inflation expectations had risen, adding to the risk of inflation persistence" despite some signs of weaker growth. 5 of the 6 voting for the cut argued that the BoE should take "a gradual approach to the withdrawal of policy restrictiveness" but did not commit to any moves in the future.