ADP National Employment Report

ADP National Employment Report

- Source

- ADP

- Source Link

- https://adpemploymentreport.com/

- Frequency

- Monthly

- Next Release(s)

- May 6th, 2026 8:15 AM

-

June 3rd, 2026 8:15 AM

-

July 1st, 2026 8:15 AM

-

August 5th, 2026 8:15 AM

-

September 2nd, 2026 8:15 AM

-

September 30th, 2026 8:15 AM

-

November 4th, 2026 8:15 AM

-

December 2nd, 2026 8:15 AM

Latest Updates

-

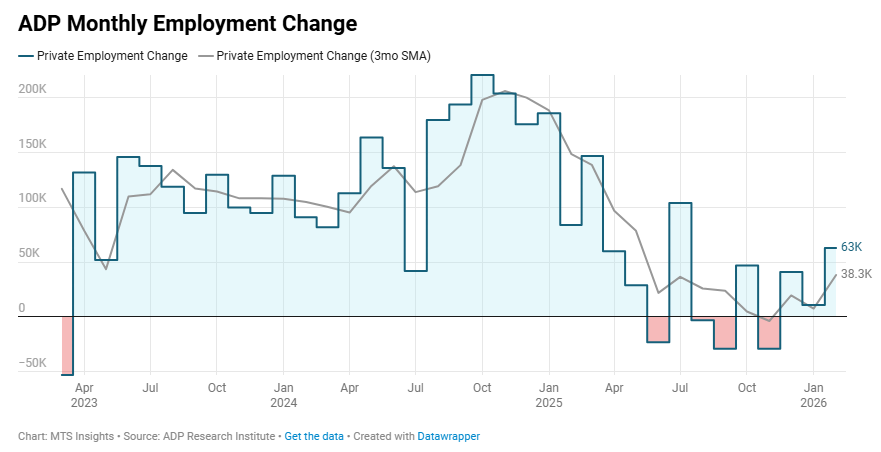

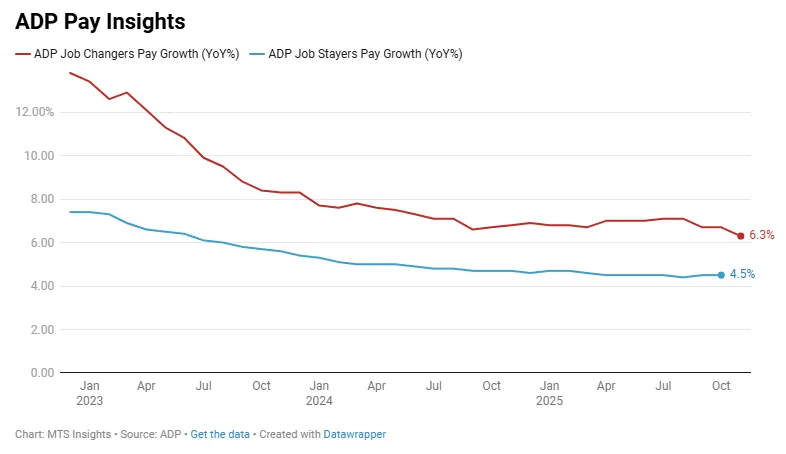

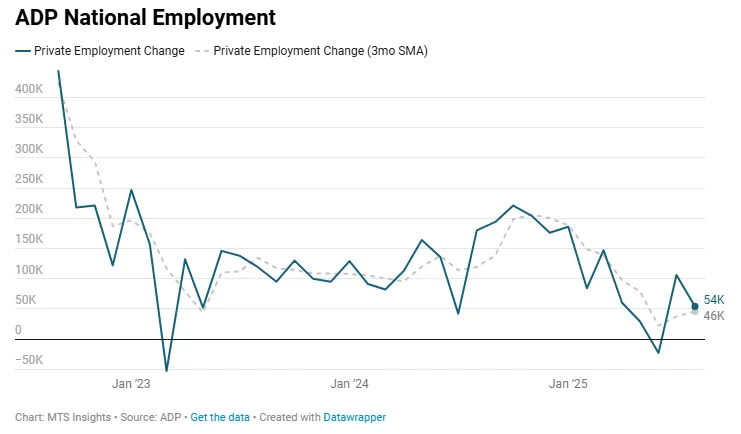

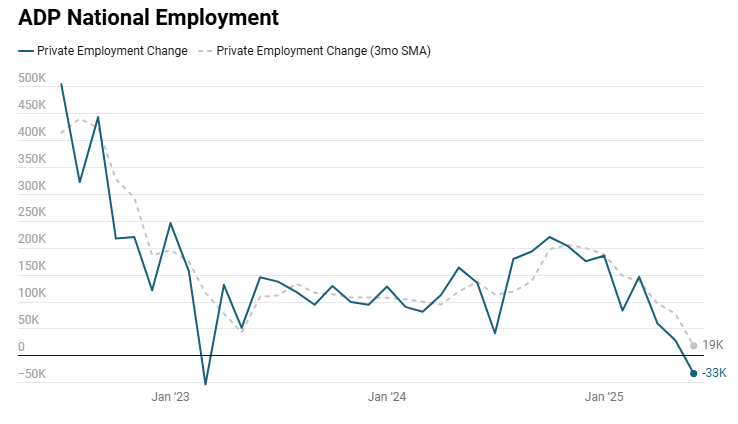

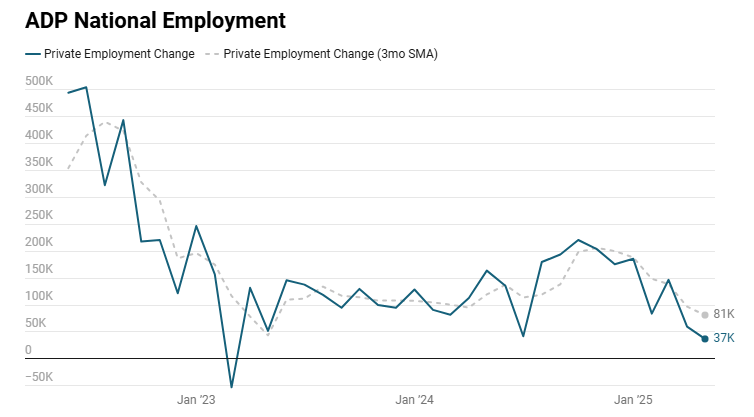

ADP estimates that US private sector employment increased by +63,000 (vs +45,000 expected) in February, while job-stayer pay growth held at +4.5% YoY, indicating a moderate rebound in hiring with wage growth remaining steady.

-

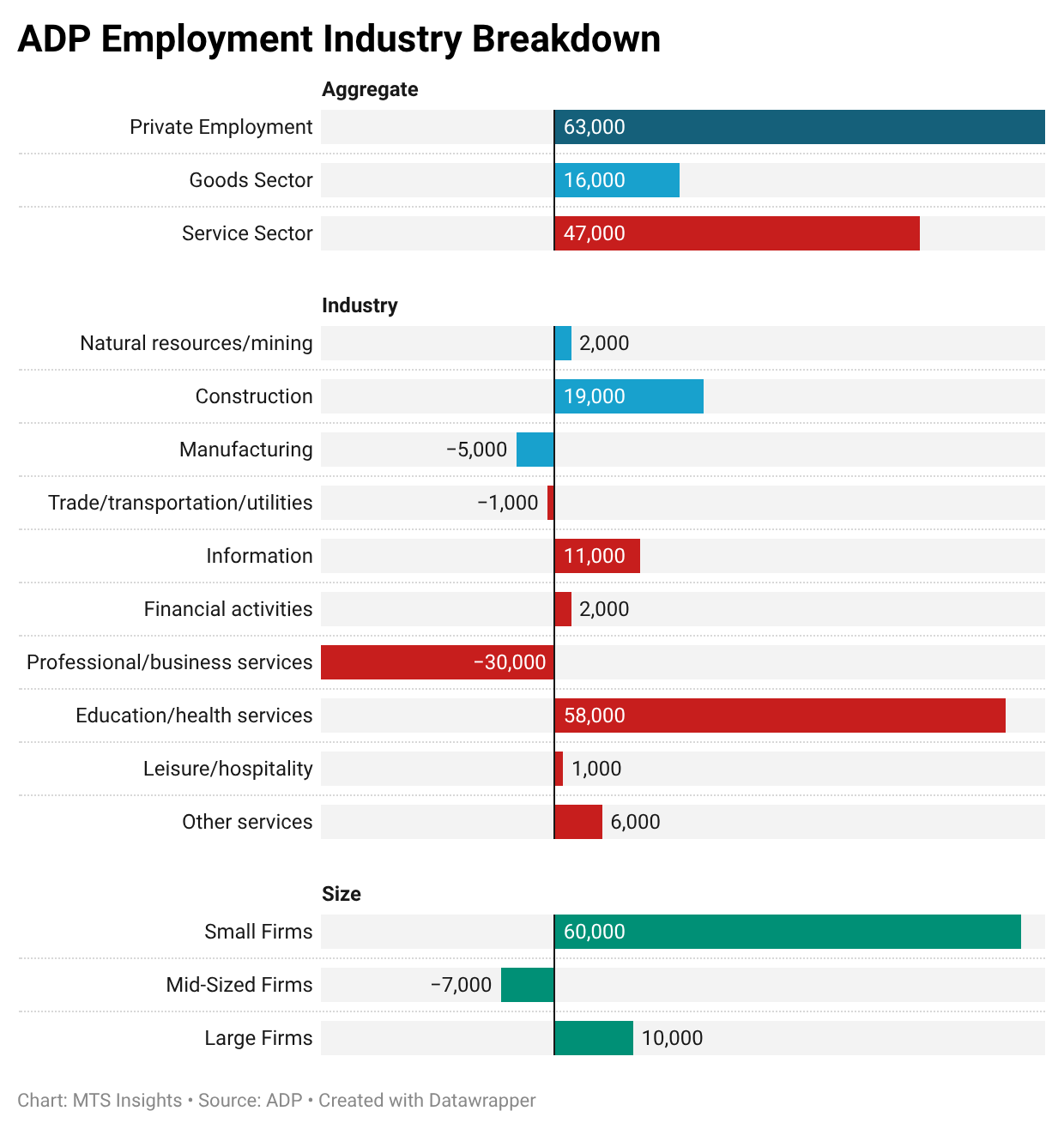

The +63,000 increase in private employment marked the strongest monthly job gain since July 2025, signaling a pickup in hiring after weaker readings in recent months.

-

Goods-producing industries added +16,000 jobs overall, led by construction (+19,000) and natural resources and mining (+2,000), while manufacturing posted a decline of -5,000 jobs.

-

Service-providing industries accounted for the majority of gains with +47,000 jobs, driven primarily by education and health services (+58,000), while professional and business services saw the largest decline at -30,000.

-

Regionally, employment increased in the South (+37,000), West (+19,000), and Northeast (+11,000), while the Midwest recorded a decline of -4,000 jobs.

-

Small establishments accounted for the bulk of hiring with +60,000 jobs, including +58,000 at firms with 1-19 employees, while medium-sized firms shed -7,000 jobs and large establishments added +10,000.

-

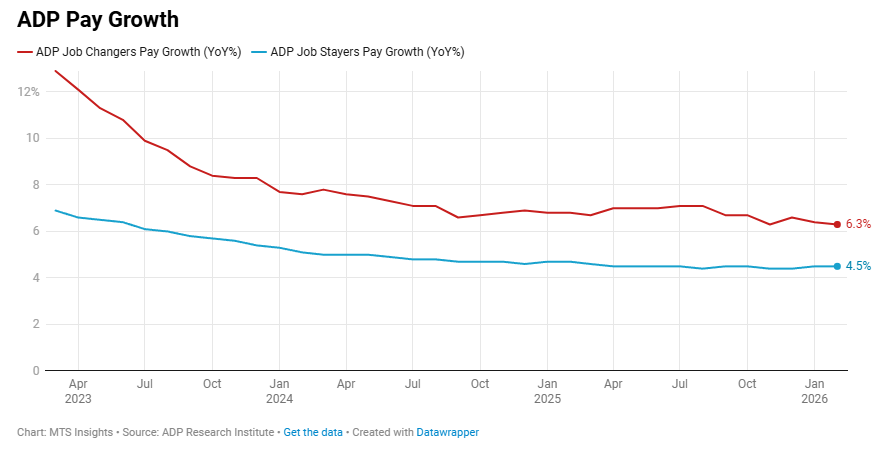

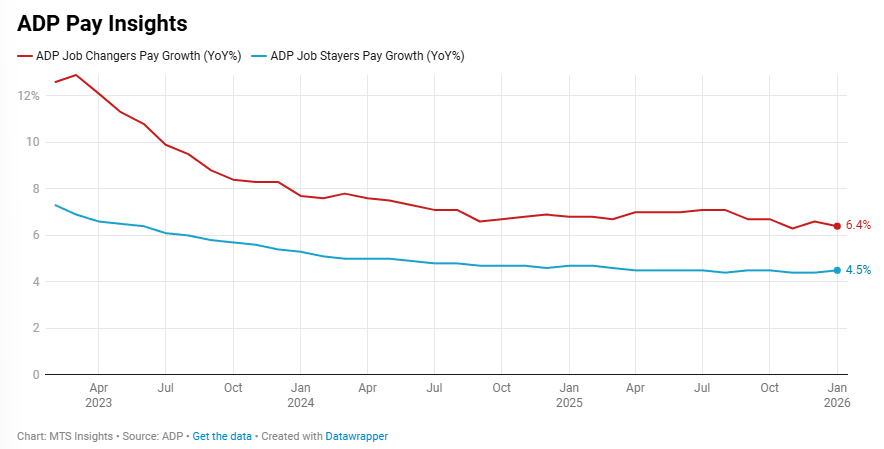

Pay growth for job-stayers remained unchanged at +4.5% YoY in February, indicating steady wage growth for workers who stayed with the same employer.

-

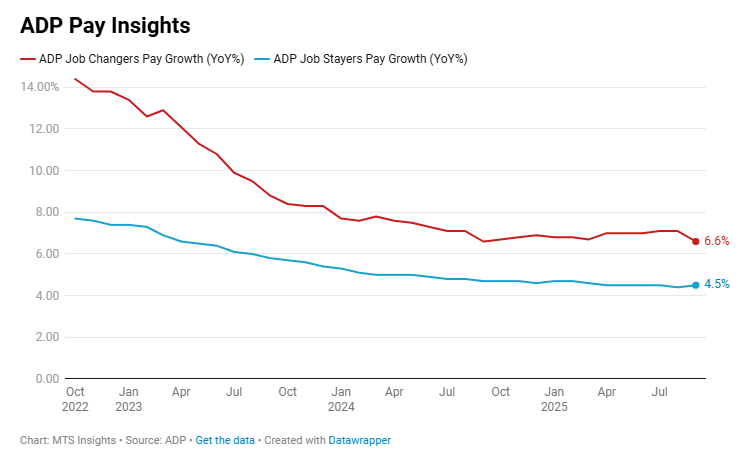

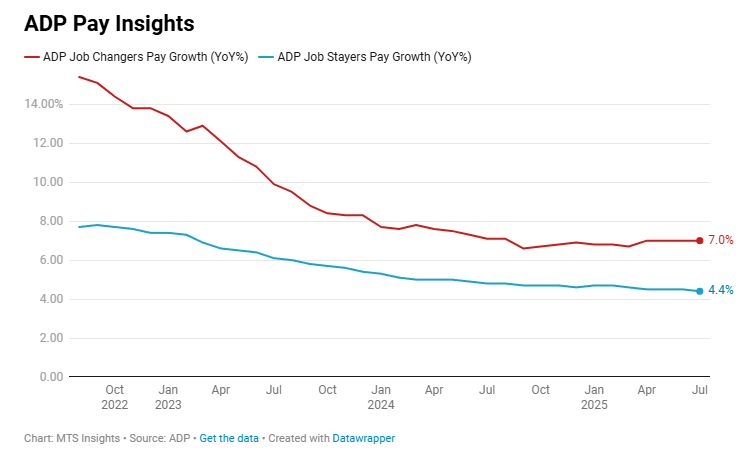

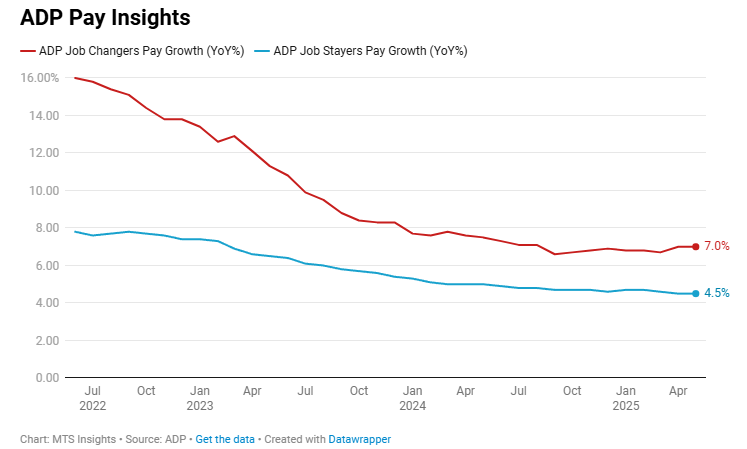

Pay growth for job-changers slowed to +6.3% YoY (down from +6.4% YoY), and ADP noted that the wage premium for switching employers declined to a record low in February, suggesting reduced pay advantages for workers changing jobs.

-

-

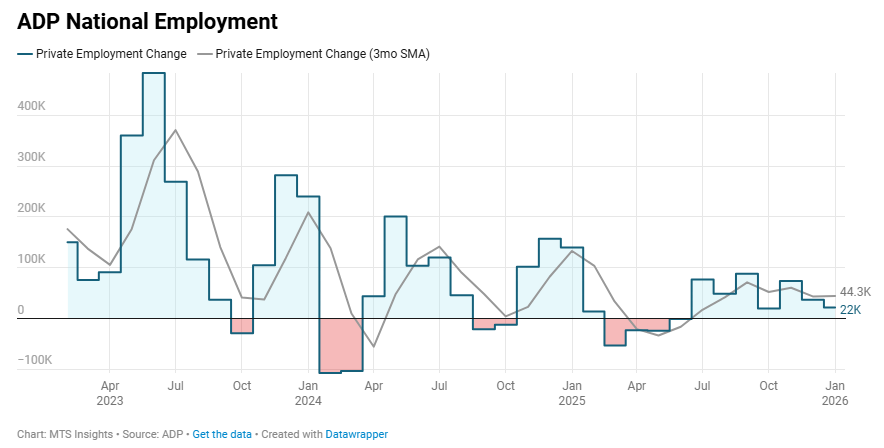

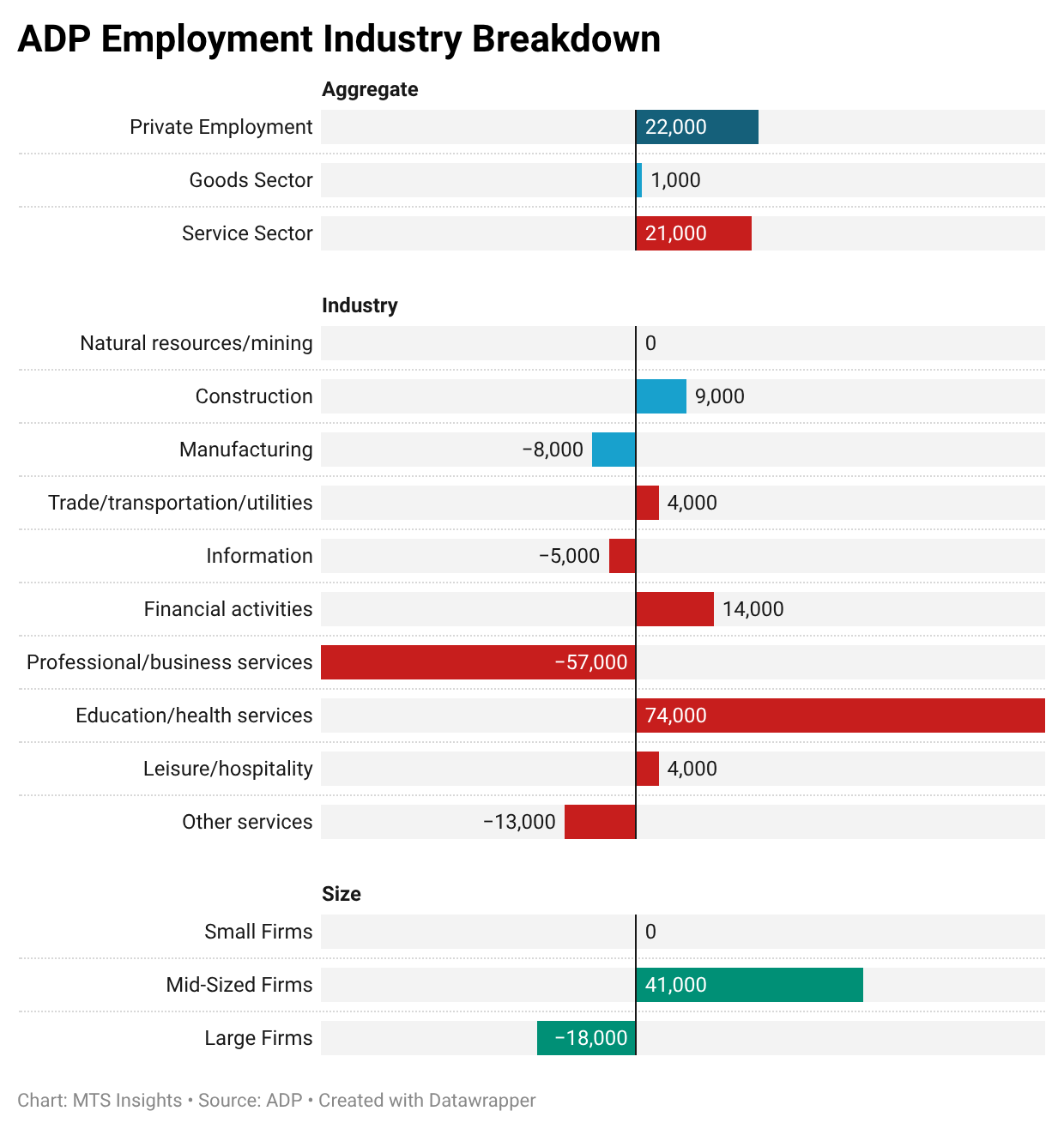

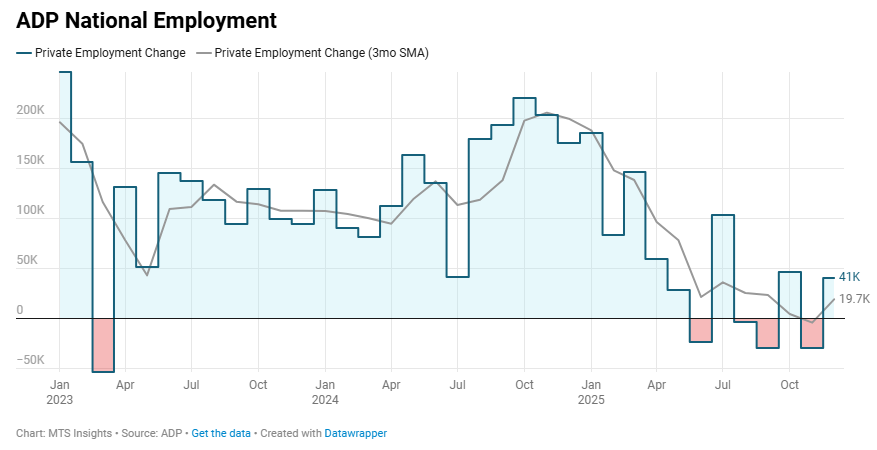

ADP estimates that US private sector employment rose by +22,000 in January (following a downward revision in December), indicating subdued hiring momentum at the start of 2026.

-

The softer January and downward revision in December (from 41,000 to 37,000) put the 3-month average at roughly +44,000, showing hiring remained modest despite earlier strength.

-

Education and health services led job gains with +74,000 positions, standing out as the primary source of employment growth during a weak hiring month.

-

Professional and business services shed -57,000 jobs, representing the largest sectoral drag on overall employment.

-

Manufacturing employment declined -8,000, extending a run of monthly job losses that has persisted since March 2024.

-

Service-providing industries added a net +21,000 jobs, while goods-producing sectors posted only a small +1,000 increase, reflecting uneven sector performance.

-

Regionally, employment rose in the Midwest (+25,000) and Northeast (+17,000), but fell in the South (-10,000) and West (-11,000), with large declines in the South Atlantic and Pacific subregions.

-

Mid-sized firms accounted for most hiring with +41,000 jobs, while large firms cut -18,000 positions and small firms were flat overall.

-

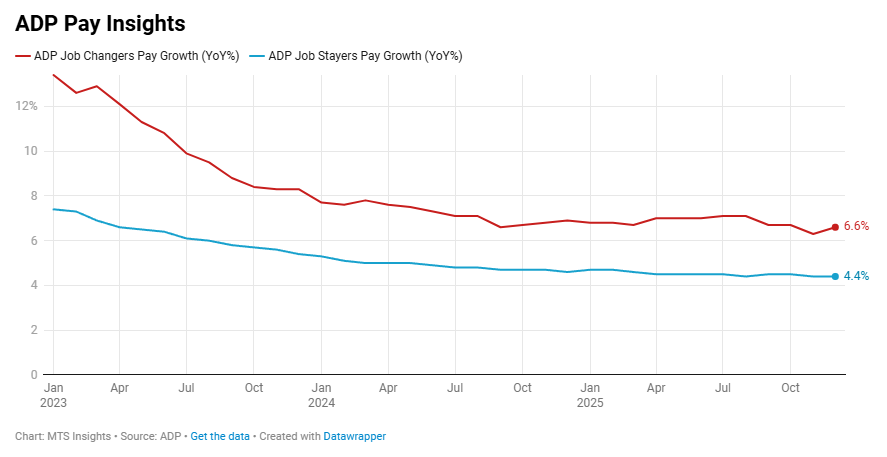

Job-stayer pay growth edged up to +4.5% YoY (Dec: +4.4%), while pay growth for job changers eased to +6.4% YoY (Dec: +6.6%), indicating largely stable wage trends despite slower job creation.

-

-

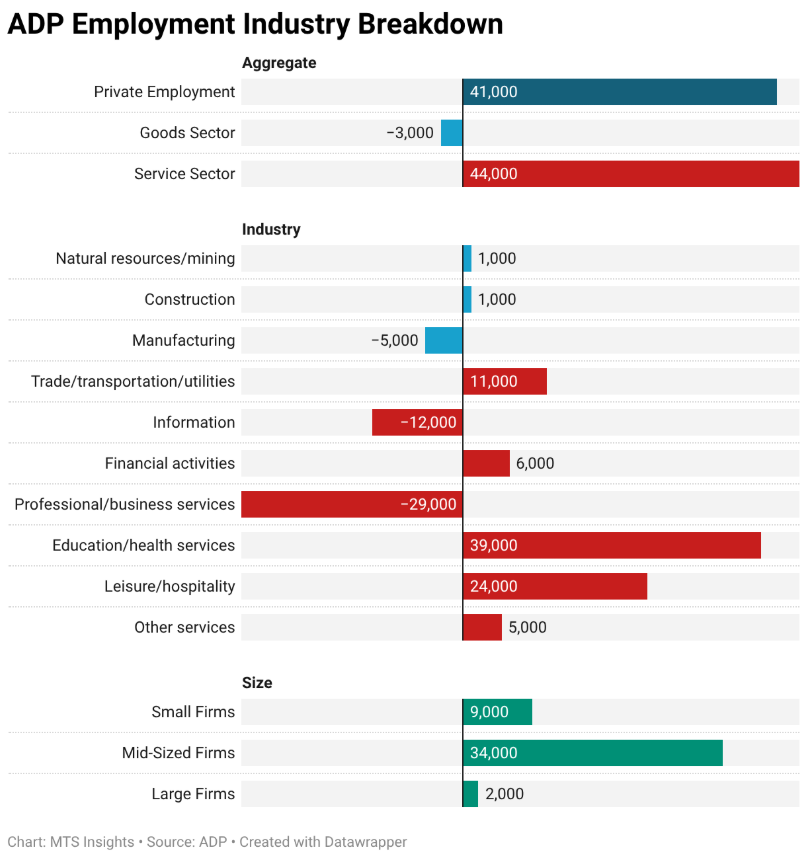

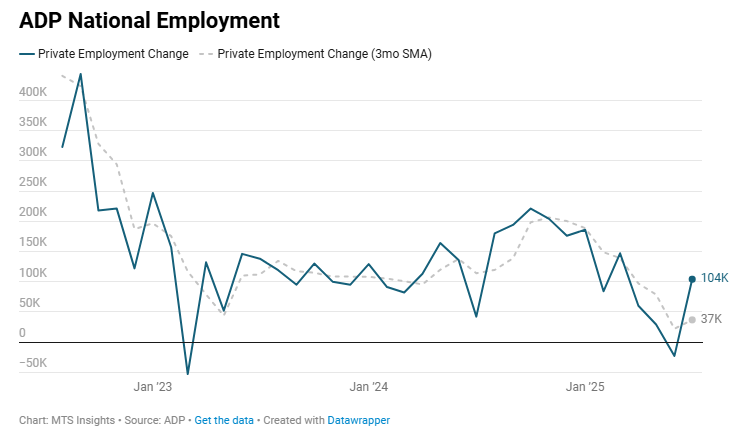

ADP estimates that US private sector employment rose by +41,000 (vs +47,000 expected) in December 2025, marking a modest rebound in hiring after a -29,000 decline in November.

-

Private sector employment increased by +41,000 in December, reversing November weakness and driven primarily by service-providing industries (+44,000), while goods-producing employment declined -3,000.

-

Education and health services led job gains at +39,000, followed by leisure and hospitality (+24,000) and trade, transportation, and utilities (+11,000), offsetting declines in professional and business services (-29,000) and information (-12,000).

-

Manufacturing employment fell -5,000, contributing to the overall contraction in goods-producing industries despite small gains in construction (+1,000) and natural resources and mining (+1,000).

-

Regionally, job growth was concentrated in the South (+54,000) and Northeast (+40,000), while the West saw a sharp decline of -61,000, largely driven by losses in the Pacific region (-59,000).

-

By establishment size, medium-sized firms added +34,000 jobs and small firms added +9,000, while large firms posted only modest gains of +2,000, indicating limited hiring among the largest employers.

-

Job-stayer pay growth held steady at +4.4% YoY in December, unchanged from November, suggesting stable wage growth for existing employees.

-

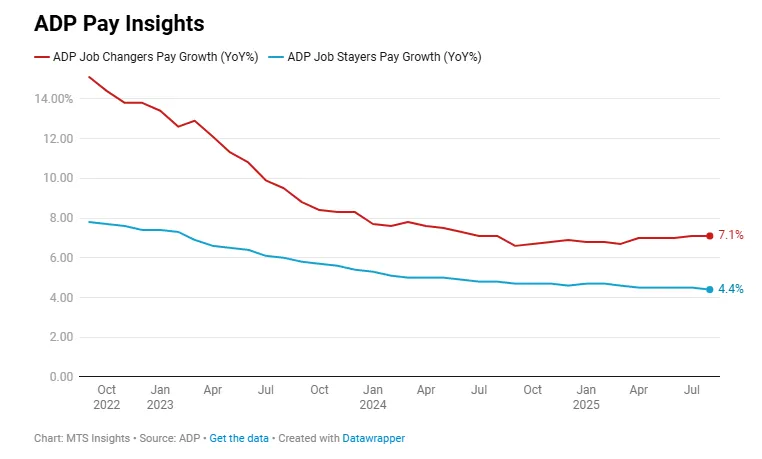

Pay growth for job changers accelerated to +6.6% YoY (Nov: +6.3%), indicating stronger wage gains for workers switching jobs despite subdued overall hiring momentum.

-

-

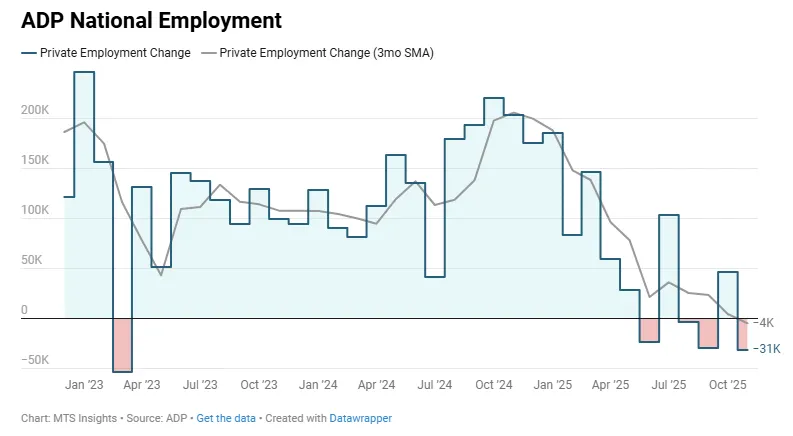

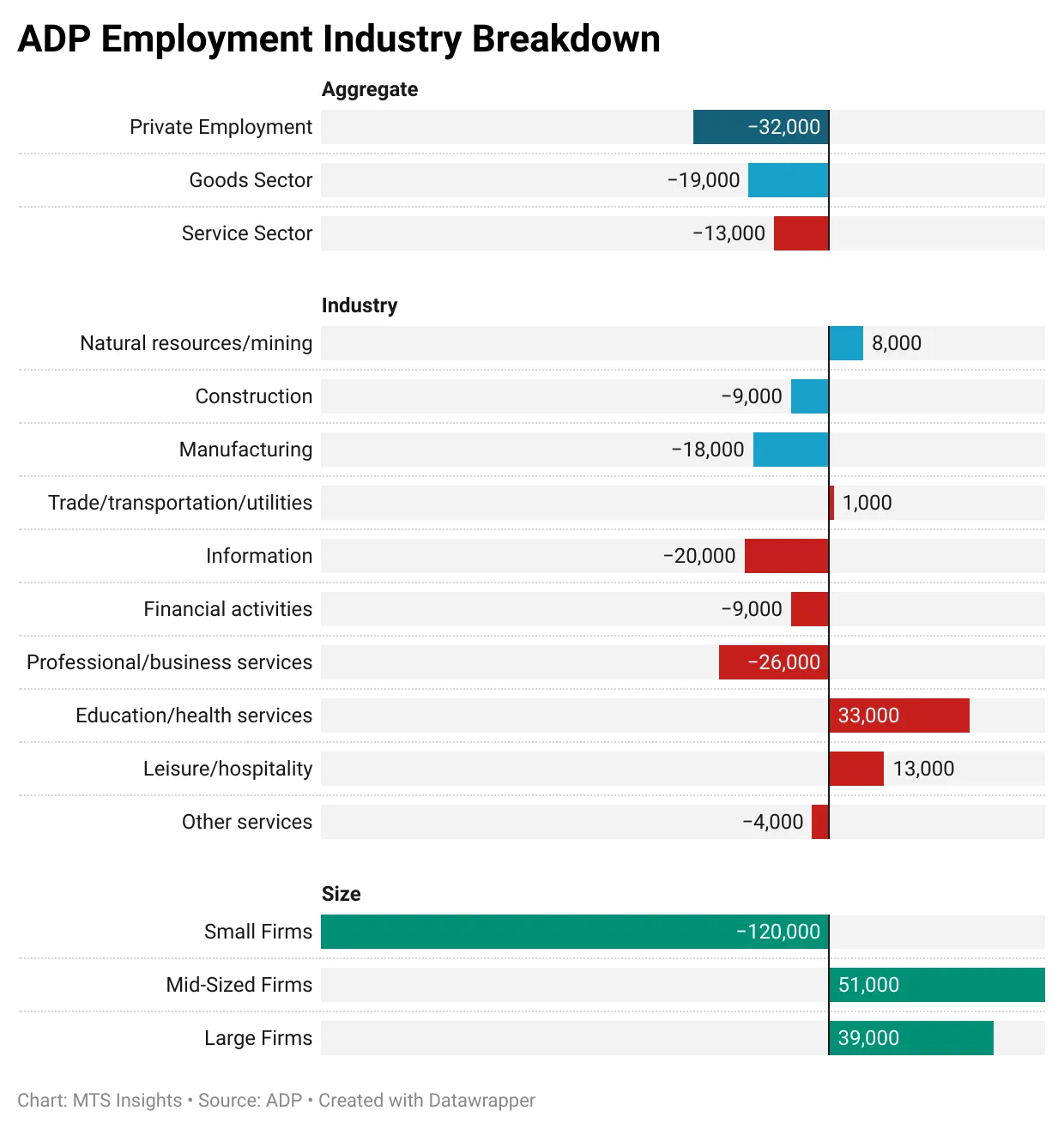

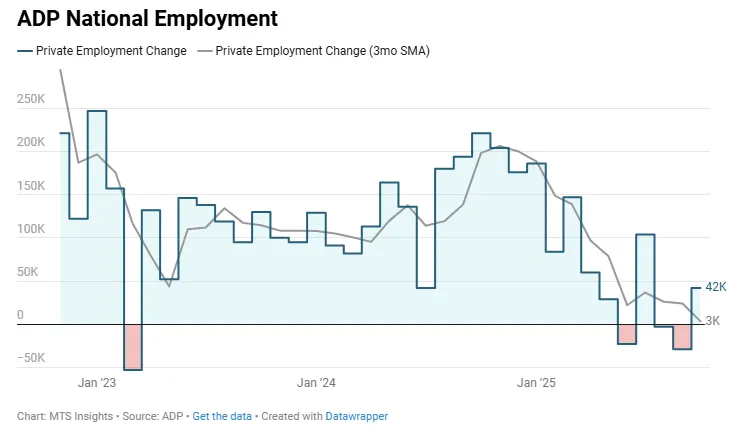

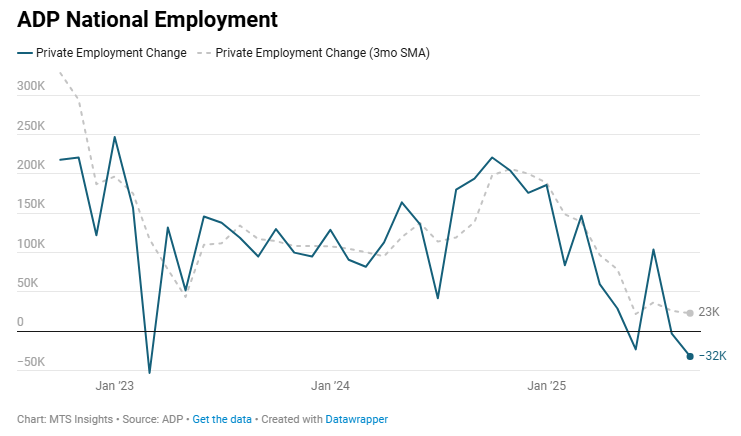

ADP estimated in the November edition of its National Employment Report that private payrolls declined by -32,000, the largest monthly decline that ADP has reported since March 2023. The fourth monthly decline in six months was well below the modestly optimistic forecast of an increase of 10,000. The weak reading was further confirmation of a trend of deterioration in hiring demand that has been developing since Q2 2025. The three-month average dropped to below zero for the first time since the pandemic, falling from around 37,000 in July to 5,000 in October and now around -4,300 in November.

The details point to a broad-based decline across industries, with education & health services continuing to be an outlier:

-

The private goods sector saw employment down -19,000 in November, led by declines in construction (-9,000) and manufacturing (-18,000). The manufacturing industry specifically has seen four straight months of declines, with the November drop being the largest in that sequence, for a total decline in private manufacturing employment of -30,000 in that period.

-

The private services sector saw employment decline -13,000 in November. Within the services industries, the changes were more mixed, but the biggest declines were seen in information (-20,000) and professional & business services (-26,000). Offsetting the job losses in the rest of the sector were gains in education & health services (+33,000) and leisure & hospitality (+13,000). Excluding education & health services, the headline employment change would have been the worst since the pandemic at -65,000.

The segmentation by firm size shows that the decline in employment continues to be concentrated in small businesses. ADP reports that smaller firms lost a total of -120,000 jobs in November, while mid-sized and large firms both saw job gains of 51,000 and 39,000, respectively. This is a continuation of the trend we have seen over the last few months and confirms that the labor market is experiencing a cyclical downtrend where the economically sensitive parts of the economy are hurting the most.

ADP’s wage data also signaled weakness in the labor market. The annual pay growth of job changers has been tracked as an indicator of tightness in employment data, and it just saw its largest deceleration since September 2024, which, coincidentally, was when the Fed decided to cut rates by 50 bps. Job changers’ pay growth now sits at 6.3% YoY in November, falling from 6.7% YoY in October, the lowest reading since February 2021. The wage data also supports to narrative that small businesses are leading the labor market deterioration. While large and mid-sized firms’ wage growth (for job stayers) was between 4.7% and 4.9% YoY, wage growth in the smallest segment of firm size (1-19 employees) was just 2.5% YoY.

-

-

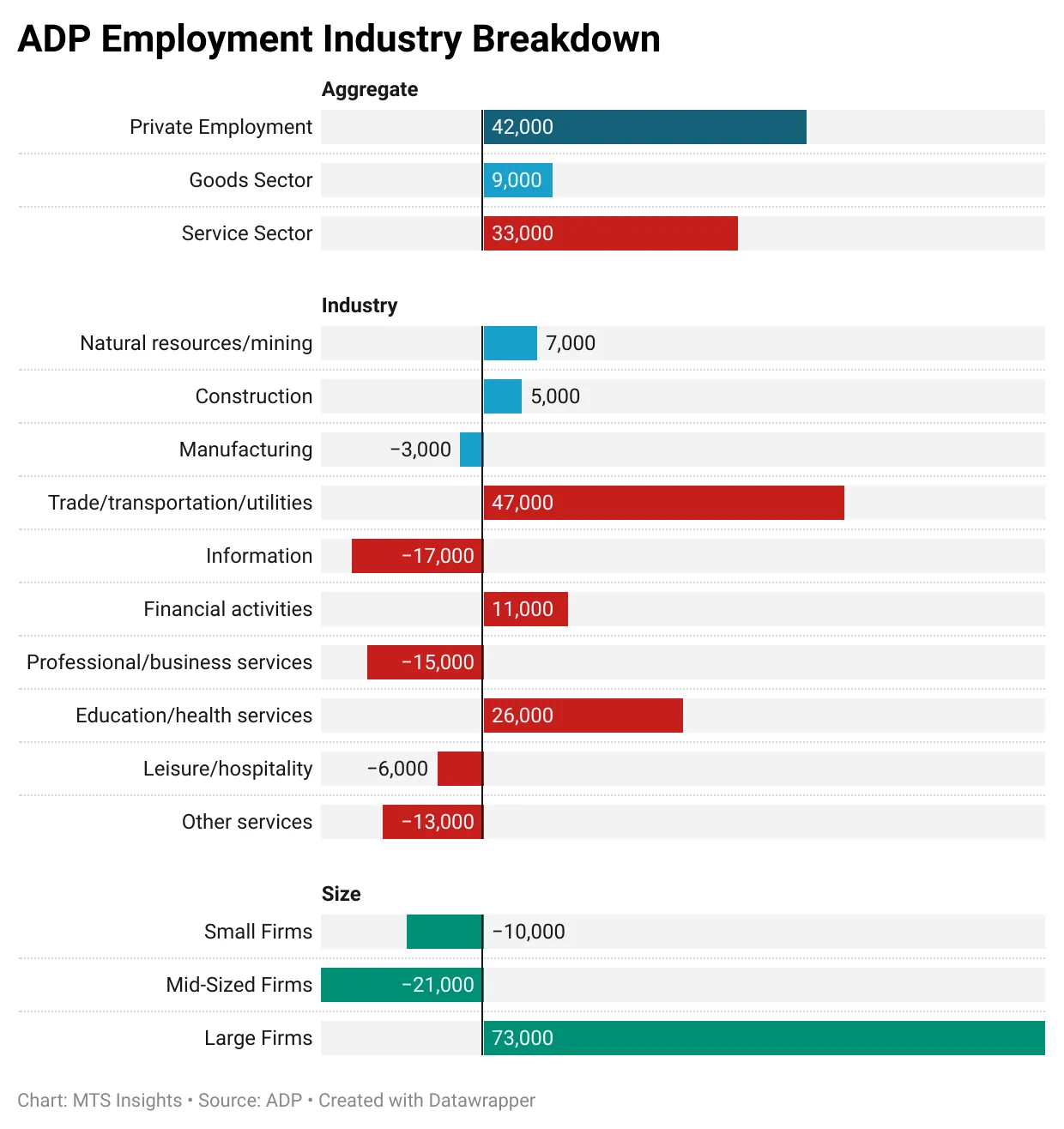

The ADP National Employment Report estimates that broad private sector employment increased by 42,000 in October, beating expectations of a 25,000 increase and pointing to a rebound in hiring after weak readings in August and September. Additionally, the drop in employment in September was revised up slightly by about 3,000 to -29,000, a positive development mostly in that there wasn’t a major downward revision (which has been a feature of recent BLS reports). Most notably, the momentum from employment growth has clearly fallen away. The 3-month moving average has fallen further to just 3,300 from around 20,000 to 30,000 over the summer.

The private sector job gains continue to be fueled by strength in the service sector, while the goods sector sees little to no employment growth. In October, the service sector added 33,000 jobs, while the remaining increase of 9,000 was seen in the goods sector. The individual industries that stood out were trade, transport & utilities (+47,000), education & health services (+26,000), and finance (+11,000). There continues to be a softening in the business services and information industries, which may be a result of trends in AI innovation. Business services, specifically, has seen a -28,000 drop in employment in just the last two months. Another result worth mentioning is another small decline in manufacturing of -3,000 in October, after a -2,000 decline in September, suggesting that tariffs have still not provided a boost to manufacturing employment in the few months they have been implemented.

The segmentation of the employment gains by firm size was also very interesting in October. Large firms with 500 or more employees accounted for all of the employment growth during the month, adding 73,000. This increase was offset by declines in small- and medium-sized firms where employment fell -10,000 and -21,000, respectively. A similar trend was evident in the September data, where large firms added 33,000 and small- and mid-sized firms lost -60,000. These recent data points indicate that current economic conditions are disproportionately affecting firms more exposed to cyclical swings, implying that rate cuts could help stabilize labor market conditions.

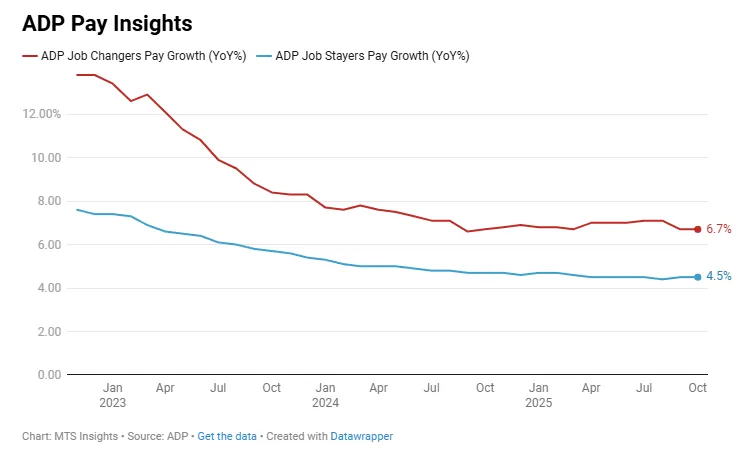

ADP also provides an update on wage growth, but for October, this was less interesting. Specifically, it reported that annual pay growth for employees who changed their jobs and those who stayed at their jobs were both unchanged from the September readings of 6.7% YoY and 4.5% YoY, respectively. In general, wage growth has trended around these levels for the entirety of the year after declining more significantly in 2023 and 2024. The BLS data of average hourly earnings shows a similar trend with wage growth sticky around 3.6-3.8% YoY.

-

Private sector employment fell -32k in September 2025, well below expectations of a 50k increase and the largest decline since March 2023.

-

ADP released revisions that removed 60k jobs from the previous two months: July revised down -2k to +104k, August revised down -57k to -3k.

-

Goods-producing industries lost -3k jobs, as gains in natural resources/mining (+4k) were offset by declines in construction (-5k) and manufacturing (-2k).

-

Service-providing industries shed -28k jobs, with professional/business services (-13k), leisure/hospitality (-19k), and other services (-16k) leading the losses, while education/health services added +33k.

-

By region, the Midwest saw the steepest decline at -63k jobs, while the Northeast added +21k, the West +15k, and the South +3k.

-

Small establishments lost -40k jobs and medium-sized firms -20k, while large firms added +33k, showing resilience among the biggest employers.

-

Job-stayers’ annual pay rose +4.5% YoY, broadly stable, with growth strongest in manufacturing (+4.7%) and large firms (+4.8%).

-

Job-changers saw slower pay growth at +6.6% YoY, down from +7.1% in August, led by softer gains in leisure/hospitality and financial activities.

-

-

Employment

The ADP employment data released today gives us a preview of what private payroll growth might look like tomorrow in the BLS employment situation report. The headline private payroll employment gain, based on ADP’s data, is just 54,000 for August, slower than the 106,000 added in July (revised up from the initial report of 104,000) and below expectations of a gain of 65,000. However, August job gains did outpace the weaker May and June readings which resulted in an increase in the 3-month trend from 37,000 in July to 46,000. So while the number does look soft compared to the forecast and the July gain, August hiring appears to have been more solid than what we saw at the end of Q2.

Job growth was seen in both the goods and services sectors with some divergence across industries.

- The private goods sector added 13,000 jobs, the weakest since the sector saw employment decline in May. Within the sector, an increase of 16,000 construction jobs led the way while natural resources & mining added just 4,000 and manufacturing was down -7,000. It is notable that the construction industry saw another decent month of job gains (+15,000 in July) since it is known as a cyclically sensitive segment of the economy.

- The private services sector added 42,000 jobs, continuing to be the primary source of employment growth in the private sector. However, many services industries reported a weak month, and the overall service sector increase in payrolls was driven by one strong industry. That industry was leisure & hospitality which saw an increase of 50,000 jobs in August, building on strength that it saw earlier in the summer (July: +46,000, June: +32,000). Outside of that industry, smaller gains in information (+7,000) and professional services (+15,000) were offset by declines in trade, transport & utilities (-17,000), education & health (-12,000), and financial activities (-2,000).

Another positive takeaway from the data release this morning is that the growth in private employment was seen across all firm sizes. Mid-sized firms saw the strongest growth at 25,000, but large and small firms were not far behind with gains of 18,000 and 12,000, respectively. Even though it was the weakest, the growth in small business employment is notable because, like construction employment, it is cyclically sensitive. Thus, we don’t have to worry about a leading signal flashing red. Though it is worth noting that small business employment is actually slightly down over the last month since it dropped -47,000 in June, offsetting the 24,000 small business jobs added in August and July.

Pay Growth

The other component of the ADP National Employment Report is ADP’s measures of pay growth. Over the last two years, the measures have been mostly stable and very slightly decreasing. The August data did not show a divergence. Annual pay growth for “job changers” remained unchanged at 7.1%, remaining stubbornly high so far this year. Annual pay growth for “job stayers” ticked down to 4.4%, another signal of a slow deceleration in compensation. It is worth noting that ADP’s pay growth measures are very new, with data only going back to 2020. So it’s hard to tell how these readings compared to pre-pandemic periods. If there is anything to take away from this data, it’s that in the near-term there hasn’t been any major changes in employee compensation which is consistent with the stickiness we have seen in the BLS’s average hourly earnings data.

-

According to ADP, US private sector employment increased by 104k in July 2025, with services leading the gains.

- Goods-producing jobs rose +31k, including +15k in construction, +9k in mining, and +7k in manufacturing.

- Service-providing jobs increased +74k, led by leisure/hospitality (+46k) and financial activities (+28k), while education/health services declined -38k.

- By region, the West added +75k jobs, the South +43k, the Midwest +18k, while the Northeast lost -18k.

- Large and medium-sized firms each added +46k jobs; small businesses added just +12k.

- Job-stayer pay rose 4.4% YoY, while job-changer pay was up 7.0% YoY, both unchanged from June..

-

US private sector employment declined by -33k (vs 99k expected) in June 2025, the first net job loss in over a year, driven by large declines in professional/business services and education/health, despite gains in manufacturing and leisure/hospitality.

- Goods-producing jobs rose by +32k, with manufacturing up +15k, construction +9k, and mining +8k.

- Service-providing sectors shed -66k jobs, including -56k in professional/business services and -52k in education/health; leisure/hospitality added +32k.

- Small firms (-47k) and medium firms (-15k) cut jobs, while large firms (+30k) added workers.

- Regionally, the South added +13k jobs while the Midwest (-24k), West (-20k), and Northeast (-3k) all posted declines.

- Job-stayer pay growth eased slightly to 4.4% YoY in June from 4.5% in May, while job-changer pay growth dipped to 6.8% YoY from 7.0%.

-

ADP reports that the private sector added 37,000 jobs in May, the weakest monthly gain since March 2023 and well below April’s revised 60,000 gain.

- Goods-producing jobs declined -2,000, with manufacturing down -3,000 and mining down -5,000.

- Service-providing sectors added 36,000 jobs, led by leisure/hospitality (+38k), but business services (-17k) and education/health (-13k) saw sharp declines.

- Medium-sized firms (50–249 employees) added 51,000 jobs, while small (-13k) and large (-3k) firms shed jobs.

- Regionally, the West added 37k jobs, while the Northeast lost -19k.

- Job-stayer wage growth held steady at 4.5% YoY, while job-changer pay growth was unchanged at 7.0% YoY.

-

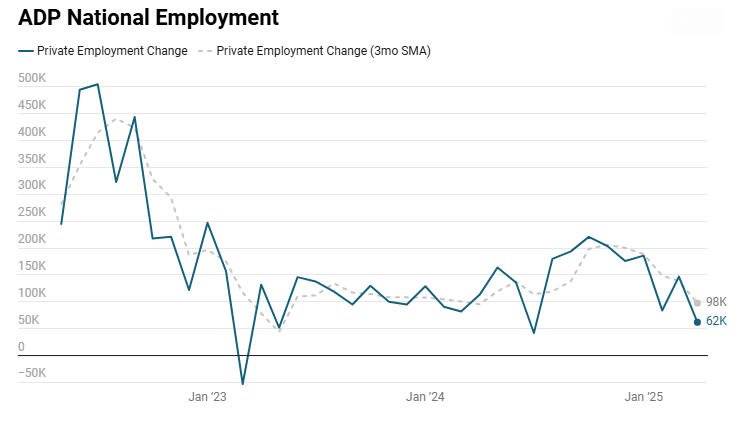

ADP reports that the private sector added 62k jobs in April, below expectations of 108k added.

- The goods and services sector both added jobs, up 26k and 34k, respectively. Leisure & hospitality saw the largest gain at 27k.

- ADP estimates only 4k manufacturing jobs were added in April.

- Small and large businesses added 11k and 12k, respectively. Both trailed the job growth by mid-sized businesses at 40k.

- The March employment gain was revised down -8k to 147k.

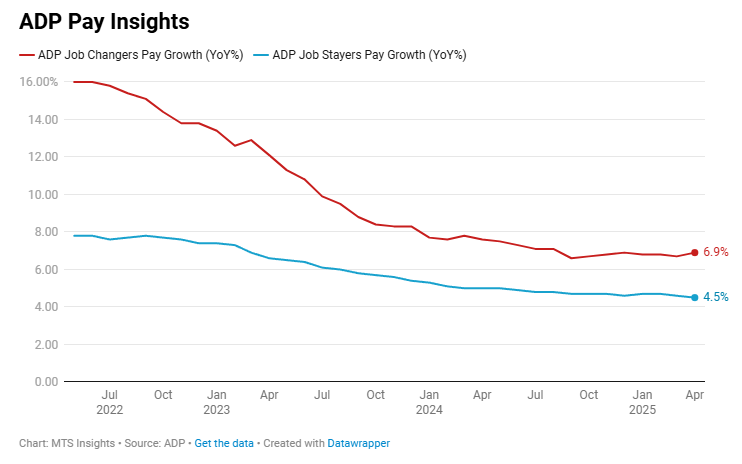

ADP wage growth ticked up for job changers but declined for those staying at their jobs.

- Job changer annual wage growth increased to 6.9% YoY in April, up from 6.7% YoY in March.

- Job stayer annual wage growth eased to 4.5% YoY in April, down from 4.6% YoY in March.