ACCI-Westpac Business Survey

ACCI-Westpac Business Survey

Data

Industry

- Source

- Westpac

- Source Link

- https://www.westpaciq.com.au/

- Frequency

- Quarterly

- Next Release(s)

- March 15th, 2026 8:30 PM

Latest Updates

-

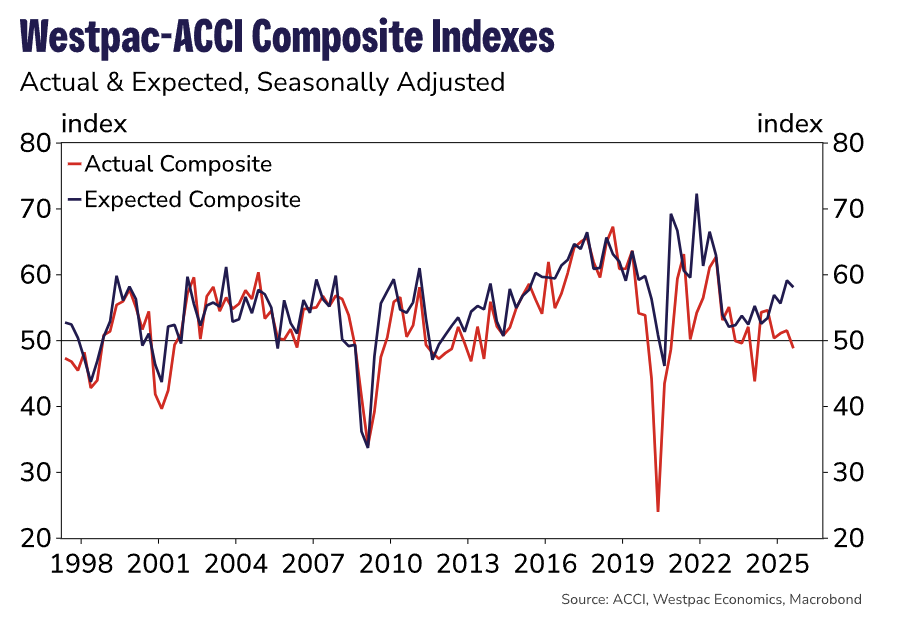

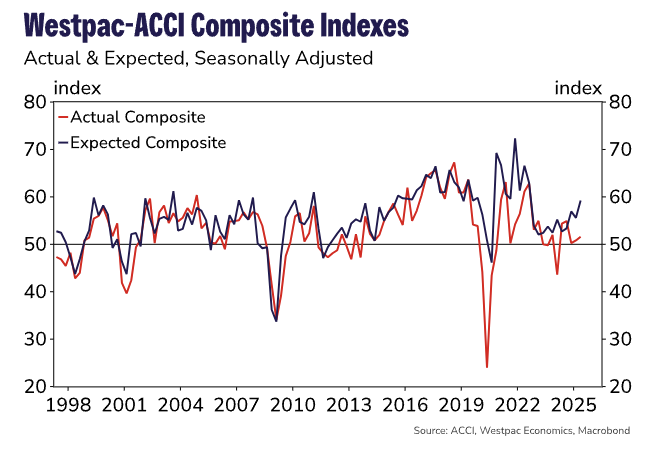

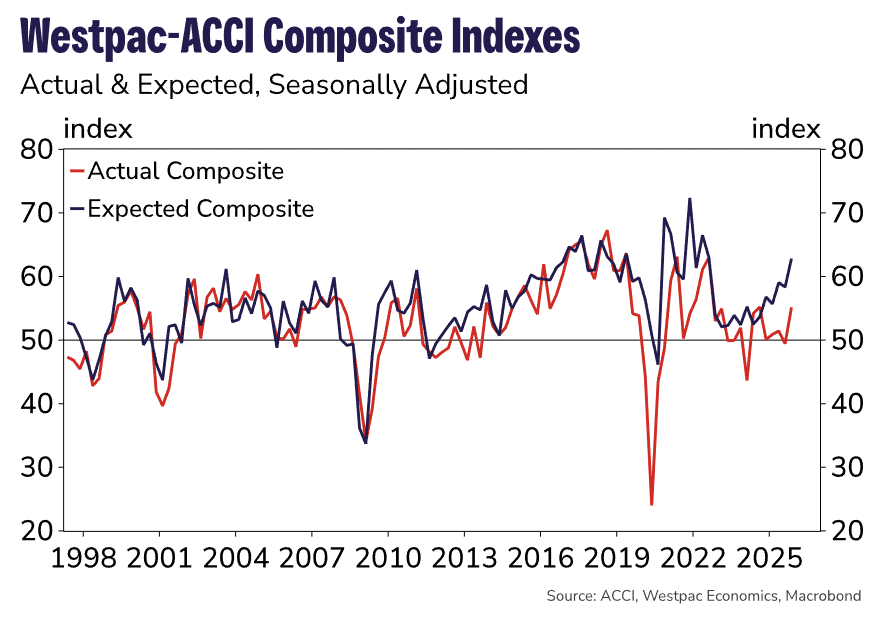

Conditions in the manufacturing sector improved significantly heading into year-end. The Westpac-ACCI Actual Composite moved decisively into positive territory, up from 49.4 in Q3 to 55.1 in Q4, marking the strongest reading since mid-2024. The increase was driven primarily by an expansion in output and a lift in new orders. Employment also rose, albeit more modestly, while overtime usage was unchanged.

- This improvement echoes trends in official data. There is a genuine upswing in consumer spending underway, coming off the back of an improvement in real household disposable incomes. Moreover, there were some early signs of a broader pick-up in investment across the economy.

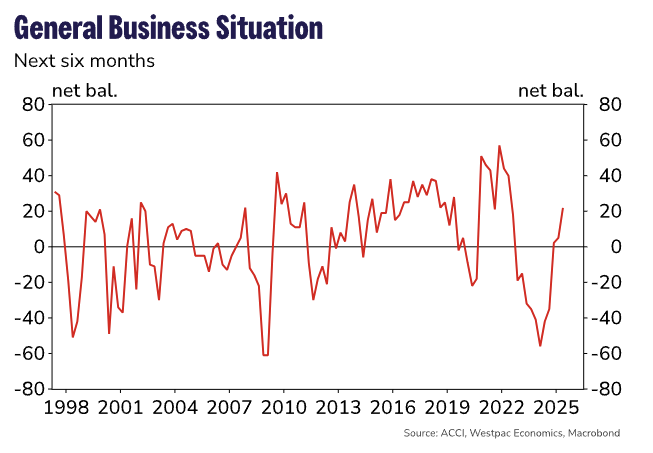

- The latest improvement still fell short of expectations, however, manufacturers remain increasingly optimistic. The Westpac-ACCI Expected Composite climbed to a post-pandemic high of 62.8 in Q4. This optimism is broadly based across production, demand and labour market sub-components, underscoring manufacturers confidence in the current economic upswing.

- Still, there remain some risks. Inflation has recently picked up, and there is some uncertainty over the trajectory for interest rates. How these dynamics unfold and the impact on consumer demand and/or investment, will be key.

- Cost pressures have eased notably since 2022/23, but they remain elevated at around double the pre-pandemic average pace. Against this backdrop, manufacturers are finding there is limited scope to pass on these costs in the form of higher prices. Although profit expectations have improved recently, this appears to reflect a greater degree of confidence over the direction, rather than magnitude.

- The increase in headcount in Q4 marks a tentative shift from the moderate job shedding environment over the past two years. However, the availability of skilled labour remains a pressing issue, with a net 22.4% of manufacturers indicating that labour was "harder to find" now versus six months ago. Additionally, 24% of respondents cited labour as the single factor most limiting production – continuing one of the longest stretches of acute labour shortages in the survey's rich history dating back to the 1960s.

- Capacity utilisation bounded higher in Q4, supported by firmer new orders and output and a modest lift in employment. There is a risk that labour unavailability, together with material shortages, keeps capacity relatively tight for longer, hampering firms' ability to meet demand in full.

- Firms still expect to expand investment and capacity. A net 26% of respondents indicated they intend to increase plant and equipment investment over the coming year, while a net 12% intend to lift building investment.

-

ACCI-Westpac Business Survey: Q1 2025

-

ACCI-Westpac Business Survey: Q4 2024